Micron reports earnings after the market close on Wednesday—could the sharp pullback present a buyin

Earnings Options Strategy | Storage Giants Go Head-to-Head on Earnings Day! What to Watch for in Sandisk's Report Amid Strong Expectations and High Pricing?

$SanDisk (SNDK.US)$ SanDisk is set to release its earnings report after market close on January 29 EST. After delivering a total return of 559% in 2025, making it the best-performing component of the S&P 500 Index, SanDisk has once again taken the lead in early 2026, nearly doubling in value with a year-to-date return of 98%. No company in history has ever managed to secure the top performance spot in this index for two consecutive years.Given the current frenzy in the storage market, market sentiment is in a delicate tug-of-war between 'strong expectations and high pricing.' Close attention to this earnings report will be pivotal in validating the storage investment thesis.

Institutional forecasts predict that SanDisk will achieve revenue of $2.676 billion in Q2 2026, slightly above the upper limit of the company’s previous guidance of $2.65 billion.;Earnings per share are expected to reach $3.126.In addition to SanDisk, other storage giants such as Samsung, SK Hynix, and Western Digital will also release their earnings reports on the same day.

Having doubled since the start of the year, NVIDIA’s CES speech once again highlighted key insights.

SanDisk was spun off from Western Digital in February 2025 as a pure-play NAND flash memory business. Its products have directly benefited from the massive data storage demands generated by hyperscale data centers for training and deploying artificial intelligence models.

The main driver of this cyclecomes from the mismatch between strong demand growth and limited supply expansion.In addition to strong demand for AI servers, the recovery of the general server market is also a key driver. Looking back at the situation in 2025, we can see that the memory market was largely supplier-driven, with suppliers having greater bargaining power in pricing negotiations due to product shortages.

The direct catalyst for this round of market activity at the beginning of 2026 came from $NVIDIA (NVDA.US)$ CEO Jensen Huang's speech at CES,NAND was the most surprising part.This shift in logic further fueled SanDisk's growth expectations, catalyzing a surge of approximately 30% in its stock price after CES.The newly added 'Inference Context Memory Storage Platform' (ICMS platform) reduces the original pressure on HBM by utilizing NAND as an 'external memory.' In layman's terms, NAND has been upgraded from a cheap data warehouse to an expensive 'external brain' for AI, evolving from traditional 'cold storage' into a 'secondary cache/long-term memory' for GPUs.

SNDK's market share in NAND is actually not very high, ranking fifth globally, but compared to other companies in the industry, SNDK is more focused on this sector. This also allows SNDK to lead the storage segment when the focus of the storage industry shifts.Despite $Western Digital (WDC.US)$ 、 $Seagate Technology (STX.US)$ and $Micron Technology (MU.US)$ Other companies in the storage industry also saw their stock prices rise, but none matched SNDK’s gains.

Core focus: Verifying whether AI can revalue storage

The highlight of this earnings report is not simply data that “exceeds expectations,”but rather whether management can confirm a structural shift: Can NAND evolve from a mere 'storage medium' into a key component during the AI inference phase?Moreover, the market will closely watch its Q3 performance guidance and whether management's positive outlook on long-term trends continues.SNDK's three main business segments are data center, edge, and consumer businesses.

1. Data Center: Revaluation from 'supporting role' to 'AI inference layer'

This is the biggest source of expectation differential in this earnings report,the core of SNDK’s high valuation. Although the data center business accounted for only 11.66% last quarter, it has shown the fastest growth rate, and withAI Computing PowerTightly linked. Following Jensen Huang of NVIDIA's introduction of the ICMS concept, SNDK’s SSDs are no longer just simple cold storage but have become 'external GPU memory' in AI inference processes.

The market will focus on management's guidance regarding visibility of enterprise SSD (eSSD) orders. AI storage solutions targeting top cloud service providers represent a potential opportunity for market share growth. If these materialize progressively from this quarter to the next, it will improve the growth trajectory of this business. If SNDK can confirm entry into the supply chains of leading cloud vendors this quarter, its valuation logic will shift from being a traditional storage cyclical stock to becoming an AI infrastructure stock.

2. Supply discipline and profit elasticity

Institutions like Bernstein predict that the ASP uptrend for NAND will continue until 2027, which is a long-term positive. However, as a cyclical industry, investors must also be wary of the ' reflexivity of a supercycle.' The barrier to expansion in the NAND industry is relatively low. Compared to the oligopoly in the DRAM sector, the competitive landscape in the NAND market is more fragmented. Amid the 'prisoner's dilemma,' manufacturers generally adopt a defensive stance of 'if you don’t move, I won't move,' fearing unilateral capacity expansion could trigger a price war.We need to confirm during the earnings call whether the company has maintained strict capital expenditure (Capex) discipline amid improving profits. This is crucial for determining how long the cycle can last.

The guidance provided by the company last quarter for Q2 Non-GAAP gross margin was 41%, a significant jump from 30% in Q1.Profit improvement in the previous quarter reflects recovery driven by price increases and structural optimization. For this quarter, the market expects a gross margin of 42%, close to the company’s guidance. If pricing discipline continues and manufacturing and supply chain efficiency improvements persist, EBIT and earnings per share are expected to rise simultaneously, potentially delivering surprises under the influence of operating leverage.

3. Edge and client-side business: Testing the resilience of the cash cow

As the base of revenue (accounting for about 60%), the edge and client-side business acts as SNDK's safety net.Performance in this segment heavily relies on the global consumer electronics replacement cycle.

Although this sector lacks an appealing AI narrative, 'volume-price balance' is the key focus. Whether channel price hikes over the past two quarters can be successfully passed on to end customers, and whether the average selling price (ASP) in mainstream capacity segments can remain stable, will directly determine the company's gross margin foundation. We need to closely monitor the increase in the proportion of high-capacity products within the product mix, which is not only crucial for offsetting seasonal fluctuations but also provides upward momentum for single-quarter gross margins.

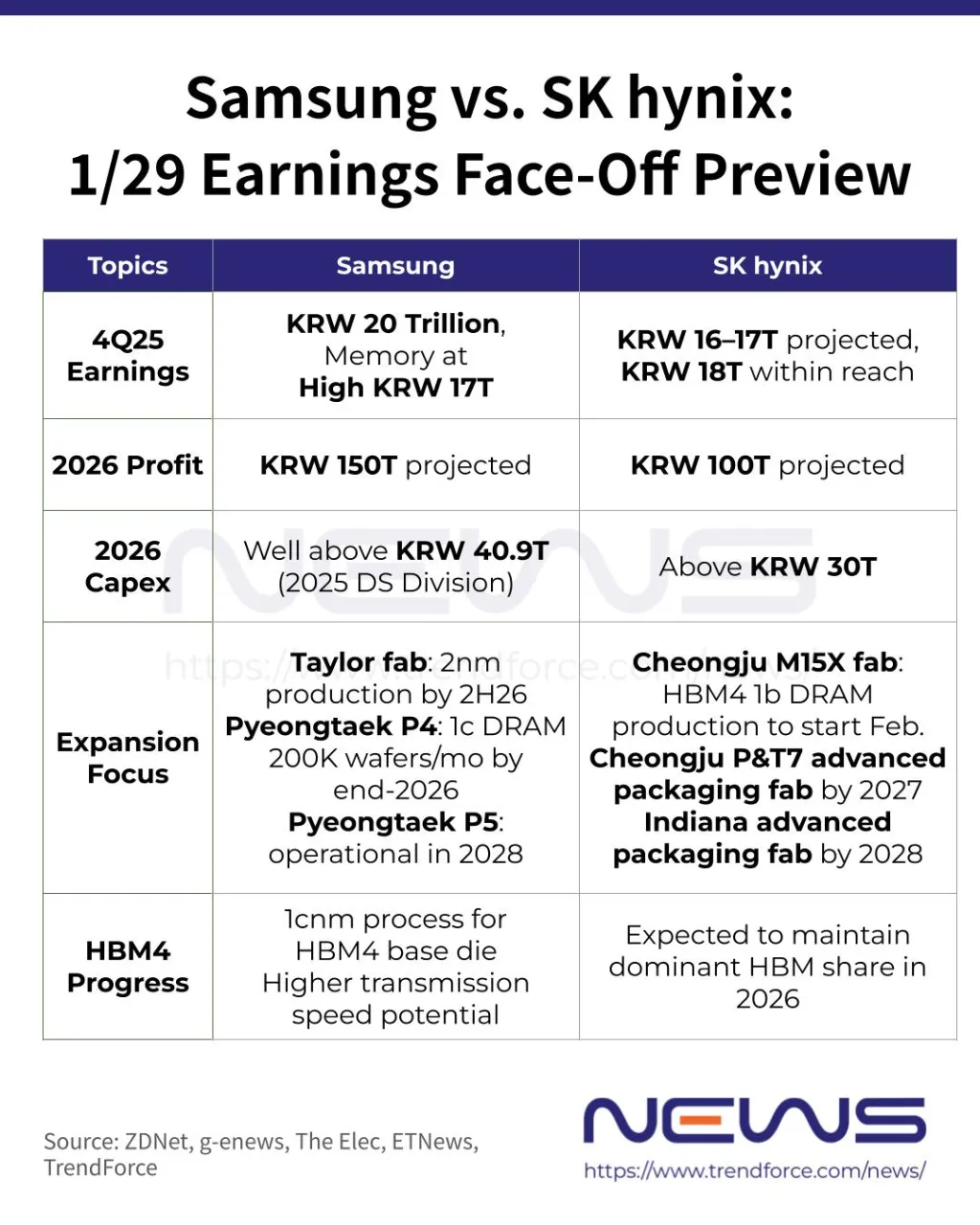

Several storage giants released their earnings on the same day: Samsung, SK Hynix, and Western Digital.

In addition to SanDisk, other storage giants such as Samsung, SK Hynix, and Western Digital will also release their earnings reports on the same day.

Samsung Electronics$CSOP Samsung Electronics Daily (2x) Leveraged Product (07747.HK)$With SK Hynix$CSOP SK Hynix Daily (2x) Leveraged Product (07709.HK)$released their results on the same day for the first time.Although neither company is listed on the US stock market, their analysis of the future storage market and capital expenditure plans will still have a profound impact on the US-listed storage sector.According to the latest earnings preview, Samsung Electronics' Q4 revenue is expected to exceed 90 trillion Korean won, with operating profit surging 208% year-over-year, potentially making it the first South Korean company to achieve a quarterly operating profit surpassing 20 trillion Korean won. While SK Hynix has a high exposure to HBM business, limiting its benefit from traditional DRAM price increases, its quarterly operating profit is still projected to reach at least 18 trillion Korean won.

Another highlight of this earnings release is the two companies’ outlook on peak performance in 2026 and their capital expenditure plans. The market generally expects Samsung to significantly increase its investment in the storage sector to boost HBM production and advance capacity construction in the United States, while SK Hynix’s capital expenditure is projected to exceed 30 trillion Korean won by 2026.

Options Strategy: With IV reaching elevated levels, what options strategies can be considered?

$SanDisk (SNDK.US)$The technical outlook shows short-term consolidation needs, with significant resistance above. The short-term overbought condition has eased, causing the rally to pause temporarily. However, the medium-term uptrend line remains intact, indicating that the overall trend has not fully reversed.

The current options pricing already reflects substantial risk premium. Options market data shows:The implied volatility (IV) is as high as 107%, at a historically elevated level (with an IV percentile of 80%);The put-call ratio (PCR) for the latest trading day (January 26) was 0.9, recently hovering around 1.0, indicating that the forces of buyers and sellers are relatively balanced, with no extreme bullish or bearish sentiment appearing.The implied volatility in the options market suggests an earnings day fluctuation range of ±16%.

In a high IV environment, this implies a lower success rate for simple 'buyer strategies' (Buy Call/Put) - even if the direction is correctly predicted, if the stock price does not rise significantly enough, a rapid collapse in volatility (IV Crush) could still lead to option losses. A strategy focused on 'selling volatility' is more suitable, using the high premiums to build a safety cushion. Below are operational suggestions for investors with different risk preferences:

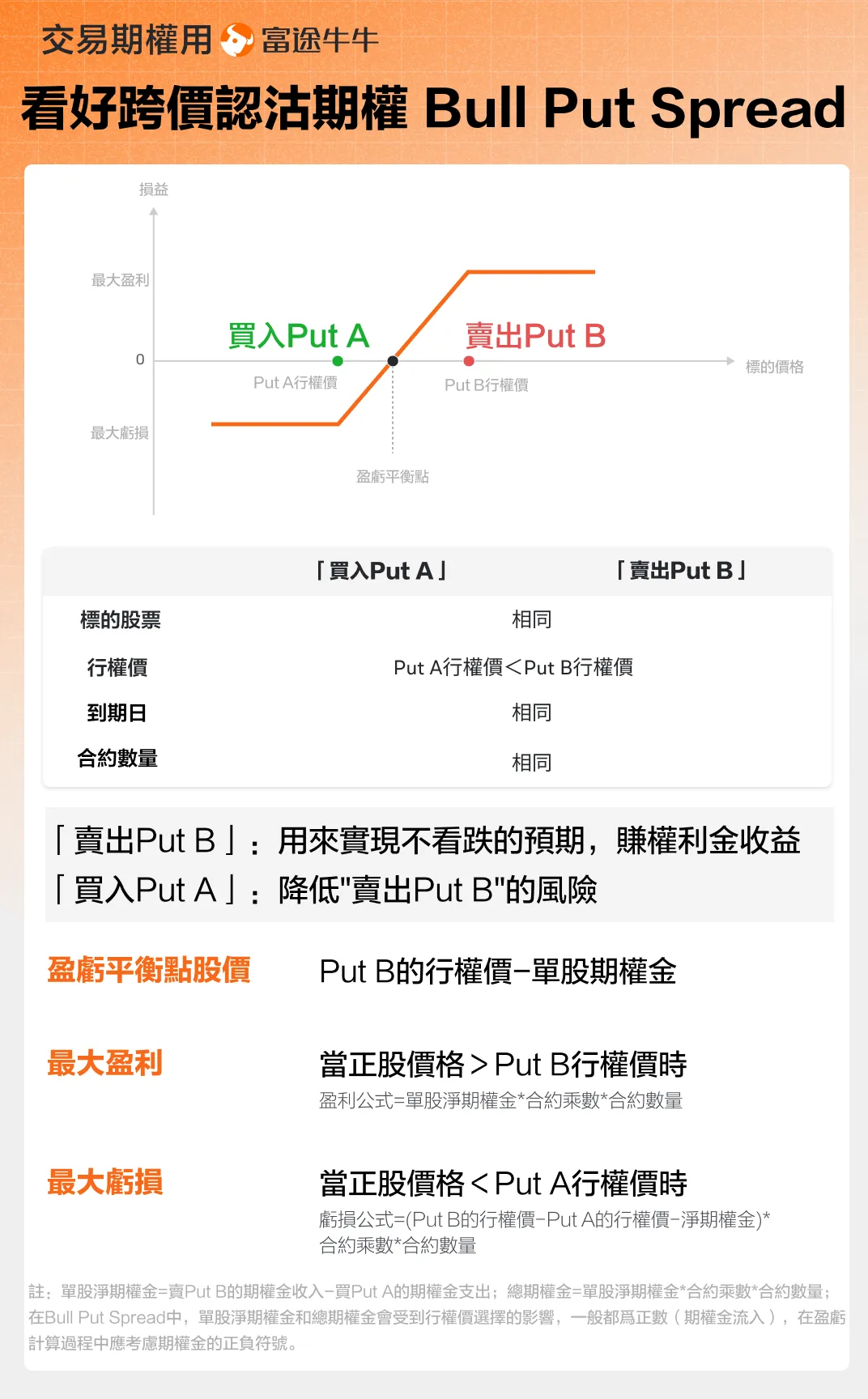

1. Aggressively bullish: Bull Put Spread

This strategy is suitable for investors who believe the stock price will break through previous highs but are reluctant to directly buy calls due to excessively high IV. Given the current high IV, directly buying call options may result in volatility decay; thus, a Bull Put Spread can be chosen instead. Essentially, this is a 'low-risk short put strategy,' carrying the characteristics of being an option seller, applicable when expecting the market won't decline.

This strategy generates income from option premiums while reducing the seller's risk. Therefore,it is suitable for implementation when implied volatility is high, as profits can be made even if the stock price remains stable, moves sideways, or fluctuates.When the stock price rises above the higher strike price, both options are out-of-the-money, resulting in maximum profit, equal to the total premium received at the time of opening the position.

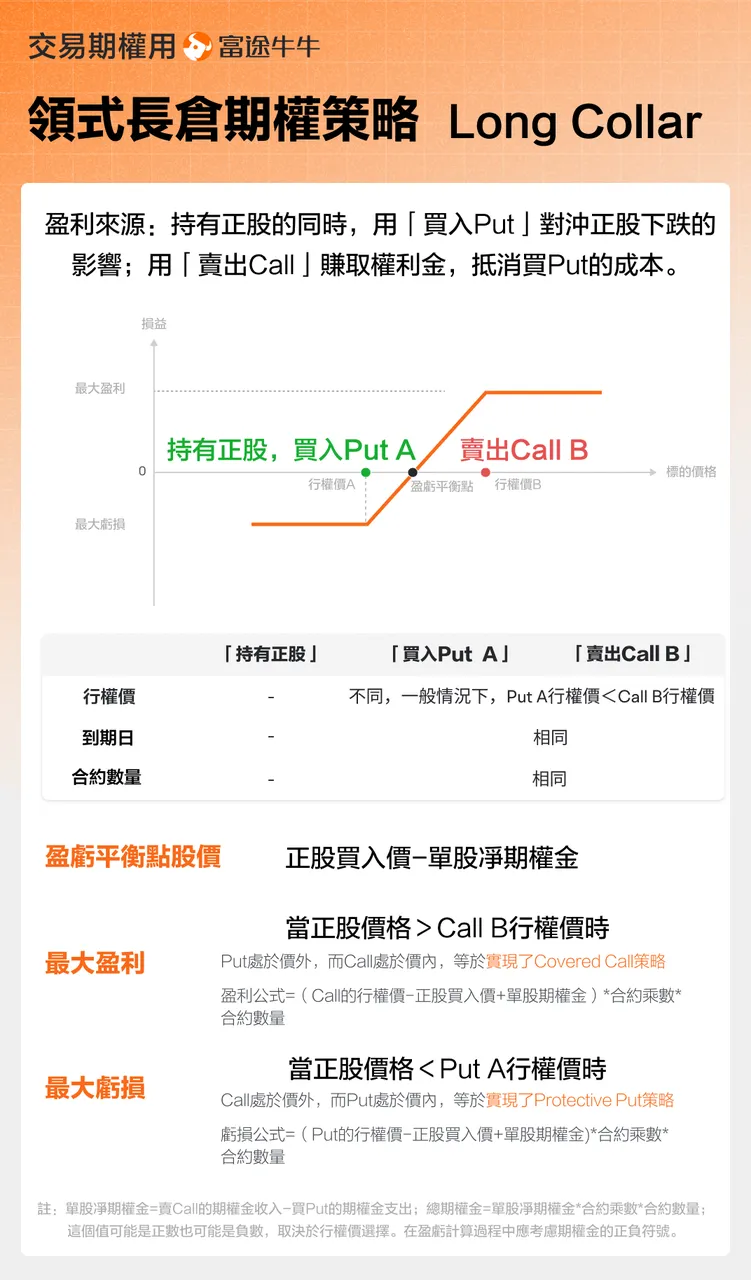

2. Stockholders / medium-to-long-term bulls (protection and enhancement strategies): Covered Call or Collar

Suitable for investors who already hold SNDK shares at lower levels, are concerned about a potential 'sell-the-news' pullback after the earnings release, or wish to use high implied volatility (IV) to reduce their holding costs.Covered CallWhile holding the position, sell calls with strike prices at resistance levels; if earnings results drive a sharp upward move, you'll exit with profits at higher levels; if the market moves sideways or declines, the substantial premium collected will significantly lower your holding cost, providing a buffer against downside risk.

