Yuan Ji Yun Jiao Aims for IPO, Must Overcome Two 'Hard Bones'

Text by Yike Commercial, Author: Dachun, Editor: Yi’an

On January 12, 2026, Yuan Ji Food Group, the parent company of Yuan Ji Yun Jiao, officially submitted a main board listing application to the Hong Kong Stock Exchange, initiating the process for its IPO in Hong Kong and reaching a crucial moment toward becoming the 'First Dumpling Stock'.

For the general public, Yuan Ji Yun Dumplings is not a new face. Emerging from a Guangzhou vegetable market in 2012, it rose to prominence in 2020 by pivoting to fresh takeout stores due to the pandemic, and now firmly holds the leading position in the ready-made dumpling sector. It can be said that Yuan Ji Yun Dumplings is a capital market myth propped up by the 'Made-to-Order and Cooked on the Spot' concept.

According to the CIC Report, as of September 30, 2025, Yuan Ji Food is the largest Chinese fast-food company in China and globally in terms of store count. In the first nine months of 2025, Yuan Ji Food was also the largest dumpling and wonton enterprise in China, measured by GMV of dumpling and wonton products in the retail and foodservice industries.

However, this company is now facing the most stringent capital scrutiny due to its 'Made-to-Order and Cooked on the Spot' concept. The pre-made food controversy in 2023 and the food safety incident at the end of 2024 brought this rapidly growing company down from its pedestal, with issues pointing directly to an over-reliance on franchisee-based profit models and supply chain crises stemming from a lack of systematic management.

After experiencing growing pains, Yuan Ji Yun Dumplings launched comprehensive reforms in 2025. Although it managed to maintain the basic performance level, signs of growth concerns began to emerge.

