2026 IPO bonanza! Over 90% of new stocks rose on their debut

IPO Outlook | Domestically Dominant, Overseas Under Pressure: Is Gemi Lei, the Chinese Coffee Machine Brand, Seeking Solutions in Hong Kong?

Amidst the accelerating penetration of global coffee culture and the wave of consumption upgrade in China, the Chinese coffee machine industry is at a historic turning point - evolving from a 'niche tool' to a 'lifestyle carrier,' moving from contract manufacturing to technological independence and brand internationalization. As a benchmark company in this transformative wave, Gemi Lei Holdings Limited (hereinafter referred to as 'Gemi Lei') has officially launched its bid for the Hong Kong capital market.

According to Zhitong Finance APP, the Hong Kong Stock Exchange disclosed on January 29 that Gemi Lei submitted an application for listing on the Main Board, with CITIC Securities acting as the exclusive sponsor. Amidst the current wave of domestic substitution entering the coffee equipment industry, how does Gemi Lei, which has been deeply involved in the industry for over a decade, measure up?

Strategic transformation shows significant results, with revenue and net profit steadily increasing

According to the prospectus, GemiLai is a professional coffee machine company in China. After more than a decade of development, the company has established an integrated business model covering product design, R&D, manufacturing, sales, and after-sales services, achieving comprehensive coverage of the coffee machine industry value chain. Currently, its products are distributed to over 60 countries and regions worldwide, with cumulative sales exceeding 2 million units, serving more than 400,000 users. It has become a representative Chinese coffee machine brand entering the international market.

According to Frost & Sullivan, in terms of revenue, GemiLai ranks as the second-largest coffee machine brand in China’s coffee machine industry and the largest domestic coffee machine brand, with a market share of approximately 7.5% in 2024. In the same year, in terms of revenue, GemiLai ranked as the largest coffee machine brand in China's semi-automatic espresso machine industry, with a market share of approximately 16.0%. It also ranked as the top brand in the split-type semi-automatic espresso machine sector, with a market share of approximately 27.9%.

