Fiber optic shortage triggers upstream supply concerns! Will fiber optic stocks continue to rise?

No more choosing between the two! Are the performance figures for optical communication and copper interconnect sectors exploding together?

Recent earnings reports from US companies show thatprofit growth rates for companies in the data center interconnect sector generally outpace those in traditional mainstream AI sectorssuch as cloud services and chip sectors.

The reason lies in the exponential increase in cabling and signal integrity challenges as data centers grow in complexity and connection demands rise, leading to nonlinear growth in the connector segment. Future data centers may adopt a hybrid architecture of optical and copper connections.

Currently, there are three paths for data center expansion: Scale Up, Scale Out, and Scale Across, corresponding to vertical scaling, horizontal scaling, and cross-domain collaboration. These three approaches increase demand for connectivity chips, optical interconnects, copper connections, and network connections at different levels.

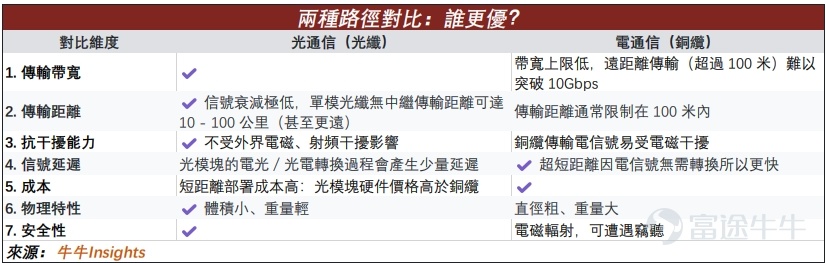

For distances of several meters, copper connections have a significant cost advantage over optical communication. Meanwhile, CPO co-packaged optics in ultra-short Scale-Up scenarios and fiber optic cables in ultra-long Scale Across scenarios offer better cost advantages. Optical vs. copper comparison is as follows:

Recent financial performance of companies that have announced their earnings reports.As shown below; among them$Broadcom (AVGO.US)$ and $Marvell Technology (MRVL.US)$It is also a major player in the connectivity sector, but considering the diversity of its products, it is not listed separately in the table below.

Data center connectivity encompasses multiple areas:

1. Optical interconnection

1) In the optical interconnect sector,$Coherent (COHR.US)$ 、 $Lumentum (LITE.US)$ 、 $Fabrinet (FN.US)$As a major optical module company, the core component of optical modules is the laser chip EML. In the high-end laser sector, the main players, in addition to COHR and LITE, mainly include Broadcom. It is worth mentioning that Fabrinet only engages in system-level packaging and manufacturing of optical modules and does not have its own optical module brand, resulting in relatively low added value or profit margins.

2) In addition to optical modules and laser EMLs, the optical interconnect sector also has companies that specialize in optical cables, such as$Corning (GLW.US)$ 。

3) In the future,Co-packaged Optical CPOThis will bring incremental value to the optical interconnect sector, addressing the power consumption and density pain points of Scale-up computing node interconnections. Coherent mentioned during a recent earnings call that pluggable optical modules will remain the dominant form factor in the Scale-Out domain for the long term. $NVIDIA (NVDA.US)$ The company has already laid out its CPO supply chain. Market expectations suggest that the CPO industry chain will generate substantial revenue by 2028.

Q&A: Why are both companies in the optical module space, yet Coherent's revenue growth is much lower than Lumentum's?

The reason is related to the revenue structure. Apart from data center optical communications, Coherent also operates in traditional telecom and industrial lasers, which have slower growth rates and have weighed down Coherent's overall performance. Additionally, Lumentum’s high-end laser EML products hold higher market share, establishing a stronger competitive moat.

2. Copper Interconnects and Power Delivery Connections

Representative companies include $TE Connectivity (TEL.US)$, $Amphenol (APH.US)$and $Credo Technology (CRDO.US)$Credo Technology, which focuses on active cables, with this business accounting for over 65% of its revenue. Notably, Credo Technology maintains a high gross margin, with the previous quarter’s gross margin reaching 67.55%.

In addition to cables, Amphenol, like TE Connectivity, produces high-speed connectors. However, TE Connectivity is not solely focused on data centers; it also has significant influence in electric vehicle connectors, and its exposure to the data center market is relatively smaller compared to other companies.

3. Network Connectivity

Major players in this area revolve around switching chips and switches. The leading companies in switching chips are Broadcom, Marvell, and $Microchip Technology (MCHP.US)$ and so on; the main companies in the switch industry include $Cisco (CSCO.US)$ 、 $Arista Networks (ANET.US)$ , Juniper Networks (which was acquired last year by $Hewlett Packard Enterprise (HPE.US)$ ).

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

37

113