Netflix: Will the acquisition drag down the drama king? Time to test faith again

By Dolphin Research

Netflix (NFLX.O) released its Q4 2025 earnings report after market close on January 20 EST. Overall, the results were a mixed bag. Coupled with the impact of the WBD acquisition, this represents an upgraded collision between short-term pressure and long-term faith.

Specifically:

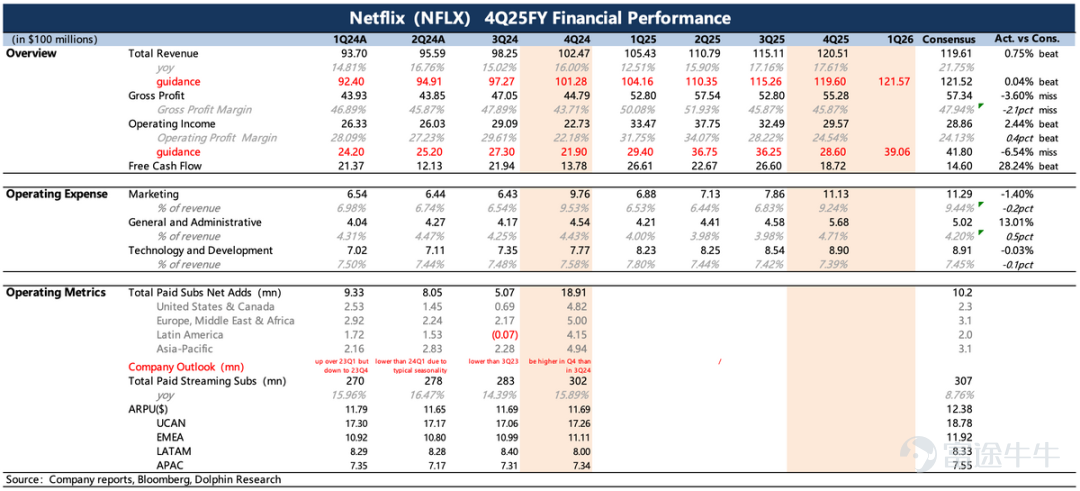

1. Q4 Exceeds Expectations:The positive aspect of the earnings report is that the fourth quarter performed well, with both revenue and profits exceeding expectations (impacted by deferred Brazilian tax payments to be settled in 2026), and a favorable trend of accelerating growth, primarily driven by the popularity of the final season of 'Stranger Things' during the fourth quarter.

However, compared to the first three quarters, the fourth-quarter revenue benefited more from price increases. The total number of subscribers at year-end exceeded 325 million, up about 8% year-over-year, a noticeable slowdown from last year's growth rate of around 15%. Subscriber growth issues are likely the core reason why Netflix went all out to acquire WBD, which has also raised market concerns about Netflix's long-term organic growth momentum.

2. Guidance Is Lackluster:Concerns over organic growth momentum have led the market to pay closer attention to management’s future growth guidance in this earnings report. In reality, the guidance for Q1 2026 and the full year 2026 was relatively lackluster, barely meeting consensus expectations, which were not particularly high: Q1 revenue growth forecast at 15.3%, with annual growth projected between 12% and 14%.

