The Dilemma and Way Out of US Finance

By Chen Ningdi

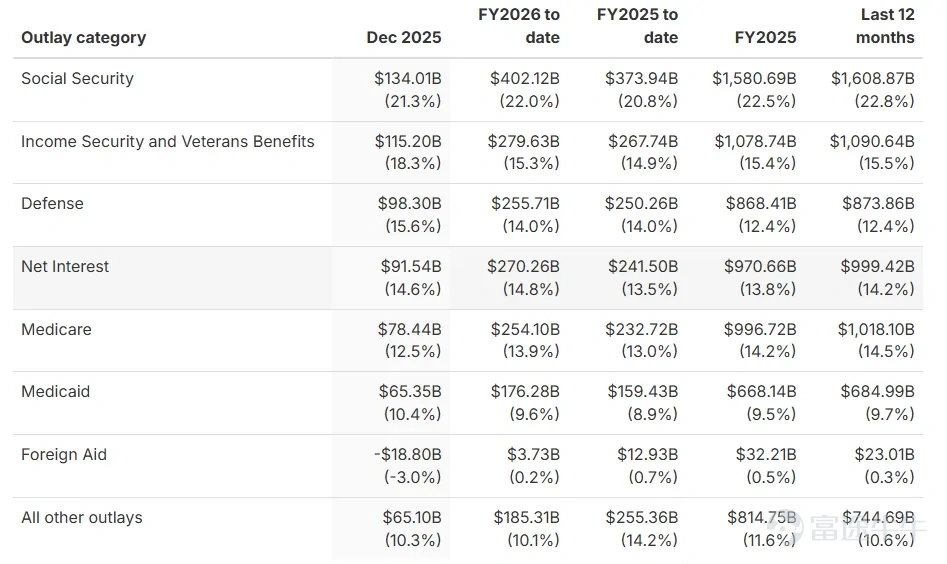

The US Treasury recently released fiscal data for the first quarter of fiscal year 2026 (October 2025 - December 2025). Fiscal revenue amounted to $1.22 trillion, an increase of 13.09% year-on-year; fiscal expenditure was approximately $1.83 trillion, an increase of 1.85% year-on-year; the deficit was approximately $602.4 billion, a reduction of $109 billion compared to the same period last year. What worries the market most in the fiscal expenditure is the continued rise in interest payments. Interest expenditure in the first quarter of fiscal year 2026 was about $270 billion, higher than $241.5 billion in the same period in 2025.

Figure 1: US fiscal expenditure data since the 2025 fiscal year, Source: Joint Economic Committee (JEC), U.S. Treasury

01 Rising interest continues, fiscal sustainability under pressure

There are two factors behind the interest: one is the total amount of government debt, and the other is the debt interest rate. Under the current system, there is almost no possibility of reducing the total amount of debt; the only adjustable factor is the interest rate. The annualized interest expenditure in the first quarter of fiscal year 2026 accounted for 3.6% of GDP, higher than 3.3% in fiscal year 2025.

Figure 2: Treasury debt balance since 2025, Source: Joint Economic Committee (JEC), U.S. Treasury

The average interest rate on the current US $38 trillion of government debt is 3.36%. According to the US Treasury yield data as of January 16, 2026, the 1-year yield is about 3.54%, the 2-year is about 3.59%, and the 3-year is about 3.66%; for shorter terms like the 6-month, it's around 3.63%, which is not lower than the 2-year. The very short end, such as 1-month and 2-month, is also mostly around 3.65%.

Figure 3: Average interest rate of U.S. Treasury bonds, source of information: U.S. Treasury

Therefore, if the Treasury prioritizes the lowest-interest maturities when issuing debt, it will more likely focus new issuance in the 1-3 year range, especially the relatively lower-cost 1-2 year segment, rather than the 10-year, 20-year, or 30-year maturities where rates exceed 4.2% or even approach 5%. Looking ahead, as low-coupon bonds issued during the low-rate period of the past decade gradually mature and need to be rolled over at higher rates corresponding to the current yield curve, the overall average financing costs will gradually rise, leading to increasing interest payments.

Figure 4: The amount of long-term debt maturing increases overall interest expenses, Source: MacroMicro

As interest payments continue to rise, the sustainability of US debt will come under market scrutiny! Especially since the fiscal deficit has not significantly narrowed, and interest expenditure already surpasses military spending, the US has reached a point where adjustments are unavoidable.

What cards does the Federal Reserve have to play?

1 Yield Curve Control

Amidst the backdrop of Powell being sued, the future independence of the Federal Reserve has been questioned by the market. It is highly possible that the Fed and the Treasury may revisit the old path of Yield Curve Control (YCC), which simply means committing to keeping Treasury yields near target levels by purchasing bonds. Specifically, this involves printing money to buy long-term Treasuries, expanding the balance sheet.

In October 2025, the Federal Reserve decided to halt balance sheet reduction. Currently, its balance sheet stands at approximately $6.5 trillion, having significantly contracted from the $9 trillion peak, setting the stage for the next round of quantitative easing. I believe that once interest payments exceed the Treasury’s expectations, the US will have no choice but to adopt YCC measures to suppress long-end rates. Suppressing long-end rates often results in upward pressure on short-term rates. If the decline in average funding costs remains unsatisfactory, I think the Fed may eventually prioritize inflation targets less and accelerate interest rate cuts.

2 Accelerated rate cuts, weaker dollar

If the Federal Reserve implements YCC while cutting interest rates, short-term liquidity will significantly improve at the cost of a weaker dollar and a decline in the US Dollar Index. At the same time, global commodities will begin to rise more rapidly under the combination of a weakening dollar and rising inflation expectations. Gold will be the first to benefit, followed by Bitcoin. We expect this trend to gradually emerge after March 2026, driving up asset prices.

3 Inflation is always present.

The policy mix of QE + YCC + rate cuts will drive up inflation in the United States. Especially in the current geopolitical environment, with Trump imposing tariffs, tightening immigration, and localizing supply chains, controlling U.S. inflation will be very challenging. This trend is expected to become evident in the second half of 2026.

Figure 5: U.S. inflation rate in 2025. Data source: U.S. Bureau of Statistics

From a long-term perspective, the fundamental solution to inflation lies in the success of the AI revolution in the United States, which would greatly enhance productivity. Robots could provide a large number of goods and services at low or even zero cost, and this scenario doesn’t seem far off.

Betting on AI: The Last Card for U.S. Economic Recovery

On January 6, Musk engaged in a three-hour in-depth conversation on the well-known American podcast Moonshots, during which he presented a vision of the future combining robots with AI and frankly stated:The enormous productivity growth brought by AI is the only way for the U.S. and even the world to resolve the massive national debt crisis.”

Musk spoke very decisively, mentioning a clear direction: AI must not only improve the efficiency of goods production but also bring services into this framework. Manufacturing improvements may seem limited given China’s highly competitive market, but services have huge room for improvement under the leadership of AGI (Artificial General Intelligence), which should be the focus in the future. In the past, it was difficult to standardize and scale services like factories, but the combination of robots and AGI could break down, standardize, and even automate services. Once this step is completed, the core issue of labor costs within inflation will be resolved.

Of course, AI breakthroughs require many hardware conditions to be met, such as energy, power grids, data centers, algorithms, and edge computing. Musk, Google, Meta, NVIDIA, and others are working hard on these challenges. Once breakthroughs are achieved, America's massive debt and deficit problems will be resolved. A leap in productivity is the only real solution to inflation. I will write an article specifically to share my thoughts on Musk's interview.

1.The US interest expenditure continues to rise, the scale of treasury bonds is out of control, and market doubts about fiscal sustainability are increasing.

2.It is expected that the Federal Reserve and the Treasury may adopt yield curve control measures to suppress long-term treasury bond rates in order to reduce interest. If the interest reduction is not significant, it may accelerate interest rate cuts, which could weaken the US dollar while significantly strengthening gold and Bitcoin. Gold is projected to surpass $6,000 by 2026, and Bitcoin is expected to exceed $150,000.

3. Reducing interest expenditures, curbing inflationary pressures, and forcefully lowering interest rates are all temporary solutions. Only breakthroughs in AI technology and widespread adoption of intelligent robots can drive productivity growth, which is the fundamental solution to address the massive debt crisis in the US and globally.

Author's Profile:

Chen Ningdi graduated from the University of Chicago with an honors bachelor’s degree in economics and statistics. He has over 26 years of experience in the global financial industry and founded Delin Securities and Delin Family Office. He was once the responsible person licensed by the Hong Kong Securities and Futures Commission for licenses type 1, 4, and 6. Currently, he serves as the Chairman of the Board, Executive Director, and Chief Executive Officer of Delin Holdings Group, Vice President of the Hong Kong Limited Partnership Fund Association, and authored 'The Era of Wealth Transformation: Uncovering Countercyclical Survival Wisdom.'

Disclaimer

This article is for reference only; investors should make investment decisions based solely on the information contained in company announcements.

The information and materials contained on this platform, including text, graphics, links, or other items from third-party information terminals, are for general reference purposes only. Under no circumstances does the information published on this platform constitute investment advice.

Without authorization from this official account, no one is allowed to reproduce the content without permission.

The content referenced on WeChat is for informational purposes only and is copyrighted by DL Holdings and relevant content providers. For the disclaimer, please visit the official DL Holdings website: https://www.dl-holdings.com/

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

3