Netflix Q4 Earnings Preview: 2026 Guidance, Advertising, and Warner 'Regulatory Put Option'

$Netflix (NFLX.US)$ Netflix will release its Q4 2025 earnings report and full-year 2026 guidance after the US stock market closes on Tuesday.

Since the Q3 earnings report, Netflix's stock price has dropped by -27%, significantly underperforming the S&P 500's +3% rise. The uncertainty brought by the acquisition of Warner is one of the main factors.

Investor concerns lie in:whether the deal will turn Netflix from a 'high FCF + low leverage + buyback machine' into a new entity characterized by 'content asset integration + rising leverage + regulatory uncertainty'.Even with strong fundamentals,the pending M&A itself could increase valuation discount/volatility.

Options Strategy Handbook

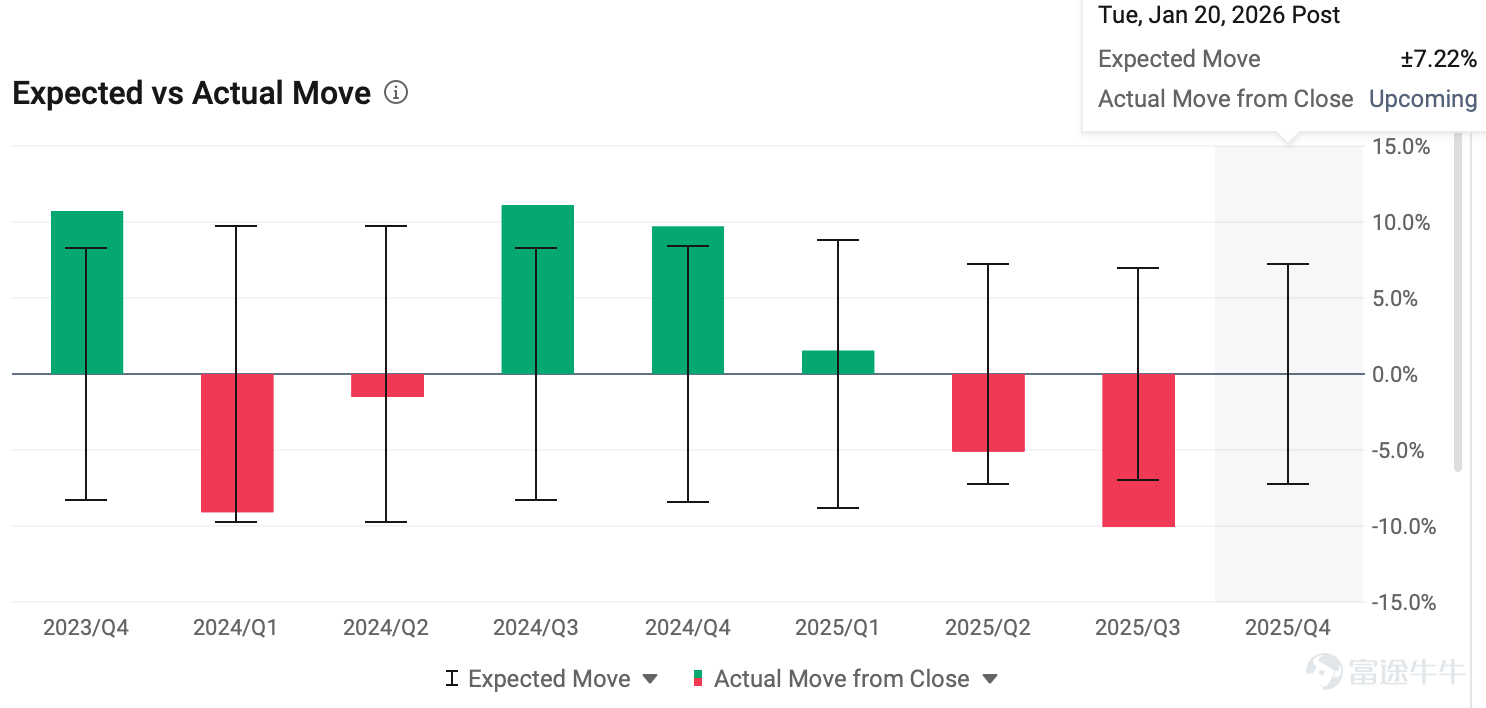

The options market implies a post-earnings stock price fluctuation ofPlus or minus 7.22%。

The current put/call ratio is 0.88, indicating slightly bullish market sentiment. The implied volatility is approximately 46% , which is considered a moderate level based on the IV rank. If expecting a post-earnings stock price movement exceeding 7.2%, one could consider being an options buyer.

