NVIDIA's Q4 earnings report was impressive, but why is the market not responding positively?

NVIDIA Earnings Preview: Can the GB300 Volume Surge and Rubin Acceleration Crush the AI Bubble Argument?

Author | Eric

The global leader in AI chips, NVIDIA $NVIDIA (NVDA.US)$ is set to release its FY26Q4 earnings report after the market closes on February 25 Eastern Time. Particularly amid the current market debate over 'AI capital expenditure bubble theory,' this report is highly anticipated. The key focus will be on the ramp-up pace of GB300, the mass production progress of Vera Rubin, and whether the company can provide strong growth guidance for the next quarter.

Market consensus expectations for key financial metrics in FY26Q4:

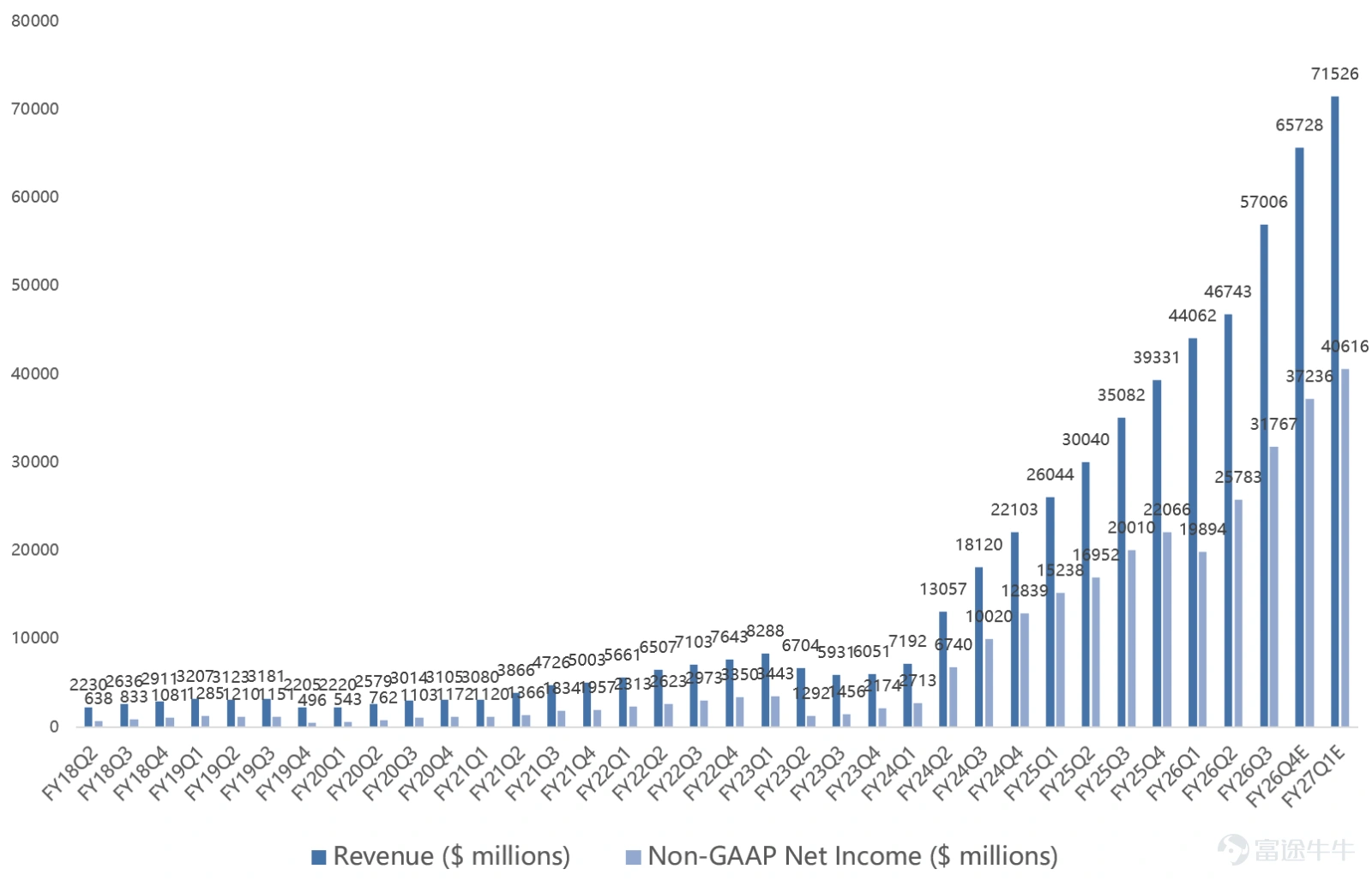

- Revenue consensus estimate$65.73 billion, growing by67%, an increase of 15% from the previous quarter, compared to prior guidance of $65 billion.

