In Collaboration with Amazon! OpenAI Ecosystem Expansion Continues

Taking the Baton from NVIDIA: Broadcom’s Earnings Report in a Zero-Tolerance Moment?

Author | Eric

Global leader in AI ASIC chips $Broadcom (AVGO.US)$ will release its FY2026Q1 earnings report after the market closes on Wednesday. The market is primarily focused on $Alphabet-C (GOOG.US)$ the ramp-up pace of TPU and other vendors' ASIC orders, as well as their impact on gross margins, while also expecting further upward revisions to AI backlog data.

Consensus expectations for core financial metrics in FY26Q1:

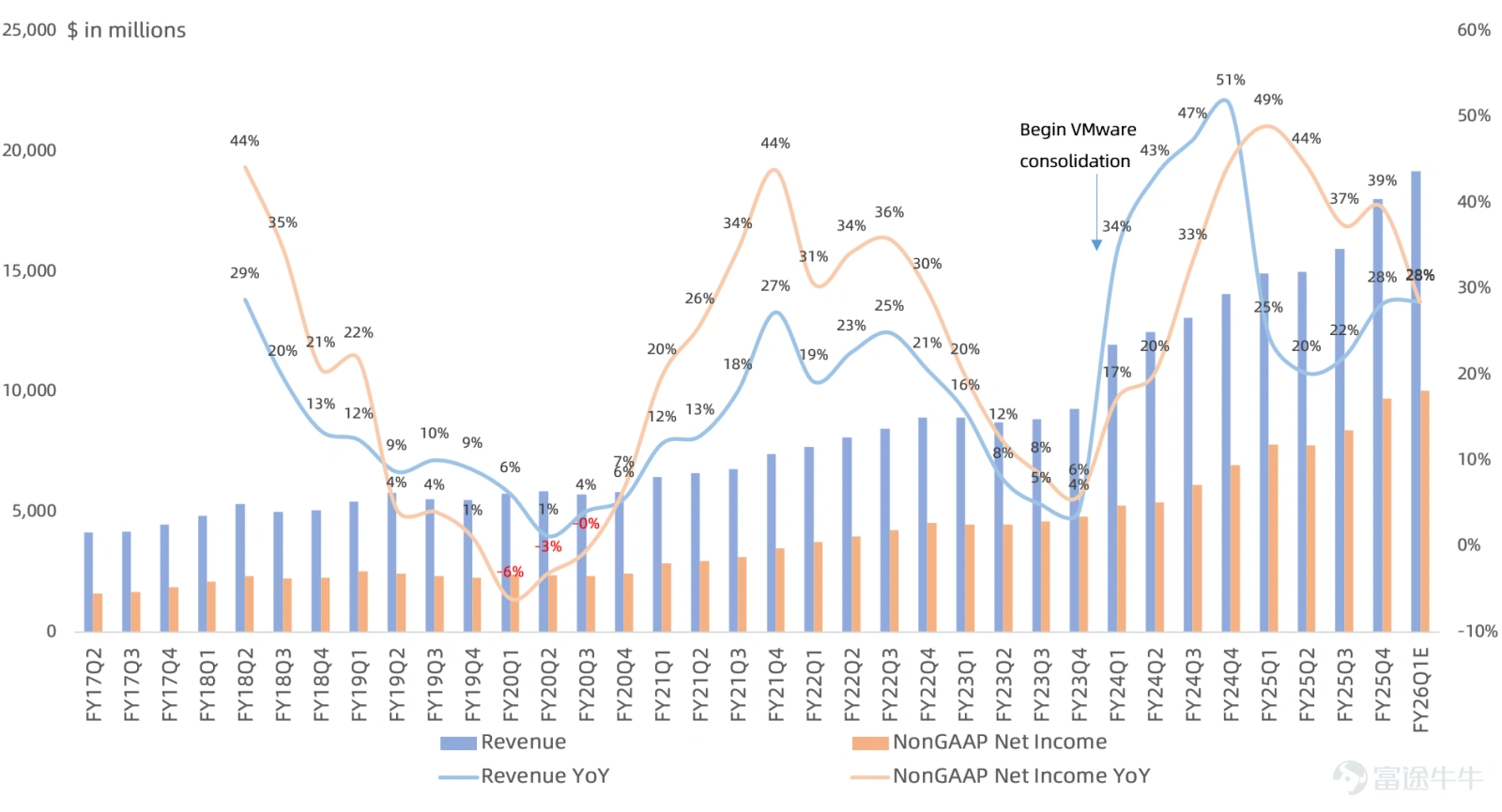

– Market consensus for revenue isUSD 19.17 billion, growing by29%, representing a 6% increase quarter-over-quarter, compared to the previous guidance of USD 19.1 billion.

– Market consensus for GAAP gross margin is67.3%, down 0.7 percentage points year-over-year and down 0.7 percentage points quarter-over-quarter.

– Market consensus for GAAP operating profit isUSD 8.3 billion, growing by79%, reflecting an 11% increase quarter-over-quarter. Market consensus for Non-GAAP operating profit isUSD 12.61 billion, growing by28%, up 6% quarter-over-quarter.

– The consensus GAAP net profit forecast isUSD 7.05 billion, growing by28%, representing a 17% decline quarter-over-quarter. The consensus Non-GAAP net profit forecast isUSD 10.05 billion, growing by28%, reflecting a 3% increase quarter-over-quarter.

The three key highlights of the FY26 Q1 earnings report are:

1. Will AI-related backlog orders be further revised upward?

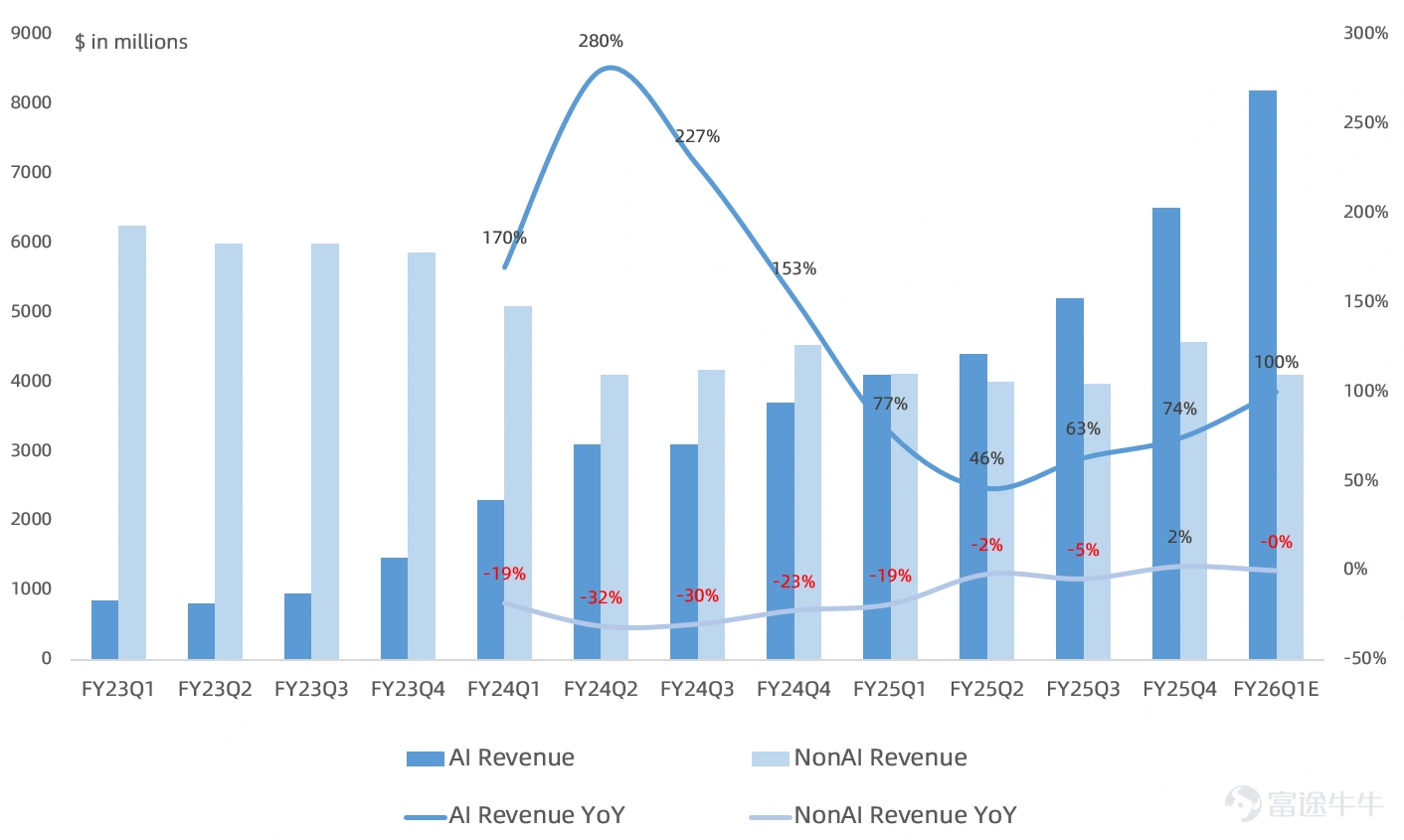

Market expectations for this quarter's Broadcom semiconductor revenue areUSD 12.3 billion, growing by50%, including AI-driven revenue$8.2 billion, year-over-yearDoubling Growth, non-AI revenue was $4.1 billion, slightly down year-over-year.

Last quarter, Broadcom indicated that AI-related (XPUs, switches, DSPs, optical components, etc.) backlog currently exceeds$73 billion, accounting for nearly half of the company's total backlog ($162 billion). This $73 billion is expected to be delivered within the next 18 months.

Among this, the XPU backlog is approximately $53 billion, AI networking business around $10 billion, with record bookings for the Tomahawk 6 switch (102T), and other AI businesses totaling about $10 billion. The non-AI semiconductor business backlog stands at $16 billion.

Notably, management at the time stated that the $73 billion can be viewed as the minimum revenue expectation for AI business over the next six quarters,Last quarter, the market was not satisfied with the $73 billion order scale; attention will be on whether this figure is revised upward in this earnings report.

2. Will gross margins face further pressure as ASIC volumes increase?

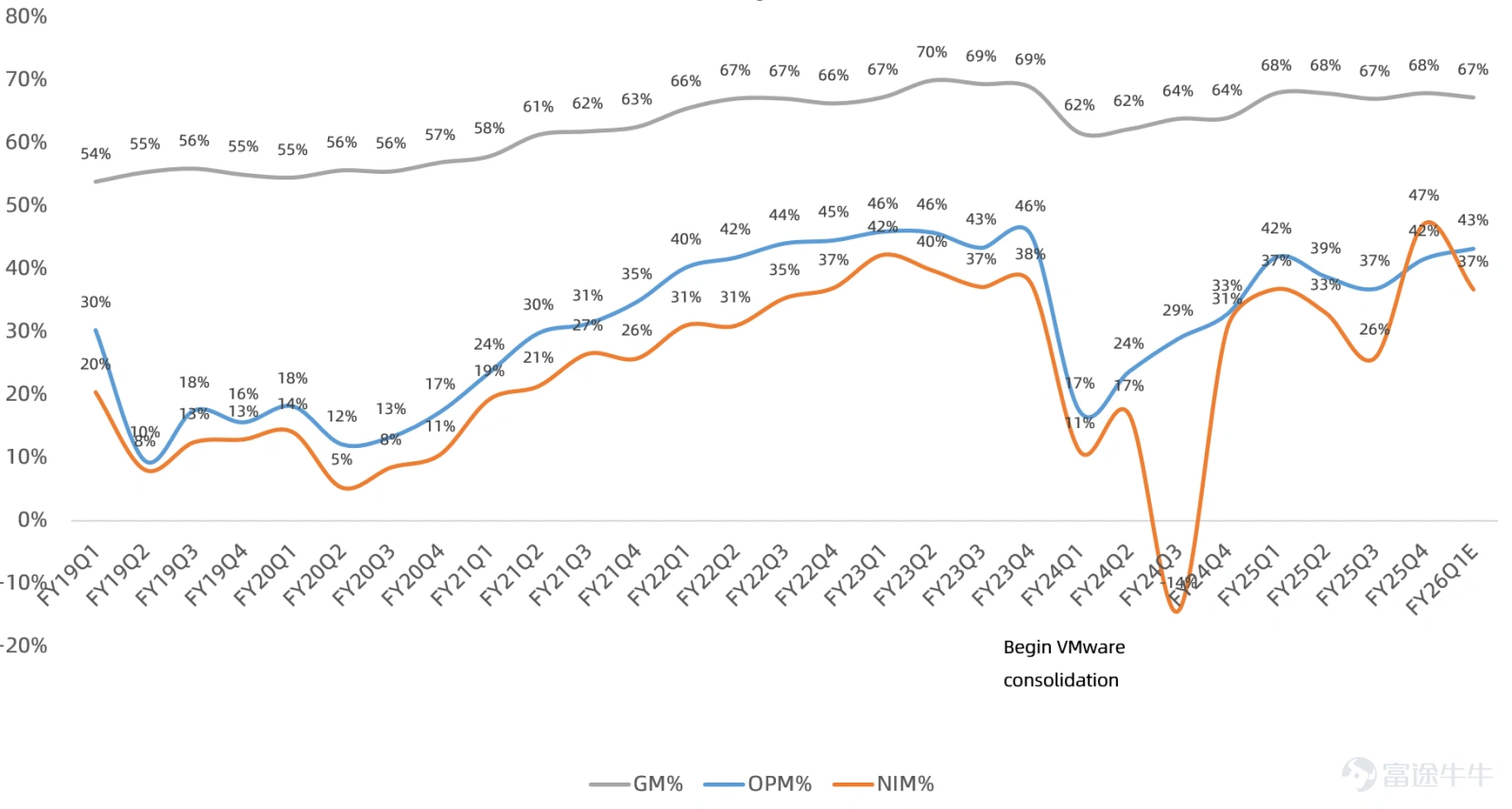

Management noted last quarter that with the increasing proportion of AI revenue,The gross margin will definitely decline in the future, and the operating margin may also fall, which to some extent led to the sharp drop in stock price after the last earnings report. The market is concerned about its continued slowdown in gross margin, especially shipments in cabinet form could further drag down the gross margin.

However, it is worth noting that although the gross margin is declining, the operating margin is increasing, mainly due to the ASIC business model. The low gross margin of ASICs is primarily because the memory components need to be externally sourced, making them uncontrollable, while the logic portion maintains a normal gross margin. However, since R&D and Opex costs are shared with customers, the overall operating margin remains decent.

3. The software business, which is the profit pillar, is showing short-term weakness and may face pressure from large AI models in the long term

Last quarter, Broadcom's infrastructure software businesses represented by VMware, Symantec, CA, and Brocade reported revenue ofUSD 6.9 billion, growing by19%, up 2% sequentially, accounting for39%However, it is worth noting that the overall gross profit margin of the software business is as high as93%Operating profit margin78%. Notably, the overall gross margin of the software business is extremely high at , compared with Broadcom's semiconductor business gross margin of 68% and operating margin of 59%. The recent AI-driven logic impacting U.S. software stocks has also affected Broadcom,What's more alarming is that the software business contributes nearly half of Broadcom’s profits.

Last quarter, management provided guidance that software revenue for the fiscal year 2026 will remainat a low double-digit growth rate. Q1 is the off-season for renewals; focus on management's long-term outlook for the software business this quarter.

Summary

In summary, $Broadcom (AVGO.US)$ As the world's second-largest AI chip company in the semiconductor industry, with AI computing power chips in severe short supply, there is ample growth potential for both ASIC and GPU solutions.

However, last week's earnings report, which exceeded expectations across the board, $NVIDIA (NVDA.US)$ led to a sharp decline in stock price, somewhat dampening sentiment for semiconductor AI chips. The market will also have very low tolerance for errors in Broadcom’s upcoming earnings report, especially considering Broadcom’s current growth rate lags behind NVIDIA’s and its valuation is nearly twice as expensive as NVIDIA’s.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

2

13