Core Financials

Analysts expect Q4 2025 revenue to reach $11.96 billion, representing a 16% year-over-year increase; GAAP EPS is forecasted at $0.55, reflecting a 29% YoY growth.

According to Bloomberg consensus estimates,the gross margin for Q4 is forecasted at 45.3%, with an operating profit margin of approximately 24.1%. Q4 is typically Netflix's major content release season and a key marketing period, leading to higher related expenses.Additionally, in Q4 2025, Netflix set aside an annual supplementary provision of approximately USD 165 million due to a tax dispute in Brazil.

What is the market focusing on?

1) Q4 earnings growth drivers: price hikes, content, and live streaming pushing 'viewing hours' higher

Content and viewing (engagement) remain the foundation

- According to Nielsen, streaming is approaching 50% of U.S. TV time and continues to take share from cable and broadcast television (in November, streaming reached 46.7%, up 5 percentage points year-over-year; Netflix increased by 0.6 percentage points year-over-year to 8.3%).

Live/Sports: More critical for 'ad inventory' and 'ad tier penetration'

In the two NFL Christmas games,The Lions–Vikings game had a global AMA (average minute audience) of approximately 30.5 million, and the other game,Cowboys–Commanders, had a global AMA of about 22.4 million。

– The boxing match,Jake Paul vs. Anthony Joshua,had Netflix reporting a globalAMA of approximately 33 million。

2) Advertising business: Moving from 'storytelling' to a phase of 'focusing on details'

Key quantitative metric: 190 million MAVs (measured by 'individuals' rather than 'accounts')

- JPM: Netflix Global190 million MAVs(Monthly Active Viewers), defined as 'the number of members watching at least 1 minute of ads per month × average household size'.

- Reuters also reported on the MAV metric, emphasizing it as a milestone for the advertising business.

'Pipeline' development: Ad platform, DSP, and measurement partners are in place; the next step is to improve fill rates and programmatic share.

- Netflix already hasthousands of advertisers, its self-developedNetflix Ads Suite, and integration with multiple third-party DSPs (such as Amazon, Google DV360, The Trade Desk, Yahoo, etc.) and50+ measurement partners。

– Ads are still primarily based onIO (Insertion Order, direct client orders) , but are expected to gradually shift towardsprogrammaticas the main method; and it is clear thatthe ad tier is still diluting overall ARM, and it may take a few more years to catch up with the standard tier (through higher fill rates and more advertisers).

Product iteration: Interactive ads and Dynamic Ad Insertion (DAI) are the 'incremental levers' for 2026

– Currently being tested in the US and CanadaModular ad formats and interactive video adsand plans to expand the delisting scope to the entire European Economic Area by the end ofGlobal rollout around Q2 2026; while testing in select markets and librariesDAI (Dynamic Ad Insertion), to scale up in 2026.

– Netflix's official 'Three Years of Advertising' update also mentioned the expansion of programmatic partners and progress on Ads Suite.

3) Warner Deal: A 'major source of noise' beyond fundamentals, but it may also reshape Netflix’s capital structure narrative

– Netflix’s bid for Warner assets is cash plus stock at $27.75/share; and expects to use$50 billion in new borrowingsto finance the current bid.

– The deal values Warner at approximately$82.7 billion(including$72 billion in equity value + assuming about $10.7 billion in net debt))。

– If the acquisition is completed, Netflix’s debt could jump from 'close to $15 billion' to about$75 billion; the company's target for cost synergies is$2–3 billion annually(Achieved within three years).

– The “breakup fee” in the acquisition agreement, amounting to a staggering5.8 billionUSD. If the deal falls through due to regulatory non-approval or unexpected issues, Netflix will have to pay this hefty penalty to Warner.

- The transaction has already submitted antitrust filing documents, and will next undergo strict reviews by institutions such as the U.S. Department of Justice and the Federal Trade Commission. The entire process is expected to take 12 to 18 months. Approval is anticipated to be completed by the earliest in the third quarter of 2026.

Summary

The market’s focus isn’t on Q4 growth but rather on whether future growth can be more certain. The main concern now lies in how the Warner acquisition has fundamentally shifted Netflix’s investment logic from "Stable pricing increases + cash cow driven by ad revenue growth"" to "Event-driven stock characterized by M&A integration and regulatory negotiation". In the short term, pricing power will clearly shift away from earnings reports themselves towardwhether the deal can close, how financing will occur, how high leverage will rise, and antitrust risks.。

If the acquisition and IP integration can be completed smoothly,in the future, under the dual growth drivers of 'subscription price hikes + scaled advertising,' revenue and free cash flow are expected to continue rising over the long term.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

4

23