Short-term Hong Kong stocks are being stirred by the 'deposit migration'; the biopharmaceutical sector in 2026 is worth looking forward to

The performance of the Hong Kong stock market over the past month has left many investors puzzled. On one hand, the US Dollar Index fell back below 100 again (since breaking below 100 in late November, it has continued to hover below that level), which is clearly a positive factor for Hong Kong's capital markets that operate under a linked exchange rate system. However, on the other hand, the Hang Seng Index has shown little progress during the same period, and the Hang Seng Tech Index, which includes leading technology companies, has experienced a significant pullback (the Hang Seng Index and the Tech Index have only slightly rebounded from last month’s weak performance by rising just 3.34% and 3.04%, respectively, in the first two weeks of this year).

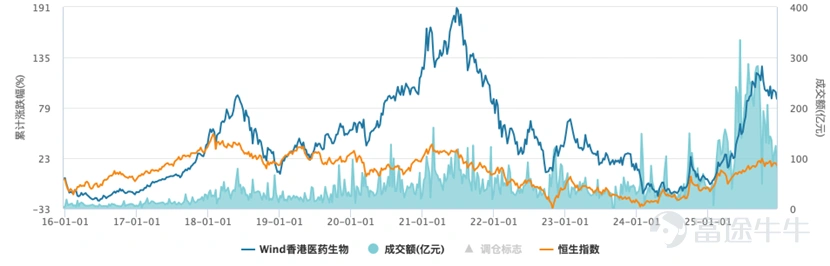

In contrast, the biopharmaceuticals sector has seen a 'big breakout.' For example, since entering 2026, Duality Biologics (09606.HK) $DUALITYBIO-B (09606.HK)$ has risen by more than 20% at one point, and Innovent Bio (01801.HK) $INNOVENT BIO (01801.HK)$ has also gained as much as 10% since the start of the year. Smaller enterprises in the industry, like Lee's Pharm (00950.HK) $LEE'S PHARM (00950.HK)$ have seen increases of up to 5%.

Standing at this point in early 2026, we may as well reorganize our analytical framework for the Hong Kong stock market to look ahead to Hong Kong's capital markets in 2026.

Core argument of this article:

First, the recent fluctuations in the Hong Kong stock market are mainly due to liquidity contraction caused by deposit migration, which will not alter the positive trend expected in the medium to long term;

Second, these risks will be mitigated by the influence of the newly appointed Federal Reserve Chair;

Third, the biopharmaceuticals sector in the Hong Kong stock market will have significant highlights in 2026.

Root Cause of Short-term Volatility in Hong Kong Stocks: Shift in Deposits

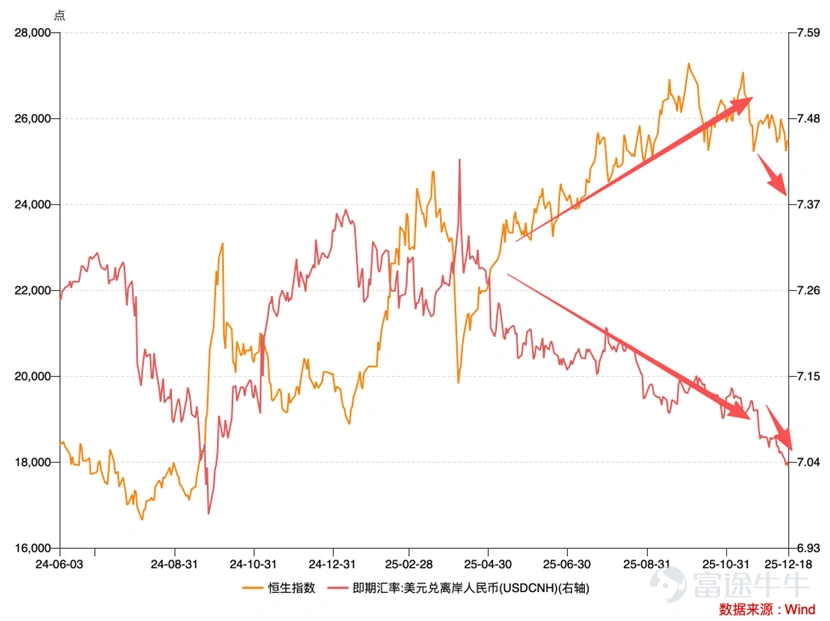

Previously, we considered 'offshore RMB' as the anchor for liquidity in Hong Kong stocks, leading to the reaction chain: 'appreciation of offshore RMB – market buys RMB and sells HKD – ample HKD liquidity – positive for capital markets.'

The success of DeepSeek and the Federal Reserve's interest rate cuts coincided in 2025. The former enhanced the valuation capabilities of Chinese tech companies listed abroad, while the latter brought overflowing US dollar liquidity into the Hong Kong market. Under the influence of these two factors, the two broken lines in the above chart show a high negative correlation, consistent with our previous analytical framework.

However, after late November, while offshore RMB maintained its appreciation trend, the Hang Seng Index entered an adjustment phase, breaking the original growth trajectory. As a result, market noise increased, and how to scientifically evaluate the relationship between liquidity and Hong Kong stocks was once again placed before us.

Before this, some institutions had already explained the above phenomenon from the perspective of 'southbound funds,' originating from the 'Guidance on Performance Evaluation Management for Fund Management Companies (Draft for Comments)' issued by regulators on December 6th, which requires fund companies to establish a performance evaluation system centered on investment returns and strengthen benchmark constraints.

As of the third quarter, mainland active equity funds had an excess allocation of approximately RMB 198 billion in Hong Kong stocks, with their Hong Kong stock holdings accounting for 30.8% of their total equity positions, while the proportion of Hong Kong stocks in their performance benchmarks was only 17%. This significant over-allocation raised concerns in the market that portfolio adjustments might lead to capital outflows.

The contraction in the scale of southbound fund inflows significantly disturbed the marginal effect on Hong Kong stocks.

We indeed recognize the driving value of southbound funds for Hong Kong stocks, but on the other hand, this still cannot explain the phenomenon of the reverse movement between exchange rates and the stock market. We must continue to focus on Hong Kong's financial market.

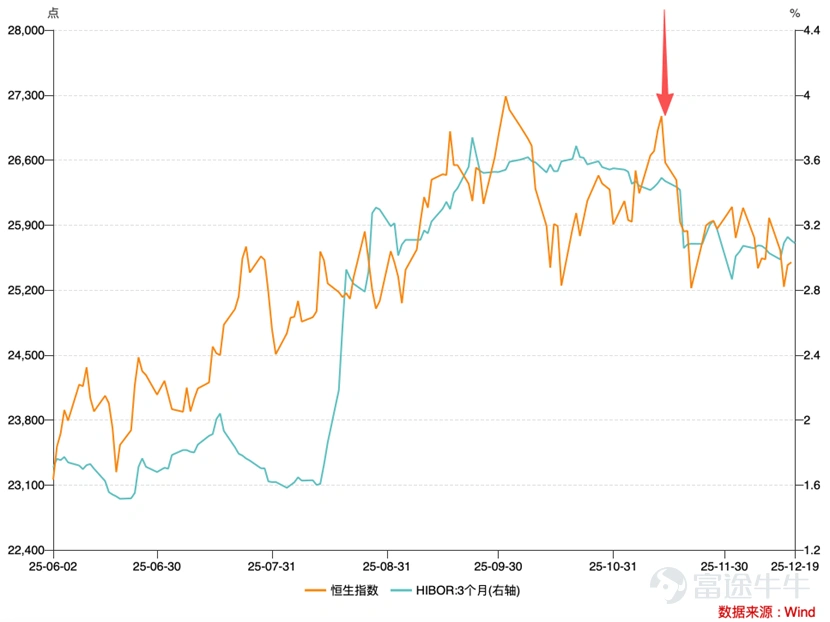

Finance textbooks often regard interest rates as the 'anchor' of liquidity (low interest rates represent strong liquidity). However, recently, when HIBOR (Hong Kong Interbank Offered Rate) declined, Hong Kong stocks were mainly characterized by contraction. Why can't this obvious positive factor be realized?

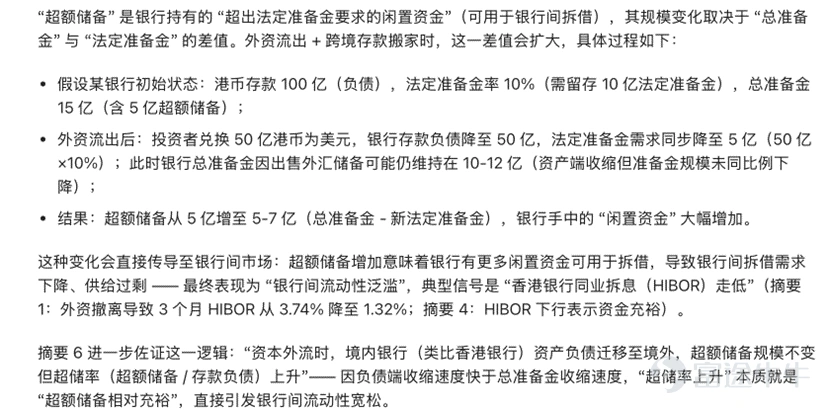

After studying Hong Kong's unique linked exchange rate system, we believe that the recent decline in HIBOR was essentially caused by the outflow of HKD deposits, not driven by improved liquidity.

Due to space limitations, we have posted the logic chain organized by AI for your reference.

In other words, the recent adjustment in Hong Kong stocks is certainly influenced by factors such as southbound capital in the short term, but the more important reason remains 'capital outflows,' leading to a tightening of liquidity in Hong Kong stocks. The chart below also shows a significant appreciation of the US dollar against the Hong Kong dollar in mid-November, coinciding with the adjustment period of the Hang Seng Index.

The appreciation of the renminbi has led to market participants scrambling to buy renminbi while selling Hong Kong dollars and transferring US dollar deposits simultaneously. These actions have helped us identify the underlying reasons behind the unusual recent movements in Hong Kong stocks.

As for why the above phenomenon occurred, we will skip the analysis process due to space constraints and only provide conclusions:

1) After November 2025, global capital markets' concerns about the 'AI bubble' have been increasingly amplified. At the same time, this period coincides with the sensitive timing of investment institutions reviewing their annual performance. Some institutions may choose to reduce their stock holdings based on the principle of securing profits.

2) US monetary policy remains uncertain, wavering between hawkish and dovish stances. During this period, overseas capital reallocates assets such as US Treasuries and gold, which negatively impacts Hong Kong stocks.

Hong Kong's biopharmaceutical sector in 2026 is worth looking forward to

We have already conducted a detailed analysis of the recent fluctuations in Hong Kong stocks from a mechanistic perspective. Next, we move on to the most important part of this article: what will be the trend and high-return sectors of Hong Kong stocks in 2026?

Since Hong Kong stocks are deeply influenced by the Federal Reserve, we can optimistically inform everyone that:

With the confirmation of the new Federal Reserve Chair, whether it is Kevin Warsh or Hassett, expectations for the Fed to cut interest rates in the first half of 2026 are very strong (Trump will use interest rate cuts as the main reference point in nominating his preferred candidate for Federal Reserve Chair). Although the market currently remains divided on future expectations, these divisions will end in the medium term once the new Fed Chair is finalized.

Afterward, the Hong Kong capital market will return to mainstream narratives, and the impact of liquidity on the capital market will also come to an end.

So, which sectors are more worthy of attention next? In this article, we focus on recommending the biopharmaceutical sector for three reasons:

First, in the short term, there will be no 'black swan events' in this sector.

