Taiwan Semiconductor's strong earnings ignite the US semiconductor sector!

Taiwan Semiconductor's explosive earnings have been released. To what extent did they exceed expectations? What investment clues are implied?

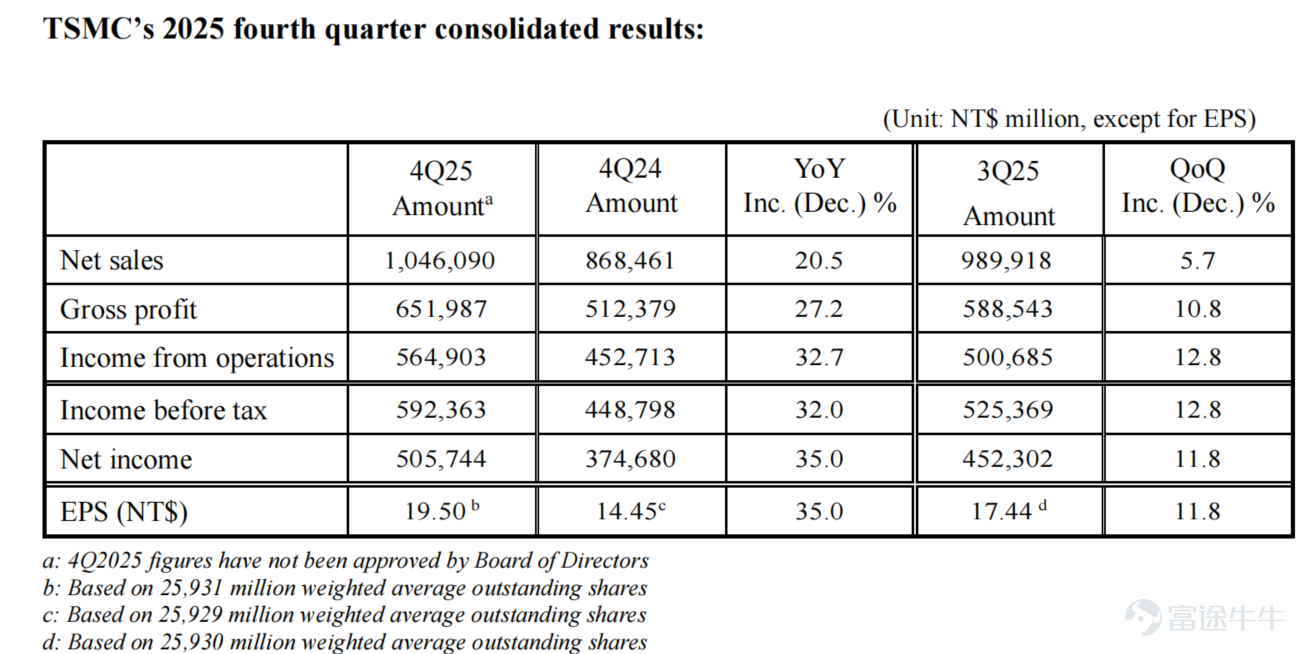

The market has been eagerly awaiting Taiwan Semiconductor's latest earnings report, released today. The Q4 2025 results not only exceeded market consensus on both revenue and net profit but also sent a more crucial signal regarding the company’s future strategy:Capital expenditure budget for 2026 is expected to surge to $52-56 billion, with the revenue share from advanced process nodes anticipated to increase further. Meanwhile, a gross margin exceeding 62% demonstrates that the company maintains strong cost control and pricing power despite its overseas capacity expansion.

$Taiwan Semiconductor (TSM.US)$ Earnings Breakdown: Not Just Exceeding Expectations, but High-Quality Growth

Market concerns over the peaking of the semiconductor cycle have been alleviated by Taiwan Semiconductor’s robust financial data. The key highlight this quarter lies in the margin elasticity driven by sustained high utilization rates.

◦ Revenue Side: Quarterly consolidated revenue reached $33.73 billion, representing a year-over-year growth of 20.5%. This figure exceeded the upper limit of the company's previous guidance, indicating that Q4 wafer shipments were not significantly affected by the seasonal slowdown in consumer electronics.

◦ Profit Side: Net profit amounted to $16.3 billion, growing 41% year-over-year, with net margin reaching 48.3%。

◦ Key Metrics: This quarter's gross margin came in at 62.3%, significantly higher than the previously guided range of 59%-61%. This indicates smooth yield ramp-up for the 3nm node, while high capacity utilization effectively diluted depreciation costs.

– Core financial data:

◦ Taiwan Semiconductor forecasts Q1 2026 revenue to be between $34.6 billion and $35.8 billion, surpassing the previous market expectation of $33.22 billion

◦ Gross margin guidance has been further raised to 63%–65%,Providing such a strong profit margin guidance during the usual industry off-season implies that the visibility of orders from key customers remains extremely high, and the supply-demand relationship for advanced processes continues to be tight.

– Guidance hints at a strong off-season:

Industrial logic behind capital expenditure guidance

Compared to the current quarter's performance, the market pays more attention to forward-looking information revealed during the earnings call. Among these, changes in capital expenditure are the most important leading indicator for assessing the semiconductor industry’s health.

CapEx jumps to the $50 billion platform: Management disclosed a 2026 capital expenditure budget of $52-56 billion, significantly higher than 2025 (approximately $41 billion).

This figure far exceeds the market's previous general expectation of $45-50 billion. Of this, 70%-80% will be allocated to advanced process technologies. This not only confirms AI demand but also indicates that Taiwan Semiconductor is ramping up production capacity in advance to address potential capacity shortages in 2027-2028.

Revenue structure undergoes qualitative change:

– 3nm becomes new growth driver: Revenue contribution from 3nm increased from 23% last quarter to 28%。

– HPC (High-Performance Computing) Dominance: Revenue share from the HPC platform remained at 58%, with year-over-year growth of 48%。

This marks thatTaiwan Semiconductor’s revenue structure has completed its transition, shifting from being 'mobile-driven' in the past to now being 'HPC-driven.' As long as the wave of AI data center construction continues, Taiwan Semiconductor's core performance remains solid.

Regarding the current capacity shortage situation,Management acknowledged during the conference call that despite aggressive capacity expansion efforts, supply remains 'still very tight.' This supply-demand dynamic provides a basis for Taiwan Semiconductor to maintain high pricing.

Semiconductor industry chain impact: Investment insights brought by Taiwan Semiconductor

Based on Taiwan Semiconductor’s earnings report and guidance, the investment logic for the semiconductor industry chain can be validated across the following three dimensions:

– Clue A: Certainty of compute chips,Taiwan Semiconductor's high growth guidance directly reflects the intensity of demand from downstream customers. In particular, the rapid increase in the proportion of 3nm chips indirectly confirms the strong inventory momentum for NVIDIA’s Blackwell architecture chips and Apple’s next-generation processors. For investors holding $NVIDIA (NVDA.US)$ Or $Advanced Micro Devices (AMD.US)$ , this is an important 'inspection report'.

◦ $ASML Holding (ASML.US)$: The majority of the capital expenditures for 2026 will be allocated to advanced process technologies, indicating that the procurement demand for EUV (especially High-NA EUV) lithography machines will remain high.

◦ $Applied Materials (AMAT.US)$ / $Lam Research (LRCX.US)$: As transistor structures become more complex (Gate-All-Around), the number of thin-film deposition and etching steps increases, leading to a corresponding rise in equipment demand.

– Clue B: Equipment manufacturers are seeing high order visibility, A surge in capital expenditure is a direct benefit for equipment manufacturers.

– Clue C: Bottlenecks in advanced packaging, Management once again mentioned the tight situation with CoWoS capacity. This means that, apart from Taiwan Semiconductor’s own packaging expansion, overflow orders may continue to flow to $ASE Technology (ASX.US)$ or $Amkor Technology (AMKR.US)$ and other major OSAT companies, while also benefiting related inspection equipment suppliers.

Options strategies can participate in relevant opportunities.

The current Taiwan Semiconductor stock price has already reflected some optimistic expectations. After the earnings report is released, investors can consider using option structures to optimize the risk-reward ratio of their positions.

Strategy One: Bull Call Spread — Capturing neutral-to-bullish returns

– Suitable Scenarios: Positive on the company’s long-term fundamentals, but believe that short-term stock prices may face consolidation due to profit-taking or limited upside due to the macro environment.

– Construction: Buy near-month at-the-money TSM Call, while selling out-of-the-money Calls 10%-15% higher.

– Purpose: Reduce position cost by selling options and lock in profit and loss range.

Strategy Two: Selling Put Spread (Bull Put Spread) — Earning volatility premium

– Suitable Scenarios: Believe that there is strong support for the stock price below, and prefer to earn time value.

– Construction: Sell Puts at the lower support level while buying cheaper Puts for protection.

– Purpose: Profit from the decline in implied volatility (IV) after the earnings report, as long as the stock does not experience a sharp pullback.

Market conditions are complex and volatile,Options strategyOverwhelmed by choices? Futubull helps you build a portfolio in three steps.Options strategy, making investment simple and efficient!

Market conditions are complex and volatile,Options strategyOverwhelmed by choices? Futubull helps you build a portfolio in three steps.Options strategy, making investment simple and efficient!

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

4

7