Tech giants boost Capex again! What's the outlook for future stock prices?

Trillion-dollar gamble on AI: Tech giants' collective spending spree sparks market panic - is it a mispricing or a bubble?

Author | Eric

In the latest earnings reports from major tech firms, the capital expenditure forecasts for 2026 have gone from already substantial to 'did someone accidentally hit a few extra zeros on the keyboard?' It's an almost trillion-dollar level of madness, far exceeding Wall Street's expectations.

– $Meta Platforms (META.US)$ :2026 capital expenditure guidance115-135 billion USD (market expectation 110 billion)Although the stock price rose by about 10% on the day, the gains failed to hold. Interestingly, while the market had reacted positively to Meta's optimistic Q1 guidance earlier, has it now 'changed its mind'?

– $Microsoft (MSFT.US)$ :Fiscal year 2026 (Q2 2025-Q2 2026) capital expenditure guidance140-150 billion USD (market expectation 109 billion)As a result, the stock price plummeted by 10%, primarily because Azure's growth rate fell short of market expectations, indicating that the market is closely watching the pace of ROI realization.

– $Alphabet-C (GOOG.US)$ :2026 capital expenditure guidance175-185 billion US dollars (market expectation 115 billion), the stock price plunged at one point, as the market is trying to come to terms with a more asset-heavy Google.

– $Amazon (AMZN.US)$ :Capital expenditure guidance for 2026 is approximately200 billion US dollars (market expectation 146 billion), leading to an approximately 11% drop in after-hours stock price, even though Amazon AWS delivered stronger-than-expected year-over-year growth24%.

What exactly is the market panicking about?

In simple terms,The speed of burning money has outpaced the speed of making money, and this gap is widening.This scenario happens to unfold at a time when market expectations are already running high. If the growth curve is clearly re-accelerating, the market can tolerate high capital expenditures. But when spending surges while revenue growth relies on distant promises, the market won’t accept it. Especially when Microsoft, for strategic reasons, 'intentionally suppresses' the growth rate of its cloud business, panic will spread.

A deeper layer of anxiety lies in profit margins, especially the potential for massive future depreciation.The money spent on capital expenditures doesn’t vanish into thin air; it turns into depreciation and amortization, lingering like a ghost in the income statements over the next few years—this is also what the major short sellers are questioning.

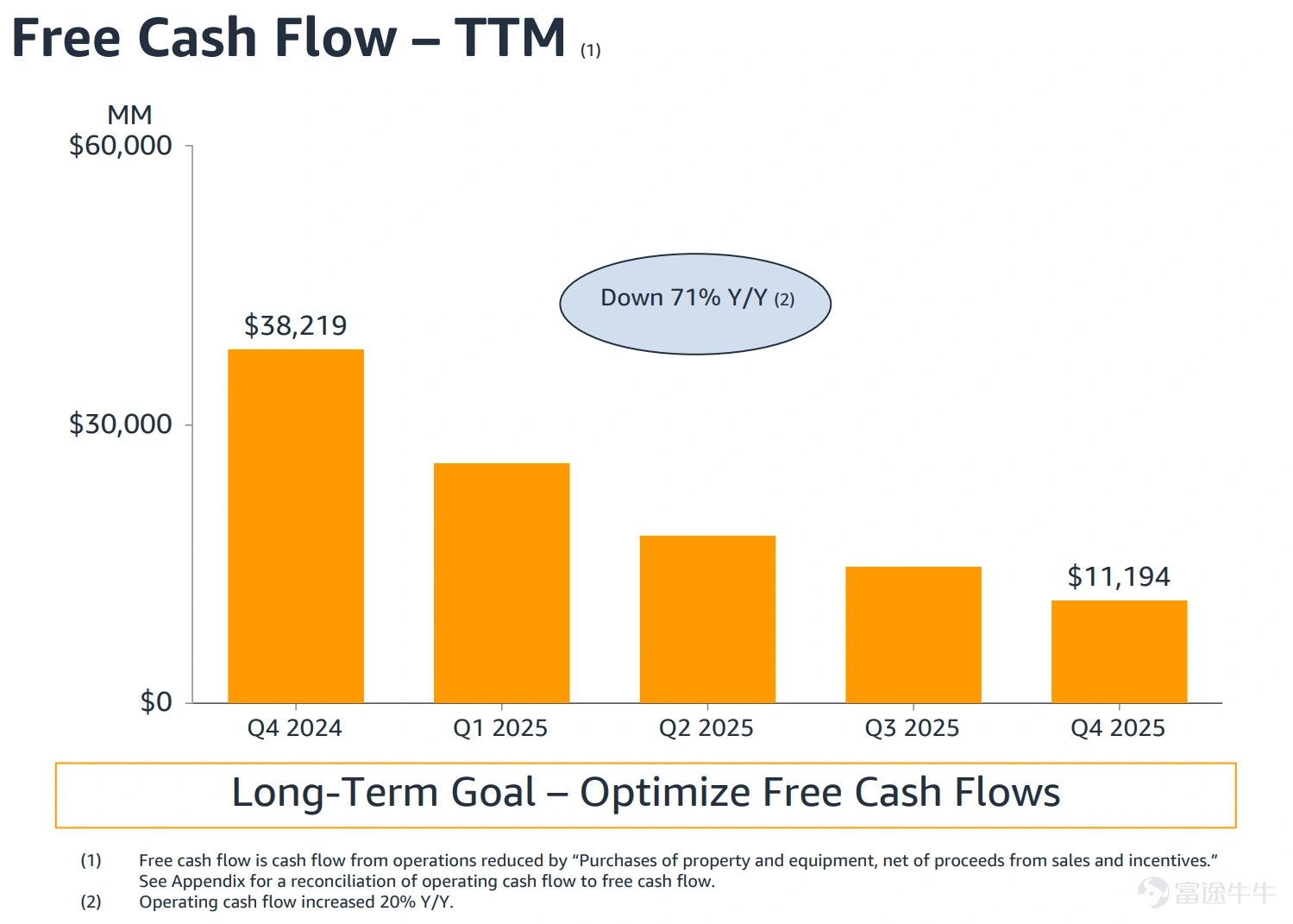

The logic of market valuation is being repriced.The mainstream logic of market valuation is primarily based on free cash flow. If capital expenditures remain high, they will severely compress free cash flow. For example, Amazon's TTM free cash flow for this quarter plummeted by 71% year-over-year, triggering market panic. Meanwhile, these tech giants used to prop up their stock prices with massive buybacks, but now their buyback capacity will be constrained by capital expenditures. For instance, Google's repurchase amount for this quarter fell by about 65% year-over-year.。

So, has the market overreacted?

Despite the prevailing panic sentiment right now, there are three logics worth pondering:

1. Investment cycles always follow the pattern of 'short-term pain for long-term gain.'

Large-scale investments often face initial market skepticism before yielding long-term returns. Recall $Amazon (AMZN.US)$ Amazon Web Services (AWS) was heavily criticized for several years due to its upfront investments in cloud computing. However, these very investments eventually created one of the most strategically valuable and economically rewarding businesses in the tech world. Even today’s highly praised $Alphabet-C (GOOG.US)$ cloud services only turned profitable in 2023. Perhaps today's large cycle of AI investment is following the same script.

2. Two high ROI scenarios for AI have already emerged: cloud computing and advertising

The growth of cloud services remains healthy across platforms, with some even continuing to accelerate on a quarter-over-quarter basis. All three of the world’s largest cloud providers have indicated that every unit of computing power they bring online directly translates into revenue. On the other hand, $Meta Platforms (META.US)$ the consistently strong advertising growth serves as evidence of AI monetization within the advertising industry.

However, this monetization varies depending on product portfolios, strategic decisions (for instance, $Microsoft (MSFT.US)$ Microsoft has faced criticism for not dedicating all its computing power to Azure), as well as the timing of when each company brings its computing power online ( $Amazon (AMZN.US)$ In the first half of last year, AWS experienced sluggish growth precisely because of delays in bringing computing power online). These factors result in varying rates of revenue growth.

3. Ongoing capital expenditures are supporting the long-term growth of semiconductor performance

When cloud giants collectively increase spending by tens of billions, downstream semiconductor beneficiaries typically see order momentum even before the giants realize their return on investment. This is why semiconductors, memory, networking, optical modules, and power sectors sometimes suffer from macro sentiment despite having highly certain fundamentals, often leading to temporary mismatches that, in hindsight, seem like missed golden opportunities. The current downturn in the semiconductor sector due to excessive capital expenditure likely reflects more of an emotional collapse than fundamental weakness.

Summary

The market is not denying AI; it wants a clearer timeline for return on investment and is concerned about uncertainties regarding profit margins, depreciation, and capital returns.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (7)

to post a comment

29

49