Long Collar Option StrategyWhile holding the underlying stock, use 'buying Put options' to hedge against potential declines in the stock. Use the income from 'selling Call options' to offset part of the cost of buying Puts, thereby achieving the goal of hedging risk at a lower cost. This is akin to purchasing a 'free insurance policy' for your holdings, locking in the maximum drawdown risk during the earnings period. It can also provideProtective Put, while also generating additional income like aadditional income just like a Covered Call strategy.

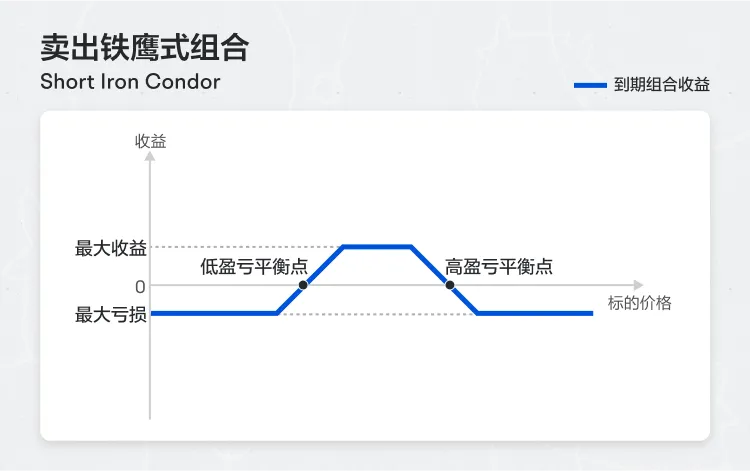

3. Range trading (volatility arbitrage): Short Iron Condor - selling an iron condor combination.

Suitable for professional traders who believe that the ±16% volatility pricing is overly exaggerated and that the stock price will fluctuate but won't experience sharp single-day spikes or crashes. This is a strategy for shorting volatility.When constructing this strategy,on the same expiration date of the underlying asset, simultaneously sell slightly out-of-the-money put and call options and buy even more out-of-the-money put and call options to form a combination.

As long as the stock price remains within a wide range of fluctuations after the earnings announcement and the price of the underlying asset stays between the upper and lower breakeven points, this strategy generates positive returns by collecting premiums on both the Call and Put sides. When the stock price exceeds the upper breakeven point or falls below the lower breakeven point, the strategy incurs losses, but these losses are limited. The strike prices can be determined based on the investor's risk appetite; considering SNDK’s history of occasional one-sided extreme movements, wider settings would present relatively lower risks and require strict position control.

Finally, here's a small perk for fellow investors—welcome to claim it!Beginner's Options Package

This event is exclusively for invited HK users, click to learn moreDetailed event rules >>

Major upgrade to the US options mechanism! New Monday and Wednesday options added for nine major symbols including Tesla and NVIDIA. A step-by-step guide to profiting from end-of-term options using the NiuNiu tool >>

Disclaimer

This content does not constitute any offer, solicitation, recommendation, opinion, or guarantee of any securities, financial products, or tools. The risk of loss in buying and selling options can be substantial. In some cases, your losses may exceed the initial margin amount deposited. Even if you set contingent orders, such as 'stop-loss' or 'limit' orders, these may not necessarily prevent losses. Market conditions may make these orders unexecutable. You might be required to deposit additional margin within a short period. If you fail to provide the required amount within the specified time, your open positions may be liquidated. However, you will still be responsible for any account deficit arising from this. Therefore, before trading, you should study and understand options and carefully consider whether such trading suits you based on your financial situation and investment objectives. If you trade options, you should be familiar with the procedures upon exercising options and at expiration, as well as your rights and obligations when exercising options and at expiration.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

48

185