Taiwan Semiconductor's strong earnings ignite the US semiconductor sector!

Detailed Analysis of Taiwan Semiconductor's Latest Earnings: A Bold Bet Exceeding $52 Billion on the Future

Text | China Finance Press

The world's largest wafer foundryTaiwan Semiconductor (TSM.US)Announced its Q4 results for the fiscal period ended December 31, 2025, becoming the first and most representative AI technology company to release quarterly earnings.

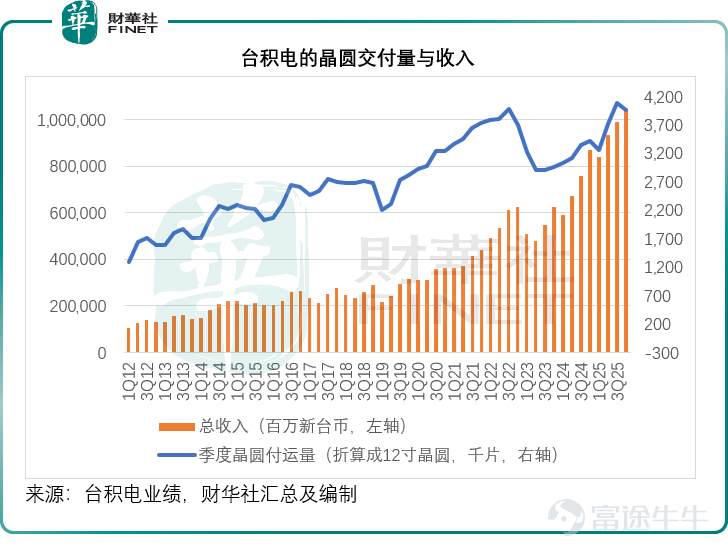

Driven by a surge in AI computing power demand, Taiwan Semiconductor’s latest quarterly earnings hit new highs. In Q4, its wafer shipments (converted to 12-inch wafers) grew by 15.89% year-on-year to 3.961 million units, with quarterly revenue rising 20.45% year-on-year to NT$1.05 trillion, as shown in the chart below. For the full year, revenue increased by 31.60% year-on-year to NT$3.81 trillion.

In terms of technological processes, the most advanced 3nm products accounted for 28% of Q4 revenue, up two percentage points from the same period last year and five percentage points higher than the previous quarter. Meanwhile, 5nm and 7nm process revenues contributed 35% and 14%, respectively. Collectively, products using processes below 7nm (advanced processes) accounted for 77% of total wafer revenue, compared with 74% in both the same period last year and the previous quarter.

For the full year, 3nm accounted for 24% of revenue, while 5nm and 7nm revenues contributed 36% and 14%, respectively. The total revenue contribution from processes below 7nm reached 74%, five percentage points higher than the 69% in 2024.

By platform, high-performance computing (HPC) remained its largest revenue source, accounting for 55% of Q4 2025 revenue, up 2 percentage points year-over-year but down 2 percentage points from the previous quarter. Smartphones maintained a 32% share, down 3 percentage points year-over-year but up 2 percentage points from the previous quarter.

Compared with Q3 2025, smartphone demand rebounded significantly. Q4 revenue grew 11% sequentially, while HPC grew by 4%. Digital consumer electronics declined by 22%, and automotive revenue fell slightly by 1%. See the chart below.

Due to cost improvements, favorable exchange rate movements, and further increases in capacity utilization, its Q4 2025 gross margin reached 62.3%, surpassing the previously guided range of 59.0% to 61.0%. This represents a year-over-year increase of 3.3 percentage points and a quarter-over-quarter rise of 2.8 percentage points.

For the full year, the 2025 gross margin was 59.9%, up 3.8 percentage points year-over-year, primarily driven by higher capacity utilization and cost optimization, offsetting unfavorable currency impacts and margin dilution from overseas wafer fabs.

The operating profit margin for Q4 2025 increased by 5 percentage points year-over-year and 3.4 percentage points quarter-over-quarter to 54.0%, significantly exceeding the previously guided range of 49.0%-51.0%, mainly due to improved cost efficiency.

For the full year, the operating profit margin reached 50.8%, up 5.1 percentage points year-over-year, benefiting from improved operating leverage.

Driven by this, Taiwan Semiconductor's Q4 net profit attributable to shareholders grew 34.98% year-over-year to NT$505.744 billion, with quarterly return on equity (ROE) at 38.8%, up 2.6 percentage points year-over-year and 1.1 percentage points quarter-over-quarter.

For the full year, Taiwan Semiconductor's 2025 net profit attributable to shareholders was NT$1.72 trillion, up 46.42% year-over-year, with return on equity (ROE) at 35.4%, an increase of 5.1 percentage points year-over-year.

Taiwan Semiconductor also provided guidance for Q1 2026 performance, expecting the gross margin to rise by 170 basis points to 64% at the midpoint, benefiting from ongoing cost improvement efforts, including enhanced production efficiency and capacity utilization, offsetting the continued dilution from overseas wafer fabs.

Management outlined six influencing factors for their 2026 outlook during the earnings call.

On one hand, management expects overall capacity utilization in 2026 to increase moderately, with N3 gross margin anticipated to surpass the company’s average level at some point in 2026.

At the same time, Taiwan Semiconductor is also improving the production efficiency of its wafer fabs to increase output and strengthening cross-node capacity optimization, including flexibly allocating capacity between the N7, N5, and N3 nodes to optimize profitability.

