Another earnings miss? AMD plunges over 17% post-results!

Can AMD's better-than-expected results break the valuation deadlock?

$NVIDIA (NVDA.US)$ competitor $Advanced Micro Devices (AMD.US)$ reported better-than-expected financial results for the December 2025 quarter.

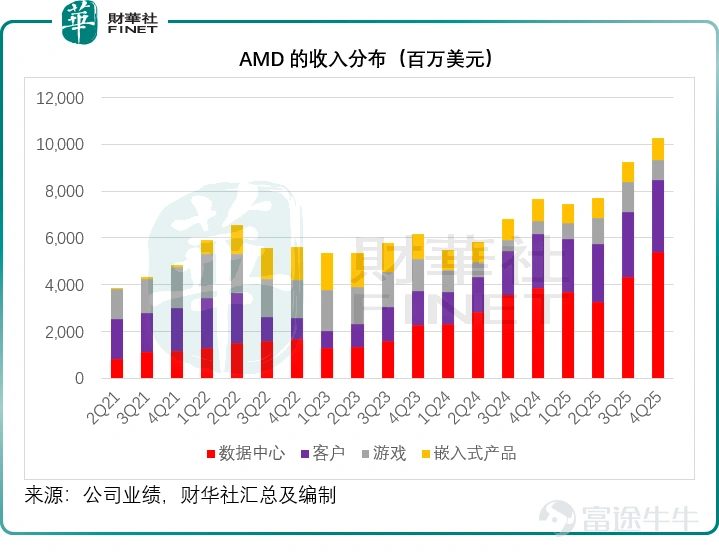

AMD’s financial results for the quarter ending December 27, 2025, showed that driven by AI chips, quarterly revenue from the data center segment increased 39.41% year-over-year to $5.38 billion. Both the client and gaming segments achieved strong growth, with quarterly revenues increasing 33.90% and 49.73% year-over-year to $3.097 billion and $843 million, respectively. Its total quarterly revenue rose 34.11% year-over-year to $10.27 billion, surpassing market expectations of $9.67 billion.

AMD’s operating profit margin for the data center segment continued to improve, with the profit margin for the December quarter increasing by 2.58 percentage points year-over-year and rising by 7.82 percentage points sequentially to 32.57%. This drove AMD’s fourth-quarter non-GAAP gross margin up by 2.95 percentage points year-over-year and 3.02 percentage points sequentially to 57.01%. The adjusted operating margin improved by 1.33 percentage points year-over-year or 3.58 percentage points sequentially to 27.79%.

Driven by robust revenue growth and continuous margin improvement, AMD’s non-GAAP diluted earnings per share increased 40.37% year-over-year or 27.50% sequentially to $1.53, surpassing market expectations of $1.32.

During its earnings call, AMD revealed that sales of its Instinct MI308 chip in China reached $390 million in Q4 and projected that its revenue from China this quarter would reach $100 million.

Nevertheless, after the earnings announcement, AMD shares plunged more than 8% during after-hours trading.

Why did AMD's stock price plummet after reporting better-than-expected earnings?

Including this forecast, AMD expects its Q1 2026 revenue to be approximately $9.8 billion, plus or minus $300 million. At the midpoint, this represents an annual increase of 32% but a sequential decline of 5%. The non-GAAP gross margin is expected to be around 55%. We speculate that part of the reason for the sharp drop in its post-earnings stock price might be related to a slowdown in revenue growth guidance for Q1 2026.

Further analysis shows that the sharp drop in AMD’s stock price after earnings was not due to a single factor but rather the result of multiple pressures, including structural concerns in its performance, gaps between market expectations, industry cycle adjustments, and valuation corrections.

From the perspective of earnings structure, the standout performance in Q4 may have been influenced by some temporary factors, raising questions about sustainability. Management disclosed during the earnings call that its quarterly gross profit included a $306 million gain from the release of MI308 inventory. Excluding this gain, its gross margin would be approximately 55%, not 57%.

In 2025, AMD’s stock price has surged by 75% cumulatively, and it has risen 13.05% year-to-date. In contrast, NVIDIA’s stock price has fallen 3.30% year-to-date, meaning AMD has outperformed NVIDIA in terms of stock performance this year, reflecting the market’s more optimistic expectations for AMD. Some analysts even predicted that AMD's quarterly revenue could exceed $10 billion, but its actual guidance fell short of this benchmark, which may also be one of the reasons for the stock price pullback.

Rising costs and external environment pressures have further heightened market concerns. In Q4, AMD's R&D expenses increased by 36.10% year-over-year to $2.33 billion, surpassing market expectations of around $2.2 billion. Selling and administrative expenses rose by 51.26% year-over-year to $1.198 billion. Non-GAAP operating expenses surged by 42% year-over-year to $3.001 billion, outpacing revenue growth, reflecting the company's ongoing cost pressures as it seeks to catch up with NVIDIA, advance chip iteration, and expand its market presence. Meanwhile, trade restrictions continue to impact its business, and the Q1 revenue forecast of $100 million from China is significantly lower than the previous quarter’s $390 million, indicating potential ongoing uncertainty in contributions from the Chinese market and raising questions about future growth drivers.

From an industry perspective, the AI chip sector is undergoing a phase of adjustment, with market tolerance for AI investments continuing to decline. Investors are now focusing more on profitability rather than just growth narratives. Recently, the S&P 500 technology sector has remained under pressure, with NVIDIA and other tech giants experiencing declines, reflecting that the market is reassessing the logic of high investment for high growth—investors are no longer blindly chasing AI-related stocks but are instead placing greater emphasis on the return prospects of capital expenditures. $Microsoft (MSFT.US)$ In this context, funds are shifting from highly valued AI chip stocks to more economically sensitive cyclical stocks, leading to sector-wide sell-offs. As a core player in the AI chip space, AMD naturally cannot remain unscathed.

In fact, not only did AMD's stock plummet, but NVIDIA's stock also fell nearly 3% overnight, once dropping over 5%, and was still slightly down 0.59% after-hours.

Notably, AMD is not entirely without long-term potential. The company’s competitiveness in the CPU market continues to strengthen, with client business growing by 33.90% year-over-year in Q4, far exceeding the global PC market’s growth of less than 10% year-over-year in Q4. Whether in desktop CPUs or server CPU segments, AMD has shown impressive performance, establishing a solid foundation.

At the same time, Lisa Su emphasized during the earnings call that the development progress of the MI450 series is proceeding extremely well, with plans for official release and mass production starting in the second half of this year as scheduled. The company maintains a very strong partnership with OpenAI and plans to gradually increase production starting in the second half, a process that will continue through 2027. She expressed confidence in overall data center business growth by 2026 and projected that by 2027, AI-driven data center operations could generate tens of billions in revenue. Additionally, major cloud providers are increasing their capital investments in infrastructure, indicating sustained long-term demand within the industry, which leaves room for AMD’s future growth potential.

Author: Wu Yan

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

2

1