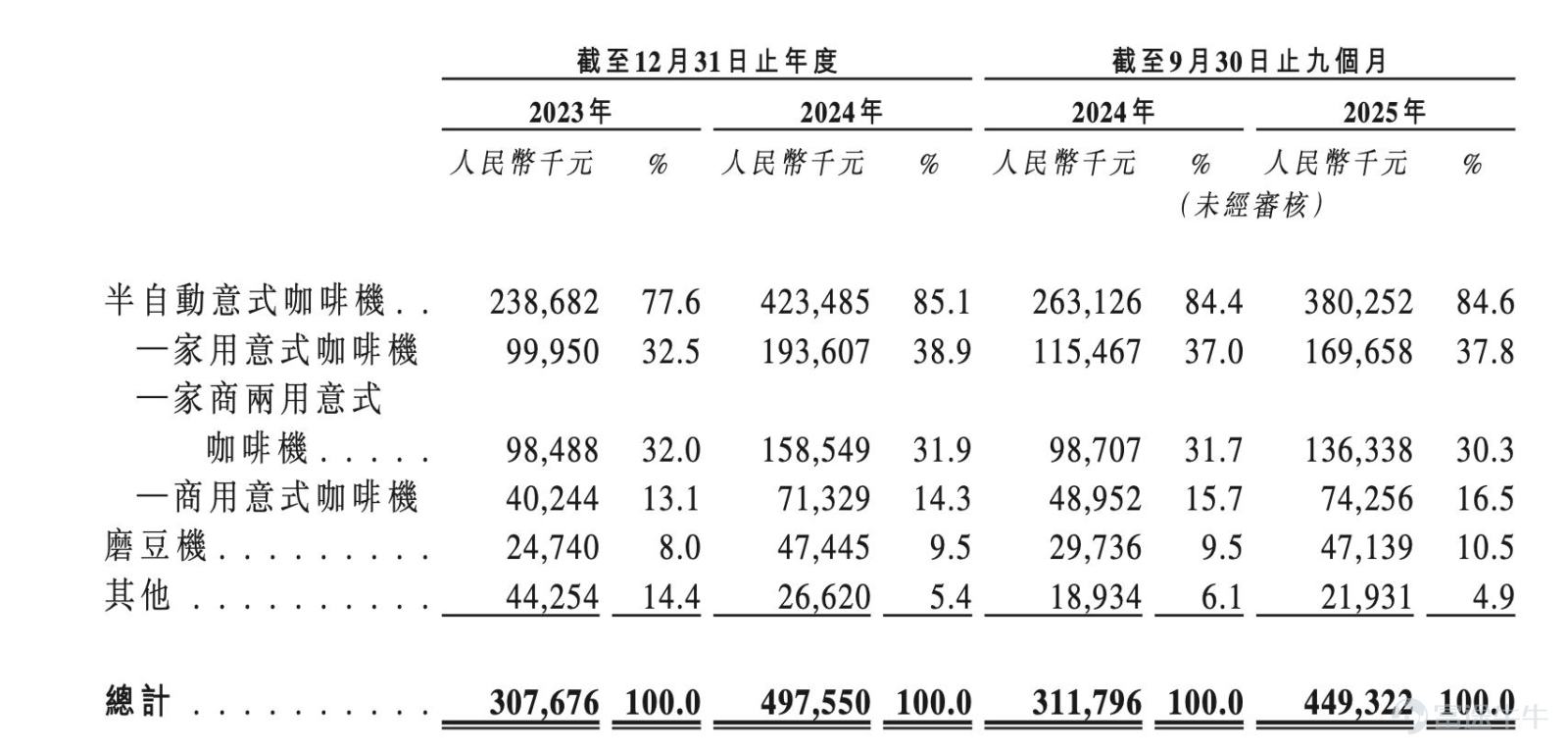

With a leading position in the industry, the company's revenue has grown year by year. In 2023, 2024, and the first nine months of 2025, GemiLai achieved revenues of approximately 308 million yuan (RMB, hereinafter), 498 million yuan, and 449 million yuan, respectively.

In terms of business segmentation, GemiLai has developed a multi-series product system of espresso machines tailored for diverse usage scenarios such as homes, offices, restaurants, and cafes, offering a wide range of SKUs to provide professional, reliable, and aesthetically valuable coffee-making equipment for different user groups. Additionally, the company has expanded its product lines to include professional grinders, coffee beans, and other coffee machine accessories.

Despite being known as a representative of high-end domestic coffee machines, the company’s revenue is actually 'semi-automatic dominated with steady commercial growth.' During the reporting period, revenue from its semi-automatic espresso machines was 239 million yuan, 423 million yuan, 263 million yuan, and 380 million yuan, showing significant growth, while the proportion of revenue continued to increase, rising from 77.6% in 2023 to 84.6% in the first nine months of 2025, further solidifying its core business position.

By comparison, although revenue from commercial applications (including commercial espresso machines and dual-use commercial espresso machines) remained stable at 139 million yuan, 230 million yuan, and 211 million yuan during the reporting period, the revenue share fluctuated, slightly declining from about 45% in 2023 to around 47% in the first nine months of 2025, with overall scale steadily expanding.

Meanwhile, the home-use espresso machine business performed robustly, with revenue increasing from 100 million yuan in 2023 to 194 million yuan in 2024, and its share rising from 32.5% to 38.9%, demonstrating sustained penetration amid consumption upgrade trends. By the first nine months of 2025, this business segment had reached 170 million yuan in revenue, maintaining a share of 37.8%, becoming the company's second-largest revenue pillar.

Other product lines, including accessories and grinders, exhibited clear strategic contraction, with revenue dropping from 44 million yuan in 2023 to 22 million yuan in the first nine months of 2025. The revenue share also plummeted from 14.4% to 4.9%, reflecting the company’s strategic adjustment to further focus on its core coffee machine business and optimize its product structure.

In terms of business models, the company has built a dual-track business architecture driven by “in-house brands + third-party ODM.” The in-house brand business serves as the core growth engine and brand value carrier, directly communicating brand positioning to end consumers and commercial users. Meanwhile, the ODM business leverages the company’s capabilities in product design and large-scale manufacturing to provide technical and production support to domestic and overseas brand clients, achieving industrial chain synergy and capacity optimization.

In recent years, the company’s strategic focus has significantly shifted toward in-house brands, reflecting a transformation path from “manufacturing-supported” to “brand-led.” From 2023 to 2024, the revenue share of in-house brands surged from 69.2% to 82.4%, reaching 83.3% in the first nine months of 2025, becoming the key driver of the company’s overall growth.

Revenue from third-party ODM business has continued to contract, gradually declining from RMB 95 million in 2023 to RMB 87 million in 2024, with its share dropping from 30.8% to 17.6%. In the first nine months of 2025, this figure further slid to 16.7%. The company acknowledged that this change stems from a deliberate strategic refocusing – while ODM business still holds value in maintaining production scale and optimizing supply chain efficiency, its weight in the company's long-term growth strategy has been systematically reduced.