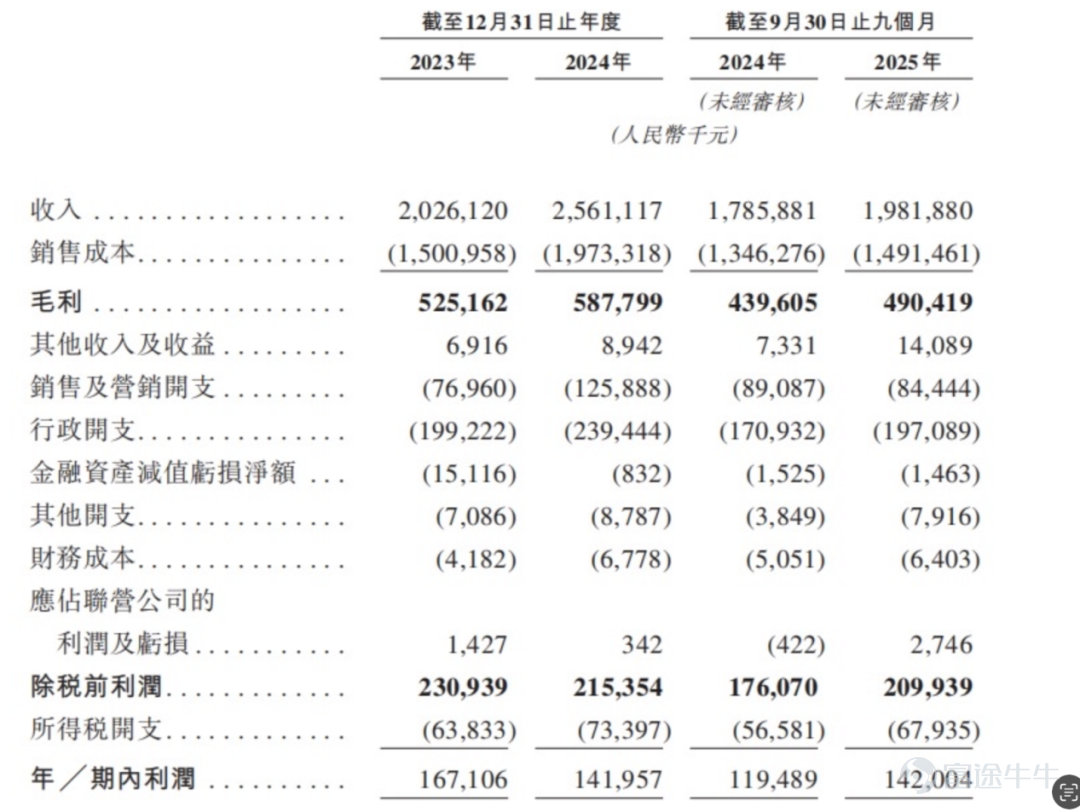

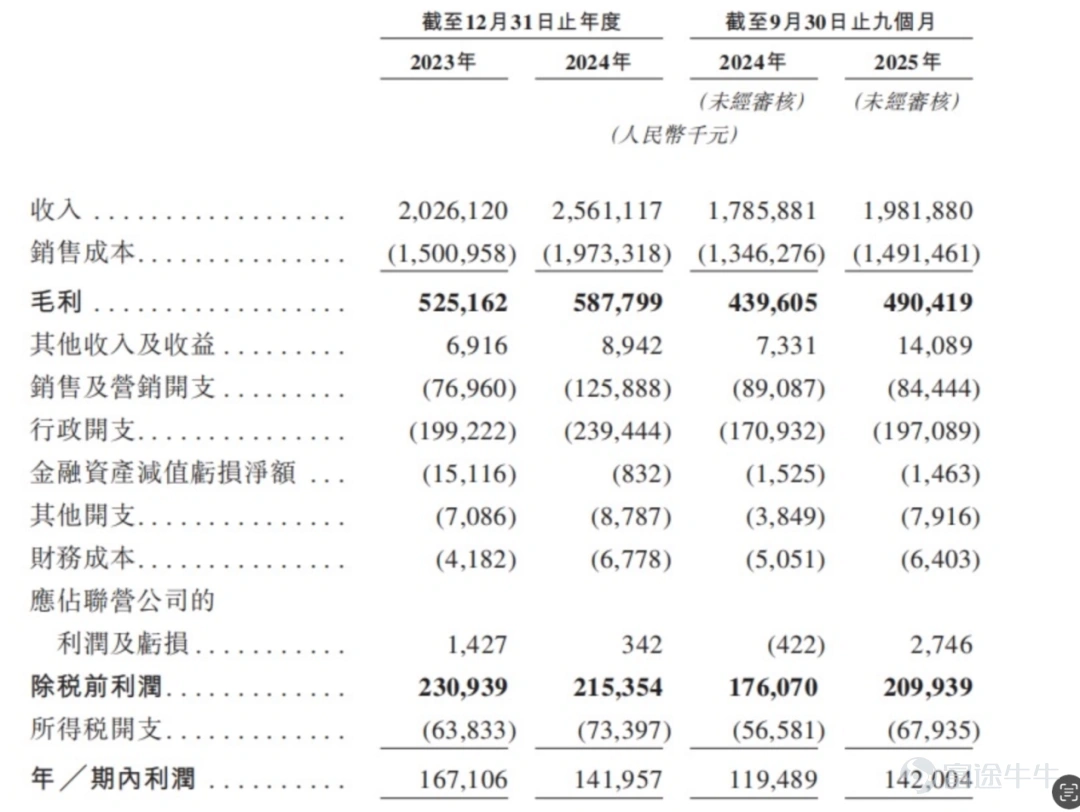

The prospectus shows that Yuan Ji Yun Dumplings' revenues for the first three quarters of 2023, 2024, and 2025 were RMB 2.026 billion, RMB 2.561 billion, and RMB 1.982 billion respectively; adjusted net profits were RMB 179 million, RMB 180 million, and RMB 192 million respectively, with revenue growth slowing and profits showing only slight increases.。

When the mental barrier of "made-to-order and cooked on-site" is breached, numerous imitators emerge in the "freshly made dumpling" sector. Can Yuan Ji Yun Dumplings, which relies on overseas expansion stories and lower-tier markets to push its IPO, tell a new story in the capital market? Facing uncertainties in lower-tier and overseas markets, can this dumpling giant overcome the two hard challenges of food safety and supply chain management before completing its Hong Kong IPO?

Yuan Ji Food has always been quietly making huge profits.

Before rushing for its IPO, Yuan Ji Food completed three rounds of financing, attracting a group of star investors including Black Ant Capital, Qicheng Capital, Yihai Kerry, and Xiamen C&D.

In June 2023's Series A round, Xiamen Black Ant No. 3 invested RMB 30 million to subscribe to 1.50% of shares, valuing the company post-investment at RMB 200 million; just two years later, in September 2025’s Series B round, RMB 150 million was raised for a 6% stake, raising the post-money valuation to RMB 2.5 billion; only three short months later in the B+ round, RMB 280 million was raised corresponding to an 8% stake, further pushing the post-money valuation to RMB 3.5 billion. Over just more than two years, its valuation skyrocketed by 16.5 times, achieving leapfrog growth.

Following intensive financing, on January 12, 2026, Yuan Ji Yun Dumplings’ parent company, Yuan Ji Food Group, officially submitted its application for a main board listing to the Hong Kong Stock Exchange, with Huatai International and GF Securities acting as joint sponsors, marking a key step in its IPO process.

Currently, among the shareholders, founder Yuan Lianghong controls 82.54% of the company's equity directly and indirectly, holding the core voting rights; major institutional shareholders include Xiamen Heiyi No. 3, Xinghan Chuangxiang, and Shanghai Yiying, while Foshan Xinxiangyuan, Foshan Yueshanhe, and Foshan Yuanyunjiao serve as employee incentive platforms, collectively holding over 13% of shares.

The influx of capital may reflect the market’s recognition of the Chinese fast-food sector and Yuanji’s expansion pace.

In its prospectus, Yuanji Yunjiao positions itself as the largest Chinese fast-food enterprise in China and globally, with a development scale worthy of the term 'largest.'

It started in 2012 from a vegetable market in Guangdong, focusing on wontons and dumplings; by 2018, the total number of Yuanji Yunjiao stores exceeded 100, and Suzhou Yuanji Factory officially began production, laying the supply chain foundation for subsequent scaled expansion and marking the first key milestone in its development.

Around 2020, community-based dining demonstrated strong risk resistance, making freshly cooked dumpling businesses highly sought after. Capitalizing on this trend, Yuanji Yunjiao broke through the competitive frozen dumpling segment with its 'community store' and 'handmade, freshly wrapped, and cooked' concept, surpassing 1,000 stores nationwide within a year and transforming from a regional brand into a national chain.

After 2023, the injection of capital further accelerated its expansion.

How large is Yuanji Yunjiao’s current scale? The answer is: number one.According to official brand information and Zhai Men Can Yan, as of September 2025, Yuanji Yunjiao leads with 4,266 stores globally among Chinese fast-food chains. Xiong Dawo and Xijiade have approximately 1,200 and 800 stores respectively, while Jixiang Wonton operates more than 3,000 stores under the 'small shops, big chain' model, but still lags behind Yuanji Yunjiao in scale.

In terms of coverage, as of September 30, 2025, Yuanji Foods has expanded across 32 provinces, autonomous regions, special administrative regions, and municipalities in China, as well as Southeast Asian countries, with industry-leading expansion speed during the period.

The key to Yuanji Yunjiao building its 'Dumpling Kingdom' lies in the word 'franchise.' According to the company’s prospectus, it employs a dual-brand strategy with 'Yuanji Yunjiao + Yuanji Weixiang,' establishing an 'integrated catering-retail' business model.

Yuan Ji Yun Jiao is a core catering brand with three standardized store models: dine-in stores, ready-to-cook takeout stores, and raw food takeout stores. Yuan Ji Wei Xiang, on the other hand, focuses on the retail sector, selling pre-packaged dumplings and wontons through supermarkets, ready-to-eat retail channels, and distributors, creating complementary scenarios.

The franchise model is the direct reason for Yuan Ji Yun Jiao's rapid scaling.According to the prospectus, as of the first three quarters of 2025, franchise stores accounted for more than 95% of the total number of outlets. As a leading brand in the dumpling and wonton segment, Yuan Ji Yun Jiao naturally attracts entrepreneurs due to its concentration in community streets and residential areas, where customer bases are more stable, follow-up marketing costs are lower, and returns are more controllable and significant, thus gaining investors' favor.

However, while the franchise model brought success, it also brought risks, with the hidden dangers of rapid expansion erupting in 2024. At the end of 2024, the 'earthworm incident' involving Beijing Yuan Ji Yun Jiao once triggered public opinion.This exposed deep issues of systematic loss of control in the franchise model and ongoing repercussions from the food safety crisis.

Under the shadow of a trust crisis, Yuan Ji Yun Jiao shifted its development focus from 'speed' to 'quality,' rapidly penetrating lower-tier markets while accelerating efforts to capture growth opportunities in overseas dining markets, and simultaneously embarking on a diversified product strategy to seek new growth solutions.

According to the prospectus, the share of Yuan Ji Food in third-tier and below cities has been increasing year by year, rising from 19.8% in 2023 to 26.6% in 2025 (as of September 30), while the proportion of stores in first-tier cities has been steadily declining from 58.1% to 51.0%, indicating progress in expanding into lower-tier markets, but the consumption ability in these cities may impact overall per-customer revenue and profitability.

Meanwhile, Yuan Ji Food has opened five stores in Singapore and will use this as a base to focus on developing the Southeast Asian market, while preparing to selectively enter East Asia, Europe, and North America, aiming to build a global brand.

The scale of the rapid surge cannot conceal the underlying anxiety of Yuan Ji Yun Jiao.

The prospectus shows that Yuan Ji Yun Jiao’s growth has started to slow significantly. The prospectus shows that in the first three quarters of 2023, 2024, and 2025, Yuan Ji Yun Jiao's operating revenues were RMB 2.026 billion, RMB 2.561 billion, and RMB 1.982 billion, respectively. Although revenue is still rising, the growth rate has shown a significant decline, with its revenue growth dropping from 26.4% in 2024 to 11% in the first three quarters of 2025.

In terms of profitability, during the same period, Yuan Ji Yun Jiao's gross profits were RMB 525 million, RMB 588 million, and RMB 490 million, respectively; the gross profit margins were 25.9%, 23%, and 24.7%. Although the gross profit margin in the first three quarters of 2025 rebounded slightly compared to 2024, it still did not reach the level of 2023.

Image/Yuanji Cloud Dumpling Prospectus

The loss of growth momentum mainly stems from Yuan Ji Yun Jiao's profit model being overly reliant on suppliers and the supply chain.The prospectus shows that Yuan Ji Food's main source of income is selling ingredients to franchisees, i.e., producing fillings, dough, and other foods in factories and selling them to franchise stores. These franchise stores then sell food to consumers through dine-in, take-out of cooked and raw foods, as well as delivery services.Essentially, they are making a markup from franchisees.

Therefore,There are two key factors affecting Yuan Ji's profitability: the first is the willingness of franchisees to join; the second is the turnover efficiency of the supply chain.The number of franchisees and their revenue directly determine the revenue ceiling of Yuan Ji Food. If a large number of franchisees incur losses or close their stores, Yuan Ji Food's revenue will be immediately impacted.

For franchisees, the key issues are return on investment and the payback period, which are closely related to the revenue generated by individual stores.

According to its prospectus, the total GMV of the stores increased by 31% from RMB 4.772 billion in 2023 to RMB 6.248 billion in 2024. For the nine months ended September 30, 2025, the GMV was RMB 4.789 billion. During the same period, the total number of orders rose from 180 million, to 250 million, to 210 million, showing an overall upward trend.

Notably, the GMV per order has shown a declining trend. According to the prospectus data, the GMV per order may have dropped from RMB 26.1 in 2023 to RMB 24.7 in 2024, and then further to RMB 22.8 in the first three quarters of 2025.

While the number of stores and total orders continue to rise, the average spending per order keeps decreasing due to industry pressures and price wars, keeping both the gross profit per order and the net profit per order at low levels.

In other words, for investors, the same investment now requires more effort and a longer period to achieve the same returns, naturally dampening investment enthusiasm.The data also supports this.The prospectus shows that the number of Yuan Ji Food franchisees as of the end of the third quarter of 2023, 2024, and 2025 were 1,656, 1,956, and 2,065 respectively, with fewer new franchisees being added.

Under these circumstances, it is not easy for Yuan's Food to attract new franchisees, and the exposure of food safety incidents only adds to their challenges.。

Following the food safety incident, Yuan Ji Yun Jiao initiated significant reforms, inviting Zhang Jun to serve as COO of Yuan Ji Yun Jiao, introducing professional third-party monitoring companies, establishing a 365-day, 24-hour negative review instant warning mechanism, and promoting quasi-direct management measures... Undertaking comprehensive reforms ranging from emergency response mechanisms to the franchise management system, supply chain optimization, and organizational restructuring.

The prospectus reveals that under the category of 'sales and marketing expenses,' its full-year sales and marketing expenses surged to RMB 125 million in 2024, marking a substantial increase of 63.6% year-on-year. Administrative expenses rose from RMB 199 million to RMB 239 million, eroding the current period's profits. As of the first three quarters of 2025, although administrative expenses dropped to RMB 197 million, they were still equivalent to the entire 2023 level. This indicates that internal organizational system reforms are underway, but the associated costs remain difficult to cut.

For Yuanji Foods, a long-term structural risk is its leading scale but significantly lagging profitability compared to industry peers.

The prospectus shows that Yuanji Foods’ gross margin has consistently fluctuated around 25%. This figure is far lower than listed Chinese catering companies, such as Xiaocaiyuan and Green Tea Group, whose gross margins are over 60%, as well as 'the first Chinese noodle stock' Meet Noodles, which also reports a gross margin above 60%.

The root cause of profitability being much lower than leading companies in the industry lies in an imbalanced product cost structure.

It should be noted that Yuanji Foods mainly profits from the price difference of supplying franchisees rather than end-market premiums, causing its single-store profitability to be significantly lower than high-ticket restaurant brands.This model determines that its profit potential is constrained by supply chain pricing mechanisms.

In the upstream supply chain, Yuanji Foods is heavily affected by raw material costs.The prospectus reveals that from 2023 to September 2025, material costs accounted for over 85% of total sales costs, reaching as high as 87.5%, with pork procurement alone making up 35%. A high proportion of low-margin ingredients indicates room for improvement in cost control capabilities.

In the mid-to-downstream supply chain, inventory and turnover efficiency have a significant impact.This model is consistent with the per-order profitability logic of mega chain brands like Mixue Ice City. Its profitability is built on the absolute scale of store numbers and order density, converting low per-order profits into stable overall returns through extreme cost control and massive order volumes.

This model has obvious advantages but also prominent disadvantages. Yuan Ji Yunjiao supplies fillings, dough, and other short-shelf-life ingredients to over 4,000 franchise stores. While it maintains efficiency in ensuring freshness and controlling inventory loss during rapid order growth, once order growth slows, the pressure from fixed costs and supply chain expenses will quickly become apparent.

However, it's clear that Yuan Ji Food’s supply chain efficiency still needs improvement. The prospectus shows that Yuan Ji Yunjiao’s inventory turnover days for the first three quarters of 2023, 2024, and 2025 were 15.5 days, 12.1 days, and 15.0 days respectively, showing significant fluctuations. This reflects unstable supply chain management efficiency, and as stores continue to expand, inventory management pressures may further increase.

To improve profitability, a key influencing factor is to enhance the profitability of individual stores, but this is not an easy task.

Yuan Ji’s 'freshly wrapped, freshly cooked' selling point is essentially a business of trust. Around 2024, Yuan Ji Yunjiao was exposed for using a central kitchen model similar to Xibei’s, where the dumpling wrappers and pork fillings used in their stores were frozen products. This psychological gap directly labeled Yuan Ji Yunjiao with a reputation of 'pseudo fresh preparation.'

Adding to this, the 'user finds worm incident' caused Yuan Ji Food’s reputation to plummet to rock bottom, exposing problems in its franchise model: the lack of a sound emergency mechanism and an effective franchisee management system.

Moreover, factors impacting the revenue composition of individual Yuan Ji stores include competition from similar brands, price wars on food delivery platforms, and channel diversion.

After the trust crisis, the 'freshly wrapped, freshly cooked' model was widely imitated by competitors. Brand mindshare and competitive moats faced challenges. In this context, numerous local restaurants started promoting offers like '15.8 yuan all-you-can-eat freshly wrapped dumplings' or '24 yuan all-you-can-eat,' including free side dishes, fruits, and drinks.

The revenue of individual Yuan Ji Yunjiao stores heavily depends on offline foot traffic from nearby communities. However, given the relatively fixed population coverage and consumption frequency of a community store, combined with some consumers unwilling to pay full price, achieving single-store revenue growth becomes challenging.

Meanwhile, Yuan Ji Yunjiao faces intensifying online competition. After the 2025 food delivery war, a large number of orders flowed to low-cost channels like Pin Hao Fan, where countless merchants sell 12 dumplings for 9.9 yuan. Yuan Ji Yunjiao was forced into this price war, increasing marketing investments and issuing coupons to compete for customers.

Under internal and external pressures, Yuan Ji Yun Jiao, which has adhered to the 'freshly-made' model, has fallen into a passive situation, with its core value being diluted by disorder.

The prospectus shows that the net proceeds from Yuan Ji Yun Jiao's Hong Kong IPO will mainly be used in five key areas: digital and intelligent construction, overseas market expansion and supply chain development, brand building and product research, supply chain upgrading, and replenishing working capital for general corporate purposes.

Whether expanding overseas or domestically, Yuan Ji Yun Jiao must tackle two tough challenges: the 'pre-made VS freshly-made' concept and 'supply chain and cost control.' These not only directly affect consumers' perception of the brand but also influence its future commercialization capabilities. How long can Yuan Ji Yun Jiao keep the aroma of its 'freshly-made' dumplings going? We'll have to wait and see.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1