Tech giants boost Capex again! What's the outlook for future stock prices?

High revenue and profits, but Apple's future looks uncertain?

On the evening of January 29, 2026, $Apple (AAPL.US)$ Apple reported its first-quarter financial results for the fiscal year 2026, ending December 27, 2025, with several core financial metrics showing significant year-over-year growth, marking the best quarterly performance in its history.

The business achieved coordinated growth in products and services, breaking through in multiple global markets. Continued progress was made in localizing the supply chain and advancing technology research and development, showcasing the operational resilience of the tech giant.

However, behind the impressive results, concerns over supply chain tightness are gradually surfacing. Coupled with structural capacity shortages in the industry, this has created uncertainties for future growth. Management's subsequent guidance also reflects anticipation and considerations for addressing potential risks.

All core financial indicators showed strong performance, with profitability efficiency continuing to improve.

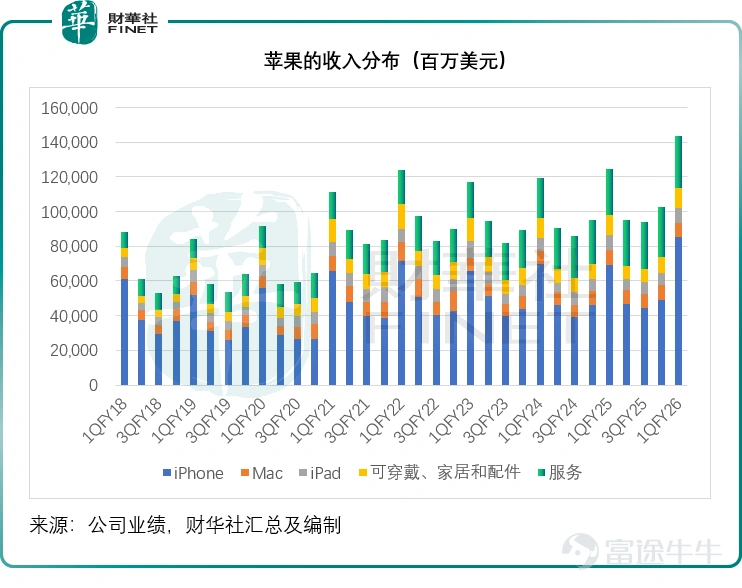

In the December quarter, Apple generated revenue of $143.76 billion, representing a year-over-year increase of 15.65%, setting a new record for its best quarterly growth. Revenue from iPhones surged by 23.33% year-over-year to $85.27 billion, also a record high, driven primarily by the iPhone 17 series.

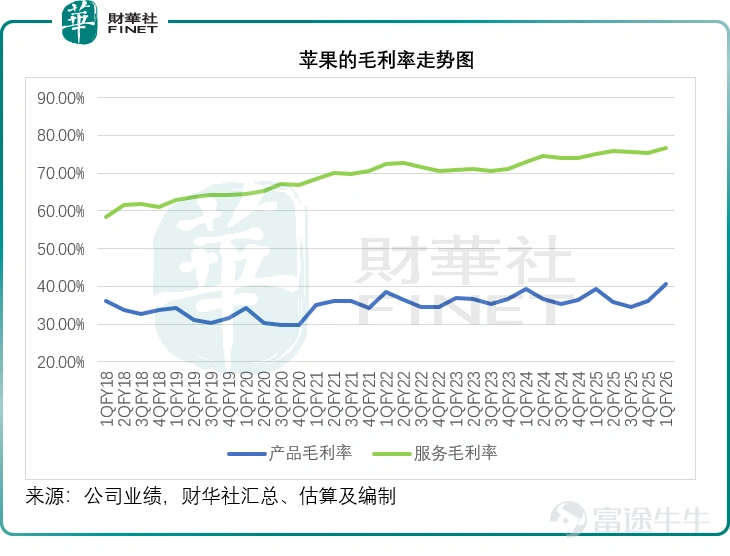

Its services division also hit a new high in quarterly revenue, growing 13.94% year-over-year to $30.01 billion, achieving record revenues across advertising, cloud services, music, and payment services. Both product and services divisions delivered strong gross margin performances, reaching 40.68% and 76.52%, respectively, increasing by 1.36 and 1.49 percentage points year-over-year. The company's overall gross margin rose by 1.28 percentage points year-over-year to 48.16%.

Benefiting from improved gross margins and operational efficiency, Apple's diluted earnings per share in the first quarter increased by 18.33% year-over-year to $2.84. In the first quarter, net cash flow from operating activities grew by 80.14% year-over-year to $53.93 billion. Apple's CFO noted that as of December 2025, Apple held $145 billion in cash and marketable securities, with total debt at $91 billion, resulting in net cash of $54 billion at the end of the quarter. The company returned nearly $32 billion to shareholders, including $3.9 billion in dividends and equivalents, and repurchased $25 billion worth of Apple stock, fulfilling its commitment to a cash-neutral position.

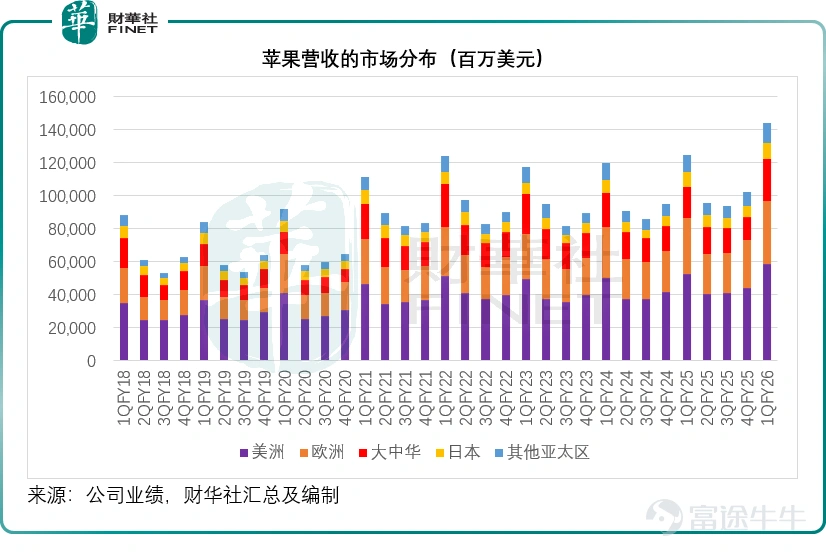

Comprehensive breakthroughs were achieved in global markets, with standout performances in emerging markets and Greater China.

In tandem with revenue and profit growth, Apple saw success across all global markets. During the earnings call, Cook stated that the December quarter set historical revenue records in the Americas, Europe, Japan, and other parts of the Asia-Pacific region, achieving growth in most tracked markets. Both emerging and mature markets demonstrated robust growth momentum, reflecting Apple's strong resilience on a global scale.

Greater China emerged as the most outstanding regional market during the period, with revenue growing by 37.88% year-over-year to $25.53 billion, significantly exceeding market expectations. This growth was primarily driven by the popularity of the iPhone 17 series, along with Apple's optimized channel strategies in mainland China, increased trade-in subsidies, and the introduction of localized features. Cook revealed that the number of iPhone upgrade users in Greater China reached a record high, while the number of switchers from other brands grew by double digits, indicating Apple's continued competitiveness in the premium market and strengthening user loyalty and brand appeal.

In emerging markets, Apple continues to maintain its growth momentum, with the Indian market achieving strong double-digit revenue growth and becoming a key incremental market for global growth. In recent years, Apple has continuously increased its production capacity and marketing efforts in India, gradually expanding local production to meet local market demands with tailored products, progressively unlocking growth potential in emerging markets, and injecting new momentum into long-term revenue growth. It has already opened five retail stores in India and plans to open another new store soon in Mumbai.

600 billion strategic investment implemented, advancing supply chain localization and technology R&D simultaneously

Cook emphasized that Apple’s previous commitment to invest $600 billion over the next four years in key industries such as advanced manufacturing, chip engineering, and artificial intelligence (AI) is steadily being executed, gradually building a more resilient supply chain system and technological moat.

The ongoing push for supply chain localization has become an important measure for Apple to hedge against fluctuations in the global supply chain: the new manufacturing plant in Houston has started delivering self-developed chip servers supporting Apple Intelligence, marking the transition of the server product line from overseas to U.S.-based production, providing computational power support for AI applications and private cloud computing; collaboration with Corning in Kentucky has achieved 100% localized manufacturing of cover glass for iPhones and Apple Watches, deepening upstream component localization; in the semiconductor field, partners $Micron Technology (MU.US)$ have broken ground on advanced packaging and testing facilities, with plans to purchase 20 billion U.S.-made chips by 2025, furthering the construction of an end-to-end silicon supply chain across the U.S. This move not only aligns with policies encouraging the return of U.S. manufacturing but also aims to enhance supply chain stability. Additionally, Apple has partnered with Michigan State University to establish a manufacturing institute, fostering a collaborative system between industry, academia, and research to support local technological innovation and production capacity implementation.

However, its localization strategy is still in progress and cannot fully alleviate pressures from global supply chain tensions in the short term. Moreover, the pace of capacity release for U.S.-based chip manufacturing and packaging remains uncertain.

On the technology development front, although Apple failed to deliver on its promise to enhance Siri functionality through AI by 2024, it is addressing gaps in AI capabilities through diversified collaborations, such as leveraging $Alphabet-C (GOOG.US)$ the latest Gemini 3 AI model, utilizing external technologies to strengthen its own AI competencies. Meanwhile, R&D related to Apple Intelligence continues to advance, forming synergies with hardware deployments in servers and chips, which could lead to breakthroughs in future AI terminal applications. However, management declined to disclose details of its collaboration with Google during the earnings call.

Future outlook remains robust, with supply chain tightness posing the main challenge

Based on the strong performance of the December quarter, Apple's management provided solid growth guidance for Q3 of fiscal year 2026 (March quarter), demonstrating confidence in future developments.

Management expects total revenue for the March quarter to increase by 13%-16% year-over-year, a forecast that already includes the best estimate for iPhone supply constraints; service revenue growth is expected to remain consistent with the previous quarter, maintaining steady momentum.

In terms of gross margin, it is projected to range between 48%-49%, showing a slight room for improvement compared to the December quarter, potentially signaling ongoing optimization of profitability. Operating expenses are expected to be in the range of $18.4 billion to $18.7 billion, roughly flat compared to the December quarter, with stable costs underpinned by increased R&D spending year-over-year, reflecting Apple’s continuous investment in technological innovation.

Supply chain tightness has become a core bottleneck constraining Apple's future growth. Regarding iPhone supplies, Cook revealed that strong demand coupled with tight advanced process node supply has driven channel inventory to extremely low levels as of the end of December. Current delivery cycles for some models have lengthened, and if production capacity cannot catch up in time, not only will the company miss out on growth opportunities from popular models, but user demand may also shift to competitors, weakening its share of the premium market—a risk that occurred in 2022 when component shortages for the iPhone 13 series cost Apple billions in revenue in a single quarter, highlighting the direct impact of supply constraints on profitability.

From the perspective of industry structural issues, the global shortage of advanced process capacity is not a short-term supply-demand mismatch. Taiwan Semiconductor’s 2nm process, even before mass production, has already been fully booked by giants like Apple, with lead times stretching into 2027. Other areas such as CoWoS packaging and high-bandwidth memory are also in dire straits, with this structural shortage expected to persist through 2026, directly affecting the iteration and production capacity of Apple's key products, including iPhones and AI servers.

The impact of a strained memory supply chain is gradually becoming evident. Management indicated that while the impact on the December quarter’s gross margin was minimal, it has clearly constrained profitability for the March quarter, an effect already incorporated into the 48%-49% gross margin guidance.

A sharp rise in global memory prices will directly increase hardware production costs. If Apple cannot pass on these cost pressures by raising product prices—given that pricing in the premium market is already near the threshold of consumer acceptance, price increases could suppress demand—it will directly squeeze product gross margins and weaken profitability. Regarding these risks, Cook mentioned considering various response options but did not disclose specific measures, leaving the effectiveness of subsequent actions yet to be seen.

Conclusion: Growth alongside strategic planning

Apple’s impressive performance in the December 2025 quarter is the result of optimized product portfolios, expanded market channels, and cost control capabilities working in tandem: the blockbuster effect of the iPhone 17 series drove hardware revenue growth, the high-margin nature of the services business continued to optimize profitability, global market breakthroughs broadened growth potential, and robust financial health provided support for strategic initiatives. Meanwhile, Apple’s efforts toward localizing supply chains, developing chips, and advancing AI strategies are long-term measures to address industry competition and supply chain volatility, though their success still requires long-term validation and cannot offset existing risks in the short term.

Objectively speaking, Apple’s current growth resilience coexists with potential risks. In the short term, the negative impacts of supply chain tightness will continue to unfold, with iPhone supply shortages potentially limiting sales growth and rising memory prices squeezing profit margins. If improperly managed, this could lead to weaker-than-expected results in subsequent quarters.

This record-breaking performance reflects Apple’s comprehensive strength, but it does not mean growth without challenges. How to resolve supply chain bottlenecks and balance short-term profitability with long-term strategy will be crucial for maintaining its leading position in the industry going forward.

Author: Wu Yan

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

4

1