Tech giants boost Capex again! What's the outlook for future stock prices?

Earnings Options Strategy | Cloud + Gemini in the spotlight, will Capex steal the show? How will Google's earnings report play out?

The key factors for this earnings report from Google are not just whether 'advertising exceeded expectations,' but also two other things ——The acceleration rate of Google Cloud and how high the 2026 CapEx guidance will be raised to.The options market is currently pricing in a post-earnings volatility of around 6%.

The current market consensus shows that $Alphabet-A (GOOGL.US)$$Alphabet-C (GOOG.US)$ Q4 revenue is expected to reach approximately $111.45 billion, growing by about 15% year-over-year, with EPS at around $2.64, reflecting a year-over-year growth of approximately 23%. In terms of business breakdown, the market expects Google Cloud's growth rate to be about 36% year-over-year.

The three major highlights of this earnings report: Cloud, AI, CapEx.

Highlight one: Cloud needs to be 'faster' and 'more profitable.'

What the market is looking for in cloud this time iscontinued acceleration in growth + continued improvement in profit margins,because the overall narrative in big tech is shifting towards:AI spending can be substantial, but returns must be visible.。

– If the cloud business growth rate reaches or exceeds the consensus36%, and profit margins continue to improve, it will be seen as Google's“AI investment - market demand - financial return realization”positive feedback loop being fully operational.

– Conversely, even if total revenue/ EPS beats expectations, but the cloud business growth rate falls short, the market could interpret this as 'weak AI demand/intensified competition,' leading to significant pressure on the stock price given the current sentiment.

Key focus two: How will Gemini’s “explosive popularity” reflect in the earnings?

Following the release of the new version of Gemini at the end of last year, its popularity quickly surged. In what form will this explosive popularity be confirmed in this earnings report?

First, let's look at the official disclosed 'hard metrics.' Management publicly mentioned last quarter that the Gemini app had over 650 million monthly active users; the company processes about 7 billion tokens per minute; the number of monthly active users reached 2 billion for 'AI Overviews'; and the company disclosed that 'over 70% of cloud business customers are using AI-related capabilities.'

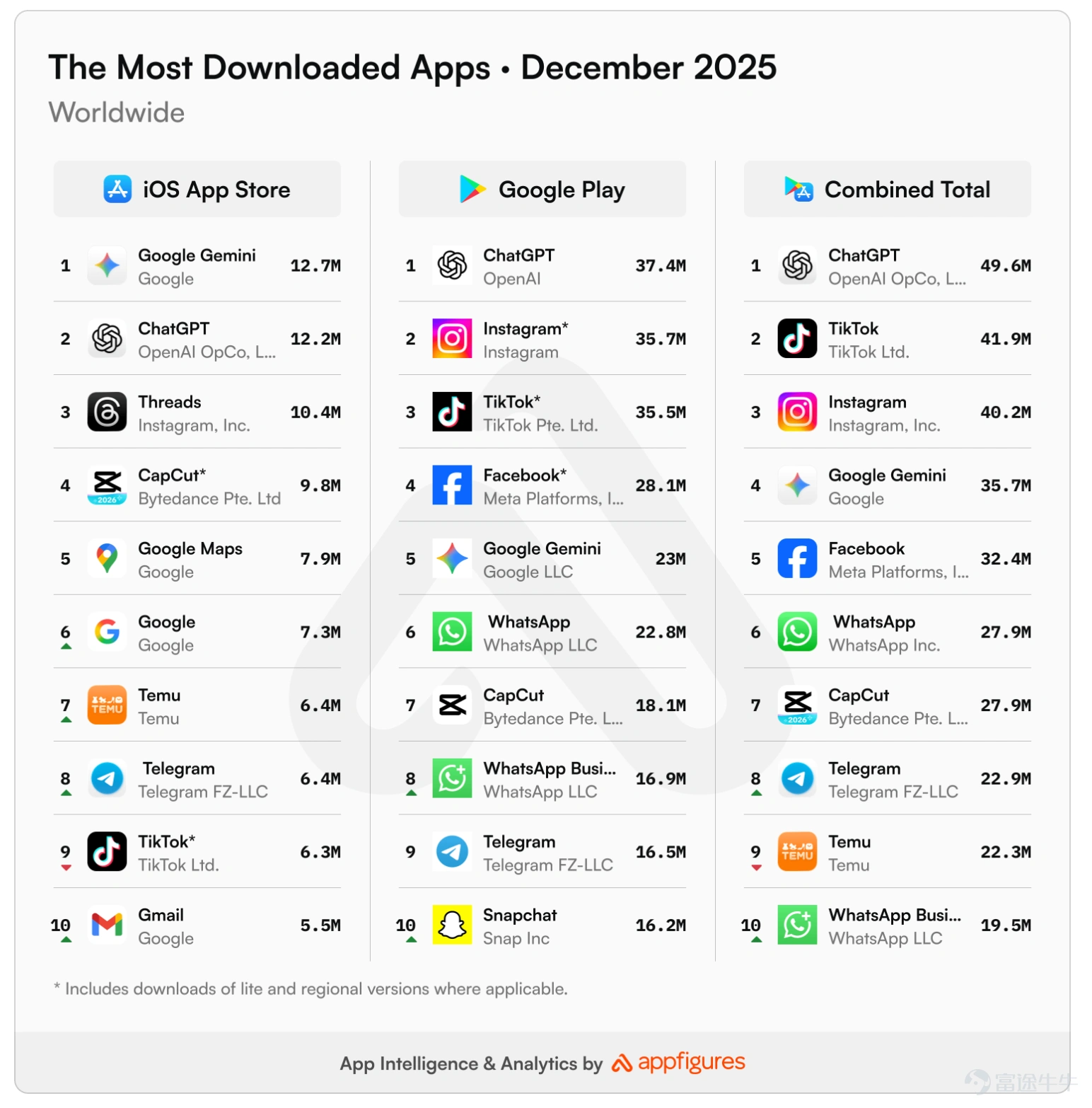

Tracking the latest data shows that third-party platforms also confirm Gemini’s popularity. Appfigures data shows that in December 2025, Gemini ranked approximately 35.7 million downloads globally.

Similarweb's data indicates that as of January 2nd this year, Gemini showed outstanding performance in terms of traffic share changes over the past 12 weeks within the 'general AI tools' category,with its traffic share continuing to increase in the overall market.

Whether Gemini’s popularity will be reflected and confirmed in financial data will be critical information impacting the entire AI narrative.

Key point three: Will 2026 CapEx become the 'biggest risk factor'?

This point determines whether the market will continue to give Google a valuation premium.

The market has formed a "reference point": Meta Platforms raised its 2026 capital expenditure guidance to as high as $135 billion, but due to strong ad performance and AI providing clearer returns on ad spending, $Meta Platforms (META.US)$ the stock price actually rose.

The concern for Google is that if CapEx jumps too sharply, depreciation and cost pressures will show up faster in the financials, which is also a worry that the market has repeatedly discussed recently. Some institutions currently forecast Google's 2026 CapExto increase to approximately $140 billion.。

How will the market price this? A continued increase in CapEx is not purely negative, but it must be accompanied bystrong evidence of returns from cloud business/advertising efficiency/new product monetization.Providing sufficiently strong "evidence of return." Otherwise, it would follow $Microsoft (MSFT.US)$ the path after the earnings release: no problem with growth,but 'excessive spending + insufficient return justification' directly triggered a revaluation.。

Three possible scenarios for post-earnings stock price movements and how to position options strategies.

Scenario 1: Bullish – Cloud business exceeds expectations + CapEx upward revision within expectations

– Trigger condition: Cloud business growth/margin exceeds expectations; CapEx is high but management provides a clear explanation of the financial return timeline.

