Micron's earnings have doubled—explosive growth! Is it still a good time to jump into memory stocks?

SanDisk Q2 Review: Explosive Performance, Dynamic PE Around 10x, Multi-Year Agreements + Prepayments – Where Else Could It Be Revalued?

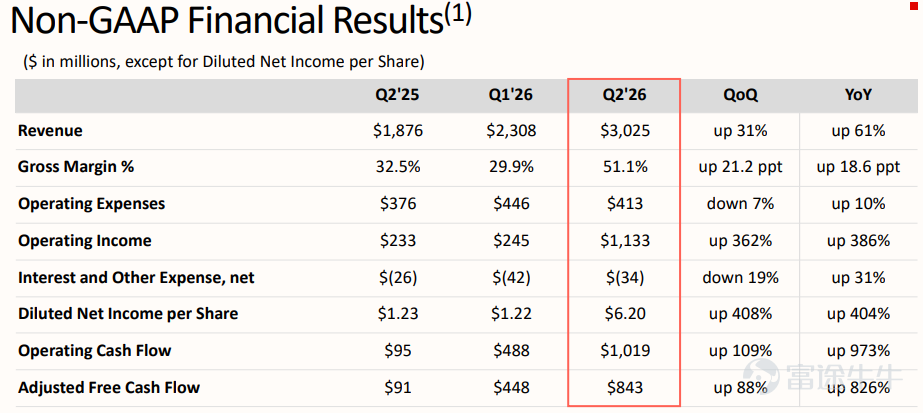

$SanDisk (SNDK.US)$ The FY2Q26 results and FY3Q26 guidance not only significantly exceeded the company's prior guidance but also surpassed Wall Street consensus expectations across the board.

But the bigger highlight is not just the exaggerated growth in profitability, but a strategic shift: the company is signaling that SanDisk’s narrative may be transitioning from 'volume-driven cyclicality' to 'stronger pricing power + increasing data center mix + tighter contract models (multi-year agreements + prepayments).'

Quick Performance Overview

This FY2Q26 beat was fundamentally driven byprice and mix,rather than 'volume expansion.'

– Revenue: $3.025 billion(Up 31% quarter-over-quarter, up 61% year-over-year)

– Non-GAAP gross margin: 51.1%, significantly higher than the company's previously provided41%–43%range. Management explained: the core contribution came fromhigher prices, and cost reductions were in line with expectations.

- Volume vs price: Bit shipments increased by only single digits quarter-over-quarter, butASP/GB (price per GB) rose mid-30% (over 30%)- Price was the main driver.

- Product structure: Data center revenue$440M, up from the previous quarter+64%, significantly outperforming other end markets.

Four key points to watch

1) FY3Q 'High Gross Margin Play': fewer bits, tighter supply, stronger profits

- FY3Q26 Guidance:Revenue $4.4B–$4.8B, Non-GAAP GM 65%–67%, Non-GAAP EPS $12–$14

- Company expectations:Q3 will be more undersupplied than Q2

- But at the same time, it indicates:Bits declined by mid-single-digit percentage quarter-over-quarter

Considering these points together, the meaning is very straightforward:Even with lower shipment volumes, pricing and structure must be strong enough to 'offset' the decline in volume. This differs from the traditional NAND rebound driven by volume recovery, resembling more of a 'phase-based regime shift'.

For a rough estimate: if we use the midpoint EPS of $13 as the basis for estimation, Q3 net profit will exceedUSD 2 billion, which annualizes to approximately8 billion USD. Based on the post-market capitalization of approximately 90 billion USD, the correspondingforward PE is around 11x。

2) Multi-year agreements + advance payments: Potentially rewriting the 'contract rules' in NAND

Management repeatedly emphasized: The demand driven by AI represents a step change (a step-like increase), shifting customer behavior from 'quarterly negotiations' to multi-year agreements。

The key point is that the company has clearly outlined the 'critical terms' of the multi-year agreements:Duration, pricing, volume, coverage, and prepayments.

More importantly, the company confirmed that it hassigned and completed delivery了for at least one agreement involving prepayment,and there aremultiple others in the pipeline.。

Why is this worth highlighting? Because 'price increases' can be cyclical, butcontract structuresonce altered, could lead to a shift in the valuation framework: if prepayments and multi-year commitments become the norm rather than exceptions, NAND cash flows might increasingly resemble 'semi-contracted infrastructure inputs' rather than 'quarterly auctioned volatile items'—visibility improves.The volatility discount (or even valuation discount) offered by the market may decrease.

3) 'Optional upside' in data center demand: exabyte forecast revised upwards three times, with KV cache not yet included in the base scenario

Management disclosed that its internal assessment of the growth rate of data center exabytes in 2026has been continuously revised upwards over three forecasting periodsto a high-60% range (above 60%).They also emphasized that in this earnings cycle's calculations,assumptions about further upward revisions to CapEx were not factored in.。

Regarding NVIDIA’s mention at CES of key-value (KV) cacheThe management has made it clear: this part of the demand.Not yet included.The current discussed demand figures.

Preliminary scale assessment: KV cache may beAn additional approximately +75–100 exabytes will be brought in 2027.In the following year, it may even be possible.Roughly doubled。

Conclusion - Key Increment: The data center line may hide another layer beyond the "baseline assumption."Additional uplink spaceIf these new inference/cache/storage demands start to be truly reflected in the orders and further enter into the multi-year agreement framework, the story tension will be stronger.

4) Supply-side lock-in: JV extended to 2034, stabilizing supply in the short term but introducing a COGS variable in the long term

The company extended its JV with Kioxia to December 31, 2034, and disclosed a significant manufacturing service commitment:

– Payment of $1.165 billion (USD 1.165B) for 2026–2029 (calendar years) to Kioxia’s manufacturing services

– This cost will be gradually reflected through **COGS (Cost of Goods Sold)** over the next nine years, starting now

In the short term, this appears more like a measure to ensure stability in a tight supply environmentLocking in supply certainty; in the long term, it will become a structural variable in the discussion of 'through-cycle margins' — because whether tight or not, this cost amortization path will persist underneath the model.

Conclusion

The strong profitability projected for FY2Q26 and FY3Q26 is only the surface; the deeper core lies in: the company is shifting the narrative from 'unit-driven cyclical fluctuations' toward 'pricing power + data center mix + a contractual framework of multi-year agreements (including prepayments)'.

Of course, the risks are clear: if supply tightness eases, customer bargaining power rebounds, or the spread of multi-year agreements underperforms expectations, then the 'reevaluation room' will be swiftly repriced.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (8)

to post a comment

22

90