Hotcoin Research | When Macro Factors Become the Pricing Logic: Forward-Looking Analysis of Macro Variables in the Cryptocurrency Market for 2026

Author: Hotcoin Research

The current fluctuations in the cryptocurrency market can no longer be explained solely by 'narrative hype' or 'on-chain innovation.' Cryptographic assets are increasingly behaving like 'macro-sensitive risk assets,' being pulled back and forth by interest rates, inflation, dollar liquidity, regulatory frameworks, geopolitical factors, and institutional fund flows. You may see the same on-chain data interpreted as 'capital inflow' when expectations of rate cuts rise, but as 'risk contraction' when tariff threats and geopolitical tensions escalate. Similarly, ETF inflows represent long-term growth when regulatory channels are clear, but they can also become an outlet for short-term panic during periods of heightened policy uncertainty. Macro variables are no longer background noise; they have become the core engine driving market trends, retracement depth, and structural shifts.

This article will analyze the mechanisms and impact pathways through which macro factors influence the cryptocurrency market, outline the key macro variables that could affect the market in 2026, and project their potential evolution and implications for cryptocurrency market movements. It aims to provide ordinary investors with a clearer framework: in 2026, amidst growing macro noise, how to identify where trends originate, why volatility occurs, why capital favors certainty, and which variables require immediate portfolio and risk exposure adjustments once they shift.

In the early days of the cryptocurrency market, the impact of macro factors was not yet evident, with crypto assets being more driven by their own supply and demand dynamics and technological advancements. However, as market capitalization expanded and institutional participation increased, crypto assets gradually came to be regarded as high-risk investments, and their price volatility became increasingly linked to the macro environment. Below are the typical pathways through which major macro variables influence the cryptocurrency market:

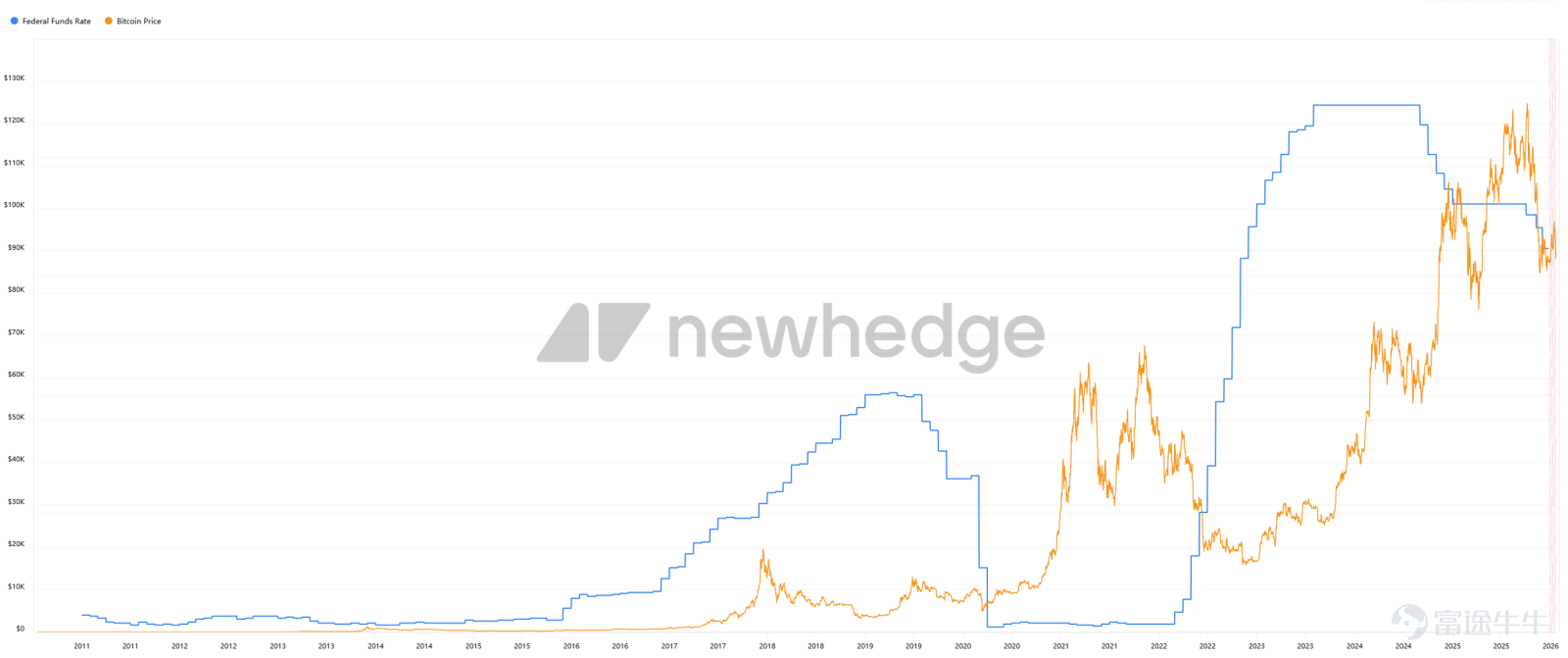

Interest Rates and Liquidity: Interest rates determine the tightness or looseness of the monetary environment, thereby influencing global liquidity and risk appetite. When interest rates decline or liquidity expands, investors are more inclined to allocate funds to high-risk assets, potentially shifting capital from low-yield bonds to stocks, cryptocurrencies, and other areas. Conversely, in a high-interest-rate environment, rising risk-free rates diminish investors' motivation to invest in crypto assets. The ultra-low interest rate, loose environment between 2020-2021 fueled a risk asset boom; whereas starting in 2022, rapid interest rate hikes above 5% caused liquidity to tighten sharply, pressuring the crypto market. In the second half of 2024, the Federal Reserve began a rate-cutting cycle, with rates expected to fall to the 3.5-3.75% range by the end of 2025, and further ease to around 3.25% in 2026. Interest rates and liquidity are arguably one of the most significant macro factors affecting the cryptocurrency market in recent years.

Inflation and Economic Growth: Inflation levels influence monetary policy direction and directly affect fiat currency purchasing power and investor sentiment. In a high-inflation environment, central banks typically adopt tightening policies, a process that weighed on the cryptocurrency market in 2022. However, inflation also prompted some investors to view Bitcoin as 'digital gold' to hedge against inflation risks. This safe-haven attribute did not immediately manifest during the high-inflation period of 2021-2022, instead being overshadowed by the negative effects of tightening policies. On the other hand, economic growth or recession indirectly impacts cryptocurrency investment by influencing corporate and household wealth and market risk appetite. The downturn in the cryptocurrency market between 2022-2023 stemmed partly from policy tightening amid high inflation, while slowing global economic growth and rising recession expectations also dampened speculative enthusiasm. Overall, inflation and business cycles shape the policy environment and risk sentiment, exerting medium-term influences on crypto trends, often intertwined with interest rate policies.

Regulatory Policies and Legal Environment: Regulatory variables significantly impact the cryptocurrency market by altering the behavioral norms of market participants, channels for capital inflow and outflow, and expectations of legality. Positive regulation, such as clarifying legal status or approving new investment channels, often boosts investor confidence and attracts additional capital. Conversely, stringent regulatory actions like banning trading or prosecuting industry leaders can trigger market sell-offs and risk aversion. From 2021-2023, U.S. regulators’ enforcement actions against certain cryptocurrency projects and delays in ETF approvals temporarily weighed on market sentiment. However, regulatory frameworks gradually advanced across countries from 2024-2025 brought some positive developments: for instance, Europe’s MiCA regulations introduced unified oversight standards starting in 2025, while the U.S. passed the stablecoin bill (GENIUS Act) in 2025 and provided standardized approval pathways for exchange-traded products (ETPs), enhancing compliance and transparency, viewed by markets as long-term positives. The short-term impact of regulatory factors is reflected in policy news shocks, while over the long term they profoundly reshape industry structure and capital distribution, making them another decisive variable alongside monetary policy.

Institutional Capital Flows and Market Structure: As compliant investment channels like ETFs open up, and listed companies and institutional investors participate, the capital structure and pricing mechanisms of the cryptocurrency market are evolving. Institutional capital, typically large in scale and favoring mainstream assets, amplifies market trends when entering or exiting. For example, after the debut of the first U.S. spot Bitcoin ETFs in 2024-2025, massive capital inflows followed. Statistics indicate that in 2025 alone, Bitcoin ETFs and listed companies’ Bitcoin holding plans, such as MicroStrategy, contributed nearly $44 billion in net buying demand. Institutional participation also brings structural changes, with Bitcoin’s dominance in the overall cryptocurrency market cap rising above 60% in 2025, significantly higher than previous cycle peaks, indicating a concentration of funds in leading assets like Bitcoin.

Stablecoins and Capital Flows: Stablecoins, as a key infrastructure of the cryptocurrency market, directly reflect the 'reservoir' status of on-exchange funds through their issuance and circulation scale, which is also influenced by the macro environment. During bull markets, capital inflows drive rapid growth in stablecoin market caps, while bear markets see declining stablecoin demand and contraction in scale. Changes in stablecoin supply often lead or simultaneously reflect the dynamics of capital entering or leaving the market. For instance, during the 2020-2021 bull market, supplies of stablecoins like USDT and USDC surged from under $30 billion to over $150 billion by the end of 2021; during the 2022 bear market, total market caps slightly declined, stabilizing at around $1.3 trillion in early 2023. Entering the new 2024-2025 market cycle, the stablecoin market expanded again, with the global stablecoin market cap now exceeding $3 trillion, marking a 75% increase from a year ago.

Monetary Policy Direction – Impact Strength: ★★★★★

Entering 2026, the global monetary policy environment is at a critical turning point. The Federal Reserve experienced a pivot from tightening to easing between 2024 and 2025: after consecutive rate hikes pushed the federal funds rate peak to 5.25%, it began to gradually cut rates at the end of 2024. In 2025, the Federal Reserve cut rates three times, lowering the rate to a range of 3.5%~3.75%, the lowest level in three years. In 2026, the Fed is expected to continue with mild easing but with restraint: the Fed's dot plot indicates that the federal funds rate will drop to about 3.25% by year-end. Notably, Chairman Powell’s term will expire in May 2026, which may lead to changes in the Fed's leadership and introduce some policy uncertainty. Overall, barring any significant inflation surprises, the U.S. monetary environment in 2026 will be much friendlier compared to the past two years. Although there are no signs of renewed quantitative easing (QE), at least liquidity will no longer be continuously tightened, benefiting risk asset prices.

Regarding other major central banks, both the European Central Bank and the Bank of England gradually ended their rate hikes in 2024-2025, and in 2026 they are likely to enter a wait-and-see or rate-cutting cycle, albeit with a lag behind the Federal Reserve. The Bank of Japan is an exception; its interest rates were previously long at zero or even negative, and although they were raised somewhat in 2025, they remain low. In 2026, the Bank of Japan may maintain a relatively independent pace. Overall, global interest rates are entering a downward channel in 2026, especially in leading markets like the U.S., where declining interest rates will release more liquidity and reduce the opportunity cost for risk assets. However, persistently high inflation remains a potential threat: if inflation proves stickier than expected, central banks will be constrained by price pressures and unable to ease significantly.

Inflation and Economic Outlook – Impact Level: ★★★★☆

The mainstream expectation for 2026 is that inflation rates in major economies will further converge toward target levels or even slightly undershoot them. For example, the Federal Reserve’s latest forecast shows that U.S. PCE inflation will drop to around 2.4% in 2026, close to the long-term target of 2%. Cooling inflation allows central banks to stop raising rates, which is a significant positive for risk assets, including the crypto market. If inflation remains moderate or even slightly below expectations in 2026, it could provide room for central banks to implement unexpected rate cuts or liquidity support, further boosting market valuations. For instance, when inflation data at the end of 2025 was slightly better than expected, Bitcoin and U.S. stocks rose in tandem.

In terms of economic growth, global economic growth in 2026 is expected to be moderate. The IMF forecasts that growth in major advanced economies will be around 2% during 2025-2026, with the U.S. potentially outpacing Europe slightly. A low-growth but non-recessionary environment typically supports moderate policies and stable market confidence. JP Morgan’s 2026 outlook also assumes that growth in major economies will stabilize or slightly exceed potential levels. However, if a significant financial risk event unexpectedly occurs in 2026, it could initially impact risk assets, including crypto assets. Historically, however, central banks tend to loosen policies more aggressively in recessionary environments, which could subsequently sow the seeds for a new bull market.

Risks that need continuous monitoring include: energy prices or geopolitical conflicts causing inflation to re-emerge; or leadership changes at major central banks or poor policy communication triggering market volatility. If these risks can be avoided, the easing monetary environment will become an important supporting factor for the crypto market in 2026.

Regulatory and Legal Environment – Impact Level: ★★★★☆

2025 was called the 'Year One of Crypto Regulation,' as key regulations were introduced or implemented in major jurisdictions, accelerating the crypto industry's shift from a gray area to a path of compliance. Progress on regulatory policies in 2026 will remain one of the key variables in the crypto market. Overall, global regulation is moving towards clarity and standardization, which will improve long-term market expectations. However, differences in pace across regions during the short-term transition period may also trigger capital flows and fluctuations in market sentiment.

United States: In July 2025, the first federal stablecoin law, GENIUS Act, was passed. According to the requirements of the act, regulatory agencies must issue specific implementation rules by July 2026. If the rules are properly formulated, it will greatly enhance the transparency of stablecoins and bank participation, further expanding the supply of stablecoins and the capacity of the crypto market, potentially leading to a more decentralized market structure. Currently, USDT's market share has dropped from 86% in 2020 to about 58% in 2025, while USDC has risen to 25%. Newcomers like USD1 and PYUSD have also rapidly gained prominence. Besides stablecoin legislation, the U.S. Congress pushed for discussions on the Digital Asset Market Structure Clarity Act (CLARITY Act) in 2025, attempting to delineate the boundaries between security tokens and commodity tokens. The focus in 2026 will be whether such legislation can be enacted. Although there is still political uncertainty regarding the passage of the CLARITY Act, the market is highly attentive. If the CLARITY Act passes, it could trigger another round of price increases.

At the regulatory agency level, the U.S. Securities and Exchange Commission (SEC) completed a significant shift in 2025. The newly appointed chairman launched 'Project Crypto,' reforming the rules for crypto securities comprehensively. In September 2025, the SEC approved a universal listing standard for spot commodity ETFs, significantly reducing legal barriers to issuing crypto ETFs. In 2026, more types of crypto ETF/ETP products are expected to emerge (such as multi-crypto asset basket ETFs, ETH spot ETFs, etc.), enriching investor tools and marking the inclusion of crypto assets into mainstream investment portfolios. It should be noted that the SEC and CFTC's stance on areas like DeFi and altcoins remains unclear. If regulatory constraints on certain tokens or decentralized protocols appear in 2026, it may impact the prices of related assets. However, before the CLARITY Act resolves these issues, such enforcement measures are expected to remain cautious.

Other regions: The European Union fully implemented the Markets in Crypto-Assets Regulation (MiCA) in 2025, and the EU regulatory environment is expected to remain stable and continue promoting compliance in 2026. In addition to MiCA, the EU revised its anti-money laundering regulations in 2025, requiring crypto transactions to comply with the 'Travel Rule,' which helps increase transparency in crypto transactions, aids in combating illegal fund flows, but also pressures non-compliant platforms. Major Asian economies also strengthened their crypto regulatory frameworks in 2025. Japan improved exchange and custody regulations; South Korea advanced the legislation of the Digital Assets Basic Act to comprehensively regulate crypto; Hong Kong issued more exchange licenses and introduced stablecoin regulatory rules in 2025; Singapore enacted a crypto licensing system under the Financial Services and Markets Act in 2025, entering the regularized regulatory phase in 2026. Moreover, emerging markets like some countries in the Middle East and Latin America also formulated crypto-friendly policies or attracted crypto businesses to settle in 2025 (such as the UAE, El Salvador, etc.). These regions may continue to benefit from crypto capital overflow in 2026.

In summary, regulatory variables are expected to have a more positive impact on the crypto market in 2026: clear rules remove obstacles for industry development, while policy trends still need close attention, as any regulatory movement in any region could quickly reflect in prices through the globalized market.