– Market reaction: Valuation premium continues, stock price is expected to keep rising.

Scenario 2: Neutral – Advertising revenue and profits stable, cloud business in line with expectations, but CapEx significantly higher than expected

– Trigger: Revenue/EPS is solid, but CapEx guidance rises further, with less detailed disclosure from management on returns.

– Market reaction: Stock price may experience minor volatility, with gains or losses remaining within market expectations.

Scenario 3: Bearish – Cloud business underperforms expectations, cracks appear in advertising monetization efficiency

– Trigger: Cloud business falls below consensus; or Search/YouTube growth slows, shaking the foundation of the business model.

– Market reaction: Potential for larger-than-options-implied gaps, with volatility significantly greater than 6%.

Considering the different stock price scenarios, investors can strategize around earnings options accordingly:

Strategy One: Directional Strategy, suitable for those with clear bullish or bearish views

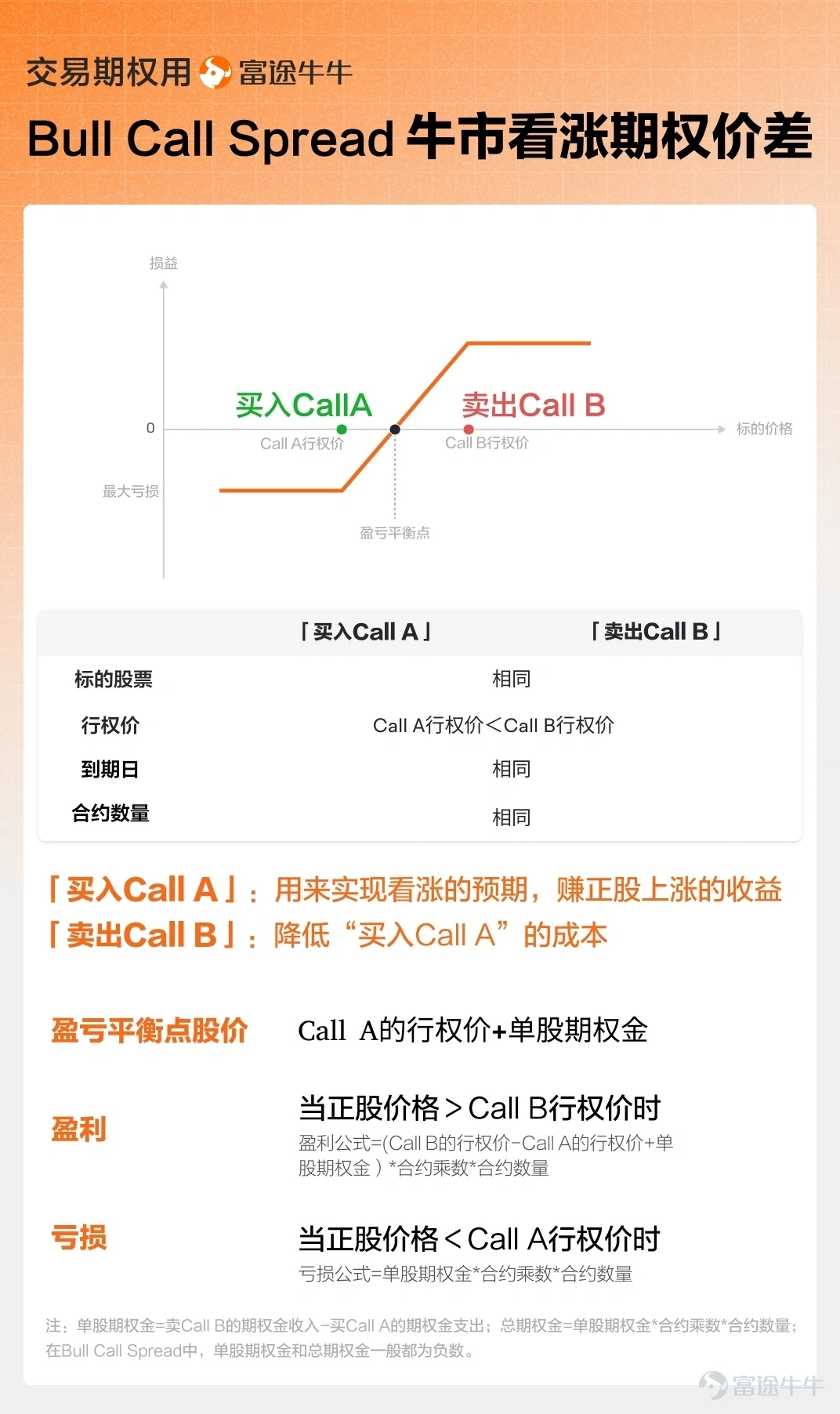

- Bullish:Bull Call Spread,This strategy has a lower cost compared to directly purchasing call options, but the potential profit is also capped, making it suitable for investors with directional views who prefer a more conservative approach.

