Tech giants boost Capex again! What's the outlook for future stock prices?

Tesla Earnings Commentary: Non-Automotive Business Revenue Share Rises to 28%

Previously, $Tesla (TSLA.US)$The Q4 car sales have been announced with a significant decline, so market expectations were not high. The decrease in adjusted earnings per share after this adjustment was better than expected. In this earnings report, non-automotive business revenue accounted for 28%, compared to less than 13% in Q4 of 2022, indicating Tesla's declining reliance on car sales. Considering the higher profit margin in the energy business, the company’s overall profit dependence on automobiles has decreased more significantly.

Core Financial Indicators

Revenue:Tesla's fourth-quarter revenue was $24.9 billion, a year-on-year decrease of 3.14%.

Earnings per share:The adjusted earnings per share (non-GAAP) for the fourth quarter was $0.50, a year-on-year decrease of 17%. The adjusted earnings per share in the second quarter saw a year-on-year drop of 31%.

Segment split

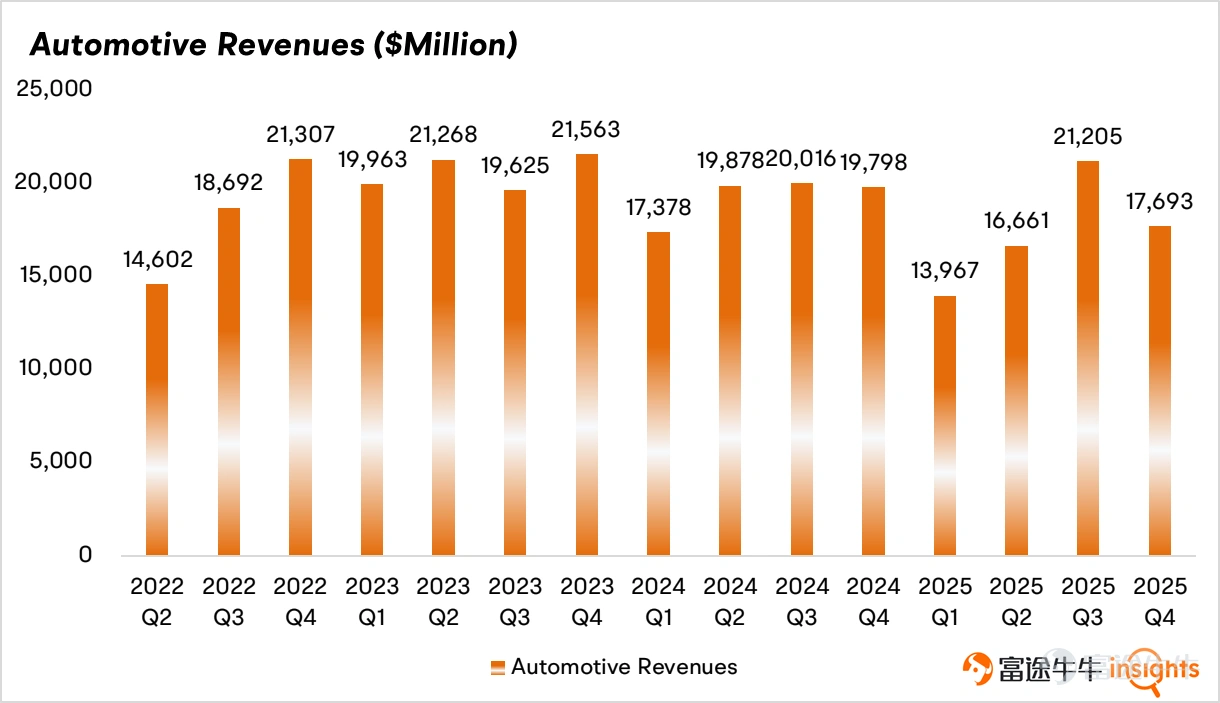

Automotive business (core pillar):

Q4 2025 automotive business revenue reached $17.693 billion, a year-on-year decrease of 10.6%. Compared with the previously announced 15.6% drop in car sales, the average selling price (ASP) actually increased, which aligns with the launch of the Model Y L in the second half of 2025 driving up ASP. Based on automotive business revenue and sales, the Q4 2025 ASP was calculated at $42,300, compared to $39,950 in Q4 2024. The automotive gross margin, excluding carbon credit sales, was 17.9%, exceeding market expectations of 14.1%.

However, with the launch of the cheaper version (referred to by Tesla as the standard version), there may be a scenario in the future where sales volume rises but the ASP decreases again. Additionally, the impact of the expiration of electric vehicle tax credits is expected to gradually diminish.

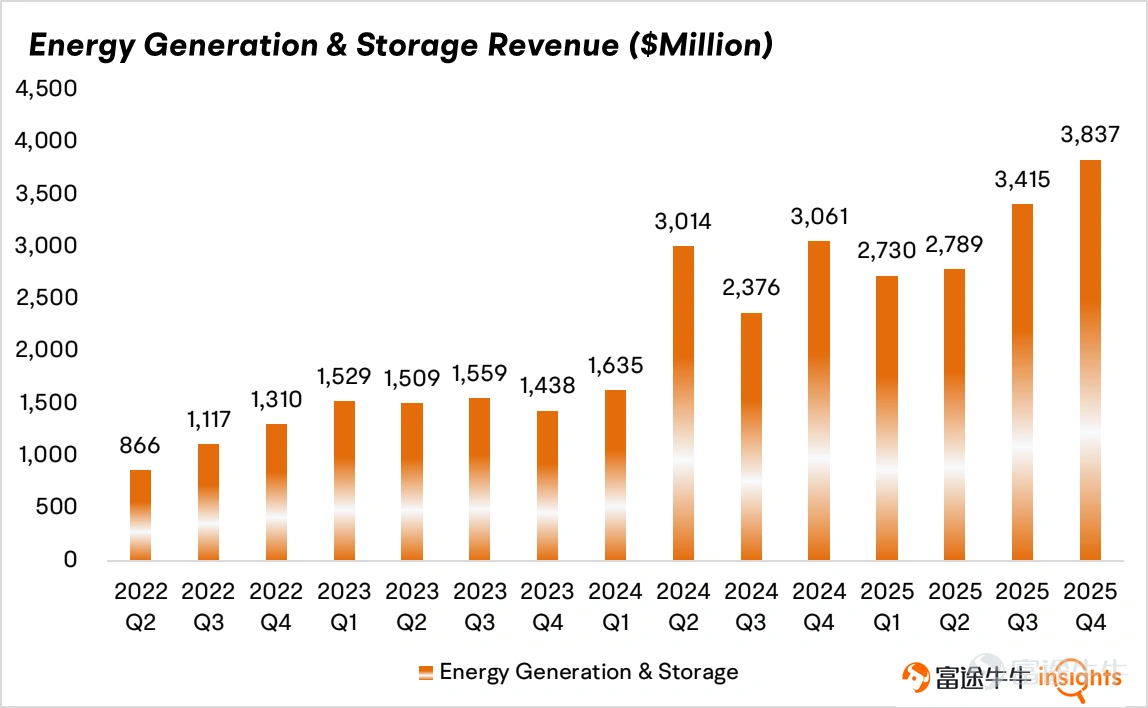

the energy business

This segment's revenue hit a new high, reaching $3.837 billion, a year-on-year increase of 25.4%. In terms of GW figures, Tesla previously announced that energy storage deployments increased by 29.1% year-on-year, indicating a slight decrease in unit prices. However, the Megapack 3, which is expected to be delivered in the second half of 2026 and offers a 28% increase in unit capacity, is anticipated to reduce lifecycle costs. Market forecasts suggest that the unit price of Megapack 3 will be higher than the previous generation, leaving room for further revenue growth acceleration.

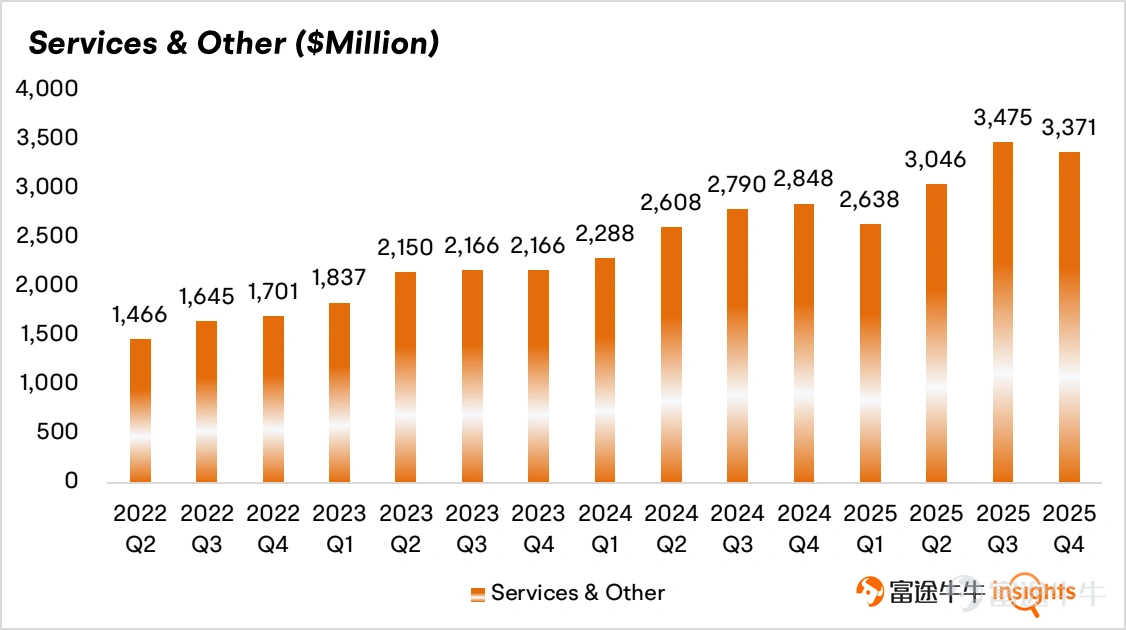

Service revenue

Revenue from this business segment increased by 18.4% year-over-year to $3.37 billion, but fell by nearly $100 million quarter-over-quarter. This decline may primarily be attributed to a drop in sales volume during the quarter, which led to a decrease in insurance business. Meanwhile, Tesla continues to expand its charging infrastructure. The number of Supercharger stations reached 8,182 this quarter, an increase of 429 from the previous quarter, while also preparing in advance for the expansion of Robotaxi services.

Management's statements on Robotaxi and Optimus

The company’s progress in FSD and Robotaxi is consistent with Elon Musk’s remarks at the Davos Forum, including the plan to begin testing unsupervised Robotaxi services in Austin by December 2025. The company disclosed for the first time the number of FSD subscribers, reaching 1.1 million by Q4 2025. Assuming Tesla transitions FSD to a subscription-only model at $99 per month, annualized revenue would reach $1.307 billion. The company reported that the number of subscribers doubled year-over-year, making FSD one of the fastest-growing segments. Given the low marginal cost of software businesses, the market tends to assign a higher valuation to this segment.

The company also revealed that the unsupervised version of FSD began pilot testing in South Korea in Q4 2025. Additionally, "commercial operation of unsupervised Robotaxis" has been included as a performance metric in the CEO’s bonus evaluation. FSD version 14 has introduced more comprehensive driving assistance features, including parking space search and automatic parking functions.

In terms of robotics, Tesla reported significant upgrades to Optimus in 2025, including the latest hand design. The third-generation Optimus Gen-3 was described as the first design aimed at mass production. However, this information had already been repeatedly communicated to the market.

Tesla announced a framework agreement with Elon Musk’s artificial intelligence startup xAI. The company agreed to invest approximately $2 billion in xAI’s Series E preferred shares. The transaction is subject to standard regulatory conditions and is expected to close in the first quarter of 2026.

Summary

Overall, Tesla's earnings report exceeded market expectations. Key areas to watch going forward include the mass production timelines for new products such as Optimus 3 and Cybercab. Following the release of the earnings report, the stock price rose by more than 2%.

– Valuation:

Tesla's current P/E ratio exceeds 290x, placing it at the 76th percentile over the past five years.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (2)

to post a comment

7

20