Institutional Funds and Investment Tools – Impact Level: ★★★★☆

2026 may witness a significant increase in the 'institutionalization' of crypto assets. First, with the successive launches of U.S. spot Bitcoin ETFs and Ethereum futures/spot ETFs, traditional financial institutions are incorporating crypto assets into their asset allocations at unprecedented levels. Products like ETFs lower the barrier to investing in crypto, prompting conservative institutions such as insurance companies, pension funds, and university endowments to venture into Bitcoin through ETFs and small-scale exploratory allocations. Statistics show that Bitcoin ETFs listed in the U.S. in 2025 brought approximately $30 billion in additional inflows to Bitcoin. This figure is expected to continue rising in 2026, with asset categories expanding from BTC and ETH to include crypto portfolio ETFs, DeFi ETFs, etc. A continuous inflow of funds from the securities market via ETFs will provide lasting buying support for Bitcoin and major coins. Fundamentally, ETFs change the capital structure, dispersing market positions across numerous institutional portfolios, thus reducing systemic risk.

Second, holding crypto assets and including them in corporate financial statements is becoming a trend. As of January 21, 2026, MicroStrategy has cumulatively held 709,715 Bitcoins, accounting for 3.38% of the total Bitcoin supply. An increasing number of companies are including crypto assets on their balance sheets, enhancing market recognition. Additionally, emerging 'Digital Asset Treasury' (DAT) companies have gone public, injecting substantial buying pressure into the market in 2024-2025, with expectations to expand further in 2026. However, attention should be paid to the fact that when coin prices are high, these holding companies might consider profit-taking or reducing their positions, thereby bringing marginal selling pressure. Overall, increased institutional holdings reinforce Bitcoin's store-of-value attribute and market stability, but also introduce some degree of cyclicality—where institutions may buy low and sell high, thus moderating extreme volatility.

Market Structure Changes: Another impact of institutional participation is the alteration of market structure and volatility patterns. In 2025, Bitcoin dominance rose above 60%, with relatively low volatility. This can partly be attributed to institutional preference for blue-chip assets, causing funds to concentrate more on leading market cap coins like BTC and ETH rather than speculative altcoins. Simultaneously, the development of derivatives markets and the use of options hedging strategies suppressed some short-term volatility. In 2026, Bitcoin's institutional holding ratio is expected to rise further, with Ethereum continuing steady growth. For mid-to-small cap tokens, 2026 may present a mixed picture. On one hand, macroeconomic recovery could benefit overall market cap expansion, with Bitcoin leading a potential 'altcoin season.' On the other hand, clearer regulation is a double-edged sword for altcoins. In 2026, the altcoin sector may not experience the widespread euphoria seen in 2017 or 2021 but instead see a split scenario: top-tier quality projects benefiting from industry growth, while bottom-tier and high-risk tokens remain sluggish.

In summary, driven by institutionalization, the 2026 crypto market may be dominated by institutions and compliant funds, with blue-chip coins and quality projects at the core, and speculative bubbles relatively contained.

Geopolitical Events and Macro Risks – Impact Level: ★★★☆☆

In addition to economic and regulatory factors, geopolitical situations and major macro risk events can indirectly impact the crypto market by influencing investor risk appetite and capital flows. The following aspects should be closely monitored in 2026:

International Tensions and Conflicts: Geopolitical uncertainty (such as geopolitical conflicts and trade frictions) often triggers short-term risk aversion in global markets, with capital flowing into traditional safe-haven assets like the US dollar and gold, while high-risk assets such as stocks and cryptocurrencies face downward pressure. However, severe long-term geopolitical risks (such as economic sanctions or currency devaluation by certain countries) sometimes stimulate localized crypto demand, as people look for ways to transfer assets and hedge against inflation. For instance, following the Russia-Ukraine conflict, the Russian ruble plummeted, leading to a surge in local Bitcoin trading volumes. Potential risks in the international landscape in 2026 include rising tensions in Eastern Europe and the Middle East, renewed geopolitical conflicts involving the US in places like Venezuela and Greenland, great power competition resulting in sanctions and capital controls, and uncertainties surrounding the US midterm elections. These factors are likely to increase global risk aversion, negatively impacting the crypto market in the short term. However, over the long term, the 'neutral' and 'borderless' nature of crypto assets may position them as a liquidity outlet amid global financial fragmentation, which could be where their value in hedging traditional systemic risks lies.