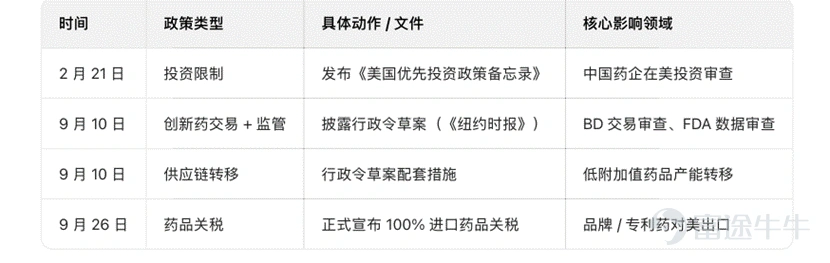

From February to September 2025, the Trump administration introduced policies successively, aiming to curb China's innovative drug internationalization process and global industrial chain participation through transaction reviews, regulatory thresholds, tariff pressures, supply chain shifts, and investment restrictions. The specific measures are as follows:

With the recent meeting between the leaders of both countries, consensus is gradually being reached on some core sensitive issues (such as the U.S. starting to lift the chip sales ban on China). Additionally, according to media disclosures, Trump is highly likely to visit China in April 2026. During this period, the probability of Trump introducing restrictive policies on the biopharmaceutical sector is extremely low.

Second, in 2025, China readjusted the procurement rules for medical insurance drugs, no longer using the 'lowest price' as a reference.

Previously, leading pharmaceutical companies secured medical insurance procurement orders by leveraging scale advantages and squeezing out medium-sized enterprises with 'irrationally low prices.' This not only increased the market share of industry leaders but also compressed the survival and R&D space of biopharmaceutical companies, constraining the pace of innovation in the industry.

As the first year of implementing the new procurement system, biopharmaceutical companies’ income statements will significantly improve in 2026. Given that the overall system design is more favorable to small and medium-sized enterprises, our outlook for SMEs is more optimistic.

So, which companies will we focus on recommending next?

In 2025, the biotechnology and pharmaceuticals sector in Hong Kong stocks significantly outperformed the broader market, showing solid 'growth stock performance.' The industry's average price-to-earnings ratio (ttm) was 37x, which is also at a relatively high historical level.

Considering the new variables for the industry in 2026 and current valuation capabilities, companies with excellent market performance in 2026 need to possess the following qualities:

1) Small and medium-sized enterprises, where the marginal effect of policies is more pronounced;

2) Companies with weaker valuation capabilities, where a value depression effect exists.

Based on this, our key recommendations are as follows:

Duality Biologics (09696.HK), an important partner of BioNTech SE, a global leading biotechnology company. In recent years, both parties have jointly developed next-generation ADC pipelines that are about to reach several milestones. For instance, their jointly developed next-generation B7H3 ADC, BNT324/DB-1311, is expected to initiate evaluation in 2026, specifically Phase III clinical trials as a first-line treatment for advanced metastatic castration-resistant prostate cancer.

Over the years, Duality Biologics has invested substantial research and development funds into cancer treatments, and 2026 could very likely be the 'harvest period' transitioning from R&D to output; this warrants close attention.

Lee's Pharmaceutical (00950.HK) currently trades at a P/E ratio below 10x but has been highly active in business expansion. Recently, it acquired Staccato One Breath Technology, a proprietary platform technology with broad therapeutic potential, creating synergies with its existing product pipeline and securing global rights as the licensor and manufacturer of Staccato Alprazolam. The company meets the dual criteria of being undervalued and benefiting from centralized procurement.

Sino Biopharm (01177.HK) primarily focuses on cardiovascular and liver disease treatments while actively developing drugs for oncology, pain management, diabetes, respiratory diseases, and other conditions. Recently, its developed Cumarasertib capsule received marketing approval (to be used in combination with Fulvestrant for treating hormone receptor-positive, human epidermal growth factor receptor 2-negative (HR+/HER2-) locally advanced or metastatic breast cancer patients who have undergone prior endocrine therapy). Considering its current P/E ratio of just 23x (below the industry average), its valuation is likely to rise in the short term alongside improving operational performance.

Despite significant volatility in Hong Kong stocks towards the end of 2025, some friends may feel disheartened and discouraged. However, within our framework, we remain optimistic and bullish about the capital markets in 2026. We hope this article provides new insights and assistance, and together, let us look forward to the market trends this year.

Author: Tiexin

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

3