Another earnings miss? AMD plunges over 17% post-results!

AMD's Mid-Year Battle: Strong Earnings Can't Hide Guidance Concerns, Market Awaits MI450 Launch in Second Half

Author | Eric

Global semiconductor giant $Advanced Micro Devices (AMD.US)$ After-hours Q4 earnings report released, after-hours stock price plunged 8%. Let’s dive into what exactly happened.

Three key highlights of the earnings report:

1. The Q1 sequential decline guidance fell short of market expectations, and the earnings release still needs to wait for the MI450 series volume increase in the second half of the year.

Many figures in AMD's 2025 Q4 earnings report initially appeared to surpass market expectations, but after excluding revenue from China's MI308, it did not exceed expectations by much. Moreover, AMD’s guidance for 2026 Q1 failed to show a sequential surge similar to AI memory stocks. $Micron Technology (MU.US)$ 、 $SanDisk (SNDK.US)$ Especially considering that AMD’s valuation is much higher than its competitors. $NVIDIA (NVDA.US)$ and $Broadcom (AVGO.US)$ This is also the main trigger for stock price volatility.

AMD expects Q1 revenue of $9.8 billion (including $100 million in revenue from China’s MI308), up 32% year-over-year but down 5% sequentially. Non-GAAP gross margin is 55%, up 1.3 percentage points year-over-year but down 2 percentage points sequentially. Non-GAAP net profit is $2.07 billion, up 32% year-over-year but down 18% sequentially.

AMD’s Q1 revenue guidance by segment: Data center business, represented by server CPUs, GPUs, and FPGAs, showed year-over-year and sequential growth, with both server CPUs and GPUs growing sequentially. Client business, represented by notebook and desktop CPUs, and gaming business, represented by gaming consoles and desktop GPUs, grew year-over-year but saw seasonal declines sequentially. $Tesla (TSLA.US)$ Embedded business, represented by Xilinx FPGAs and automotive chips, showed mild year-over-year growth but experienced seasonal declines sequentially.

From this perspective, AMD’s short-term earnings growth remains limited, and it still needs to wait for the volume increase of the MI450 series in the second half of the year. Management expects the MI450 series to start contributing revenue in Q3 and achieve large-scale volume production in Q4.

2. EPYC CPU performance was impressive, but management still did not provide full-year AI revenue guidance, only indicating data center growth of over 60%.

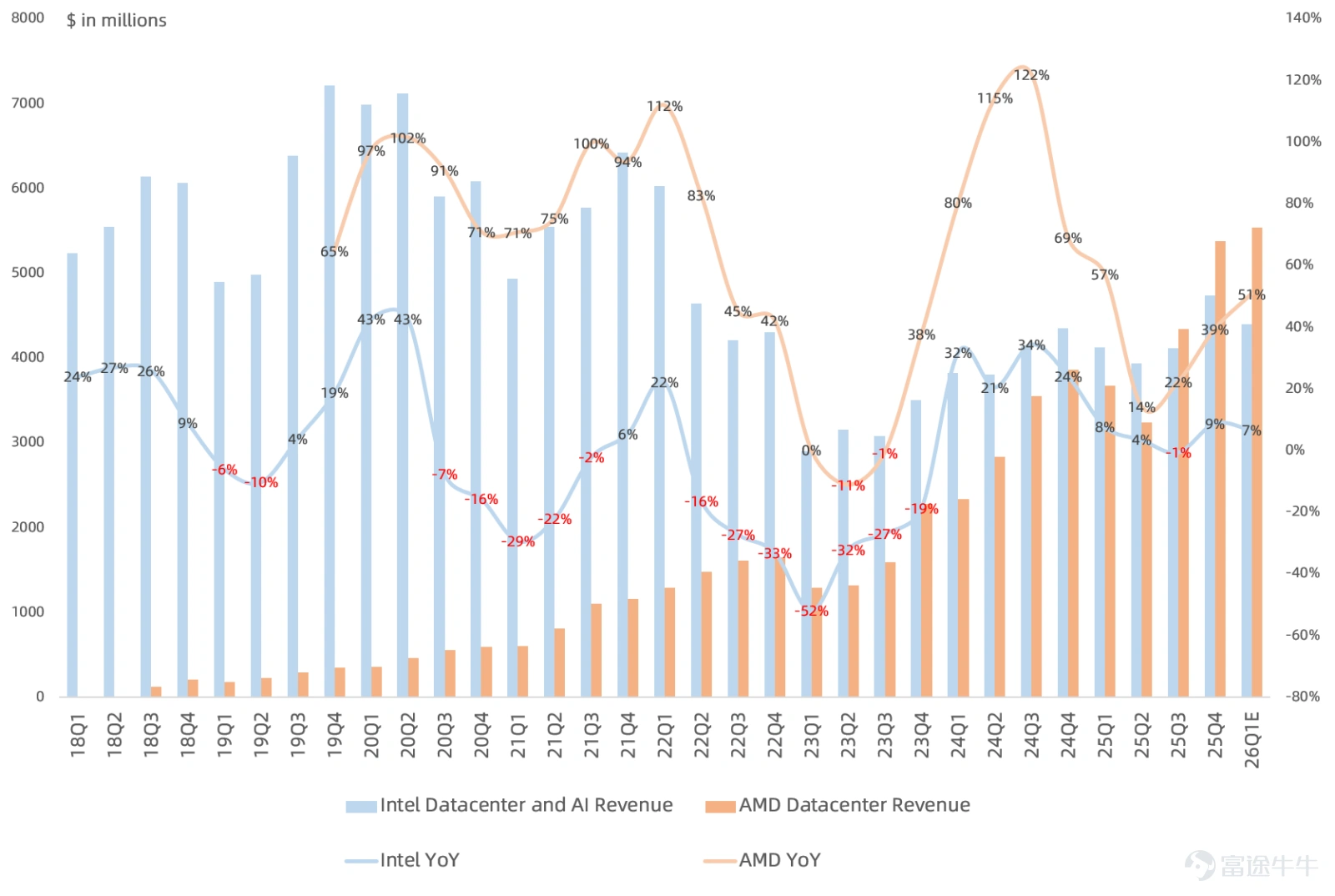

AMD's data center revenue for this quarter was $5.38 billion, up 39% year-over-year, with the majority still contributed by server EPYC CPUs. Adoption of Zen5 EPYC Turin CPUs accelerated this quarter, accounting for more than half of total server CPU revenue (approximately $1.5 billion). Demand for Zen4 EPYC Genoa CPUs remained strong as well. Revenue from server CPUs for cloud and enterprise customers hit record highs this quarter, with market share also reaching new peaks.

Management stated that customer demand for the 2nm Zen6 EPYC Venice CPUs, which are expected to enter mass production this year, is very strong. They believe that the overall server CPU TAM in 2026 will experience robust double-digit growth, reaffirming market views on the strong demand for server CPUs.

This quarter, data center GPU revenue reached new highs primarily driven by the ramp-up of the MI350 series. Among this, $3.9 billion in revenue was recognized from the Chinese MI308, and even after excluding MI308 revenue, growth remained positive quarter-over-quarter. In addition to its multi-generational partnership with OpenAI (6GW GPUs), active discussions are ongoing with other clients regarding large-scale, multi-year deployments starting later this year based on Helios and MI450.

The second half of the year will be a key inflection point for MI450, with related revenue starting in Q3 but seeing significant volume in Q4. The MI500 series is expected to enter mass production in 2027, equipped with HBM4E, using the CDNA6 architecture and a 2nm process. Management reiterated expectations for over 60% annual compound growth in data center business revenue over the next three to five years, reaching an annual revenue level of tens of billions of dollars by 2027. Although Lisa Su again did not provide AI revenue guidance for 2026 (what exactly is concerning them?), she provided guidance for over 60% growth in data center revenue for 2026, though the market understands that this still blurs the distinction between CPU and GPU guidance.

