Waller's new policy measures are in the works! How should investors respond?

Gaozhan Weekly Interest Rate Analysis | The Fed Welcomes a New Leader! From Powell to Warsh, What Market Impact Will the Policy Shift Bring?

Issue 202602

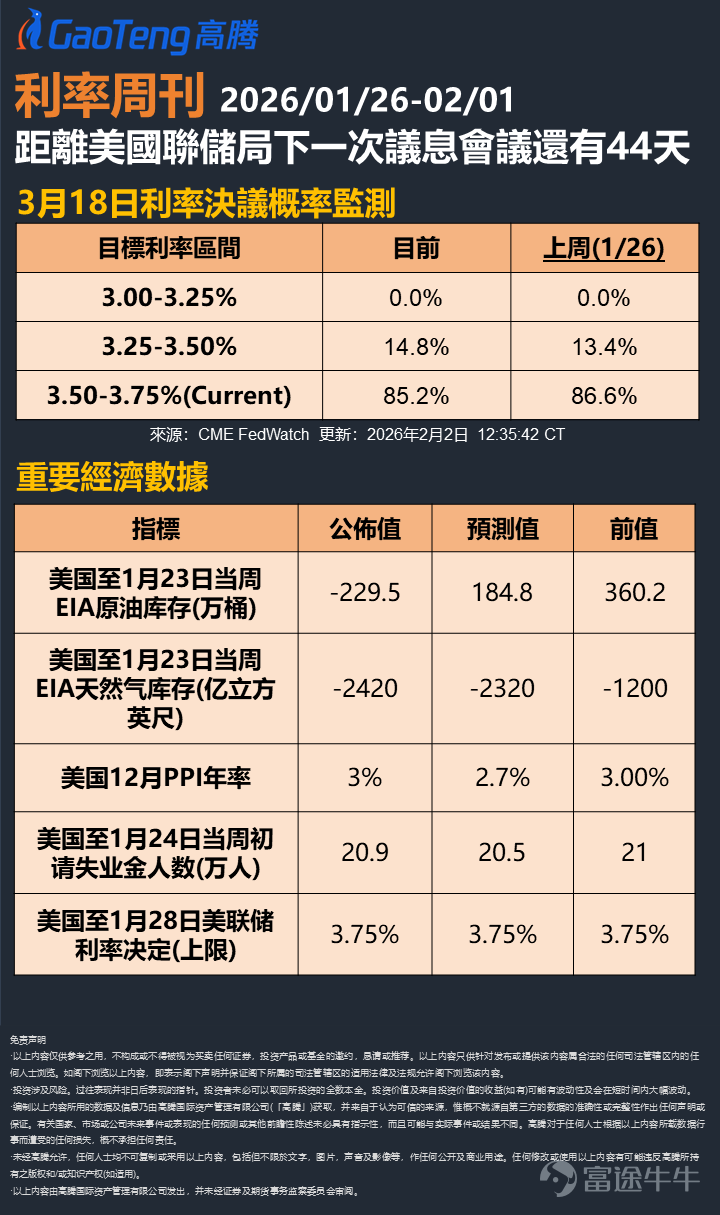

According to CME Fedwatch, the market predicts a 14.8% probability of the Federal Reserve cutting interest rates by 25 basis points on March 18, 2026, with an 85.2% probability of maintaining the current rate.

Controversy Surrounding Warsh's Nomination

On January 30, U.S. President Trump officially nominated former Federal Reserve GovernorKevin Warshto succeed Jerome Powell as the Federal Reserve Chair. Warsh served as a Federal Reserve Governor from 2006 to 2011 and was known for his "hawkish" stance during his tenure, though he has shifted his position in recent years, openly supporting Trump’s call for interest rate cuts.

On the same day,The U.S. Department of Justice disclosed 3 million pages of documents related to the Epstein case. Wash was reportedly on the guest list for the 2010 'St. Barts Christmas' event; neither the White House nor Wash has responded, further fueling public controversy. Doubts have arisen regarding his ability to uphold the independence of the Federal Reserve, with overnight reactions to his nominationPrecious metals market volatility and U.S. stock declines, while the dollar exchange rate and bond yields strengthened in response。

‘Trump’s spokesperson’?

Wash's core policy proposal is ‘Concurrent rate cuts and balance sheet reduction’:A plan to control inflation by reducing the Federal Reserve's balance sheet (QT), lowering bank reserve requirements, and creating room for interest rate cuts. Macquarie Group strategist Thierry Wizman pointed out, 'Wash is not the Fed’s spokesperson but Trump’s representative, having almost entirely followed Trump’s lead on monetary policy since 2009.'

However, policy implementation will be subject to internal checks within the FOMC. Wells Fargo Investment Institute’s Global Fixed Income Strategy Head, Reiling, emphasized, 'Interest rate cuts require majority support from the FOMC; the Chair only holds one vote. Wash will need to garner sufficient consensus, which presents a unique situation.'

Monetary Policy: Caught in a dilemma, expectations for interest rate cuts have cooled

Policy Remains Cautious:The Federal Reserve kept interest rates unchanged at 3.75%, ending three consecutive rate cuts. Powell emphasized that rates are at the 'upper end of the neutral range,' but internal divisions within the committee intensified, with two board members voting against the decision, advocating for a rate cut.

Market Expectations Revised Downward: Market expectations for the number of rate cuts in 2026 were reduced from three to two,with the first rate cut now expected in July rather than June. The US Dollar Index rebounded by 0.8% to surpass the 97 mark, the US Treasury yield curve steepened, and precious metals came under pressure. The Fed is caught between the dilemma of 'fighting inflation' and 'promoting growth', and the policy direction will depend on the pace of inflation’s decline and labor market resilience.

Amid policy uncertainty, stock, bond, and forex markets showed volatile divergence.

Equity Market: Volatile downward trend, tech stocks under pressure

- Trend:The Nasdaq Composite Index exhibited a 'rise-then-fall' pattern throughout the week, briefly approaching the high of 23,900 points mid-week, before closing at 23,461.82 points on Friday, accumulating a loss of 223.30 points, or a 0.94% decline.

-Driver:Profit-taking pressures on the technology sector intensified, compounded by fluctuating market expectations regarding the Federal Reserve's rate-cutting pace, triggering profit-taking sentiment among investors, leading to the index's pullback.

Chart: Nasdaq Composite Index performance from January 26 to February 1

Bond Market: Short-term yields strengthen, curve steepens

Trend:The US 10-year Treasury yield closed at 4.220% on January 30, down 0.018 points for the day, representing a 0.42% decline. The yield retreated slightly from its recent high of 4.267% but remains in the upper range of 4.2%-4.27%, oscillating at higher levels.

Drivers:Market concerns over the expansion of the US fiscal deficit persisted, compounded by ongoing reductions of US Treasury holdings by overseas central banks, which pushed yields up to 4.267%. A brief surge in safe-haven buying led to profit-taking, causing yields to pull back slightly.

Chart: Trend of U.S. 10-Year Treasury Yield from January 26 to February 1

Foreign Exchange Market: Stabilizes and rebounds

Trend:The US Dollar Index showeda 'first fall then rise' pattern for the weekTrend, early in the week once broke below the 97 level, FridayClosed up at 97.161, rising by 0.029 points, a gain of 0.03%, stabilizing after overall low-level volatility.

Drive:Fed's balance sheet reduction drives up long-end supply pressure; cooling rate-cut expectations boost the short end. Coupled with sluggish economic recovery timing in the Eurozone, temporary rebound in the market's demand for dollar safe-haven assets drove the index to bounce back from its lows.

Chart: Trend of U.S. Dollar Index from January 26 to February 1

Fundamentals of the U.S. economy

Energy Market: Sharp inventory drawdown, tightening supply-demand dynamics

Crude oil inventories plummeted:EIA crude oil inventory fell by 2.295 million barrels, far exceeding the expected increase of 1.848 million barrels, contrasting sharply with the previous rise of 3.602 million barrels. This reflects surging heating demand and increased refinery utilization driven by the cold snap. Crude imports dropped 7.7% year-on-year to 6.6 million barrels per day, shifting energy stockpiles from growth to decline and supporting oil price strength.

Accelerated natural gas inventory drawdown: Natural gas inventories fell by 242 billion cubic feet, a larger drop than the expected -232 billion cubic feet, marking the largest weekly decline in three years. WTI crude oil rose over 14% in January, but institutions predict that global crude oil inventories could exceed 2 million barrels per day by 2026, with long-term risks of oversupply still present, warranting caution against price pullbacks.

Producer-side inflation: PPI exceeds expectations, ongoing corporate cost pressures

PPI remains elevated: December PPI year-over-year at 3%, higher than the expected 2.7%. Core PPI increased 3.3% year-over-year, service prices rose 0.7% month-over-month, and wholesale prices for machinery and equipment climbed 4.5%, reflecting continued cost pressures on businesses. Some companies are gradually passing tariff costs to the production process, delaying rate cuts.

Manufacturing recovery: Durable goods orders rebounded strongly with a 5.3% month-over-month increase (expected 3.7%, previous -2.1%), factory orders also performed significantly better than expected at 2.7% month-over-month, while the Chicago PMI rose to 54 (expected 44), indicating a revival in production activities, though cost pressures will continue to affect consumers.

Dynamics of other major central banks

China: Maintaining liquidity stability

On January 29th, conducted a 354 billion yuan 7-day reverse repo operation, injecting a net 143.8 billion yuan to ensure ample liquidity before the Spring Festival; signed a renminbi clearing arrangement with the Central Bank of Sri Lanka, promoting the development of offshore renminbi markets.

Japan: Interest rate hike cycle begins

The minutes from the Bank of Japan's December 2025 meeting showed that members unanimously agreed that 'if the economy meets expectations, it would be appropriate to continue raising interest rates,' but emphasized that policy will remain accommodative. The market expects two rate hikes may occur in 2026, ending the negative interest rate policy.

Europe: Policy unchanged

The European Central Bank kept the main refinancing rate unchanged at 4.5%, stating in its announcement that 'inflation returning to target levels will take time.' It will continue full reinvestment of maturing bonds under the APP until the end of 2026.

UK: Hawkish stance

The Bank of England maintained the benchmark interest rate at 5.25% (with a 7-2 vote), emphasizing that 'a restrictive policy needs to be maintained to curb inflation.' Core CPI is projected to return to 2% by Q4 2026.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

6

3