New stock party is in full swing! Around 80% of new listings in 2026 rose on their debut day

IPO Outlook | WiseTech: The Profit Miracle and Cash Flow Concerns Behind Vertical Integration

Recently, WiseTech Co., Ltd. (hereinafter referred to as 'WiseTech') officially submitted its listing application to the Main Board of the Hong Kong Stock Exchange, with CCB International acting as the sole sponsor. This platform-based medical device company, which focuses on disposable endoscopes, has quickly become a focal point in the capital market due to its impressive financial data - a gross profit margin of 72.62% and a net profit margin of 47.26% in 2024, as well as its leading position in the global market. However, behind its high gross profit margin halo, a series of challenges such as excessively high customer concentration, declining cash flow, and intensifying market competition cannot be ignored.

Vertical Integration and Product Advantages Build Moat; Financial Performance Shows 'Structural Differentiation'

The prospectus shows that WiseTech positions itself as a 'platform-based medical device company,' the core of this concept being its unique vertical integration model. The company independently controls the entire process from the independent research, development, and manufacturing of core optoelectronic components and precision parts to the assembly of complete systems, making it one of the few companies globally to successfully achieve vertical integration of the disposable endoscope supply chain.

This vertical integration model brings significant cost advantages and technical control. The prospectus shows that the company's gross profit margin increased from 69.1% in 2023 to 73.7% in the first nine months of 2025, with the continuously climbing profitability partly due to cost optimization brought by supply chain autonomy. Meanwhile, the technical specifications of the company’s products are also highly competitive – developing 'one of the thinnest disposable ureteroscopes in the world' and 'one of the thinnest cystoscopes in the world (with a working channel of 6.6Fr),' these technological innovations are of great significance in minimally invasive surgery, able to reduce patient suffering and lower surgical risks.

In terms of product portfolio, WiseTech has formed a three-brand matrix consisting of its own brand OTU (ONETU®), OTU co-branded products, and WiScope®, covering six major fields: urology, hepatobiliary surgery, respiratory medicine, otolaryngology, gastroenterology, and gynecology. As of the publication date of the prospectus, the company has eight approved product categories in major global markets, with an additional five product categories under development expected to enter the market between 2026 and 2027.

In terms of market position, based on 2024 shipment volumes, WiseTech ranks among the top three brands in the US, European, and Japanese single-use ureteroscope markets. This achievement is particularly remarkable for a Chinese domestic medical device company, especially considering the high technological barriers and strict regulatory environments in Europe, America, and Japan. It reflects the international competitiveness of the company's products.

Notably, WiseTech's financial data reveals distinct characteristics as a leading enterprise in the disposable endoscope field: while revenue growth has been stable, profitability remains exceptionally strong. However, recent growth momentum has shown signs of fatigue, with profits under significant pressure.

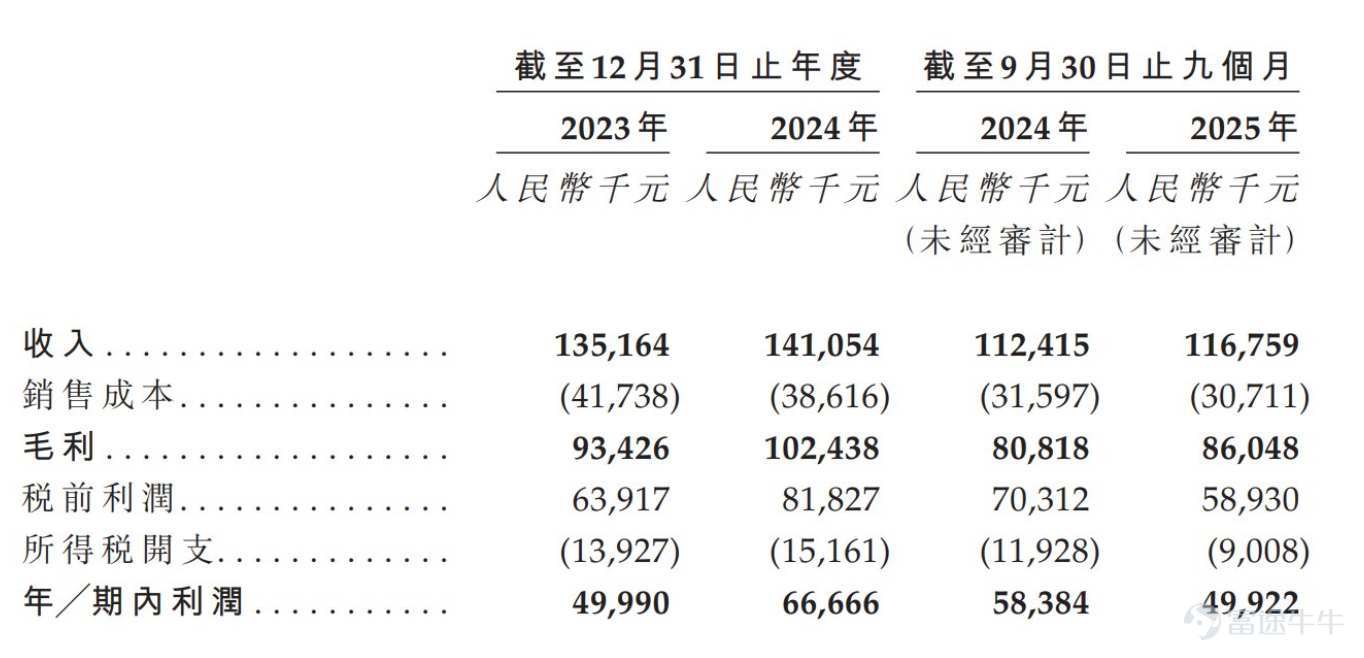

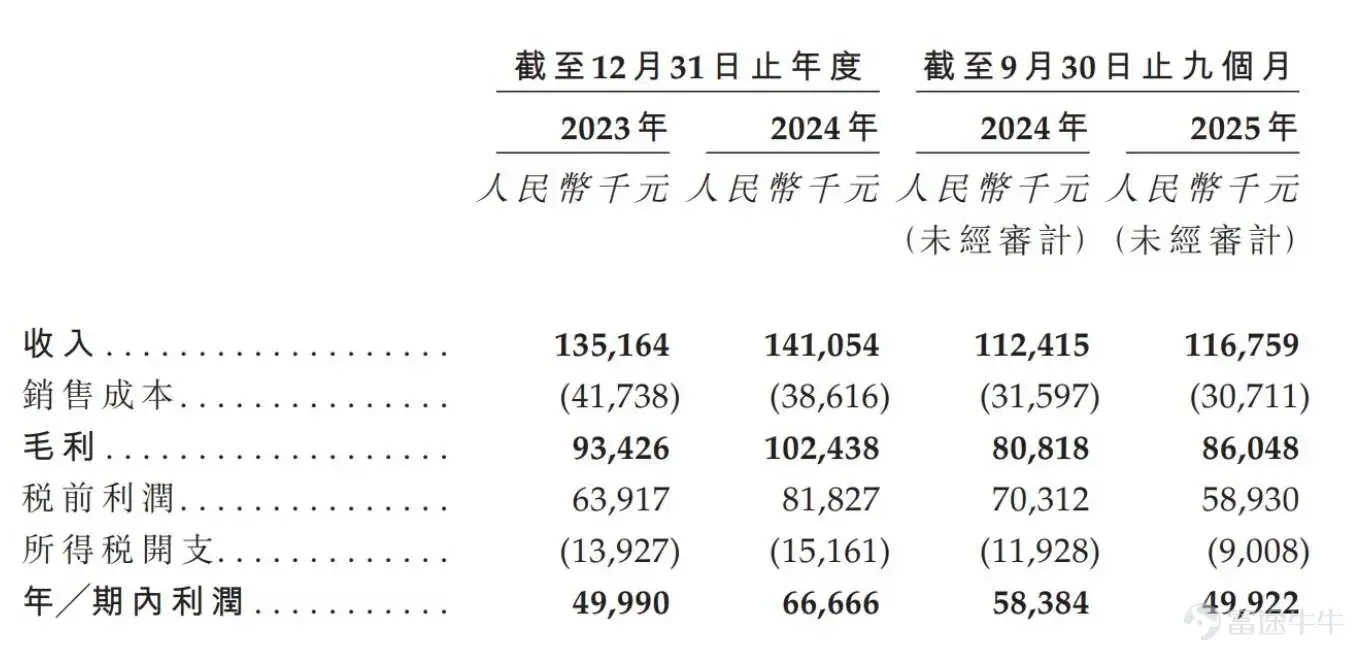

From the perspective of revenue scale, the company achieved full-year revenue of 141 million yuan in 2024, representing a year-over-year increase of approximately 4.4% compared to 135 million yuan in 2023, indicating relatively steady growth. More noteworthy is the performance in the first nine months of 2025: revenue for this period was 117 million yuan, up only 3.86% from 112 million yuan in the same period of 2024, showing no significant acceleration in growth. This suggests that the company’s market expansion and revenue growth may have entered a plateau phase.

However, the company’s profitability metrics are impressive. Gross margin increased significantly from 69.1% in 2023 (gross profit of 934 million yuan / revenue of 1,352 million yuan) to 72.6% in 2024 (gross profit of 1,024 million yuan / revenue of 1,411 million yuan), and further rose to 73.7% in the first nine months of 2025 (gross profit of 860 million yuan / revenue of 1,168 million yuan). This consistently upward gross margin curve strongly supports the company’s claim of cost advantages and technology premium derived from “vertical integration of the supply chain.” The proportion of sales costs to revenue steadily declined from 30.9% in 2023 to 26.3% in the first nine months of 2025, directly driving the improvement in gross profit.

In terms of pre-tax profits, the company reached 81.83 million yuan in 2024, a substantial increase of 28.0% from 63.92 million yuan in 2023, far outpacing revenue growth and highlighting operational leverage. However, this growth trend reversed in the first nine months of 2025: pre-tax profit for the period was 58.93 million yuan, down 16.2% from 70.31 million yuan in the same period of 2024. This directly led to a decline in net profit (net income) from 58.38 million yuan in the same period of 2024 to 49.92 million yuan, representing a drop of 14.5%. Despite a reduction in income tax expenses (from 11.93 million yuan to 9.01 million yuan), it was insufficient to reverse the downward trend in profits.

In summary, WiseTech’s financial performance exhibits a “structural divergence”: on one hand, although revenue growth is moderate, the extremely high and continuously improving gross margin demonstrates the strong market competitiveness and pricing power of its products. On the other hand, the modest revenue increase coupled with double-digit profit declines in the first nine months of 2025 exposes new challenges faced by the company during its growth process. The profit decline may stem from increased sales and marketing expenses in response to heightened market competition, ongoing heavy investment in R&D, and operational efficiency issues (such as rising inventory, prolonged collection cycles leading to higher operating costs). This aligns with the deterioration in operating cash flow disclosed in the prospectus (a year-over-year decrease of 19.45% in the first nine months of 2025). Finally, the net profit margin remained exceptionally high at 47.3% in 2024, and even in the first nine months of 2025 when profits declined, it stayed at a lofty 42.8%. Such a high net profit margin is rare in the medical device industry, reflecting both the success of its business model and potentially becoming a risk factor amid intensifying competition and rising cost pressures.

WiseTech's financial statements portray a company at a critical turning point: it has built a robust profitability moat through technological advantages and vertical integration, but is also facing growing pains transitioning from a “high-margin niche market leader” to a “platform for scalable growth.”

Behind the high growth of the endoscope sector, customer concentration and cash flow challenges remain unresolved.

The disposable endoscope market is at a crucial stage of rapid growth and structural reshaping. Due to its ability to effectively avoid cross-infection risks associated with traditional reusable endoscopes, and significantly reduce hospital cleaning, disinfection, and maintenance costs, it is rapidly becoming a key growth driver in the global medical device industry. Industry forecasts predict that the global market size will expand from approximately $2 billion in 2023 to over $6 billion by 2030, with an annual compound growth rate exceeding 17%, indicating vast market potential.

However, this high-growth sector also exhibits significant competitive barriers and consolidation characteristics. Currently, the international market is dominated by giants such as Ambu, Boston Scientific, and Olympus, which together account for over 40% of the global market share. Among them, Ambu holds approximately 25% of the European market, while Olympus occupies about 35% of the gastrointestinal endoscopy niche. These companies have built strong first-mover advantages and market moats through deep brand accumulation, continuous high-intensity R&D investment, and mature global distribution networks.

In the Chinese market, local companies such as Sonoscape Medical and Aohua Endoscopy are also accelerating their layouts. Sonoscape Medical has entered the urology disposable ureteroscope field, forming direct competition with Mingzhi Technology. As more players enter the market, the industry faces dual challenges of rising price pressures and accelerating technological iterations. Market competition is no longer limited to product performance but extends to comprehensive dimensions such as supply chain efficiency, cost control, and clinical service capabilities.

From a regional market perspective, Europe and the US are currently the main consumer markets for global disposable endoscopes, closely related to their stringent infection control regulations, well-established health insurance payment systems, and high medical standards. Mingzhi Technology’s leading position in mainstream markets such as the US, Europe, and Japan is one of its core advantages, but it also results in the company's revenue being highly dependent on overseas markets, making its financial performance vulnerable to external systemic risks such as geopolitical tensions, exchange rate fluctuations, and changes in international trade policies.

Notably, several structural risks have emerged in Mingzhi Technology’s financial and operational indicators amid its rapid expansion. First, customer concentration remains high: from 2023 to the first nine months of 2025, sales revenue from the top five customers ranged between 62.6% and 69.9%, with the largest single client consistently accounting for over 30%. This concentration means that the company's performance stability is highly tied to major clients’ purchasing decisions, posing significant dependency risks.

Second, the channel structure is relatively singular. Although the company implements a 'hybrid global commercialization strategy,' 92.8% of its revenue in 2024 still came from distributors, with only 7.2% from direct sales. Over-reliance on the distribution system, while helpful for quickly achieving market coverage, weakens the company's control over end customers, compresses profit margins, and makes sales susceptible to distributor strategy adjustments.

Third, supply chain concentration was historically high. In 2024, purchases from the top five suppliers accounted for up to 81.5% of total procurement, though this figure dropped to 44.4% in the first nine months of 2025 after implementing supplier diversification strategies, indicating efforts to improve supply chain structure. However, ensuring the stable supply of core components and raw materials remains a long-term risk management challenge, especially amid global supply chain restructuring.

Finally, concerns over growth quality have arisen. In the first nine months of 2025, the company’s net profit declined by 14.49% year-over-year, while net operating cash flow decreased by 19.45%. The deterioration in cash flow was mainly due to increased inventory and extended accounts receivable collection cycles, reflecting challenges in operational efficiency and capital turnover during the company's scale expansion. Despite maintaining a gross margin of 73.7%, the contraction in net profit may already reflect early signs of eroding profitability amid intensifying market competition.

Overall, while the disposable endoscope sector holds promising prospects, competition is becoming increasingly fierce. Whether companies can strike a balance between continuous technological innovation, robust supply chain management, balanced customer and channel structures, and refined operational efficiency will determine their ability to achieve sustainable growth in this rapidly expanding market and ultimately stand out. For Mingzhi Technology, effectively managing the aforementioned operational and financial risks while enjoying industry growth dividends is key to realizing long-term value.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment