Tech giants boost Capex again! What's the outlook for future stock prices?

Meta Q4 Review: Why the Market Isn't Fazed by Full CapEx? Meta Stabilizes Valuation with One Key Statement

$Meta Platforms (META.US)$ Q4 earnings report conveys a strong narrative: advertising revenue is expected to accelerate further, driven by both volume and price. Moreover, while management increased the investment intensity (Opex/CapEx) target for 2026, they also presented a stronger growth outlook. A key statement alleviated market fears over the potential 'ROI collapse' narrative — the company forecasts that its operating profit in 2026 will exceed that of 2025.

Financial Highlights

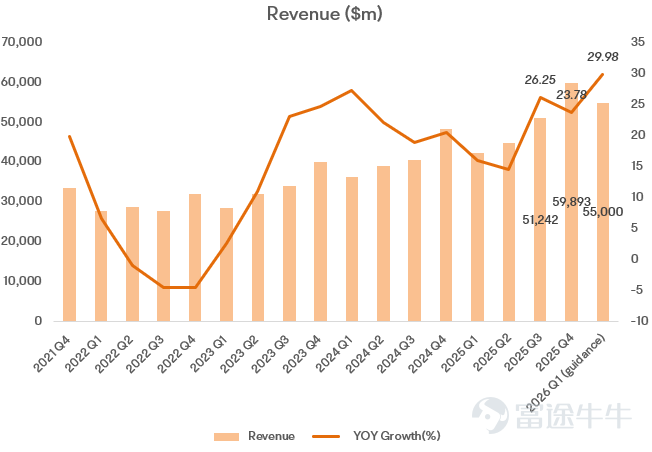

– Revenue: $598.93 billion, up 24% year-over-year

– Total costs and expenses (Total costs & expenses): $351.48 billion, up 40% year-over-year; the cost curve continues to steepen, primarily reflecting AI talent investment + R&D intensity + infrastructure load 's combined impact

– Operating profit (Operating income): $247.45 billion, corresponding to 41% 's operating margin

– Net income: USD 22.768 billion, up 38% year-over-year

The most noteworthy point

1) Why is the market no longer panicking despite higher Opex / CapEx?

Capital expenditures (CapEx) and expense guidancewere the focus of this discussion:

– Q4 CapEx: USD 22.1 billion (indicating that there is still some sense of short-term 'speed control/scheduling')

– Full-year 2025 CapEx: USD 71.4 billion

– The market had previously expected some sell-side analysts to forecast 2026 CapEx: Approximately 110–120 billion USD (roughly corresponding to a year-over-year increase of +53% to +71%)

– The management's final guidance for 2026 CapEx:115–135 billion USD (corresponding to a year-over-year increase of approximately +61% to +89%)—Higher than many investors' original 'psychological anchor'

– 2026 Total Cost Guidance:162–169 billion USD,compared to Total costs in 2025 of 117.69 billion USD, implying a year-over-year increase of approximately +38% to +44%

But the market wasn't directly crushed by the 'increased investment,' for two core reasons:

(1) Stronger short-term growth: Q1 revenue guidance reinforces that the advertising engine is still performing above expectations.

Company GuidelinesQ1 2026 revenue of $53.5–56.5 billion, implying closenessapproximately 30% year-over-year growth, which falls on the faster end of recent growth ranges. For equity investors, what they fear most is not spending money, but 'spending without seeing any progress.'

(2) The biggest concern was partially defused in one sentence: management clearly stated that operating profits in 2026 will be higher than in 2025.

This shifts the boundary from 'whether investments are out of control' back to 'whether investments can be covered by revenue and monetization.' Even if free cash flow (FCF) may still face pressure under massive CapEx, the certainty signal from the income statement helped stabilize the valuation framework on the earnings night.

2) AI CapEx ROI: What 'quantifiable clues' did management provide?

Meta this time presented the closed-loop of 'AI → better recommendations → increased engagement → stronger monetization' more as an engineering discipline rather than just a slogan.

The advertising base remains healthy (both volume and price are rising):

– Ad impressions: Year-over-year +18%

– Price per ad: Year-over-year +6%

Examples from the product side:

- Instagram Reels viewing time in the US: Year-over-year +30% or more

- Optimization on Facebook brings: Organic Feed/video views +7%(referred to as 'the Facebook product launch combination with the biggest impact on quarterly revenue in two years')

- Threads usage duration: Q4 +20%

- Instagram US recommended content structure: approximately 75% from original posts (an increase of about +10 percentage points)

Several key points from Zuckerberg’s prepared remarks:

– 2026 ‘AI Acceleration’: particularly as Agents begin to be implemented in products and internal efficiency improvements

– Technical roadmap: deeper integration of LLMs with recommendation systems and advertising systems; he noted that the current system is 'still very primitive compared to future possibilities'

– Commercialization direction: Agentic shopping (AI-driven shopping) + deeper integration with business messaging/WhatsApp

– Hardware focus: AI glasses are positioned as the 'ultimate interface,' and it was noted that glasses sales last year saw more than triple growth

– Infrastructure strategy: Emphasizing 'Meta Compute,' with greater focus on proprietary silicon and energy efficiency; it was also mentioned that as optimizations and supply chain maturity improve, cost per unit of computational power per unit of electricity is expected to decline (even pointing out that the 'cost per gigawatt' will decrease with engineering optimization)

3) Reality Labs continues to be a drag, but the phrase 'approaching peak' is very significant

Performance by segment:

– Family of Apps (FoA): Revenue USD 58.938 billion; Operating profit USD 30.766 billion

– Reality Labs (RL) : Revenue USD 955 million; Operating loss -USD 6.021 billion

The key focus is on the marginal changes indicated by management: RL's investment is increasingly concentrated in glasses/wearable devices; and management stated that RL’s losses may be similar to last year and are 'very likely close to peaking', which is expected to gradually narrow over time. For valuation, 'widening losses' is a typical risk multiplier; whereas 'peaking losses followed by convergence' would significantly improve the market's tolerance for long-term investment.

Next narrative inflection point: What is the market most focused on?

From the perspective of 'changing the narrative,' what investors are most focused on, according to Bull Insights, is Zuckerberg’s mention of 'a significant acceleration in AI development in 2026.' If this can translate into clearer AI-drivenexpectations regarding user engagement growth, monetization models, and growth potential (entry points such as models, agents, social IM ecosystems, traffic),the stock price reaction could be more positive.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (7)

to post a comment

23

62