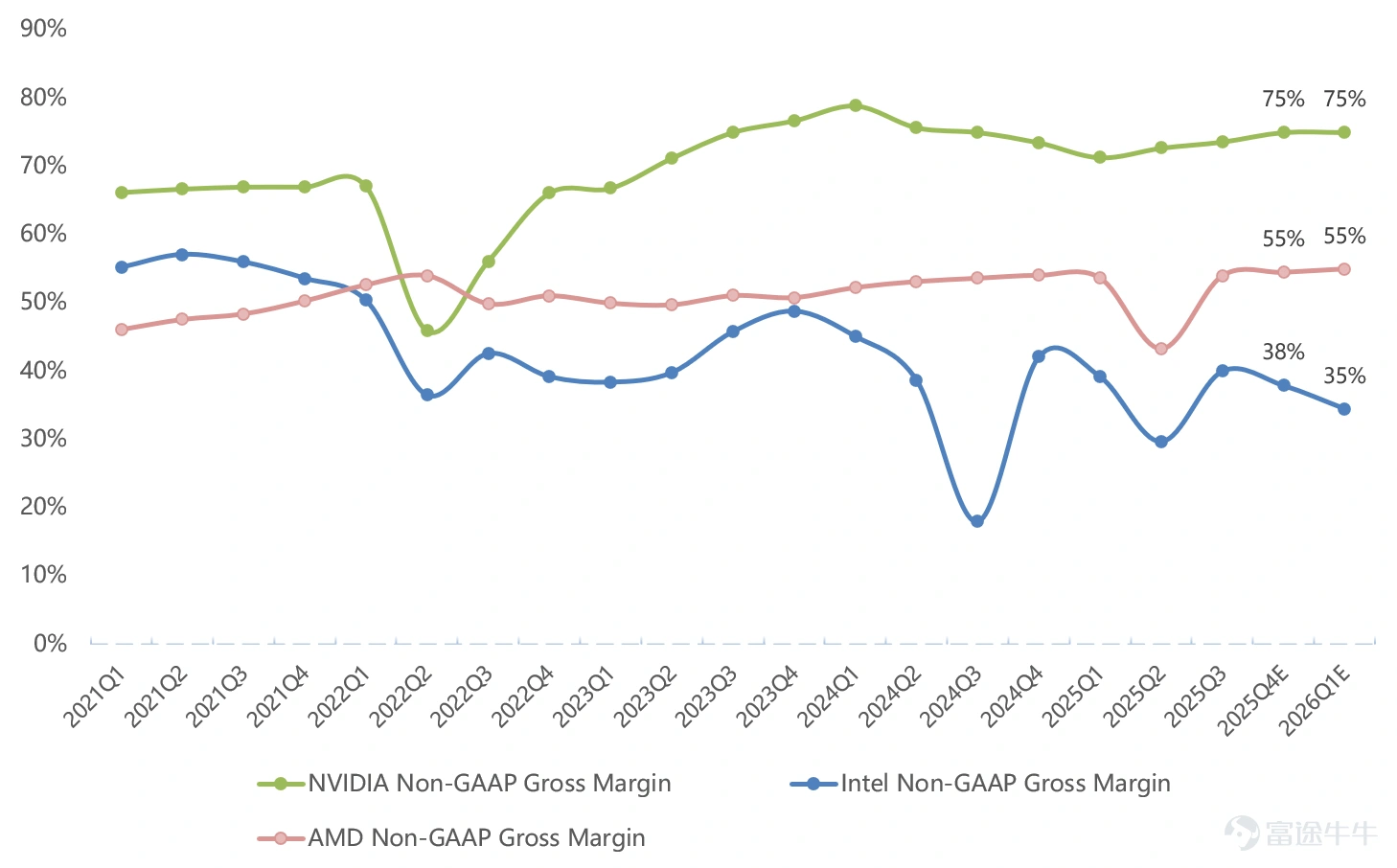

– Consensus GAAP gross margin expectations74.8%, up 1.8 percentage points year-over-year and 1.4 percentage points quarter-over-quarter, with prior guidance at 74.8%; Consensus expectation for Non-GAAP gross margin75%, up 1.5 percentage points year-over-year and 1.4 percentage points quarter-over-quarter, with the previous guidance also at 75%.

