[2026 Outlook] Plan Ahead! Share the Investment Opportunities You Are Optimistic About

Earnings and Options Strategy | Robinhood: With the crypto market slumping, can its stock price withstand cyclical earnings pressure?

$Robinhood (HOOD.US)$ is scheduled to release its earnings report after the market close on February 10, Eastern Time,The key focus of this quarter's earnings report is whether the decline in trading volume will weigh on profit performance and the company's outlook for user activity in 2026. Despite a strong annual performance in the context of a bull market in 2025, the recent slowdown in stock, options, and crypto trading activities, coupled with rising volatility, could pressure valuations.

Since the company releases key operational data nearly every month—ranging from customer acquisition, customer assets, transaction flow, margin balances, to securities lending income—by the time Robinhood announces its quarterly results, they typically do not deviate significantly from market expectations.

First, let’s look at the consensus market expectations for this earnings report:

– Institutional expectations forecast revenue of $1.341 billion for Q4 2025, reflecting a year-over-year increase of 32.29%;

– Earnings per share are expected to be $0.628, marking a year-over-year decrease of 37.81%.

Robinhood’s profit model can be summarized as 'zero-commission customer acquisition with multi-faceted monetization,'with Payment for Order Flow (PFOF)* and net interest income serving as the two core pillars. Revenue primarily consists of the following three main components:

1. Transaction-based revenues:

– Options: For a long time, options have been the largest source of transaction-based revenue. Due to the complexity and leverage involved in options trading, Robinhood earns higher order flow rebates from it.

– Cryptocurrencies: 2025 marks a milestone for its crypto business, with the completion of the acquisition of Bitstamp significantly boosting crypto trading revenue. Year-over-year growth in Q3 exceeded 300%.

– Equities: While being the foundation of the company's reputation, equities maintain a relatively stable share of total revenue, primarily driven by economies of scale from trading volumes.

2. Net Interest Revenues:

Main sources of income include financing revenue, securities borrowing revenue, segregated cash revenue, plus cash sweep (users investing idle funds through the Robinhood platform in external bank wealth management products), as well as interest income from the company’s own capital.

3. Other Revenues:

Primarily consists of Robinhood Gold subscription fees. Additionally, it includes revenue-sharing from the Gold Card (credit card) service launched in 2024-2025.

(Note: Payment for Order Flow (PFOF) does not directly charge users trading commissions but routes their trade orders to market makers, earning a share of the spread. This is the core monetization method that gives users a “free” trading experience.)