Exchange Rates and US Dollar Trends: The strength or weakness of the US Dollar Index (DXY) often shows an inverse relationship with the crypto market. When the US dollar appreciates significantly, emerging markets experience capital outflows and global liquidity tightens, creating headwinds for non-dollar assets like crypto. Conversely, when the dollar weakens, crypto assets tend to gain favor. If the Federal Reserve cuts interest rates in 2026 while Europe lags behind, the dollar may weaken moderately, reducing exchange rate concerns for non-US investors and boosting the motivation to allocate to crypto. In the event of a currency crisis in any country in 2026, there may be structural changes in regional capital inflows and outflows in the crypto market: individuals or businesses in high-inflation countries might increase their crypto holdings to preserve wealth, while the crypto market could attract new incremental users and funds from these regions.

Global Capital Controls and Tax Policies: India previously imposed high taxes and strict regulations on crypto trading, causing trading volumes to shrink. If India relaxes its policies in 2026, it could unleash significant latent demand. On the other hand, if some crypto-friendly regions tighten regulations due to policy changes, corresponding markets may contract. Another dimension is that countries are increasingly tightening regulations on cross-border capital flows (e.g., anti-money laundering and anti-tax evasion measures). Crypto can be used for legitimate cross-border transfers, such as international remittances using stablecoins, but it may also be exploited by criminals. Many countries strengthened crypto anti-money laundering enforcement in 2025, and this will become more routine in 2026. This could affect demand for certain anonymous coins or privacy-related tokens in the short term.

Overall, the impacts of geopolitical and macro risk events are sudden and short-lived, making precise predictions difficult. However, investors should have risk management plans in place, such as moderately allocating to relatively mature assets like gold and Bitcoin for hedging purposes.

Based on the above analysis of macro variables, we can make an outlook on the potential market trends for crypto in 2026. Of course, the future is full of uncertainties, and the scenarios below are intended to provide a framework for thinking; investors should adjust expectations based on real-time data.

Base Case Scenario (Moderate and Accommodative Macro Environment): The global economy grows moderately, with major central banks like the US making small interest rate cuts and maintaining rates around 3%, while inflation stays close to target levels. There are no significant negative shocks on the regulatory front, and existing regulations are gradually implemented with good market adaptation. In this scenario, the crypto market is expected to continue the upward trend from 2025 and enter a mature growth phase. Bitcoin may set new highs above the 2025 peak, driven by sustained ETF inflows and the gradual impact of reduced supply. Annual cumulative gains may narrow compared to 2025 but remain substantial. Ethereum is expected to benefit from technological upgrades and increased institutional allocations, potentially outperforming Bitcoin in certain months but generally maintaining a degree of correlation. Among mainstream altcoins, projects with clear application value and good compliance prospects are likely to be favored, while purely speculative altcoins may see relatively brief and limited rallies even in a bullish market environment. Stablecoin market size is projected to further grow, surpassing the $400 billion mark. Investor sentiment is optimistic but more rational overall, with market volatility at moderate levels and fewer instances of extreme euphoria or panic.

Optimistic scenario (macro surprises and technological breakthroughs): Several positive factors stacked on top of the baseline: rapid decline in inflation, even showing signs of mild deflation, prompting major central banks to restart quantitative easing (QE) in the second half of 2026; the US Congress smoothly passes the CLARITY Act and other crypto-related legislation, with SEC and CFTC coordinating regulation to eliminate regulatory gray areas; tech giants release major applications that bring blockchain technology to hundreds of millions of new users, or European and American pension funds begin allocating investments in Bitcoin. These additional positives will trigger 'FOMO' sentiment, pushing the market into an accelerated upward phase. In the optimistic scenario, Bitcoin prices may experience parabolic growth similar to 2017 or 2021. Top cryptocurrencies like Ethereum will also soar in tandem, potentially leading to another short-term surge in altcoins, with total market capitalization possibly breaking through multiples of the previous cycle, truly entering the ranks of global financial asset classes. However, it is important to be cautious, as this overheated state is often unsustainable, and once macro or policy environments shift, it could lead to a sharp correction.

Pessimistic scenario (macro shocks and risk events): Consider the following combination: rising US inflation hindering the rate-cutting process, systemic crises in international financial markets, stagnation or reversals in US crypto-related legislation, escalation of the Venezuela incident and sanction chain disruptions affecting energy and inflation expectations, the US forcibly acquiring Greenland and threatening tariffs on Europe, and the 2026 US midterm elections causing policy uncertainty. In this pessimistic macro scenario, the crypto market will inevitably suffer significant damage. Liquidity tightening and risk aversion could lead to a sharp pullback in Bitcoin prices, with institutional funds potentially withdrawing from crypto ETF positions due to losses in other assets or a sudden drop in risk appetite, resulting in net outflows. Additionally, if some large industry players face risks, it will exacerbate panic. In the pessimistic scenario, altcoins will suffer the deepest declines, and Ethereum will also fall with the market. For long-term investors, the pessimistic scenario offers opportunities to accumulate quality assets at lower levels; for short-term traders, they must prepare for stop-loss exits.

The most likely trajectory might lean towards positivity between the baseline and the optimistic scenario. Current signs indicate that the macro environment is gradually improving, the regulatory framework is taking shape, and internal innovation within the industry is building momentum. After Bitcoin hit new highs in 2025, it did not experience extreme speculative bubbles seen in past cycles, leaving room for further upside in 2026. Market sentiment has become more mature and rational after the洗礼 of 2022-2023. As long as there are no major negative 'black swan' events, the overall trend for the crypto market in 2026 remains bullish, albeit with milder volatility compared to before. The year's movement might be 'volatile upward': the first quarter could consolidate due to macro uncertainties or profit-taking, while the second and third quarters rise as interest rates decline and regulatory benefits materialize. If new technological catalysts emerge in the fourth quarter, there could be another push higher. Looking further ahead, 2026 may lay the foundation for the next crypto cycle. Regardless of price fluctuations, the industry’s underlying foundations are stronger than ever: growing global user numbers, increasing mainstream institutional acceptance, clear legal status, and continuous technological evolution. These fundamental factors will support crypto assets in reaching broader stages.

The crypto market in 2026 stands at a new starting point. The shifting macroeconomic landscape and policy trends will continue to largely shape the fate of this emerging market. From interest rate movements to regulatory frameworks, from institutional flows to geopolitical dynamics, various macro variables interact, making the crypto market no longer isolated from the global financial system but integrated and resonating with it. On one hand, this means that the investment logic of crypto assets is richer, requiring investors to have a macro perspective and cross-market thinking. On the other hand, this signifies that crypto is gradually maturing, with its rise and fall tied not only to speculators’ euphoria but also closely linked to global economic pulses and institutional changes.

For ordinary investors, 2026 will be a year full of opportunities and challenges. We must recognize the historical opportunities that could arise from a warming monetary environment and clearer regulations, while also remembering that markets are unpredictable, and risk events can still occur unexpectedly. Being prudent yet forward-looking, rational yet passionate, will allow us to grasp the nuances of crypto investing amidst this complex and changing macro environment. Looking ahead, the crypto market will continue to evolve, whether in bull or bear markets, driven by its inherent innovative vitality and pursuit of open finance. Let us wait and see what exciting chapters the crypto world will write in 2026, propelled by macro trends.

Hotcoin Research, the core investment research arm of Hotcoin Exchange, is dedicated to transforming professional analysis into actionable tools for your investment strategy. Through our 'Weekly Insights' and 'In-Depth Reports,' we dissect market trends; via our exclusive 'Hot Picks' column (curated by AI and expert dual screening), we help you identify high-potential assets and reduce trial-and-error costs. Every week, our analysts also engage with you live to interpret market hotspots and forecast trends. We believe that thoughtful guidance and professional support can help more investors navigate cycles and seize value opportunities in Web3.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1