- Bearish:Bear Put Spread,This strategy is constructed by buying a put option with a higher strike price while simultaneously selling a put option with a lower strike price. It is suitable for investors who are bearish on the market outlook but believe the decline will be limited, seek a higher risk-reward ratio, and prefer a more conservative style.

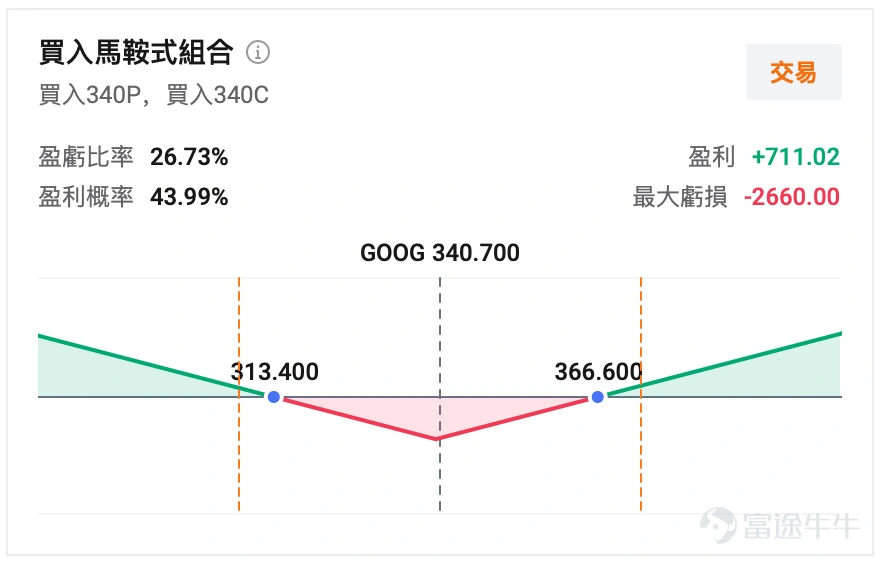

Strategy Two: Playing Volatility, anticipating larger-than-expected fluctuations after earnings, such as Long Straddle / Long Strangle,This strategy is built by simultaneously purchasing call and put options with the same expiration date. Characteristics of this strategy: No predefined expectation for the direction of stock price movement; profits can be realized as long as significant volatility (whether a large increase or decrease) occurs post-earnings and exceeds the break-even point. However, note that if the post-earnings fluctuation is small, there will be significant IV Crush, resulting in a sharp drop in option prices.

If you want more inspiration on options strategies, you can easily access it through the mobile app or the new desktop version by following the path below!

Finally, here's a small bonus for fellow investors. Fellow investors are welcome to claim it.Beginner's Options Package(This event is exclusively for invited HK users, click to learn moreDetailed event rules >>)

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (4)

to post a comment

49

48