Credo Earnings Report Analysis: High Growth Can't Mask Underlying Concerns, Why is the Market so Picky?

Author | Eric

Credo focuses on high-speed Ethernet connectivity technology, with core products including Active Electrical Cables (AEC), Line Card Retimers, Optical DSPs, and SerDes IP licensing, among which AEC is the primary revenue source, experiencing rapid growth driven by the demand for high-speed interconnects in AI data center GPU clusters.

Global AEC giant $Credo Technology (CRDO.US)$ released its FY26Q3 earnings report after market close, with its post-market share price dropping over 8%. Logically, Credo's explosive results this quarter should have sparked a rally among bulls, but the market did not respond positively. Let us take a closer look at why.

FY26Q3 Core Financial Metrics

This quarter, Credo delivered another record-breaking performance:

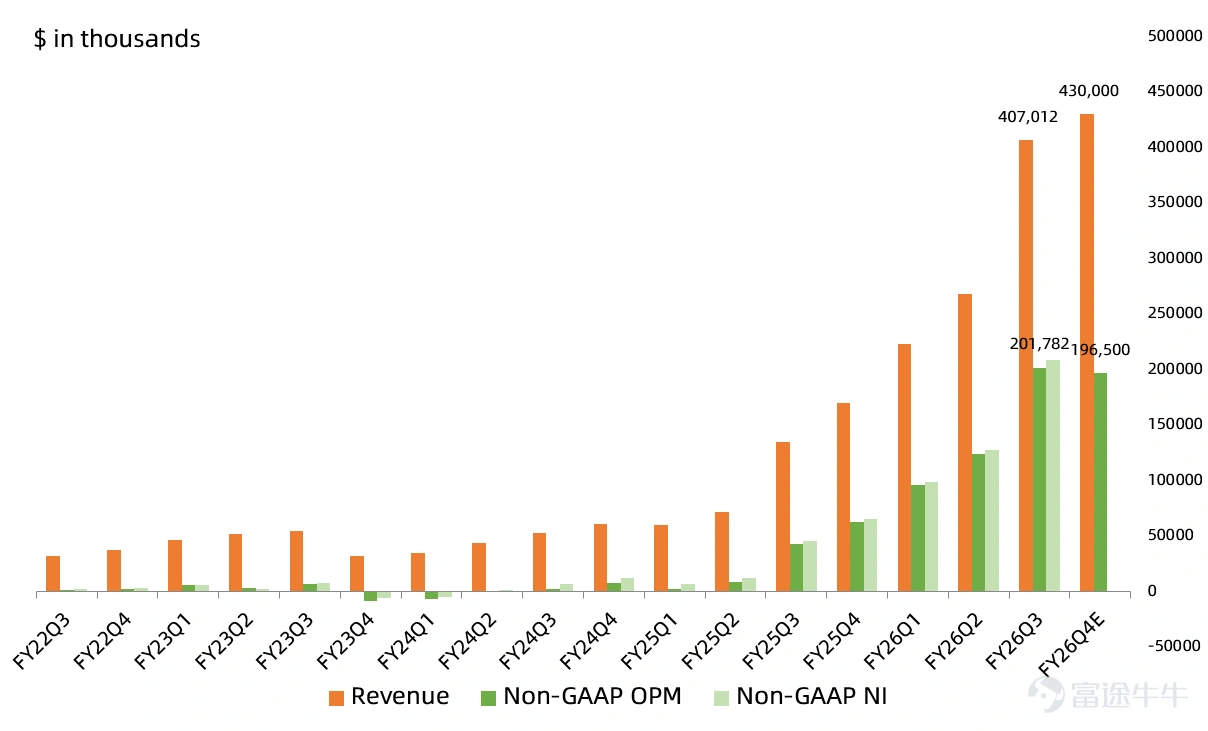

- Revenue407 million US dollars, growing by202%, marking a 52% increase quarter-over-quarter.

- GAAP gross margin68.5%, representing a year-over-year increase of 4.9 percentage points and a quarter-over-quarter rise of 1 percentage point; the Non-GAAP gross margin reached68.6%, increasing by 4.8 percentage points year-over-year and 0.9 percentage points quarter-over-quarter.

- Non-GAAP net profit209 million US dollars, growing by360%, marking a quarter-on-quarter growth of63%. The Non-GAAP net profit margin surged to51.3%, an exceptional level of profitability for a company maintaining triple-digit growth rates, which is quite rare.

Cash flow performance remained robust. Operating cash flow for this quarter was 166 million US dollars, with free cash flow at 140 million US dollars. Cash and equivalents at the end of the period amounted to approximately 1.3 billion US dollars, reflecting a quarter-over-quarter increase of 488 million US dollars, mainly driven by ATM financing and contributions from free cash flow. Inventory levels rose to 208 million US dollars, up by 57.8 million US dollars quarter-over-quarter.

Three key highlights of the earnings report

Guidance on gross margin decline 'spooked' the market

Although the Non-GAAP gross margin for this quarter is approaching69%, the company's guidance for Q4 has dropped back to the range of 64% to 66%, with GAAP gross margin guidance at 63.9% to 65.9%. Compared to the recently reported figure of 68.6%, this downward adjustment cannot be ignored. The market typically reacts sensitively to such signals indicating a peak in gross margins, even though revenue remains strong.

The CFO clearly stated during the conference call that this was due to changes in product mix and conservative forecasting, emphasizing that gross margin expansion will not follow a linear path,and will remain in the range of 63% to 65% over the long term.。

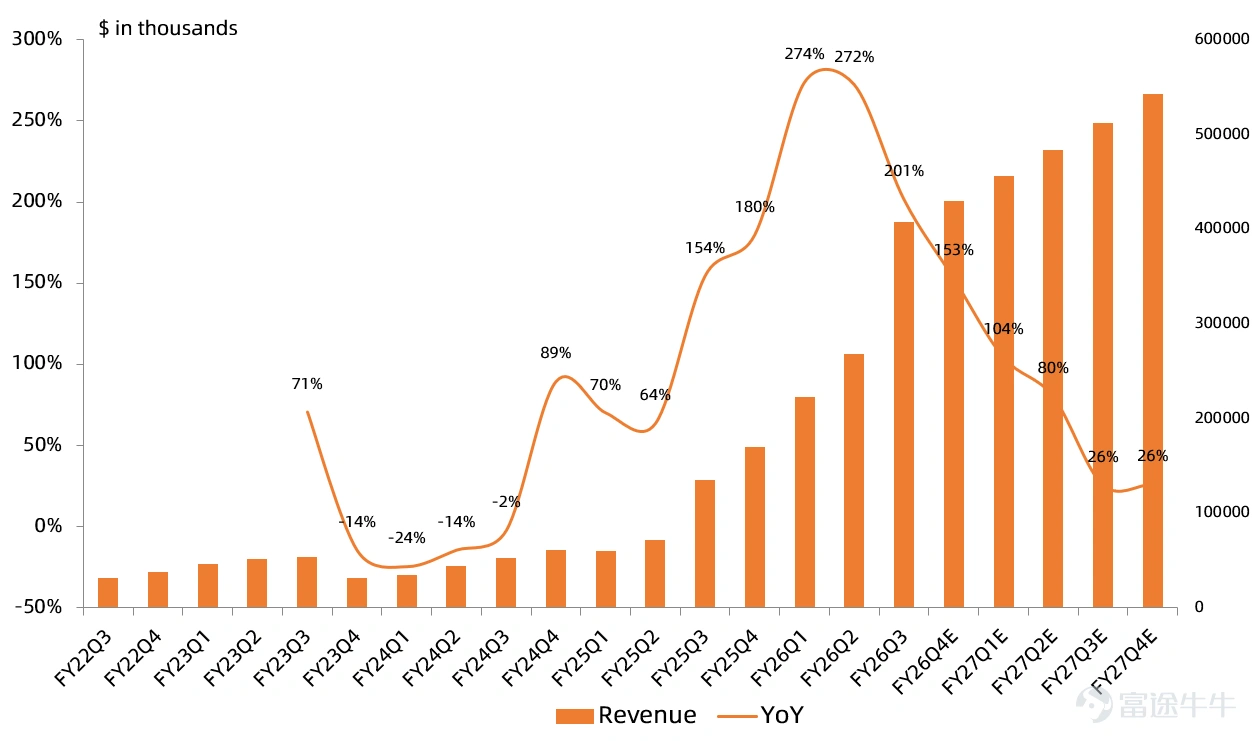

The sequential quarterly revenue growth rate for FY27 is expected to slow down significantly.

Regarding next quarter's guidance, Credo forecastsrevenue to be between $425 million and $435 million,with a Non-GAAP gross margin of64% to 66%,and Non-GAAP operating expenses between $76 million and $80 million. If calculated using the midpoint of the range, revenue would be $430 million, representing a year-over-year increase of 153%.However, the month-on-month growth rate slowed significantly to 6%, which is also a point of concern for the market. GAAP operating profit was $152 million, a year-over-year increase of 349%, with an operating margin of 35.2%, declining quarter-on-quarter. Non-GAAP operating profit was $197 million, a year-over-year increase of 214%, with an operating margin of 45.7%, also declining quarter-on-quarter.

Looking at the longer-term outlook,management indicated that quarterly revenue will maintain a mid-single-digit quarter-on-quarter growth, and FY2027 revenue year-over-year growth will exceed50%, with particular emphasis on the ramp-up of new products like PCIe Gen 6 AEC, and the production timeline for ZeroFlap optical modules being moved forward to FY2027.

However, upon closer examination, it becomes evident that the year-over-year revenue growth rate in FY27H2 will slow sharply to 20%+,Based on the average Non-GAAP net profit margin of 45% over the past four quarters,FY27 Non-GAAP net profit is projected to be approximately $900 million.

The top three customers account for a high concentration of 88%. Management expects future customer diversification.

The revenue contribution from the top three clients in this earnings report reached 39%, 32%, and 17%, respectively, collectively accounting for88%. This structure makes the financial model appear quite fragile, even if the clients themselves are in good condition. In this context, a single client's inventory adjustment cycle or project timeline shift could be enough to sway the entire quarter's performance.

Although managementexpects that in the coming quarters, there will be 3 to 4 clients contributing over 10% each,while also actively expanding into hyperscale cloud service providers and neocloud clients. Investors recognize these diversification efforts but are still aware of the current reality: excessive concentration remains a core risk factor.

Summary

This is a classic case of an earnings report surpassing expectations, yet the stock price remains under pressure due tothe market’s focus being on long-term revenue and gross margin trends—current figures alone are no longer sufficient to meet market expectations.

From an industry perspective, as long as $Credo Technology (CRDO.US)$ demand in the AI interconnect space remains so tight, this broadly supports GPU-driven AI platforms, as well as capacity building by cloud providers and neocloud companies, since increasing computing power always requires more high-speed connectivity solutions as support.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment

9

21