Trump to launch trade investigation, another tariff war on the way?

Dellin Weekly Observation (February 23, 2026)

US Tariff Changes

The US Federal Supreme Court ruled that President Trump's use of the International Emergency Economic Powers Act (IEEPA) to impose global tariffs was an overreach, rendering the 'reciprocal tariffs' and 'fentanyl tariffs' that relied on this legal basis invalid. Trump immediately signed an executive order that night, for the first time invoking Section 122 of the 1974 Trade Act to impose a 10% temporary tariff on global trading partners; within 24 hours, Trump further announced an increase in the rate to 15%, even declaring plans to issue new legally compliant tariff measures in the coming months. This temporary tariff is valid for only 150 days, and any extension will require approval from the US Congress.

Data released by the US Department of Commerce showed that the core Personal Consumption Expenditures Price Index (PCE) in December rose by 0.4%, marking the largest increase in nearly a year. The core PCE increased by 3% year-over-year, compared to 2.8% at the beginning of 2025. The closely watched super-core personal consumption expenditure rose by 0.3% month-over-month and 3.3% year-over-year, roughly in line with the same period last year. Real personal consumption expenditures in December increased by 0.1% month-over-month, compared to a previous value of 0.3%. The savings rate hit a new low since October 2022.

The minutes from the Federal Reserve’s meeting last month showed that the vast majority of participants believed that the downside risks facing the labor market in recent months had eased, while inflation might persist longer than expected. Several participants warned that further easing of policy in an environment of persistently high inflation could be misinterpreted as policymakers no longer being committed to controlling inflation. Some even suggested that if inflation remains elevated, it may be necessary to consider the possibility of raising interest rates.

The Japanese government announced that Japan's nationwide consumer price index (CPI) in January rose by 1.5% year-on-year. The core CPI, which excludes fresh food but includes energy costs, increased by 2% year-on-year, in line with market expectations, slowing from the 2.4% rise in December last year, marking the slowest growth rate in two years. The CPI excluding food and energy in January rose by 2.6% year-on-year, representing the smallest increase in nearly a year.

This week’s economic data shows that US inflation and consumption remain relatively strong. Unless future data significantly deviates from market expectations, we believe the likelihood of the Federal Reserve starting to cut interest rates in the first half of the year is low. On the other hand, despite the ruling against US tariffs being bypassed through alternative means, we still think this will limit the scope for future tariff threats from Trump, suggesting that tariffs faced by Asian countries may have peaked. Although the actual impact is limited, we believe this will reduce the risk premium in emerging markets. In terms of asset allocation, we continue to believe liquidity will support the market, and recommend US stock investors focus on companies with reasonable valuations and strong business performance, while also paying attention to structural opportunities in markets like Europe and Japan.

Government subsidy funds of 62.5 billion yuan are in place.

During the Spring Festival holiday, local governments increased subsidy allocations. Vice Minister of Commerce Sheng Qiuping introduced that the Ministry of Commerce, together with the National Development and Reform Commission and the Ministry of Finance, has allocated the first batch of 62.5 billion yuan in national subsidy funds, which have already reached local commerce departments. During the nine-day Spring Festival holiday, guidance will be provided to increase subsidy disbursement to ensure consumers can claim subsidies according to policy requirements. Additionally, the Ministry of Commerce, Ministry of Finance, and State Taxation Administration recently confirmed a pilot program for prize-winning invoices in 50 cities, with 10 billion yuan in reward subsidies to be distributed during the six-month implementation period. Of this, over 1 billion yuan in bonuses will be issued during the nine-day Spring Festival holiday.

This year coincides with the 'longest Spring Festival holiday in history' combined with the 'take 5 days off, get 15 days off' leave window, leading to explosive growth in both domestic and international tourism markets. Data shows that driven by the long holiday effect, orders for trips lasting more than five days accounted for 59.6%, with an average travel duration of 6.4 days per person. Beijing remains at the top of the most popular cities list, followed by Guangzhou, Shanghai, Harbin, Sanya, Chongqing, Chengdu, Xi'an, Fuzhou, and Kaifeng. While the domestic market is booming, outbound tourism is undergoing significant restructuring. Data indicates that outbound tourism service bookings for Spring Festival 2026 increased by nearly 30% year-on-year, with Malaysia rising to the top spot as the most popular outbound destination.

According to Maoyan Professional Edition data, as of around 6 PM yesterday (January 22), China's total box office revenue for the Spring Festival period this year has exceeded 5 billion yuan, with 'Pegasus 3', 'Awakening of Insects Silent', and 'The Courier: Winds Rise Over the Desert' ranking as the top three films in the 2026 Spring Festival box office.

This week marks the New Year holiday, and amid the anti-internal competition trend, we believe investors can explore opportunities related to the 'happiness economy' concept, focusing on sectors like hotels and airlines that face multi-year favorable cycles. At the same time, we advise investors to closely monitor consumption data during the Spring Festival and post-holiday housing market trends to assess economic recovery. Regarding asset allocation, we caution investors to avoid speculative AI-related stocks and pay attention to undervalued opportunities in cash-rich internet giants.

3 Delin Securities Perspective

Kenty Wong, Deputy CEO of Delin Securities, observed that the Hong Kong stock market was the first to welcome the Year of the Horse last week, but closed lower despite only being open for one and a half trading days due to the extended holiday. With the absence of 'northbound capital,' daily trading volume averaged only about 160 billion. The Hang Seng Index continued to hover around the 26,500-point level, falling 153 points over the week to close at 26,413. Sector-wise, Mainland artificial intelligence (AI) concept stocks were favored, with MINIMAX (0100.HK) and Zhipu (2513.HK), two newly listed stocks within the past two months, seeing frenzied trading last week. Their combined single-day trading volume on Friday exceeded 6.7 billion yuan, mesmerizing investors. Last week's CCTV Spring Festival Gala showcased the strength of Mainland robotics technology, indirectly boosting the recent performance of robot-related stocks.

Looking ahead to this week, it is expected that trading activity will return to active levels once 'northbound capital' returns to the Hong Kong market on Tuesday. Externally, President Trump has further increased import tariffs on global goods from 10% to 15%, which is likely to cause some volatility in global stock markets this week, and the Hong Kong market will not be immune. Investors must proceed with caution.

Revisions to the HKEX's ongoing public float requirements for listed companies, effective January 1 this year, now allow firms to adopt an alternative threshold: a minimum public float of 10% of total issued shares or a public float market value of no less than 1 billion yuan, in addition to the standard 25% requirement. Statistics indicate that at least five Hong Kong-listed companies have switched to the alternative threshold. Following the new rules, companies find it easier to conduct buybacks to support share prices, but there are concerns regarding concentrated ownership risks, as market participants worry whether switching thresholds could affect stock liquidity or lead to concentrated equity issues. However, since the new measures have been implemented for less than two months, it would be prudent to closely monitor market conditions, such as any unusual stock price fluctuations after adopting the alternative threshold, before making further comments.

Key News

Shaanxi Issues Digital Currency Innovation Bond, Accelerating the Implementation of Digital Currency Application Scenarios

According to the Shaanxi Release official account, Shaanxi Province issued its first digital currency innovation bond, amounting to 3 billion yuan. Under the guidance of the People's Bank of China's Shaanxi branch, the Xi'an branch of China Merchants Bank successfully issued the first phase of the 2026 annual innovation bond for a major enterprise in Shaanxi Province, and completed the collection of all funds raised in the form of digital currency, amounting to 3 billion yuan. Industry insiders pointed out that this transaction is not only the first digital currency innovation bond in Shaanxi Province but also a practical application of digital currency in innovative scenarios within direct financing, playing a positive role in improving the digital currency ecosystem and promoting financial market business innovation in Shaanxi Province.

Hong Kong's first batch of stablecoin issuer licenses will be officially issued in March. Legislative Council member Wu Jie Zhuang immediately posted on the X platform suggesting the integration of stablecoins with public fiscal policy by issuing 'nighttime consumption vouchers' to accelerate their adoption. He analyzed that this move could bring multiple benefits: citizens can directly use stablecoins for consumption and experience digital payments while easily setting up e-wallets and gradually becoming familiar with digital assets. At the same time, having compliant stablecoin issuers cover part of the promotional costs helps reduce administrative expenses. In the long run, it will also enhance public awareness of digital assets and reduce fraud cases. This is not only a convenient measure for the public but also an organic combination of public finance and innovative technology.

OpenAI Predicts Revenue to Exceed 2 Trillion by 2030

ChatGPT developer OpenAI expects revenue to climb to over 280 billion USD by 2030, showing the company’s efforts to attract more businesses and users to pay for its AI services to offset expenditures on purchasing chips, building data centers, and attracting talent.

The report noted that OpenAI's revenue last year was 13.1 billion USD, surpassing its target of 10 billion USD, while burning through 8 billion USD during the period, less than the originally estimated 9 billion USD. Currently, ChatGPT has over 900 million weekly active users, up from 800 million at the end of October last year.

Moreover, OpenAI previously committed to investing over 1.4 trillion USD in AI infrastructure in the coming years but now states that related expenditures will amount to only about 600 billion USD by 2030, a reduction of approximately 57%, reportedly aiming to align more directly with expected revenue.

ByteDance Expands AI Division

Despite years of security concerns raised by U.S. lawmakers and regulators, Chinese tech giant ByteDance plans to hire nearly 100 people for its artificial intelligence division in the United States to compete with leading American AI companies.

Related positions are posted on ByteDance's career page and belong to the Seed team, established in 2023. The team currently has labs in the United States, Singapore, and China. According to the job postings, responsibilities cover various duties, including creating international data for ByteDance's large language models, advancing text, image, and video generation tools, conducting human-like AI development research, and building scientific models to assist the company in drug discovery and design.

In 2025, DouBao, under ByteDance, was the most downloaded AI chatbot in China for the majority of the time. During this year's Lunar New Year period, ByteDance also launched its new flagship model, DouBao 2.0, along with the video generation model Seedance 2.0 and the image generation model Seedream 5.0. Reports indicate that ByteDance's Seed team is currently hiring in San Jose, Los Angeles, and Seattle, where TikTok also has large offices. The company announced that ByteDance will initiate the Seed Edge research program, focusing on the development of general intelligence models.

Trump’s global tariffs overturned

US President Trump suffered the biggest courtroom defeat in his second term as the Supreme Court ruled that his core policy tool was illegal. The US Supreme Court ruled that the large-scale tariff measures implemented by the Trump administration under the International Emergency Economic Powers Act (IEEPA) lacked clear legal authorization.

Chief Justice John Roberts, three liberal justices, and two justices appointed by Trump, Neil Gorsuch and Amy Barrett, all supported the ruling. This decision upholds a lower court's original ruling last year that Trump's tariffs were overreaching. Most of the tariffs currently imposed by the Trump administration will be forced to halt, including the so-called 'fentanyl tariffs' and reciprocal tariffs first announced in April 2025.

This ruling triggered a massive tax refund issue. Economists using the University of Pennsylvania’s forecasting model estimated that over $175 billion in tariff revenue is at risk of being refunded. The Congressional Budget Office previously projected that all of Trump’s tariffs would generate about $300 billion annually over the next decade. If $175 billion is fully refunded, it would account for more than half of total tariff revenues.

According to calculations by Yale University’s Budget Lab, the average US tariff rate has risen from 2.5% when Trump took office in January 2025 to nearly 17%, the highest level since 1934. Tariff revenue was previously used to offset tax cuts introduced last year. Now, if the tariff system collapses, it could exacerbate market concerns about the trajectory of US debt.

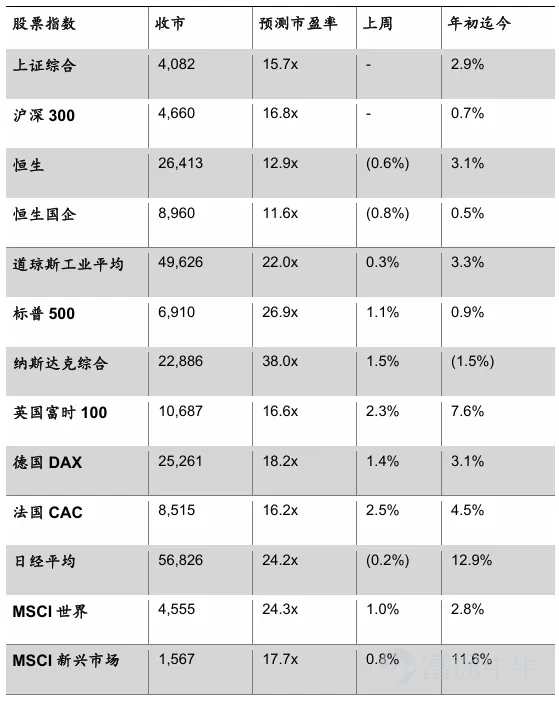

Market statistical information

This week's economic data schedule

Disclaimer

This report was prepared by DL Family Office (Hong Kong) Co., Ltd. based on publicly available information. DL Family Office (Hong Kong) Co., Ltd. is licensed by the Hong Kong Securities and Futures Commission to engage in Type 4 (advising on securities) and Type 9 (asset management) regulated activities.

The content and opinions in this report are for reference only and do not constitute recommendations, offers, solicitations, invitations, advertisements, or promotions for any securities or related financial instruments. While DL Family Office (Hong Kong) Co., Ltd. strives for accuracy and reliability in the information provided, it does not guarantee independent verification of these public sources.

DL Family Office (Hong Kong) Co., Ltd., its branches, affiliates, directors, staff, employees, agents, shall bear no responsibility for any expressions, warranties, implications, correctness, fairness, or completeness contained in this report, nor shall they assume any liability for possible errors, ambiguities, omissions, and any resulting misunderstandings or misinterpretations therein.

This report is distributed exclusively to specific individuals. Without written authorization from DL Family Office (Hong Kong) Co., Ltd., no recipient of this report may copy, distribute, disseminate, quote, republish, or provide all or part of its contents to third parties.

DL Family Office (Hong Kong) Co., Ltd. reserves all rights to this report.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (2)

to post a comment

1