[IPO Watch] Embodied Robotics Leader Jiuv Smart: Growth Anxiety of a Profitability Star

The listing boom in Hong Kong's robotics sector continues to heat up. With$UBTECH ROBOTICS (09880.HK)$ 、$DOBOT (02432.HK)$ 、 $ONEROBOTICS (06600.HK)$ As companies like Geekplus-W and Ubtech Robotics successively listed on the Hong Kong stock market, with companies like RoboSense and Standard Robots in the queue, Jiuwu Intelligence also launched its bid to the Hong Kong Stock Exchange on January 19.

This is not Jiuwu Intelligence’s first attempt at accessing capital markets. In February 2022, the company initiated A-share IPO coaching but later terminated it in December 2025 due to adjustments in market conditions and business needs, shifting focus to the Hong Kong market. Behind this move lies an urgent demand for funding, brand upgrading, and global expansion.

While most companies in the embodied intelligence track are mired in losses, Jiuwu Intelligence stands out as a 'consistent profit maker.' Backed by its full-stack technological barriers and leading position in niche markets, it has become a potentially high-quality target on the Hong Kong stock market. However, lurking concerns such as over-reliance on the clean energy industry and high customer concentration persist. This journey to the Hong Kong market serves both as an endorsement of its industry standing and the ultimate test of its ability to break through growth bottlenecks.

Full-stack technology foundation, binding top-tier clients

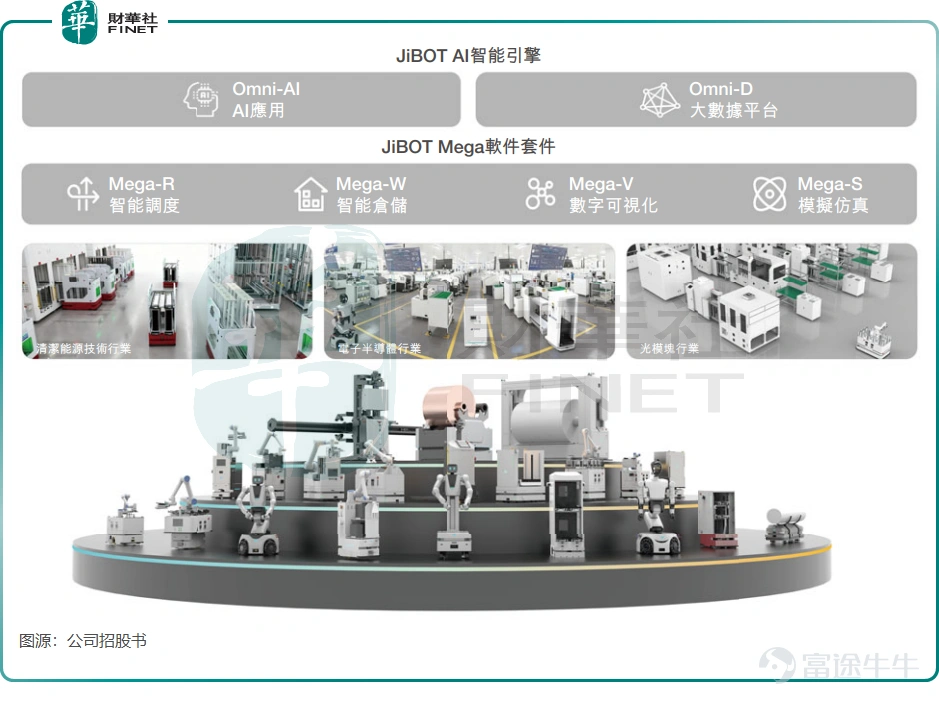

Jiuwu Intelligence is an intelligent embodied industrial robotics company primarily focused on designing, developing, and deploying multi-form intelligent embodied industrial robots with perception, decision-making, and interactive capabilities for the industrial sector.

According to the prospectus, the company’s product portfolio includes more than 150 models of intelligent embodied industrial robots, covering key stages of the entire production process.

Jiuwu Intelligence's core competitiveness stems from its full-stack self-developed capabilities. Unlike some peers that rely on external technologies or components, the company has built a complete technological system ranging from core hardware to software systems. Its self-developed JOS robot operating system is adaptable to complex operations in multiple scenarios. Deep synergy between hardware and software supports Jiuwu Intelligence’s diverse range of robot models, which can cover critical processes in crystal pulling, wafer slicing, semiconductor packaging, and more.