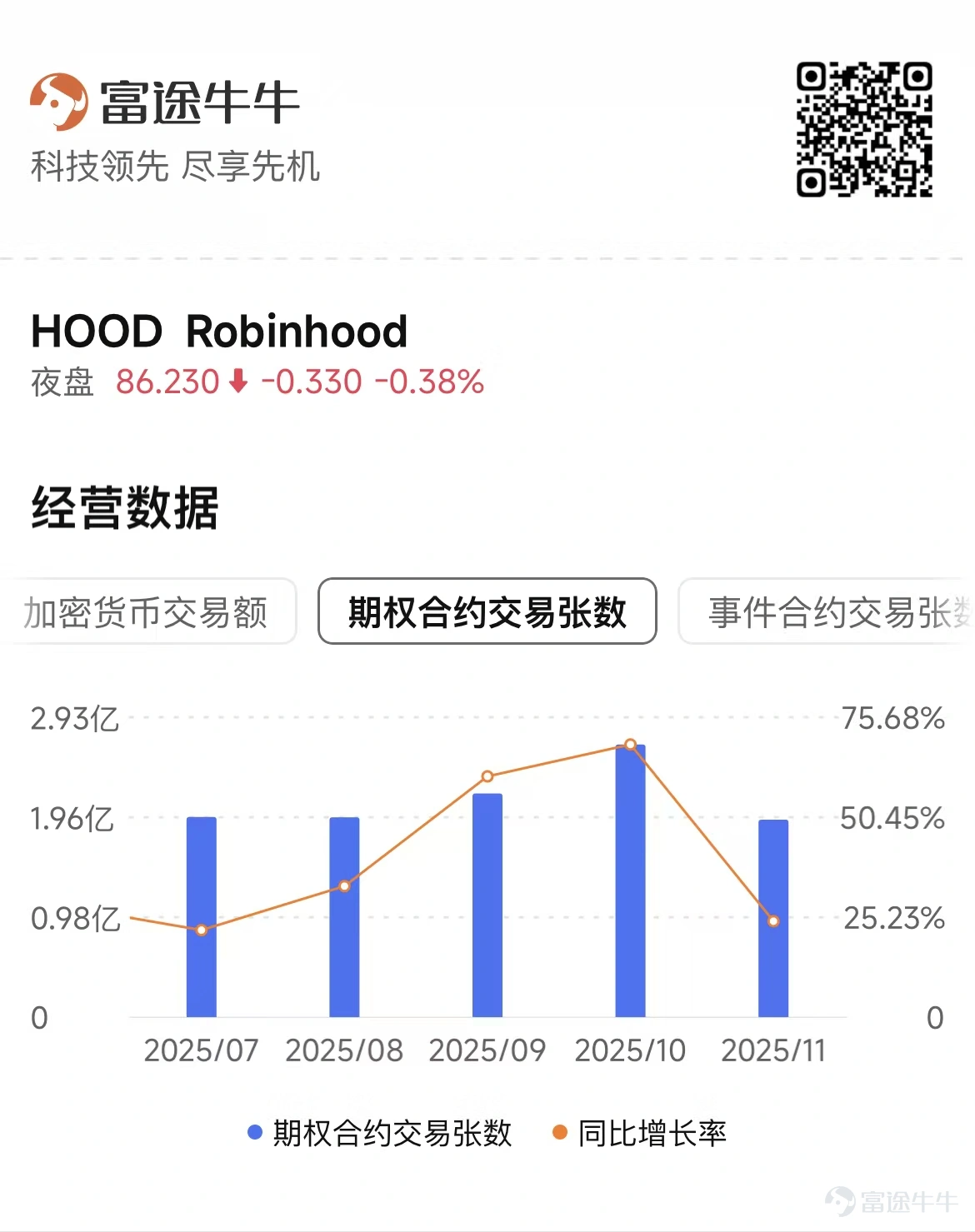

Trading Activity: November options trading volume declined month-over-month; focus on whether December data will show stabilization and recovery.

As Robinhood's core engine, trading revenue constitutes a significant portion of overall revenue, directly influenced by user activity levels and market conditions. User scale and participation are key indicators of the platform’s long-term value, especially critical when risk appetite weakens.

November trading data showed strong year-over-year growth, but several metrics declined month-over-month.Number of funded accountsDropped to 26.9 million, a decrease of approximately 130,000 from the end of October 2025, marking the first decline in recent times;Trading volumes in stocks, options, and cryptocurrenciesFell by 37%, 28%, and 12% respectively compared to October. The weakness in this data has sparked concerns in the market aboutA pullback in retail investors.

Investors will be watching whether December data can stabilize and rebound.If key metrics in December can recover effectively, it will significantly ease market anxiety over growth gaps; conversely, if the downturn continues, it may exacerbate doubts about future growth, putting pressure on stock prices.According to Bloomberg data, institutional consensus expects cryptocurrency trading revenue in the fourth quarter to possibly drop by 31% year-over-year.

It is worth noting that,Options have higher unit economics, with continuous increases in leverage and activity often contributing to higher ARPU during periods of elevated volatility, compounded by last quarter’s already high ARPU levels,If the strong and active trading environment is maintained this quarter, it will still be expected to support the resilience of overall commission income, offsetting some of the impact from the decline in traffic.

Crypto Business: Is the crypto market at the end of Q4 already bottoming out after its downturn?

The cryptocurrency business has evolved into the largest variable impacting Robinhood's earnings volatility. In the first nine months of 2025, this segment contributed up to $680 million in revenue, accounting for 37% of Robinhood's trading-related income.This makes it the second-largest revenue source, only behind options (44%).

However, the crypto asset market experienced severe two-way volatility this quarter, adding significant complexity to earnings forecasts.Although the market captured strong cryptocurrency momentum at the beginning of the fourth quarter, the collapse towards the end of the quarter posed a severe challenge. $Bitcoin (BTC.CC)$ Having fallen by half from the historical high of $126,000 in October 2025, Robinhood's stock price also experienced a significant correction of about 46% during the same period, dropping from $152 to $82.82.

In this earnings call,management's guidance on crypto trading trends from January to early February 2026 will be the top priority.Given the high volatility of crypto assets, the market urgently needs confirmation of the January start, as well as any adjustments regarding the company’s trading fee structure or new token listings, to assess whether this business line has bottomed out.

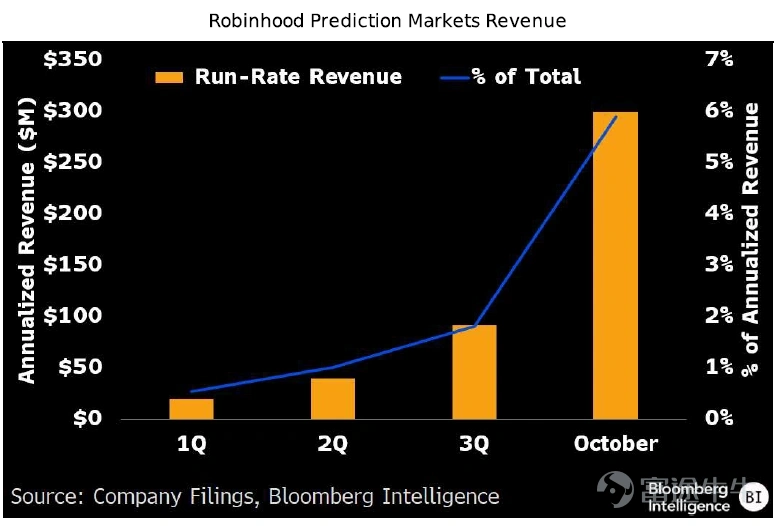

New Business Forecast Market: Strong performance in Q4, exploring the sustainability of growth post 'Super Bowl'

The prediction market emerged as the unexpected star of the third quarter, showing significant growth. The platform experienced explosive growth during the peak of the football season.

The rapid increase in event contract trading volume last quarter has led to a new business line with annualized revenue potential reaching the 'hundred-million-dollar' level. This business not only diversifies revenue streams but, more importantly, enhances user engagement through high-frequency interaction, creating positive synergy with the crypto ecosystem.

However, with the conclusion of the 60th Super Bowl on February 8, 2026, the trading peak for the NFL season in Robinhood's prediction market officially came to an end.Investors need to focus on how management plans the product roadmap for the 'post-Super Bowl era.'Can events from the NBA, March Madness, and MLB take over the traffic? And can expansion plans for non-sports contracts, such as politics and economic indicators, proceed smoothly?

If management can demonstrate a clear cross-category expansion path and prove that this business has the ability to transcend sports cycles, it will help support the 'super app' narrative.Conversely, if the prediction market revenue performs strongly in the fourth quarter but management’s outlook for the first quarter declines, the market may view it as a fleeting success rather than a sustainable business.

Interest-bearing business: Defensive income, focusing on possible adverse impacts from future interest rate path changes.

Amid heightened volatility in trading income, net interest income (NII) played a defensive role. The performance of interest-bearing businesses in the third quarter was also very strong, showcasing the company’s ability to monetize in a high-interest-rate environment.These reflect the higher risk appetite of retail investors on the Robinhood platform during bull markets, which drives stronger revenue generation for the platform in bullish conditions.

This quarter, macro interest rates remain relatively high, with customer cash balances and margin businesses providing a base level of support for net interest income; meanwhile, the platform has enhanced its spread capture capability through improvements in fund management and product optimization, which is crucial for stabilizing profits. Notably, should there be a marginal decline in the interest rate path, the net interest margin may face pressure, but customer retention and diversified asset allocation are expected to partially offset this adverse impact, maintaining profit margin resilience.

Earnings options strategy

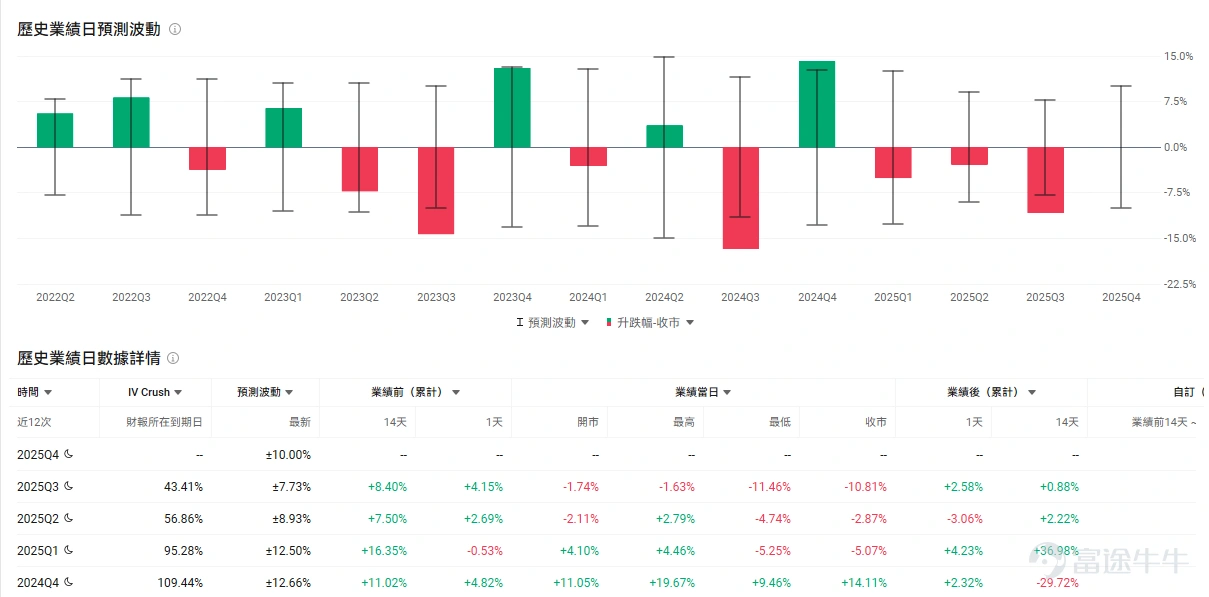

Overall, after experiencing a significant pullback, technical indicators for HOOD.US showThe moving average system indicates a bearish alignment, and the trend remains weak. However, after recent declines, the stock price has entered an oversold zone, suggesting the possibility of technical recovery.Options market trading activity reflects a relative dominance of bullish sentiment, with unusual large orders showing attention towards short-term upside potential. The implied volatility from the options market suggests a ±10% fluctuation on earnings day.

HOOD's implied volatility (IV) has remained at a relatively high level recently. On February 9, the implied volatility was 79.27%, higher than the 79th percentile of its 52-week historical volatility. High implied volatility usually means that option premiums are also relatively more expensive. Recently, options trading has been very active. The Put/Call Ratio on February 9 was 0.47, indicating that call option trading volume significantly exceeded put options,A lower Put/Call Ratio may reflect a market sentiment leaning towards optimism.

Given the currentIV being at a historically high level (>79th percentile), strategies can be built bycapitalizing on high implied volatility (IV) to sell options for profit or using spreads to reduce holding costs.

1. Bull Put Spread

If investors believe that Robinhood has entered the oversold zone and expect the market will not fall further, or predict limited upside potential in the stock price.

This strategy takes advantage of a high IV environment, acting as an option 'seller' rather than a 'buyer,' aiming to profit from time decay and declining volatility.It is ideal to construct this strategy when implied volatility is high, as profits can be made even if the stock remains stagnant, consolidates sideways, or experiences range-bound fluctuations, creating a strategy with both limited gains and losses.Even if earnings are mediocre, as long as there is no crash-like drop, the elimination of uncertainty (IV Crush) will quickly generate profits for this setup. If the earnings report triggers a significant drop in stock price, the maximum loss is capped at the difference between the two strike prices minus the premium received.

The construction involves two Puts: 'selling' an out-of-the-money Put at a higher strike price (to collect substantial premiums) while simultaneously 'buying' a cheaper Put (as protection). Both Puts share the same expiration date, strike prices, and contract quantities. When the stock price rises above the higher strike price, both options remain out-of-the-money, achieving maximum profit equal to the total premium collected upon initiation. If the underlying stock falls, the cheaper Put acts as a hedge, limiting maximum loss.

(The design images displayed on screen are for illustrative purposes only and do not constitute any investment advice or guarantees; market conditions fluctuate frequently, and the option prices shown do not represent real-world values.)

2. Long Collar Option Strategy

If investors believe that the core rationale for holding Robinhood remains intact but are concerned about black swan risks from earnings reports and short-term pullback risks, they can adopt the Long Collar option strategy.

For investors who already hold the underlying asset, simply buying put options (Protective Put) for hedging can be expensive in the current environment. The collar strategy hedges the cost of premiums by simultaneously 'buying protection' and 'selling out-of-the-money call options (Covered Call),' allowing downside risk during the earnings period to be locked in at extremely low net cost or even 'zero cost.'

The risk lies in the possibility that if the underlying stock rises, the 'selling call options' portion may be exercised, which would limit the overall profit potential. Therefore, if you are more optimistic about the upward logic, you can raise the strike price of the Call to accept a small net outlay in exchange for more upside potential.

(The design images displayed on screen are for illustrative purposes only and do not constitute any investment advice or guarantees; market conditions fluctuate frequently, and the option prices shown do not represent real-world values.)

3、Single-leg buying options (Long call/put) - Leveraging small capital for potentially large returns

If investors have a very clear bullish or bearish view on HOOD's earnings report, and believe that the volatility may exceed the current market expectation of 10%, they can try single-leg buying of call options/put options. When the stock price rises/falls significantly, investors' profits will increase accordingly.

However, investors should note that the volatility is relatively high at this time, and single-leg buying will face risks related to significant time value and volatility decay. Other things being equal, options further from the expiration date are more expensive. The closer to the expiration date, the faster the time value erodes. This strategy is suitable for investors who are highly confident in the direction of the underlying stock, aim to leverage small capital for potentially large returns, and are also prepared to accept the loss of premiums. Investors should focus on timely stop-loss and taking profits when appropriate.

Finally, here's a small perk for fellow investors—welcome to claim it!Options Beginner Pack

This event is exclusively for invited HK users, click to learn moreDetailed event rules >>

Futu's simulated trading challenge is now open for registration! Zero cost, zero risk, and you could win stock cash vouchers!

Disclaimer

This content does not constitute any offer, solicitation, recommendation, opinion, or guarantee of any securities, financial products, or tools. The risk of loss in buying and selling options can be substantial. In some cases, your losses may exceed the initial margin amount deposited. Even if you set contingent orders, such as 'stop-loss' or 'limit' orders, these may not necessarily prevent losses. Market conditions may make these orders unexecutable. You might be required to deposit additional margin within a short period. If you fail to provide the required amount within the specified time, your open positions may be liquidated. However, you will still be responsible for any account deficit arising from this. Therefore, before trading, you should study and understand options and carefully consider whether such trading suits you based on your financial situation and investment objectives. If you trade options, you should be familiar with the procedures upon exercising options and at expiration, as well as your rights and obligations when exercising options and at expiration.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

33

12