3. Rising memory prices lower the PC TAM for 2026; operating margin for client and gaming businesses declines significantly

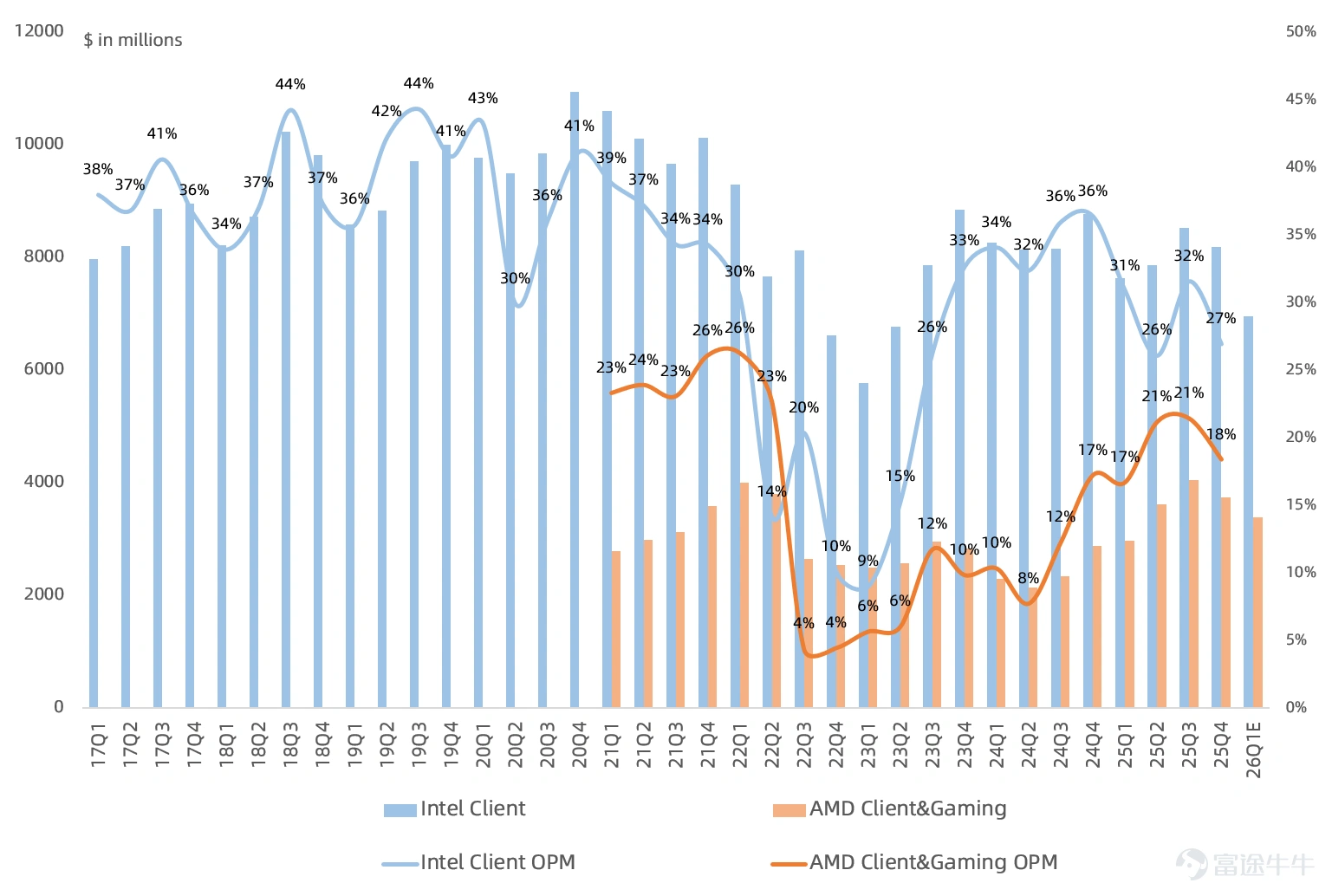

AMD has continued to gain market share in the PC sector in recent years. $Intel (INTC.US)$ Revenue from desktop CPUs hit record highs for four consecutive quarters in Q4. Ryzen endpoint shipments for notebooks also hit a record high this quarter, with commercial notebook and desktop Ryzen CPU endpoint shipments growing more than 40% year-on-year. However, AMD’s combined operating margin for client and gaming businesses in Q4 dropped to 18%, and like Intel, it has yet to return to the highs of 2021.

As the console cycle enters its seventh year, AMD's semi-custom business within its gaming segment is expected to see a significant decline in 2026. Management also noted that rising memory prices will lead to a slight decrease in the PC TAM for 2026, with the second half of the year being relatively weaker than the first half in a “non-seasonal” manner. However, management expressed confidence that the company's PC business can still grow even in a declining PC market, mainly due to its focus on the enterprise segment.

Q4 Key Financial Metrics

- Revenue of $10.27 billion, up 34% year-on-year and 11% quarter-on-quarter, including $3.9 billion in revenue from the Chinese MI308. Excluding this, revenue was $9.88 billion, higher than the market consensus of $9.65 billion, with prior guidance at $9.6 billion.

- GAAP gross margin was 54.3%, up 3.6 percentage points year-on-year and 2.6 percentage points quarter-on-quarter, surpassing market consensus of 53.1%. Non-GAAP gross margin was 57%, up 2.9 percentage points year-on-year and 3 percentage points quarter-on-quarter, exceeding both market consensus and guidance of 54.5%. This was primarily due to the impact of revenue from the Chinese MI308 and previously written-down inventory reversals. Excluding these impacts, the Non-GAAP gross margin was 55%.

– GAAP operating profit was $1.75 billion, up 101% year-over-year and 38% quarter-over-quarter, surpassing the market consensus of $1.65 billion; Non-GAAP operating profit was $2.85 billion, up 41% year-over-year and 28% quarter-over-quarter, exceeding the market consensus of $2.47 billion.

– GAAP net profit was $1.51 billion, up 213% year-over-year and 22% quarter-over-quarter, higher than the market consensus of $1.34 billion; Non-GAAP net profit was $2.52 billion, increasing 42% year-over-year and 28% quarter-over-quarter, surpassing the market consensus of $2.18 billion.

Q4 Core Segment Performance

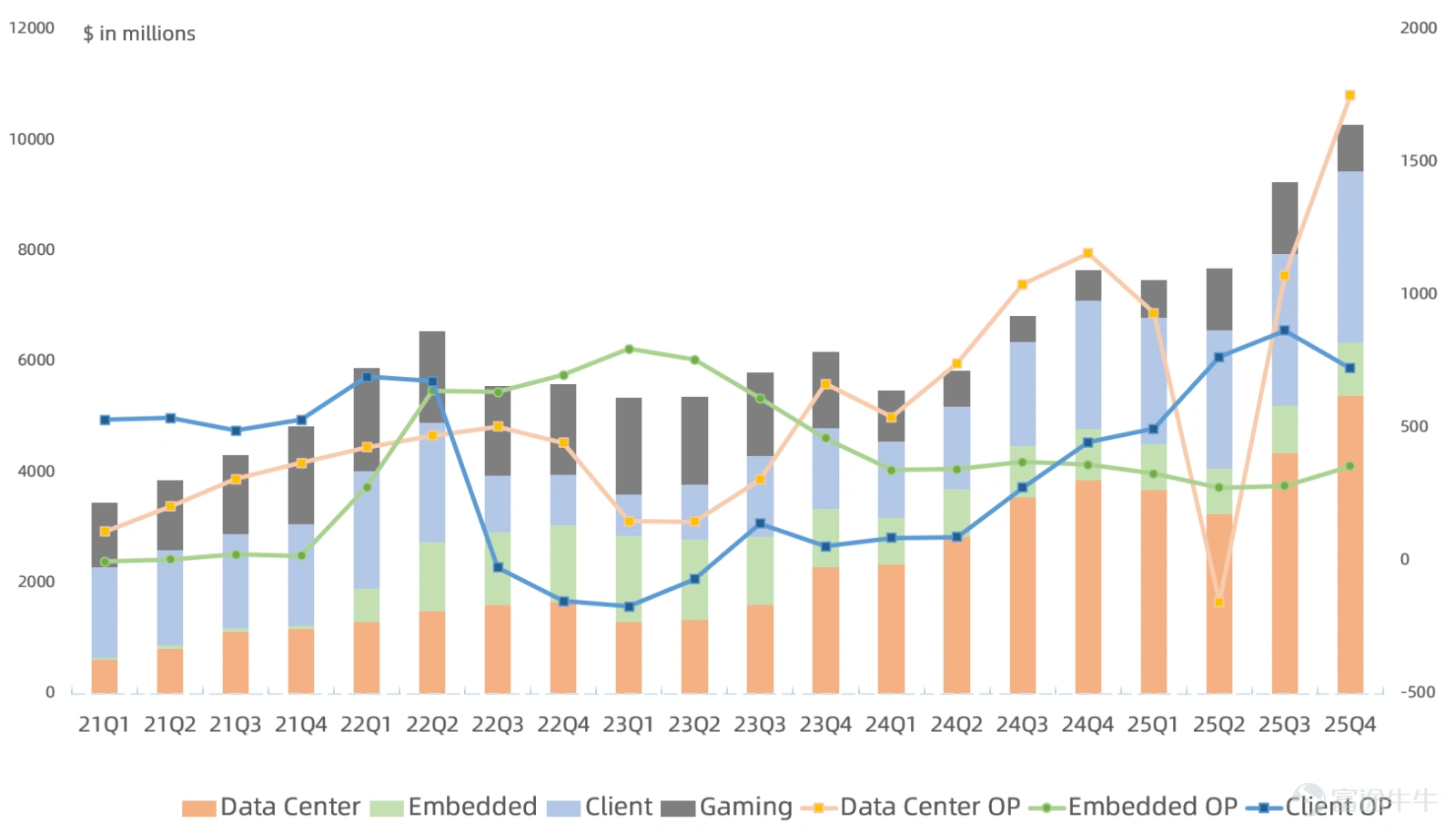

– Data center revenue, represented by server CPUs, GPUs, and FPGAs, reached $5.38 billion, up 39% year-over-year. Excluding revenue from MI308 in China, it amounted to $4.99 billion, slightly above the market consensus of $4.97 billion. Operating profit was $1.75 billion, with an operating margin rising to 33% due to the impact of MI308 in China, making this AMD's most profitable business this quarter.

– Client business revenue, represented by notebook and desktop CPUs, was $3.1 billion, a 34% year-over-year increase, surpassing the market consensus of $2.89 billion. Gaming business revenue, driven by gaming consoles and desktop GPUs, was $840 million, up 50% year-over-year but below the market consensus of $860 million. Combined operating profit for both segments was $730 million, growing 46% year-over-year, though operating margin declined by three percentage points sequentially to 18%.

– Embedded business revenue, represented by Xilinx FPGAs and Tesla vehicle chips, was $950 million, a 3% year-over-year increase, falling short of the market consensus of $960 million. Operating profit was $360 million, down 1% year-over-year, with an operating margin of 38%, still the highest among AMD's businesses.

Summary

Overall, the market had overly high expectations for AMD, hoping that its AI business would see NVIDIA-like or memory-like sequential growth. However, this still depends on the ramp-up of OpenAI’s MI450 series orders in the second half of the year. $Oracle (ORCL.US)$ The market currently underestimates AMD's reliance on OpenAI orders.

However, AMD’s EPYC server CPUs continue to erode Intel’s market share, serving as the anchor for AMD’s performance, especially given Intel’s constrained production capacity. This presents AMD with a golden opportunity, which will also determine whether AMD can smoothly navigate the earnings gap before the MI450 series ramps up.

牛牛Insights related historical articles:

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (4)

to post a comment

24

69