On the other hand, management expects that as overseas expansion scales up, the dilutive impact of overseas wafer fab capacity ramp-ups on gross margin will initially be between 2% to 3%, later expanding to 3% to 4% in the coming years. Additionally, the initial ramp of its 2-nanometer technology will start negatively affecting gross margins in the second half of this year, with a full-year dilution effect for 2026 expected to be between 2% to 3%.

Moreover, uncontrollable exchange rate fluctuations will also impact its 2026 performance.

In Q4 2025 and for the full year 2025, Taiwan Semiconductor’s capital expenditures were TWD 356.91 billion and TWD 1.27 trillion (approximately USD 40.9 billion), representing a year-on-year decrease of 1.39% and a year-on-year increase of 33.10%, respectively.

As the world races to advance AI capabilities, Taiwan Semiconductor, which supports computational power, is no exception. Its full-year 2025 capital expenditure shows a significant increase, and this trend will continue into the coming years. The company forecasts its 2026 capital expenditure budget to be between USD 52 billion and USD 56 billion, with approximately 70%-80% allocated to advanced process technologies, 10% for specialty technologies, and about 10%-20% for advanced packaging, testing, photomask manufacturing, and other projects.

Management also mentioned that due to rising costs at leading-edge nodes, Taiwan Semiconductor faces increasing manufacturing cost challenges. For example, equipment costs are becoming more expensive, and process complexity is growing. Therefore, the capital expenditure required to build 1,000 wafers per month capacity for the N2 process far exceeds the amount needed for the N3 process with the same capacity. The capital expenditure cost per thousand wafers for the A14 process will be even higher. Meanwhile, Taiwan Semiconductor faces additional cost challenges from global manufacturing layout expansion, new investments in specialty technologies, and inflationary cost pressures, all contributing to higher capital expenditure levels.

However, management stated they will maintain strategic pricing to reflect their value while collaborating with suppliers to optimize cost efficiency. They will also boost production volume and drive greater cross-node capacity optimization in wafer fab operations to improve profitability. With these efforts, management believes it is achievable to sustain a gross margin above 56% in the long term.

Every time C. C. Wei speaks at Taiwan Semiconductor’s quarterly earnings conference, he discusses industry developments and forecasts, and this time was no exception.

He estimates that the industry average growth rate of what he defines as 'Foundry 2.0' (including all logic wafer manufacturing, packaging, testing, photomask production, etc.) is 16%, while Taiwan Semiconductor's revenue growth in dollar terms reached 35.9%, surpassing the industry average.

He forecasts that with strong support from AI-related demand, the industry average growth rate of Foundry 2.0 could reach 14% by 2026, while Taiwan Semiconductor’s growth rate is expected to approach 30%.

He pointed out that AI accelerators accounted for 19% of total revenue in 2025. Looking ahead, the usage of AI models in consumer, enterprise, and sovereign AI sectors is rising, driving demand for computing power, thereby supporting robust demand for advanced wafers, which presents opportunities for Taiwan Semiconductor.

To this end, Taiwan Semiconductor will continue to increase its capacity, raise capital expenditures to support customers’ future growth, expedite the schedules of existing wafer fabs as much as possible, and improve production efficiency while optimizing capacity across nodes.

At the same time, he raised his revenue growth forecast for AI accelerators, expecting a compound annual growth rate (CAGR) of 55%-60% from 2024 to 2029, with long-term revenue CAGR potentially approaching 25%. AI accelerators will be the largest source of its revenue growth, but four platforms—smartphones, high-performance computing, IoT, and automotive—will also play a driving role.

In terms of capacity, management stated that construction of the third wafer fab in the U.S. has begun, permits are being sought to start construction on a fourth wafer fab and a fourth advanced packaging facility, and they have just purchased a large nearby plot of land to support their expansion plans. They intend to expand into an independent mega-fab cluster in Arizona to meet customer needs.

The first specialty technology wafer fab in Kumamoto, Japan, began mass production at the end of 2024 with good yields, and construction of the second fab has also started. Its technology and capacity ramp-up will depend on customer demand and market conditions.

In Europe, local commitments have been secured, and the construction of the specialty technology wafer fab in Dresden, Germany, is proceeding as planned. The capacity ramp-up plan will depend on customer demand and market conditions.

Multiple phases of 2-nanometer wafer fabs are being prepared in the Hsinchu and Kaohsiung Science Parks, with investments in advanced process technologies and advanced packaging facilities to be made locally in the coming years.

Finally, C.C. Wei mentioned the latest progress on N2 and A16: N2 is set to enter mass production in Q4 2025 at the Hsinchu and Kaohsiung sites, with good yields, and strong demand is seen from smartphone and high-performance AI applications, with a rapid ramp-up expected in 2026. Meanwhile, Taiwan Semiconductor has introduced N2P, an extension of the N2 family. N2P offers further performance and power advantages over N2 and is scheduled for mass production in the second half of this year.

Taiwan Semiconductor has also introduced the A16 technology with the industry's best ultra-power rail characteristics. A16 is most suitable for high-performance computing products with complex signal paths and dense power networks. Mass production is proceeding as planned for the second half of 2026.

Interestingly, during the earnings call, an analyst asked about Intel (INTC.US) receiving support from Trump, NVIDIA (NVDA.US) both investing in and becoming a customer of Intel, and rumors that Apple (AAPL.US) might also invest in Intel and collaborate with them. When asked if Taiwan Semiconductor is concerned about losing market share, management stated they are not worried because technological evolution is complex and takes a long time. They are confident Taiwan Semiconductor can maintain its business growth.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1