- GAAP net profit36.2 billion US dollars, growing by64%, a 13% increase quarter-over-quarter, with previous guidance at 352.1 billion USD; Non-GAAP net profit37.24 billion US dollars, growing by69%, up 17% quarter-over-quarter, with previous guidance at 367.3 billion USD.

Three core focus areas of this earnings report:

1. What is the ramp-up pace for GB300 and the mass production schedule for Vera Rubin?

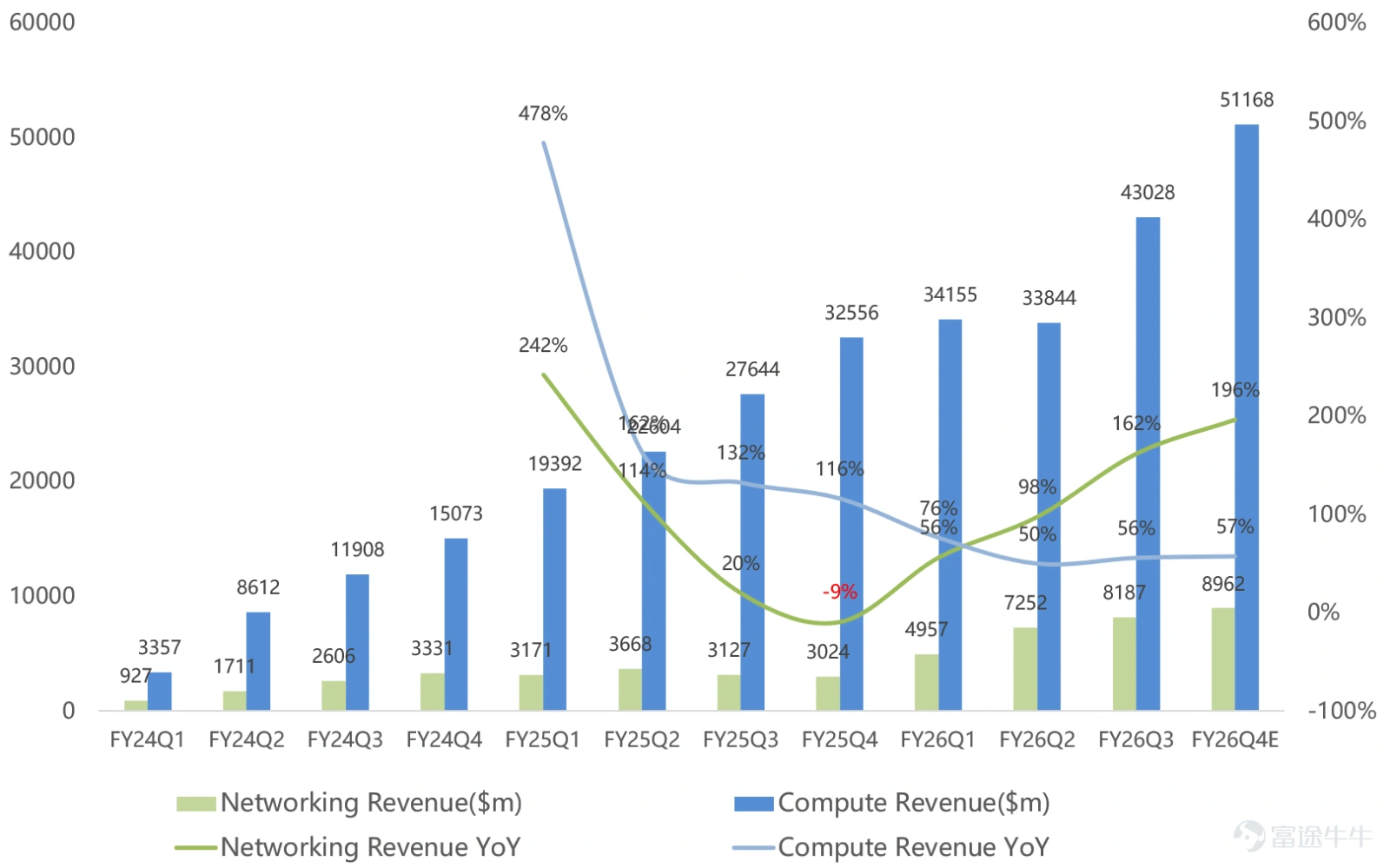

In recent years, thanks to the rapid development of AI, NVIDIA's core business has shifted completely from gaming to data centers. The market expects NVIDIA’s data center revenue this quarter to reach59.8 billion US dollars, growing by68%, up 17% quarter-over-quarter, while gaming revenue is onlyUSD 4 billion, a mere fraction of the data center business.

NVIDIA divides its data center operations into compute and networking segments. Since the large-scale shipments of the GB200 cabinets began in FY26Q1, both compute and networking revenues have grown in tandem, with accelerated volume increases. NVIDIA’s NVLink scale-up, SpectrumX Ethernet, and QuantumX InfiniBand all achieved high double-digit growth last quarter. The latest cabinet, GB300 powered by Blackwell, is just starting to ramp up shipments in FY26Q3,and is expected to drive further acceleration in data center growth this quarter. Management stated last quarter that inventory increased from USD 150 billion in Q2 to USD 198 billion to support the production ramp of GB300.

The market's primary focus for 2026 remains on the mass production schedule of the Vera Rubin series. On the supplier side, SK Hynix showcased the world's first 16-layer 48GB HBM4 product at CES earlier this year, and Samsung recently announced the official shipment of HBM4 to customers, $Micron Technology (MU.US)$ while management also indicated that HBM4 shipments have been moved forward to Q1.These signs may indicate that Vera Rubin's mass production progress is accelerating, awaiting updates from management during this earnings report.

2. The market expects Q1 guidance to show accelerated growth, with net profit targeting the top spot globally

Reviewing NVIDIA’s historical quarterly revenue actuals versus guidance, there is typically a significant gap. However, the current market consensus aligns closely with the guidance deviation,There may be a significant possibility of exceeding expectations.

In addition, considering the explosive guidance recently provided by memory companies ( $Micron Technology (MU.US)$ 、 $SanDisk (SNDK.US)$ 、 $Kioxia Holdings (285A.JP)$ ) and semiconductor ATE equipment companies ( $Advantest (6857.JP)$ 、 $Teradyne (TER.US)$ ), the market also expects NVIDIA to provide strong guidance for next quarter's (FY27Q1) performance.

The current consensus expectation in the market for NVIDIA’s FY27Q1 revenue isUSD 71.53 billion, growing by62%, with Non-GAAP net profit reachingUSD 40.62 billion, growing by, an increase of 104%. This profit level will dominate global Q1 earnings.Therefore, for this quarter's earnings report, the market may focus more on the guidance for the next quarter.

3. How will the increase in memory prices and Vera Rubin ramp-up affect subsequent gross margins?

Due to rising memory prices, not only are companies with large consumer electronics exposure (such as $Qualcomm (QCOM.US)$ ) suffering, but some data center-related companies (such as $Cisco (CSCO.US)$ ) will also see their gross margins eroded. Moreover, new capacity from the DRAM trio is not expected to be released on a large scale until 2027, leading the market to worry about whether the rise in memory prices could impact NVIDIA's subsequent gross margin.

Previously, throughout FY25, the market continuously criticized NVIDIA for its declining gross margin, primarily due to challenges encountered during the Blackwell cabinet ramp-up, which lasted an entire year. This year, seven chips of the Rubin platform are expected to ship by FY27 Q3. The market is looking forward to management’s response regarding the extent to which Vera Rubin cabinet ramp-up might affect the full-year FY27 gross margin compared to the last occurrence.

Summary

Overall, NVIDIA, which has been plagued by various factors such as 'H200 export bans,' 'self-developed alternatives,' and 'major short-selling,' can only keep proving itself through financial reports time and again. This year’s performance mainly hinges on the volume growth of GB300 and Vera Rubin, while H200 exports to China and short-term fluctuations in gross margin are just noise.The production timeline for Vera Rubin will determine whether revenue can exceed the strong guidance of $500 billion seen in the past two years.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (3)

to post a comment

22

30