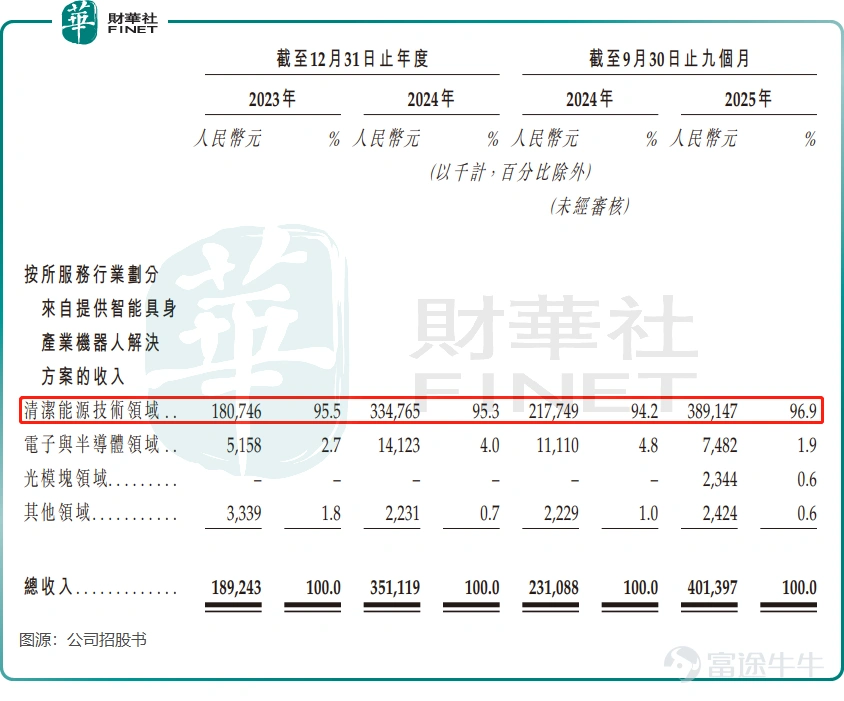

A precise focus on top-tier clients is another major advantage. The company concentrates on the clean energy and electronic semiconductor sectors. In the photovoltaic field, it provides customized solutions for LONGi Green Energy (601012.SH)’s Jiaxing plant and Tongwei Co., Ltd. (600438.SH)’s Meishan plant. In the electronic semiconductor field, it has deep collaborations with TFME, Luxshare Precision (002475.SH), and leading optical module manufacturers. From 2023 to September 2025, the company sold over 11,000 embodied industrial robots to 156 clients across 16 industries, 48 of which were publicly listed companies or their subsidiaries, showcasing strong client quality.

Market position and sales growth lead simultaneously. According to Frost & Sullivan data, in 2024, Jiuwu Intelligence ranked second in the domestic intelligent embodied industrial robot solutions industry with a 5.9% market share, ranked first in the clean energy sector, and fourth in the electronics and semiconductor sector. In terms of sales volume, it reached 2,267 units in 2023, increased to 4,178 units in 2024, and broke through 4,700 units in the first three quarters of 2025, doubling within just over two years, with scale effects gradually emerging.

The industry's rare 'profit champion'

Against the backdrop of widespread 'burning money for growth' in the intelligent robotics sector, Jiuv Wu Intelligent's sustained profitability has become one of its biggest highlights.