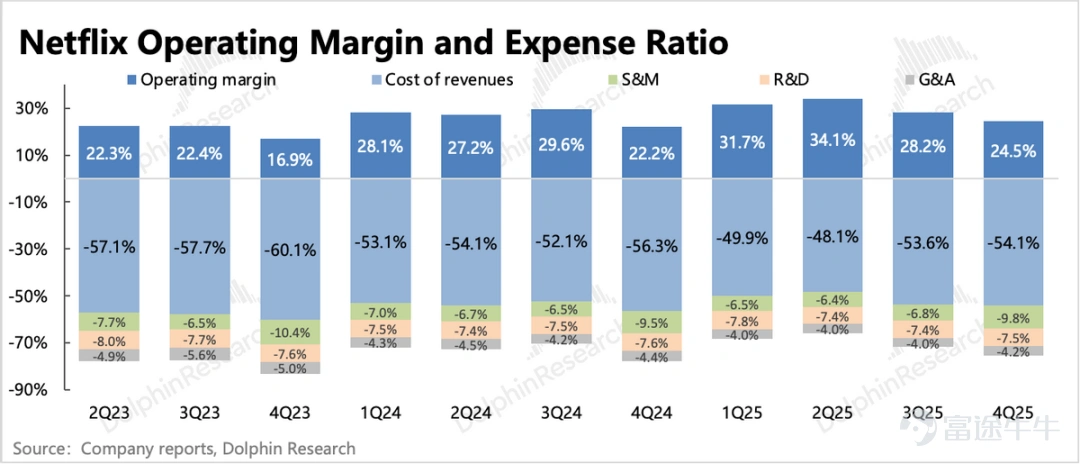

The margin guidance fell slightly below expectations due to acquisition-related expenses and the remaining Brazilian tax payments (forecast operating margin of 31.5% vs. market expectations of 32.5%).

3. Slow Progress in Advertising, Potential Turnaround This Year:Advertising revenue for the full year 2025 exceeded $1.5 billion, which aligns with Dolphin's prior expectations, but still shows a significant gap when compared to some institutions’ forecasts of $2 to $3 billion. The broader environment certainly had an impact, especially on brand advertising that relies on Netflix's traditional sales methods. Netflix is currently testing programmatic advertising in North America and plans to expand it globally in the second half of the year, which is expected to significantly boost ad revenue.

4. Cash Flow Pressure Triggered by Acquisition:In terms of cash flow usage, the focus remains on content investment and share buybacks. In the fourth quarter, Netflix spent $2.1 billion repurchasing 18.9 million shares, leaving a remaining balance of $8 billion. However, due to the pressure of the all-cash acquisition of WBD, further buyback activities will be suspended.

The company forecasts a 10% increase in content investment, but we expect it may also slightly control the actual spending like this year to further ease short-term cash flow pressure. In fact, last year’s investment scale of 17.7 billion did not reach the initial target of 18 billion.

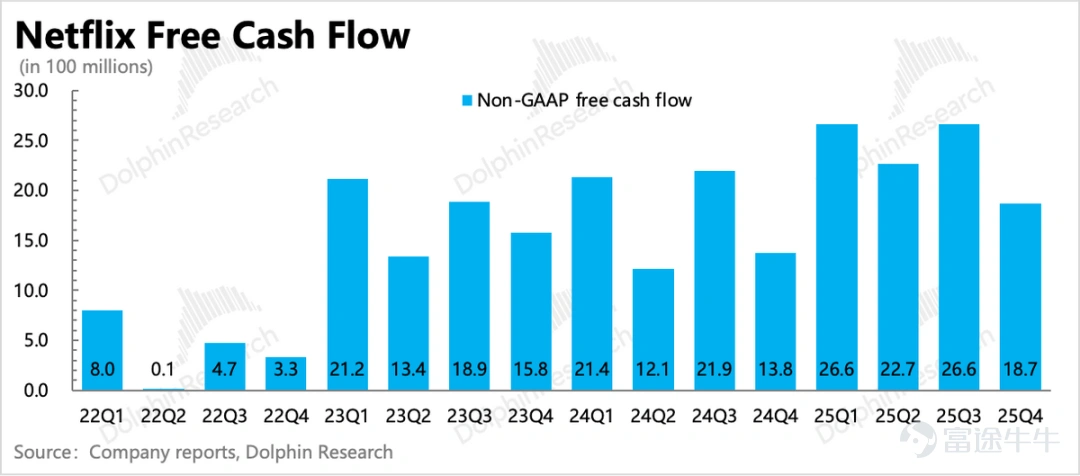

Netflix's free cash flow is expected to reach nearly 10 billion by 2025 and aims for 11 billion in 2026. However, as of the end of last year, the company only had 9 billion in net cash on its books and faces 1 billion in short-term debt repayments within the next year. After switching to an all-cash deal, Netflix needs to secure more external loans, adding 8.2 billion to the previous 59 billion bridge loan, while applying for a total revolving credit facility of 25 billion in senior unsecured credit to repay part of the bridge loan.

Thus, the remaining bridge loan stands at 42.2 billion, with estimated annual interest costs significantly higher than the potential savings from reduced content licensing expenditures post-WBD acquisition (2-3 billion). Therefore, if the acquisition process gets prolonged due to disruptions (such as being caught in regulatory reviews, dragging the process into a multi-year dilemma), the pressure on short-term cash flow will be significant.

5. Overview of Key Performance Indicators

Dolphin Research Perspective

Netflix’s stock price was weak in Q4, lagging behind other tech giants. The immediate trigger was the massive acquisition deal for WBD. During the Q3 earnings review, Dolphin Research expressed doubts about the acquisition rumors since Netflix has always adhered to the principle of 'Builders over Buyers.'

However, it is precisely the management's relentless attitude—insisting on breaking conventions—that has heightened market concerns about Netflix’s long-term organic growth. Compared to doubts about growth, the debt burden brought by the large acquisition is secondary. Thus, under the current environment that already suppresses sentiment, Netflix appears to be experiencing a collapse of faith.

It’s undeniable that the inherent uncertainty of the acquisition itself is enough to make funds cautious. The latest agreement revision further distances Paramount as a bidder, leaving only regulatory approval uncertainties.

If evaluated based on Netflix’s desired TAM (Total Addressable Market) including YouTube as part of the overall streaming market, then antitrust risks would be relatively smaller.

Based on management’s operating targets for 2026 (generally conservative), the after-hours market capitalization of 350 billion USD corresponds to a 26x P/E ratio (assuming a 15% tax rate). Though slightly above profit growth (YoY +20%), the last time valuation fell to this level was during the high-interest environment of 2022 when users experienced quarterly net declines. Therefore, Dolphin Research believes there is no need for further pessimism at this point unless long-term faith collapses. But so far, no signs indicate such a collapse.

From a long-term perspective, acquiring WBD would be highly beneficial. Although acquiring ready-made IPs might have been less appealing to Netflix in the past, it is now a viable option, especially for some irreplaceable, cross-generational top-tier IPs. Not only does it enrich the content library, but more importantly, it allows Netflix to develop entertainment content beyond film and TV to seek monetization.

The following is the detailed content

First, behind the acquisition of WBD lies the near saturation of mature markets

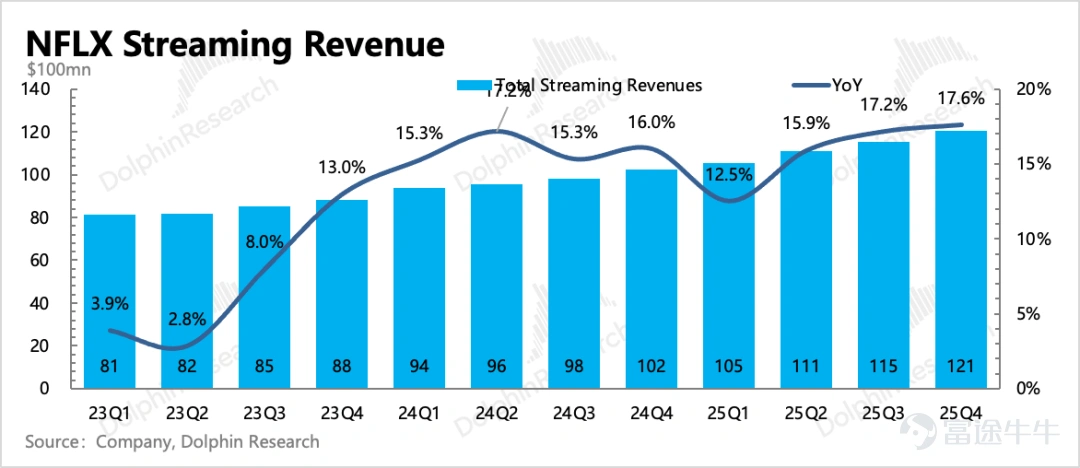

Total revenue in the fourth quarter reached 12.1 billion, up 18% year-over-year, with a neutral foreign exchange impact across different markets. Advertising revenue hit 1.5 billion, which, despite significant growth, still fell short of institutional expectations.

