Dividend Income Cheat Sheet: June Dividend Season Is Here—Earn Up to HK$1,596 Per Lot!

In Hong Kong stocks, the lowest-profile stocks have made more money

Others' fear is the best source of excess returns. When a stock trades at 2 times PE and offers a 20% dividend yield, a company doesn’t need to achieve great growth—just relatively normal profitability almost guarantees excess returns.

Everyone loves to buy into high-end businesses. AI, chips, autonomous driving – at the very least, it needs to be a consumer brand with emotional value. Otherwise, a stock can hardly be considered 'sexy' by the market.

Many companies and individuals also try hard to align themselves with these hot topics – one moment they want to do AI, the next they want to make cars, then robots, and even replace Ctrip – it’s not hard to understand, as these fields tend to yield higher capital returns.

But in fact, over the past 1-3 years, there has been a large number of 'ultra-low-end' quality assets in the Hong Kong stock market. Many of them are contract manufacturers, without technological sophistication, their own brands, or huge growth potential, yet their stock prices have surged at super-high speeds of 50%, 100%, or even 400%.

This is no coincidence but an era-defining opportunity brought by the Hong Kong stock market under specific historical conditions. And judging from the data, this opportunity hasn’t come to an end yet.

01 Low, but profitable

While everyone's attention is focused on AI, robotics, and autonomous driving stocks like Horizon, Kingsoft, and SMIC, some seemingly 'ultra-low-end' businesses are quietly raking in massive profits.

In the eyes of tech investors, Wintime Handbags Holdings isn’t even worth a glance. It’s a contract manufacturer whose main business is producing handbags for international fashion brands like CK and Lululemon, both of which are its clients.

And in this day and age, everyone knows that to make money, you must have your own brand. Even PDD Holdings, known for white-label products, keeps emphasizing helping merchants build brands. Countless contract manufacturers have flooded into Douyin (TikTok), attempting to transform into consumer brands through live streaming, and even going as far as opening flagship stores on JD.com and Taobao.

In such an era, companies primarily engaged in contract manufacturing are simply not favored in the capital markets.

Its share price is only HKD 1, with a total market capitalization of less than HKD 500 million. Recently, its daily trading volume often hovers around HKD 30,000-40,000, lower than a month's salary of a typical white-collar worker in Hong Kong.

It has no concept, no technological content, and no growth prospects (the industry is not a blue ocean). According to the stock-picking logic of many stock influencers and fund managers, this is undoubtedly a junk stock.

But in fact, the return of this stock over the past year was higher than Xiaomi, Pop Mart, and Laopu Gold, surpassing 150%.If we extend the timeframe to the past three years, its return reached an astonishing 400%, even outperforming one of the AI star stocks, Google. It ranks just behind super star stocks like NVIDIA and Palantir.

Not only that, but this company also offers an annual dividend yield of over 10%. If dividends are reinvested, its total return would increase significantly, approaching 500%.

What is excess return? This is excess return.

If luxury handbags at least carry some emotional consumption value and can be considered as 'concept stocks' for luxury goods and emotional spending, then Nanxuan Holdings’ main business area is even more 'low-end'.

Its main business is 'operating sewing machines'.Its production scope includes OEM manufacturing of products such as women’s wear, men’s wear, cashmere, scarves, and hats.

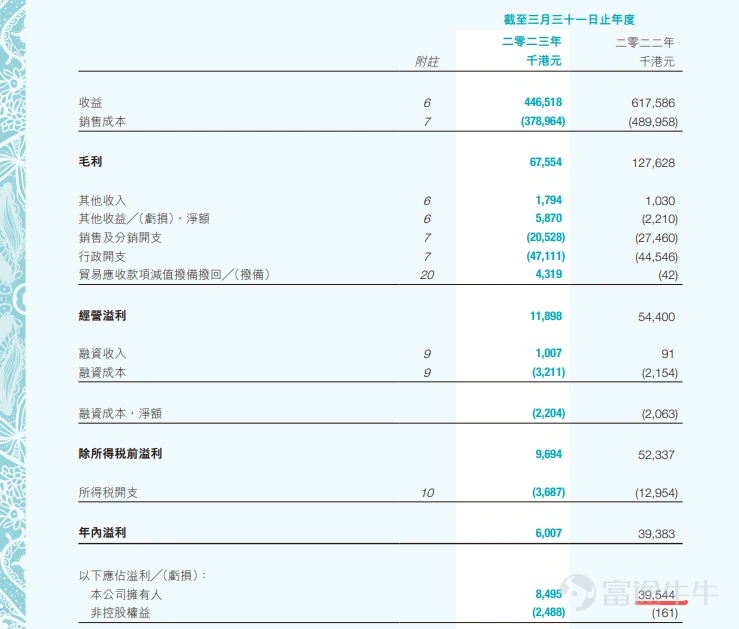

In its latest earnings report, its adjusted operating profit margin was 11.9%, which looks decent. However, contract manufacturing remains a capital-intensive business, with capital expenditures reaching HKD 250 million in the half-year report for the fiscal year 2026. Currently, its forward P/E ratio has fallen below 4 times.

This stock may not be glamorous, but it makes money.

Over the past three years, the share price of Nanxuan Holdings surged more than 220%, and over the past year, it rose more than 40%. Its returns not only outperformed the broader market but also surpassed many high-profile technology stocks. Moreover, Nanxuan's dividend yield is as high as 12%. If dividend reinvestment is taken into account, its three-year return could approach 300%.

Caption: The share price trend of Nanxuan Holdings over the past three years looks no worse than those AI technology stocks.

In the Hong Kong stock market, there are many such ordinary OEM businesses, such as Minghui International Holdings. This is a company that produces shampoo, transparent soap, shaving kits, and other products for hotels, with the renowned Shangri-La Hotels Group as one of its clients.

Of course, such businesses are not the darlings of the capital market. Its market value has fallen below net assets, with a share price of only around HK$1 — but this does not mean that buying this stock will not be profitable.

Over the past three years, the share price of Minghui International has risen more than 130%. If we factor in the 10% dividend yield and reinvested dividends, the return can approach 180%.

Although it cannot compare to the gains of Pop Mart or Laopu Gold, this return rate surpasses Tencent's performance over the past few years.

The stories of these enterprises are not isolated cases but rather a widespread phenomenon: over the past few years, some quality OEM factories in Hong Kong-listed stocks that sew clothes, make glue, produce soap, or manufacture high heels have delivered significantly higher stock returns compared to star companies in industries like the internet.

Why have they risen so much?

It is simply because their earnings were not as bad as the market had expected three years ago. Around 2022, due to factors such as market conditions, the performance of these companies experienced significant fluctuations.

However, their adjustment speed was extremely fast. In the past few quarters, the financial results of the aforementioned companies have remained stable, with slight growth amid stability. For instance, in Nanxuan Holdings' half-year report for the fiscal year 2026, revenue increased slightly by 1.6% year-over-year.

Low-end contract manufacturers may lack imagination, but they fulfill a basic necessity — not much growth potential, but also not much risk of contraction. After all, people can skip trendy toys, avoid donkey-hide gelatin, and abstain from baijiu, but how could they possibly stop wearing clothes, using shampoo, or wearing shoes?

Moreover, contract manufacturers are not AI; there won’t be substantial capital inflows into this sector that lead to abnormally fierce competition. Although their businesses may seem unattractive, they benefit from economies of scale, exclusive distribution rights, and supply chain management as moats — not easily replaceable.

The end result is that their profit margins are not low. Take Ming Hui International as an example: its gross margin of 22.7% actually surpasses most automobile manufacturers, including high-end brands like Tesla and Nio.

Of course, growth and business models are not the core reasons for these stocks' exceptionally high returns; cheapness is.

02 2x P/E ratio — how could it not make money?

If the dividends in US stocks stem from the flood of hot money after the AI boom — driving up valuations — then the dividends in Hong Kong stocks are quite the opposite: they come from capital outflows — being too cheap.

In 2022, Hong Kong stocks experienced a crash, with the Hang Seng Index plummeting 35% in just 10 months. This created a large number of low-priced stocks; even internet giant Tencent fell to around HKD 200, with a P/E ratio comparable to contract manufacturers.

Star stocks dropped to valuations of contract manufacturers, let alone real low-end manufacturing companies: Huaxin Handbags' stock price fell to around HKD 0.2, with a market cap dropping to about HKD 80 million, and it further declined by over 20% in 2023.

How cheap was this price?

This company reported a net profit close to HKD 40 million in the fiscal year 2022. Although profits fluctuated significantly in 2023, in 2022, its net profit was still close to HKD 40 million, quickly recovering thereafter. In the two natural quarters of Q2-Q3 2023 (which correspond to the 2024 fiscal year), the net profit exceeded HKD 20 million, equivalent to an annualized net profit of approximately HKD 40 million.2x forward PE.

Even considering the potential contraction in performance, at its stock price low, it could recoup its cost solely through dividends within 7 years, with an annual dividend yield close to 20%. Some high-interest loans don't even offer such a high rate.

Caption: Huaxin Handbags financial report

The market cap of South Rotating Holdings also dropped to around 450 million HKD by mid-2022, with its share price hovering at about 0.2 HKD, while in the fiscal year 2022, its net profit was still 260 million HKD —Still 2x PE (trailing).

Of course, South Rotating Holdings experienced fluctuations in net profit at that time, but even based on FY2023, which marks the trough in net profit, its PE is only 4x, still too low. Not to mention the dividends; in 2022, South Rotating Holdings distributed around 0.06 HKD per share as dividends — meaning it would take just 4 years of dividends to break even.

This is the advantage of 'low-end industries.' They have little room for growth, so most management teams are quite generous with dividends. Besides South Rotating Holdings, there's also Stella International, which produces shoes for brands like Deckers. In 2022, during the stock price low, this company could break even through dividends alone within five years.

In hindsight, these were extremely irrational prices. But in the fear-driven Hong Kong stock market, few would be optimistic about these stocks. After all, even 'tech stocks' were being ignored, and some internet platform companies fell below their net cash value, with certain internet firms trading less than 50,000 HKD in a day.

When no one was buying Tencent at 200 HKD, how much capital would flow into these manufacturers?

Other people’s fear is the best source of excess returns. When a company trades at 2x PE and offers a 20% dividend yield, it doesn’t need extraordinary growth. As long as profits remain relatively stable, it almost inevitably leads to significant excess returns.

Is this the era of opportunity for Hong Kong stocks?

From the perspective of PE and dividend yield, even after three years of sharp increases, these companies are still not expensive.

Nanxuan Holdings’ forward PE has dropped to around 3.5 times, with a TTM P/E of only about 6 times, while its dividend yield is as high as 12.14%, indicating extremely generous dividends. Huaxin Handbags’ PE remains around 5 times, with a dividend yield exceeding 10%.

Caption: Still too cheap.

Not mentioning these relatively small manufacturers, even Yue Yuen Industrial, one of the largest athletic shoe manufacturers globally, has a PE of around 10 times and similarly boasts a dividend yield of over 10%.

In the US stock market, some traditional consumer companies have P/E ratios of 20-30 times. However, in the Hong Kong stock market, there are far too many companies with single-digit PEs, dividend yields above 10%, and even those trading below net asset value. This phenomenon extends even into internet companies, where firms like Weibo and Zhihu trade below their net asset values.

For many, this represents an era of opportunity.

Take Buffett for example. In the 1950s, Buffett earned his first fortune using the 'cigar butt' strategy. He bought companies in bulk whose market values had fallen below their book assets, then profited from dividends, achieving a terrifying annualized return of over 50%.

However, the success of this strategy was rooted in the context of the times — the shadow of WWII brought two decades of prolonged stagnation in global stock markets. From the perspective of picking up cigar butts, the stock market at that time was filled with golden opportunities.

The current state of Hong Kong stocks seems to resemble that period. Beneath these 'stones,' there may be value traps or perhaps excess returns waiting to be uncovered.

Cover image source | AI-generated graphic

Author | Yang Zhichao

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (4)

to post a comment

8

15