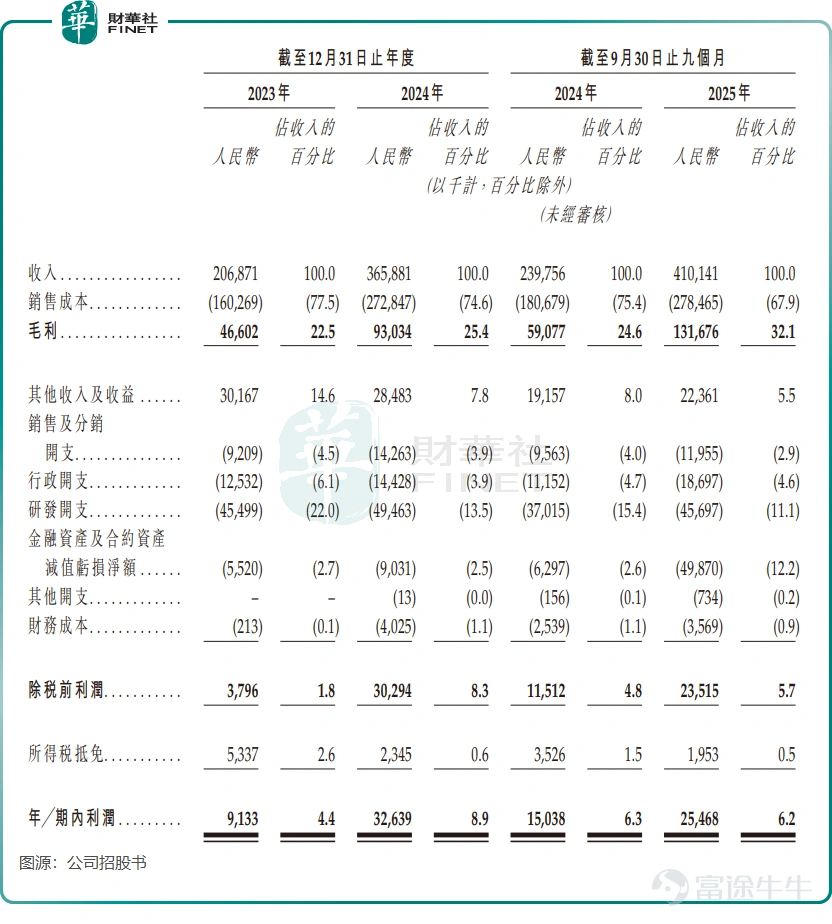

The company’s financial data is impressive, with revenues of RMB 207 million and RMB 366 million in 2023 and 2024 respectively, further increasing to RMB 410 million in the first three quarters of 2025, representing a year-on-year growth rate of 71.1%. Profits during the period also surged significantly, soaring from RMB 9.133 million in 2023 to RMB 32.639 million in 2024, reaching RMB 25.468 million in the first three quarters of 2025, continuing the high growth trend.

The continuous improvement in gross margin has been an important factor supporting profitability, rising from 22.5% in 2023 to 32.1% in the first three quarters of 2025, approaching the gross margin levels of Ubtech Robotics and Geekplus-W in the first half of 2025. This is mainly due to cost optimization brought by in-house research and development of core components such as LiDAR, as well as economies of scale released by increased sales volumes.

An efficient operating model is another key factor. The company's major customer retention rate of 72.7% exceeds the industry average, bringing stable repeat purchases through high stickiness and significantly reducing new customer acquisition costs. This is reflected on the expense side, where its sales and marketing expenditure ratio has continued to decrease, standing at only 2.9% in the first nine months of 2025, lower than most peers.

The advantage of a 'high retention + low marketing' cost-efficiency ratio has driven a virtuous cycle of revenue and profitability. However, it is necessary to be cautious as the net profit margin fell back to 6.2% in the first three quarters of 2025, primarily dragged down by RMB 49.87 million in asset impairment losses, putting the quality of earnings to the test.

Suffering from single-track dependency, urgently needs to expand into new scenarios

Behind the impressive profitability, Jiuv Wu Intelligent's growth model has obvious shortcomings.

The company's performance is highly tied to clean energy industries such as photovoltaics, with income from this sector accounting for a staggering 96.9% in the first three quarters of 2025. Although riding the wave of high industry prosperity, sectors like photovoltaics are heavily influenced by policy and production capacity cycles, and any fluctuations in demand or intensifying competition will directly impact earnings stability.

The high concentration of customers further amplifies risks. Revenue from the top five customers exceeded 60% in the first three quarters of 2025, mainly from photovoltaic clients. This not only could weaken the company’s bargaining power but also brings the risk of earnings volatility due to changes in client cooperation.

Cash flow pressure has become a hidden pain point. In 2024, the company's net profit was RMB 32.639 million, but the net cash flow from operating activities was -RMB 150 million; although this divergence eased somewhat in the first three quarters of 2025, it still exists. This reflects the heavy reliance of revenue growth on accounts receivable and longer customer payment cycles, which constrain the pace of R&D and expansion.

Developing a second growth curve has become an essential task for Jiuv Intelligence, with the electronics and semiconductor sectors as well as the optical module field emerging as key areas to break through. The company has already achieved success in the electronics and semiconductor industry, with sales growing by 62.9% year-on-year from 2023 to 2024, alongside deepening cooperation with Tongfu Supermicro and Luxshare Precision; in the optical module sector, it has secured partnerships with leading manufacturers, entering a high-growth track. Additionally, the company is expanding into automotive and medical fields, attempting to replicate its successful experience in the photovoltaic industry.

The prospects for new application scenarios are broad, but challenges coexist. The rapid release of automation demands in the electronics, semiconductor, and optical module industries provides room for growth, and the proceeds from this IPO will focus on multi-field expansion and increasing core component production capacity. However, significant differences in processes across industries demand higher adaptability and stability from robots, necessitating continuous R&D and customized innovation. At the same time, the company faces fierce competition from peers like Geekplus-W and Standard Robots, making scenario expansion quite challenging.

Conclusion

Jiuv Intelligence’s push for a Hong Kong stock listing coincides with a capitalization window for the robotics industry. The combination of 'full-stack technology, sustained profitability, and leadership in niche markets' is likely to attract capital market interest. If the IPO succeeds, it will not only replenish cash flow but also accelerate the exploration of new scenarios and global expansion, solidifying its position in the industry.

However, the test of the capital markets goes beyond short-term performance to focus on the sustainability of long-term growth. For Jiuv Intelligence, the core challenge after listing will be maintaining its advantage in the photovoltaic sector while quickly unlocking growth potential in new scenarios, reducing reliance on specific industries and customers, and genuinely improving cash flow and profitability. This journey to Hong Kong's stock market is both an affirmation of past achievements and a test of future potential.

Author: Yuan

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

1