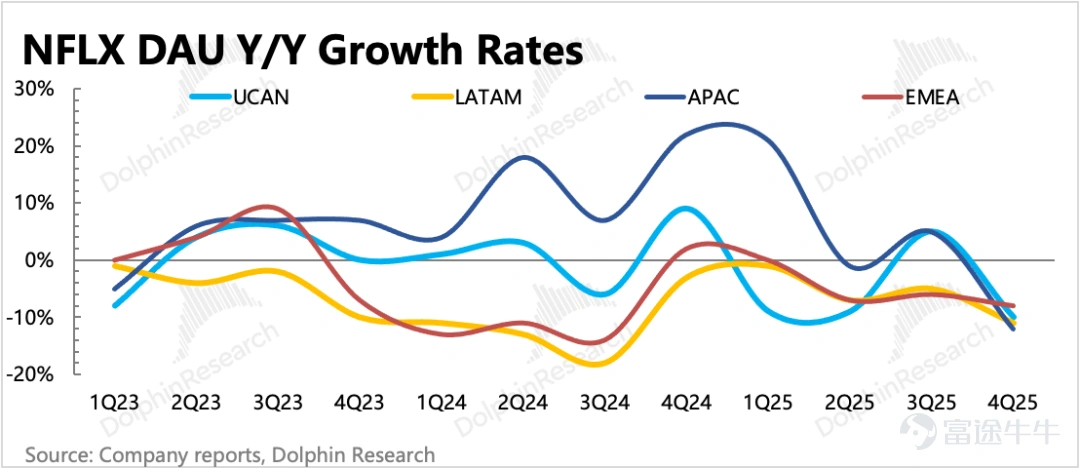

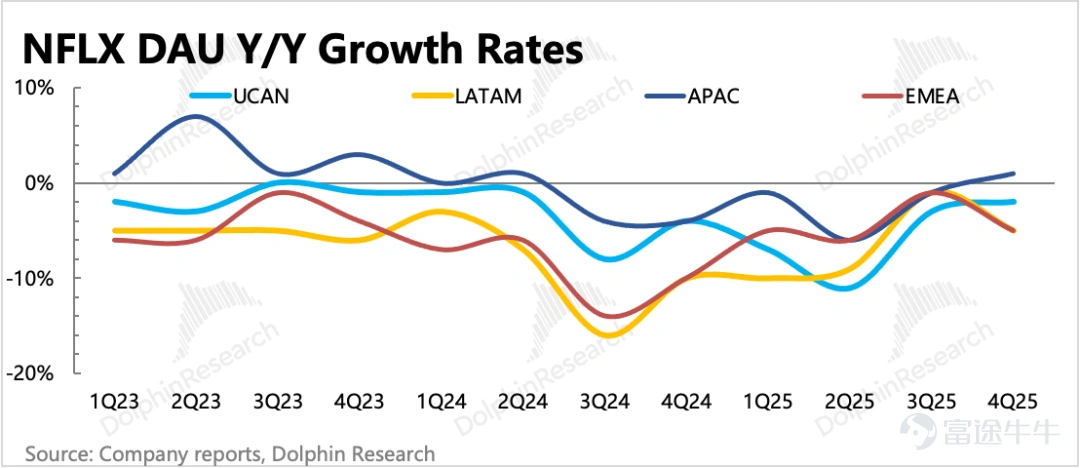

The company disclosed that its subscription user count exceeded 325 million in Q4, with a year-over-year growth rate of approximately 8%. The slowdown in user growth, especially in mature markets nearing saturation due to price increases, is why Netflix is anxious about long-term growth and willing to go to great lengths to acquire WBD.

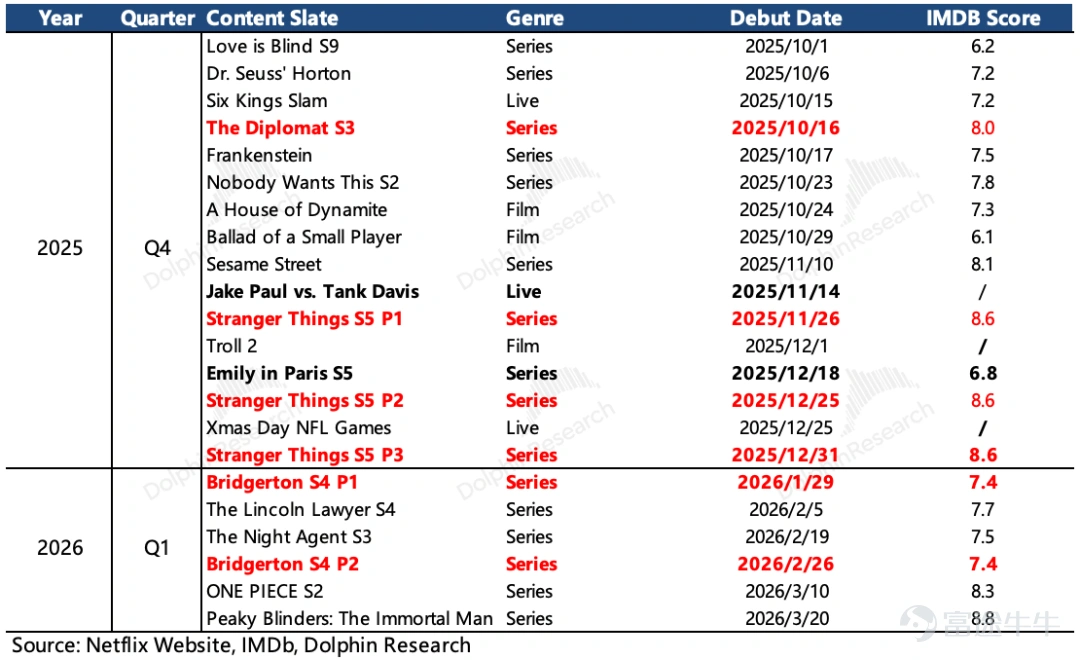

By the end of this year, Netflix will be at the tail end of this wave of content cycles. While there are certainly highlights in the content itself, from an innovation standpoint, only a few S-tier new IPs like 'Squid Games' and 'Wednesday' have emerged in the past three years. Other popular releases were mostly sequels to older IPs such as 'Stranger Things', 'You', 'Bridgerton', and 'Money Heist'.

With a user base surpassing 300 million but diminishing returns on engagement, it’s becoming increasingly difficult to maintain a revenue growth rate above 15% and profit growth over 20% to justify a PE ratio of 30-40x. Cracking down on account sharing offers only a one-time boost, while advertising support remains very limited.Fundamentally, growth still depends on producing more high-quality content, catering to users with diverse tastes, and exploring varied monetization methods, such as gaming, theme parks, and other IP derivatives.

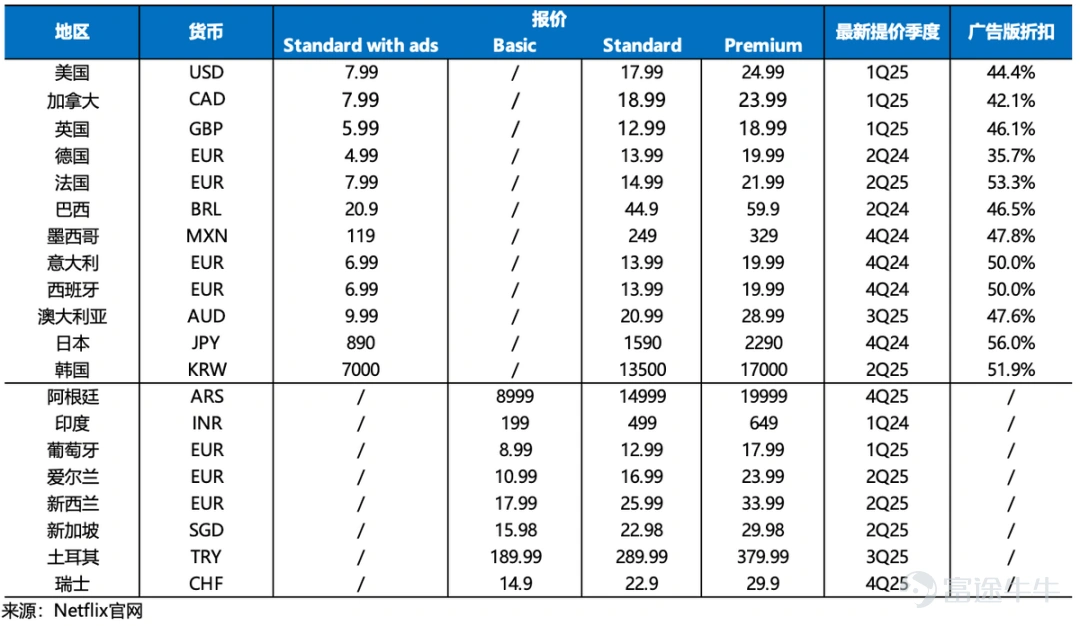

Although Netflix has seen strong momentum in user growth in international regions (mainly Asia) over the past year, the average revenue per user is less than half of that in North America. Therefore, short-term growth still relies on price hikes leveraging its monopolistic advantage in mature markets. Early 2025 saw successive price increases in North America and Europe, resulting in a noticeable pricing effect by the end of Q4.

In non-mature regions, however, price increases can easily suppress user growth trends, so Netflix does not raise prices frequently. In Q4 2025, the main price hike targeted Argentina for the third time within a year, purely to offset currency impacts.

Short-term outlook moving forward:

(1) For the first quarter of this year, Dolphin thinks that although it is the off-season, there might be a better-than-expected performance due to the airing of Season 4 of 'Bridgerton,' coupled with the late release of 'Stranger Things' at the end of last year, which could maintain its popularity into the beginning of the year.

(2) Looking at the current lineup for the second quarter, the number of top-tier IP content will significantly decrease. If there are no new hit contents scheduled afterward, there will still be a need for price hikes in some regions this year, along with higher requirements for the growth of other non-subscription revenues such as advertising and gaming.

II. Content investment target increased by 10%, but practical operations might see some control

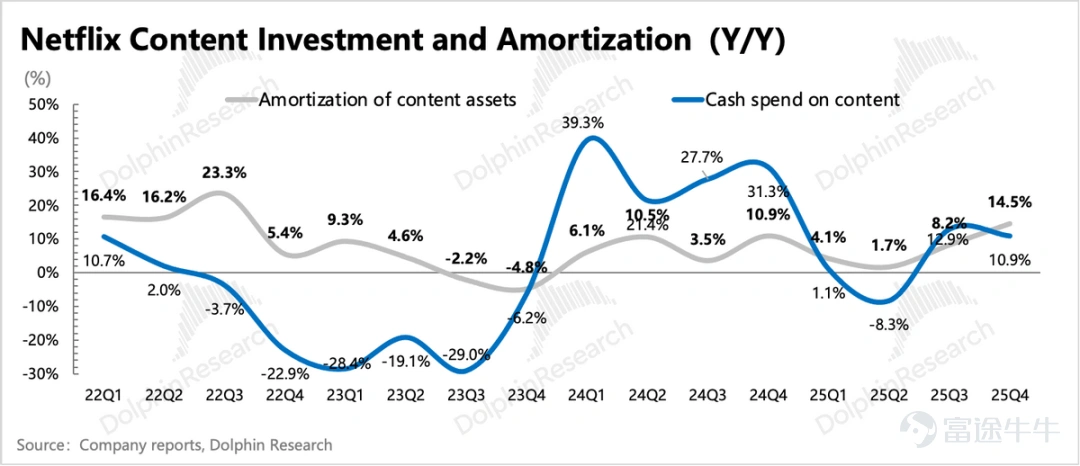

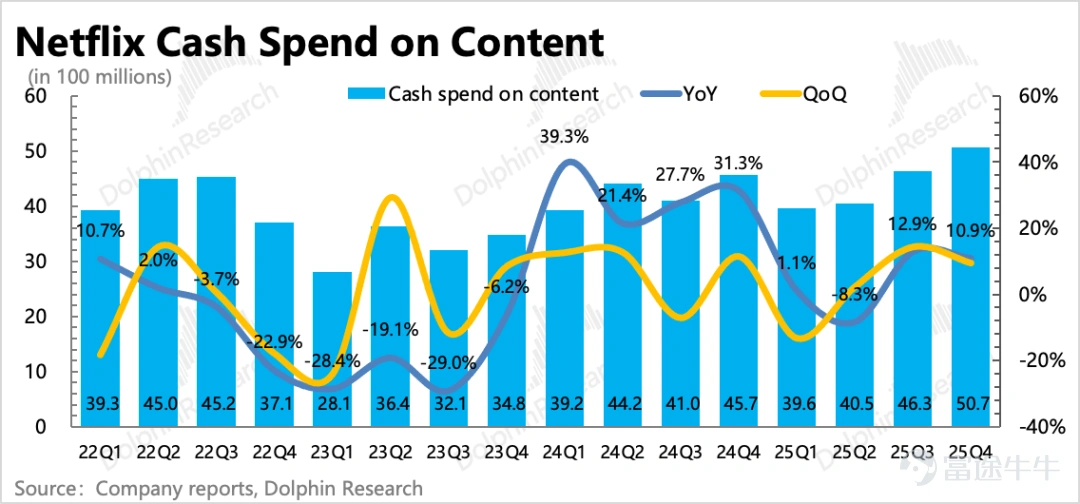

The pace of content investment by leading companies often reflects the intensity of industry competition; thus, Dolphin usually tracks the trends in content investment changes of Netflix and Disney. In Q4, Netflix's content investment was $5.1 billion, with a slight slowdown in growth compared to Q3.

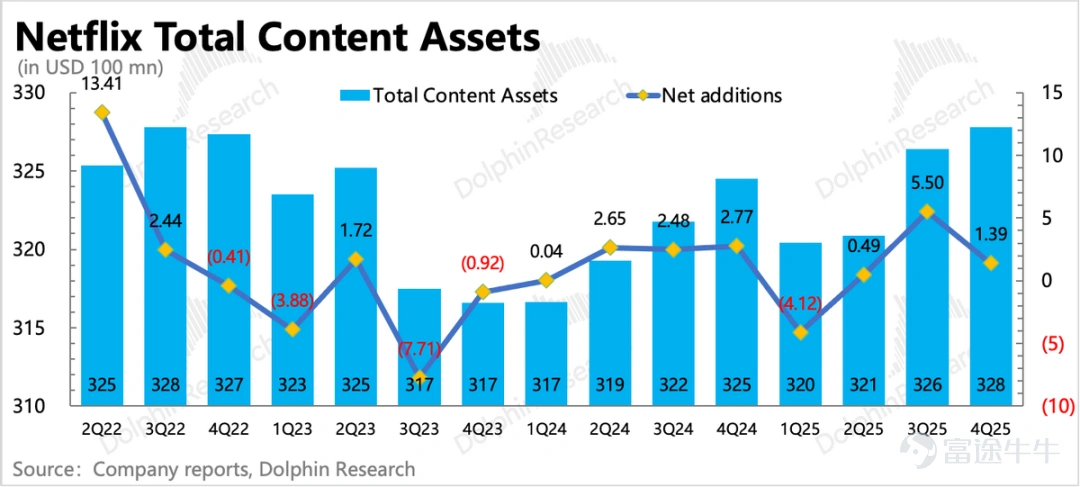

Total content investment for the year reached $17.7 billion, falling short of the initial target of $18 billion. With more blockbuster series in Q4 and increased amortization, the remaining content assets saw an increase of less than $200 million from the previous quarter.

Netflix revealed that the scale of content investment in 2026 will increase by 10% compared to 2025, reaching approximately $19.5 billion. However, considering the interest burden and cash flow pressure brought by the acquisition of WBD, we believe that actual content investment this year may also be somewhat controlled like last year.

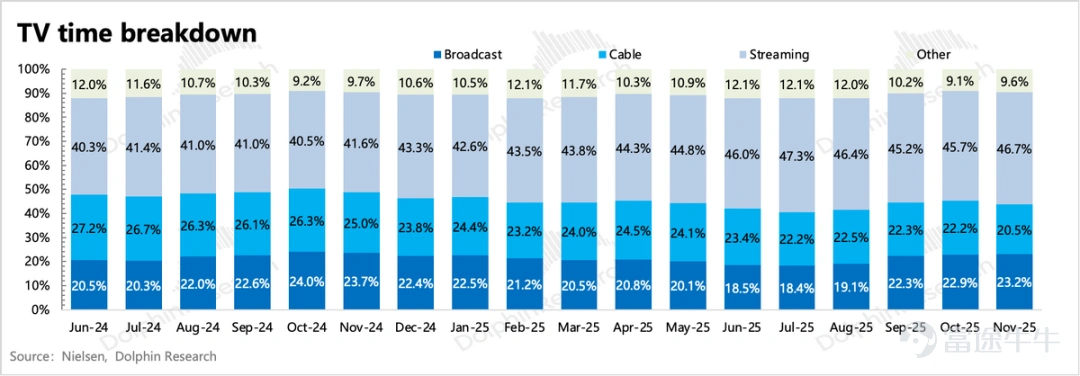

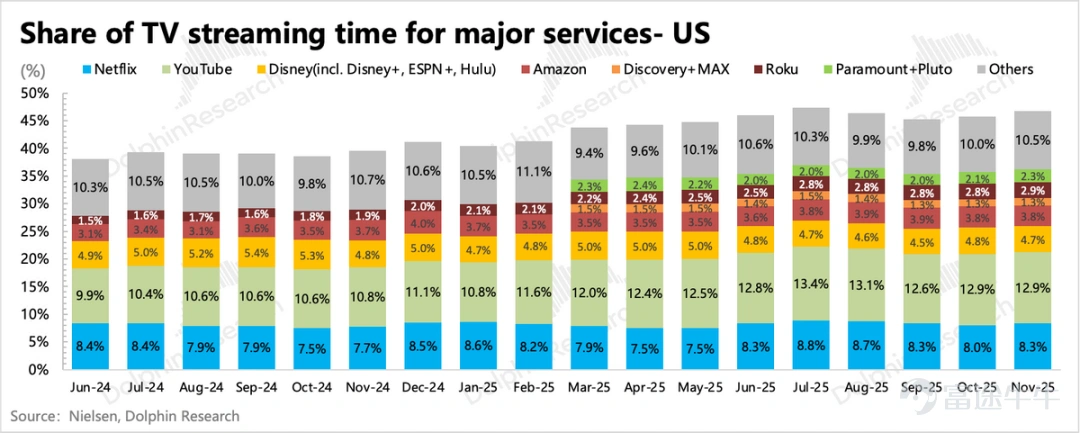

According to Nielsen's viewership share data in North America, as major content giants actively transition to streaming media, cord-cutting continues, with the viewing share increasing to 46.7%. Within streaming services, Netflix’s share remains relatively stable, and with more flagship content released in the second half of the year, user hours increased by 2% year-over-year, outperforming the growth rate in the first half of the year.

However, whether from the perspective of higher user thresholds or the impact of YouTube and short-form video platforms (TikTok, Reels), it indicates that user growth in the North American region has encountered some bottlenecks.

III. Profitability will improve in the long term, but cash flow faces short-term pressure

Netflix achieved an operating profit of nearly $3 billion in Q4, surpassing expectations. This was partly driven by higher-than-expected revenue, while the remaining Brazilian tax liability of less than $200 million was deferred to 2026 for payment, resulting in higher-than-expected profits for the period and lower-than-expected profits for 2026, although the impact magnitude was not significant. Ultimately, profit growth primarily hinges on revenue growth, so long-term growth issues warrant more attention.

Netflix's current free cash flow is close to $10 billion by 2025 and targets $11 billion for 2026. However, as of the end of last year, the company only had $9 billion in net cash on its books and faces $1 billion in short-term debt repayments over the next year. After switching to an all-cash approach, Netflix needs to apply for additional loans. On top of a previous $59 billion bridge loan, it has increased this by $8.2 billion. Meanwhile, it secured a total of $25 billion through an unsecured revolving credit facility to repay part of the bridge loan.

Therefore, with $42.2 billion remaining in bridge loans, the rough annual interest cost will be significantly higher than the potential savings on content licensing expenditures (between $2-3 billion) after acquiring Warner Bros. Discovery (WBD). Thus, if the acquisition process continues to be prolonged due to disruptions, the pressure on short-term cash flow will also increase.

In Q4, the company spent $2.1 billion repurchasing 18.9 million shares, with $8 billion remaining under the buyback program. To meet essential content investment needs and cover the additional interest burden mentioned above, further share repurchases will be suspended.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment