Another earnings miss? AMD plunges over 17% post-results!

Qualcomm Earnings Preview: Headwinds in Smartphone, Key Depends on Whether Potential Businesses Can Change the Narrative

Author/Richard

$Qualcomm (QCOM.US)$ Qualcomm will release its FYQ1 results after the US stock market closes on Wednesday. In the short term, concerns over Apple's self-developed baseband and the current smartphone market are hard to avoid, and pressure on performance over a certain period is inevitable. This quarter, the market focus has shifted from whether earnings will exceed expectations to how demand will be sustained after smartphone business inventory preparation, the sustainability of automotive business growth, and the commercial progress of AI PCs and data center chips. Signals from AI-related business implementation will directly affect long-term valuation logic.

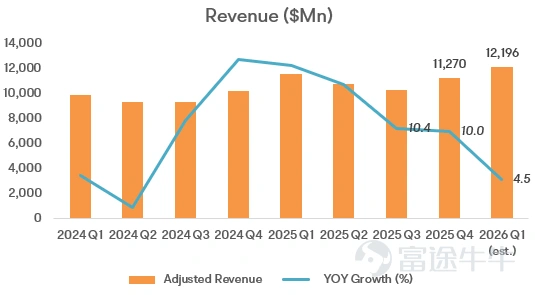

Core Financial Indicators

In the previous quarter (FY4Q25), Qualcomm provided narrow guidance for FY1Q26: revenue of $11.8 billion–$12.6 billion, including QCT (chip division) at $10.3 billion–$10.9 billion, QTL (patent licensing) at $1.4 billion–$1.6 billion; Non-GAAP EPS: $3.30–$3.50.

Consensus expectations from sell-side analysts are also close to the company’s guidance: revenue around $12.1 billion–$12.23 billion; EPS around $3.37–$3.39.

Key concerns

Pressure on smartphone business

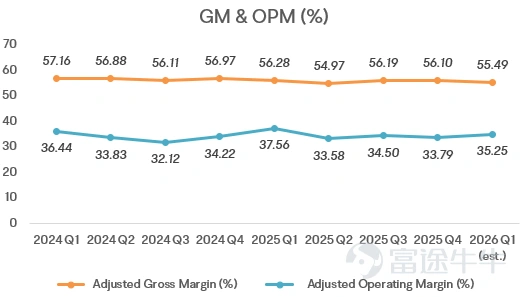

The mobile business (accounting for over 60%) is facing pressure from a pullback in demand, which is the core factor behind the slowdown in revenue growth this quarter. FY25Q4 growth was primarily driven by the early release of Snapdragon 8 Elite Gen5 by one month, prompting downstream manufacturers to frontload their inventory needs. However, Q1 of 2026 lacks similar catalysts, and global smartphone shipments are only maintaining low single-digit growth. Additionally, Apple's strategy of offering more features without raising prices for its base models is squeezing the mid-to-high-end Android market. In the short term, the mobile business is inevitably under pressure.

If memory prices remain high, many OEMs commonly respond by downgrading specs for mid-to-low-end models, extending replacement cycles, or passing on price increases to consumers. This is particularly sensitive for the Android supply chain, where demand elasticity is higher (especially noticeable in emerging markets and lower price segments). Therefore, management’s tone regarding QCT Handsets during the earnings call will be crucial.

At the same time, Apple remains a major variable. The company is testing its self-developed modems in lower-end models while continuing to rely on Qualcomm for high-end devices in the short term. This delicate balancing act between technical performance and internal development progress represents an ongoing uncertainty for Qualcomm.

Automotive/IoT: The market wants order curves

With the mobile business under pressure, investors want to see clearer growth trajectories for these potential businesses.

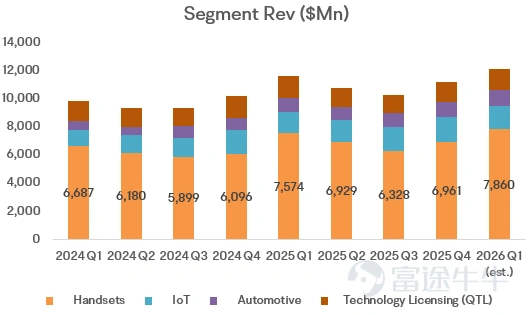

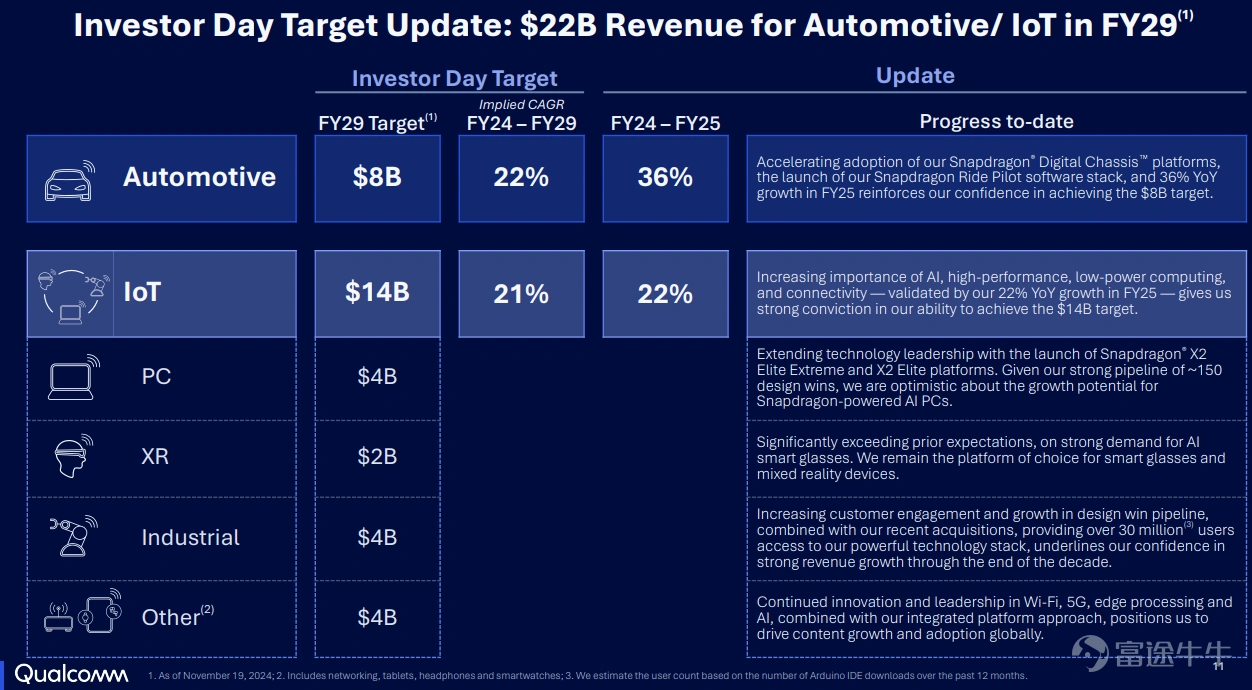

Automotive: The automotive segment, which accounts for 9% of Qualcomm’s business, has already become an important source of growth within QCT. However, bears often focus on competitive intensity, especially in China, where automakers are aggressively pushing for self-developed or alternative solutions. Even if this does not materially impact finances in the short term, the stock price tends to trade on expectations of 'market share erosion.'

IoT: Accounting for approximately 16%, growth is mainly driven by industrial WiFi 7, smart glasses, and AI PCs. For AI PCs, we need to see tangible indicators such as increased shipments, channel sales momentum, and enterprise adoption. As of the end of Q4 FY25, Qualcomm's global market share in PC chips remains below 1%, far behind Intel (78%) and AMD (21%).

Data center visibility remains low

AI chips for data centers are still in their infancy, with the first deal secured but little revenue expected in the near term. In October 2025, Qualcomm launched the AI200 data center chip, with its first customer being Humain, a Saudi Arabian AI startup. The plan is to deploy 200 megawatts of computing power by 2026, with the order expected to contribute over $10 billion in revenue across the entire cooperation cycle. However, the first batch of chips will begin shipping in 2026, with no substantial revenue recorded in Q1 2026.

This quarter, two key signals need to be monitored: first, whether the mass production progress of the AI200 chip meets expectations, and second, whether new Tier-1 customers (such as cloud computing vendors and large technology companies) are added. This will verify its competitiveness in the data center AI market and provide support for long-term valuation.

Conclusion

Qualcomm's core challenge at present lies in the contradiction between the slowdown in growth of its traditional business and the lack of a clear growth curve for its new businesses (AI, automotive). The year 2026 will be a critical test period for Qualcomm’s transformation strategy. If Qualcomm can shift the narrative from 'smartphones' to a multi-engine combination where 'automotive/IoT/PC continue to gain traction, and data centers move from concept presentations to measurable execution milestones,' it is highly likely to drive a recovery in valuation. However, if the traditional business faces pressure and the new businesses fail to make breakthroughs, the valuation may remain under pressure.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1