With revenue growth, the company’s net profit performance has also climbed steadily. GemiLei’s profit and total comprehensive income surged from RMB 22.005 million in 2023 to RMB 40.005 million in 2024, an increase of 81.8%. In the first nine months of 2025, this figure reached RMB 53.972 million, surpassing the full-year level of 2024. However, it is worth noting that the company’s gross margin has fluctuated. During the reporting period, the company’s gross margins were 41.9%, 40.5%, and 44.1%, respectively. Regarding the reasons for the decline in gross margin in 2024, the company stated that this was mainly due to the impact of factory relocation on production efficiency. As production capacity recovers and e-commerce sales increase, the company’s gross margin rebounded in 2025.

The coffee machine industry is thriving.

Behind the strong performance lies the thriving industry in which GemiLei operates.

According to a report by Frost & Sullivan, the global and Chinese coffee machine markets have shown strong and sustained growth in recent years, with particularly significant expansion in the home-use segment, becoming the core driver of industry growth.

The global market size increased from USD 15.3 billion in 2019 to USD 30.6 billion in 2024, with a compound annual growth rate (CAGR) of 14.9%, and is expected to further expand to USD 59.5 billion by 2029, with a CAGR of 14.1% during this period. Focusing on the Chinese market, its growth rate is significantly higher than the global average. The overall market size rapidly climbed from RMB 2 billion in 2019 to RMB 5.3 billion in 2024, with a CAGR as high as 21.5%, and is projected to reach RMB 12.5 billion by 2029, with a CAGR of 18.7% during this period.

In terms of industry competition, the Chinese coffee machine market is highly competitive, with international giants and local companies vying for consumer attention. According to a report by Frost & Sullivan, the total revenue of China’s coffee machine industry reached RMB 5.3 billion in 2024, with the top five market participants accounting for approximately 44.1% of the market share. In 2024, GemiLei was the second-largest coffee machine brand in China’s coffee machine industry, with a market share of about 7.5%. In terms of revenue, by 2024, the company was the largest domestic brand in China’s coffee machine market.

Zhitong Finance APP noted that although GemiLei has a solid position in the domestic market with continuous revenue growth, its performance in overseas markets shows some pressure. From 2023 to the first nine months of 2025, the company’s reliance on the Chinese market significantly increased, with revenue share rising from 69.7% to 80.9%, while the proportion of overseas business correspondingly shrank. Particularly noteworthy is the performance in the US market, where revenue plummeted from RMB 31.2 million in 2023 to RMB 10.7 million in 2024, a drop of 79.3%. Although there was a slight rebound to RMB 10.4 million in the first nine months of 2025, it remains far below previous levels. The company explained that this was mainly due to a significant reduction in cocktail machine orders by relevant customers starting from 2024. Despite efforts to stabilize the market through online channels, the issues of a single business structure and excessively high customer concentration have emerged as potential risks for overseas expansion.

Meanwhile, while the Asian market (excluding China) remained stable, contributing RMB 64.2 million in revenue in the first nine months of 2025, or 14.3% of total revenue, its growth momentum has yet to fully materialize, making it difficult to offset the impact of fluctuations in the European and American markets. Against the backdrop of the continuous expansion of the global coffee machine market and accelerated overseas expansion of Chinese enterprises, the decline in GemiLei’s overseas business not only potentially limits its ability to capture global growth dividends but also makes its revenue structure more vulnerable to changes in the economic or consumption environment of a single region. If the company fails to effectively optimize its overseas customer base, expand its diversified product lines, and enter new regional markets, the balance and risk resistance of its long-term growth may face challenges.

Driven by the dual forces of the global coffee consumption wave and the upgrade of China’s smart manufacturing, GemiLei, with its deep expertise in semi-automatic espresso machines and a clear proprietary brand strategy, has established a significant industry position and growth momentum in the domestic market. However, facing increasingly fierce industry competition and structural challenges – including heavy reliance on a single product line and the domestic market, the phased contraction of overseas business, especially in the US market, and the potential risks brought by customer concentration – the company’s long-term growth path remains a test.

This Hong Kong listing is not only a key step for Gemi Technology to broaden its financing channels, strengthen R&D, and boost production capacity, but also an important opportunity to optimize its business structure, advance brand globalization, and build a more resilient and diversified growth trajectory. In the future, whether it can consolidate its domestic advantages while effectively breaking through overseas market bottlenecks and achieve a brand leap from 'leading in China' to 'global influence' will become the core issue for continued investor attention.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment