A 2.1 billion impairment exit has unveiled the hidden truths of the online lending industry

Focus Media, a giant in the advertising industry, recently released several announcements that unexpectedly revealed the tough situation currently faced by the online lending sector.

According to a recent announcement by Focus Media, the board of directors has reviewed and approved relevant proposals. Its joint venture company, Shanghai Shuhe Information Technology Co., Ltd. (hereinafter referred to as 'Shuhe'), will repurchase 54.97% of the shares held by Focus Media for a total consideration of 7.91 billion yuan through domestic targeted capital reduction and overseas equity return. Focus Media has currently received the first payment of 4.04 billion yuan for this transaction, and Shuhe is no longer its associated company.

In short, Shuhe sold its 54.97% stake for a consideration of 7.915 billion yuan. After the transaction, it no longer holds shares or falls within the scope of associates.

The announcement also showed that Shuhe Technology, which ranks among the mid-to-upper level in the online lending industry, saw its performance in the fourth quarter of 2025 reverse downwards, with a net loss reaching about 6.84 billion yuan. The impact of the new regulations on loan assistance implemented in October last year is evident.

For Focus Media, this sale simply means giving up a previously lucrative business, and it will receive nearly 900 million yuan in investment returns. For the loan assistance industry, Shuhe, with about 50 billion yuan in outstanding loans, is now valued at less than 1.5 billion yuan, and the downward pressure on the share prices of various listed companies remains significant.

Shuhe Technology’s origins can be traced back to August 2015. Founder Xu Zhigang was previously in charge of China Merchants Bank's core product 'Palm Life', serving as the general manager of the credit card center operations department and the innovation business center. Most of the founding team had backgrounds from the credit card center of China Merchants Bank.

"Latte Finance" was one of their early smart investment advisory products. At that time, the domestic market was experiencing a wave of AI wealth management, with China Merchants Bank and several Ventures entering the field, but enthusiasm soon waned.

In February 2016, the company launched its flagship product 'Huanbei'—its early core selling point was 'credit card installment refinancing.' In other words, if your credit card interest payments were too high, you could avoid late fees by borrowing money from Huanbei at a lower rate to pay off your credit card, then repay Huanbei in installments.

Shortly after, in March, Focus Media, which was in the process of reverse merging with Seven Happiness Holdings, acquired 70% of Shuhe Technology for 100 million yuan via its wholly-owned subsidiary.

In September 2017, Focus Media transferred 100% of Chongqing Focus Microfinance Company, which had just been established and fully owned by Focus Media, to Shuhe Technology for 120 million yuan, enabling Shuhe to obtain an important internet microfinance license. In August 2025, Focus Microfinance significantly increased its capital from 335.5 million yuan to 800 million yuan. Financial reports also showed that in 2017 alone, Focus Media provided financial support of 443 million yuan to Shuhe to aid in its operational expansion.

Subsequently, through employee stock ownership, share transfers, and new investor capital injections, Shizhong Information's stake in He Technologies was diluted to 35.88%. However, after 2024, due to the capital reduction by other shareholders of He Technologies, Shizhong Information’s stake passively increased again to nearly 54.97%.

Notably, despite holding a majority stake for a long time, even up to 70% in the early stages, Focus Media has never sought nor attempted to revise the company's articles of association to gain control over He Technologies, consistently maintaining its role as a financial investor.

With the industry tailwind, He Technologies entered a high-growth phase starting from 2018. In 2019, He Technologies' total assets surged by 118.38% year-on-year, with revenue increasing by 205.92%.

By the first half of 2025, He Technologies reported operating revenue of 7.003 billion yuan, a year-on-year increase of 67%; net profit reached 631 million yuan, up 87% year-on-year; total assets rose to 16.374 billion yuan, and net assets climbed to 5.047 billion yuan. He Technologies expanded its business scope to include consumer credit, small and micro-enterprise credit, and installment services, with loans under management reaching 50 billion yuan at one point. The company holds dual licenses for online micro-lending and financing guarantees. Its app 'Huanbei' has cumulatively activated 170 million users, providing personal consumer credit services to 27 million users.

Although subject to significant discounts, overall, this investment has yielded quite impressive returns for Focus Media.

A simple calculation shows that the initial investment was 100 million yuan, and in the second year, part of the equity was sold for 120 million yuan. Now, exiting completely for 791 million yuan means Focus Media earned 811 million yuan from this investment, with an upfront payment of 404 million yuan already secured.

Of course, if measured before the implementation of the new loan assistance regulations, Focus Media's current gains would have significantly decreased.

According to the 'Asset Valuation Report' issued by Zhonglian Asset Appraisal, as of December 31, 2025, the book value of 54.97% equity in He Technologies, assessed using the market approach, stands at 2.944 billion yuan (unaudited), but the assessed value is only 782 million yuan, representing a valuation loss of 2.162 billion yuan, with a loss rate of 73.45%.

However, the enormous impairment of 2.162 billion yuan is essentially a numerical adjustment at the accounting level. Over the past few years, He Technologies has remained profitable, and Focus Media has gradually increased the equity value by including He Technologies' profits on its books according to its shareholding ratio. The announcement stated, "From 2019 to the third quarter of 2025, He Technologies maintained stable operations and sustained profitability, showing no signs of impairment." By the end of 2025, the book valuation of He Technologies held by Focus Media stood at 2.944 billion yuan. When the business logic changed and the assessed value dropped, the book value was corrected in one go during the impairment test.

Interestingly, in the first quarter of 2026, Focus Media will unexpectedly receive a windfall. According to accounting standards, the RMB 5.65 billion previously recorded in capital reserves due to the increase in Shuhe's valuation has been locked in the balance sheet. Upon completion of the transaction, the related capital reserve of RMB 5.65 billion will be transferred to current investment income, resulting in an increase of RMB 5.65 billion in attributable net profit.

Shenwan Hongyuan pointed out that Shuhe Technology has long contributed investment income, with a modest impact expected on apparent profits, but no effect on the company’s free cash flow. Based on historical financial statements, Shuhe Technology contributed approximately RMB 2.0-5.0 billion in investment income to Focus Media annually over the past five years. After Focus Media exits from Shuhe, a minor impact on apparent profits is anticipated. However, considering Shuhe Technology’s long-term lack of dividends, this only affects the book value of long-term equity investments and the investment income on the income statement, without impacting the company’s cash flow or its ability to continue paying dividends.

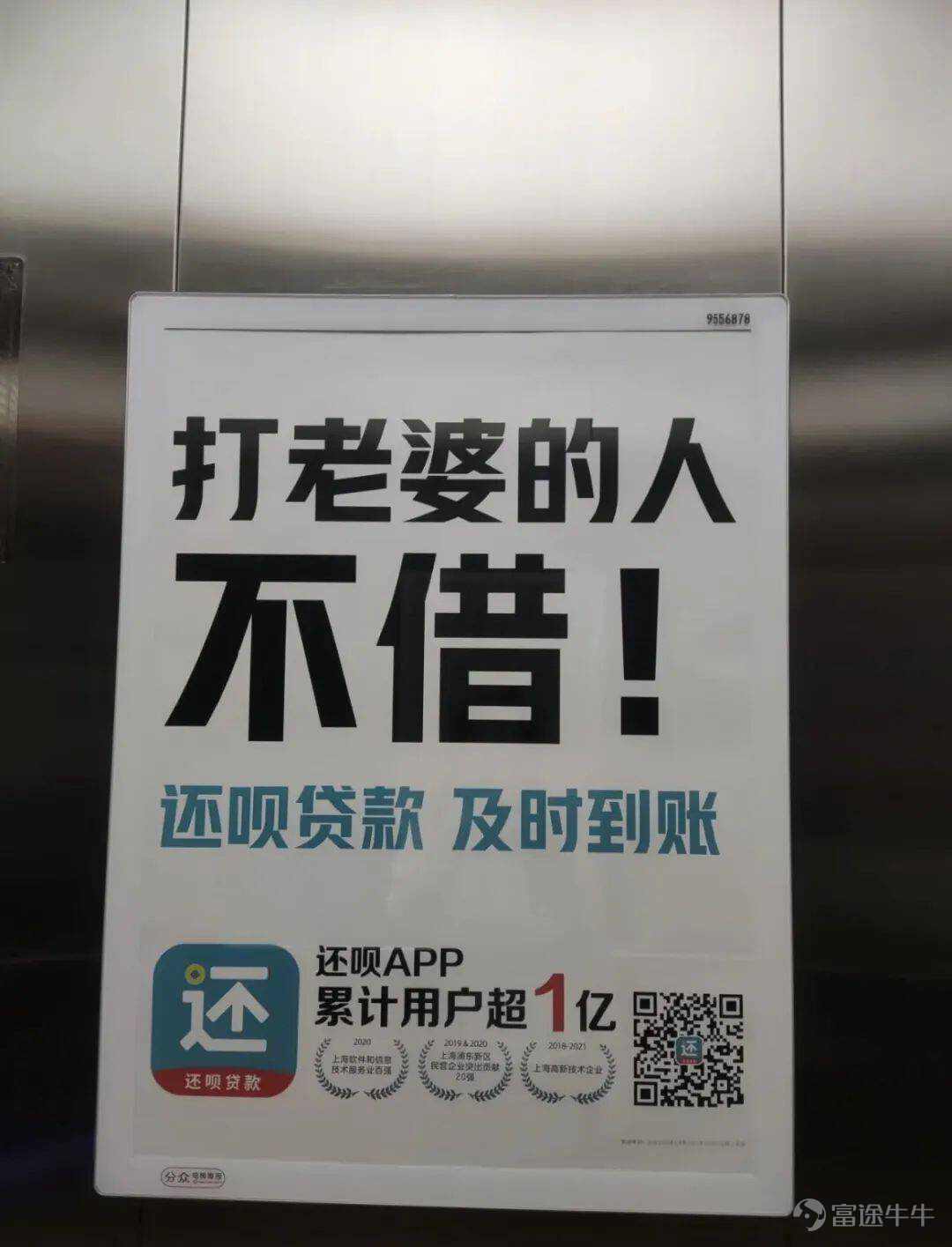

Notably, Focus Media also promoted 'Huanbei' through its core elevator advertising business, generating advertising revenue. According to Focus Media’s 2021 annual report, it received over RMB 93 million in advertising revenue from the related party, Shuhe Technology. This specific data was not listed in the annual reports for the following three years.

In 2021, a building advertisement by Huanbei through Focus Media, titled 'Wife-beaters need not apply,' sparked controversy.

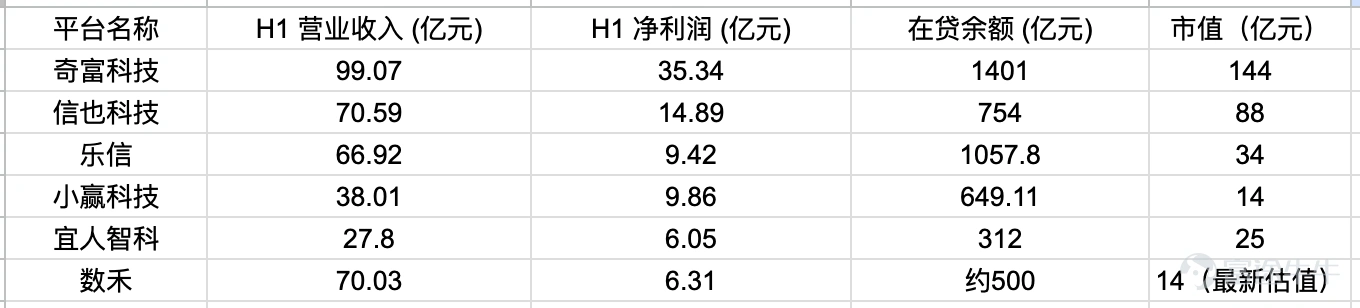

Comparison of key performance indicators for major online lending listed companies in the first half of 2025 versus Shuhe Technology

Although this sale may not be bad news for Focus Media, for the online lending industry, the impairment rate of 73.45% reflects a somewhat harsh industry sample.

Barron’s Chinese website summarized the key performance indicators for the first half of 2025 for various listed companies in the online lending industry, along with their closing market values on January 29, 2026 — it is worth noting that the current market values of most platforms are only one-third or even one-quarter of their peak levels.

Overall, Shuhe’s revenue performance is quite remarkable. With H1 revenue of RMB 7.003 billion, it is almost on par with Xinye Technology (RMB 7.059 billion) and even slightly higher than Lexin, placing it among the top tier of listed platforms.

However, Shuhe’s profitability efficiency ranks at the bottom among leading players. For instance, Qihu Technology generated RMB 3.5 billion in profits with RMB 9.9 billion in revenue; Xiaoying Technology achieved nearly RMB 1 billion in profits with RMB 3.8 billion in revenue. Despite having RMB 7 billion in revenue, Shuhe is left with only RMB 631 million in profits. This characteristic of 'high revenue, low profit' suggests that Shuhe’s customer acquisition costs or risk costs are relatively higher, which can partly explain why it suddenly turned to significant losses in the fourth quarter of last year.

From another perspective, the valuation of around 14 billion yuan for Shuhe Technology this time also sets a highly referential asset benchmark for the entire loan assistance industry. Using this actual transaction valuation as an anchor and comparing it horizontally with the data from several listed platforms in the first half of 2025, some platforms indeed face the risk of being overvalued.

For example, Xinye Technology's revenue in the first half of 2025 was 7.059 billion yuan, almost identical to Shuhe’s 7.003 billion yuan. Although Xinye’s profit (1.489 billion yuan) is significantly higher than Shuhe’s (631 million yuan), and its outstanding loan balance is larger, its market capitalization of 8.8 billion yuan is more than six times Shuhe’s valuation.

Another example is Yiren Zhike, whose net profit in the first half of the year (605 million yuan) was slightly lower than Shuhe’s (631 million yuan). Moreover, its outstanding loan balance (31.2 billion yuan) was only about 60% of Shuhe’s (approximately 50 billion yuan). However, Yiren Zhike's market capitalization reached 2.5 billion yuan, nearly 80% higher than Shuhe’s valuation from the transaction.

In contrast, Lexin and Xiaoying Technology have market capitalization logic closer to Shuhe’s. Lexin has an outstanding loan balance exceeding 100 billion yuan and a market capitalization of 3.4 billion yuan; Xiaoying Technology’s outstanding loan balance is 64.9 billion yuan, with a market capitalization of 1.4 billion yuan. The ratio of market capitalization to the scale of outstanding loans for these two companies is closer to Shuhe’s, reflecting to some extent that the market has partially accounted for their potential risk costs.(Author | Cai Pengcheng, Editor | Liu Yangxue)

For more in-depth analysis and exclusive insights on global markets, multinational corporations, and the Chinese economy, please visit

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment