2026 IPO bonanza! Over 90% of new stocks rose on their debut

Child King A+H Performance Improves: Heavy Burden of 1.9 Billion Goodwill, Persistently High Selling Expenses

Four years after listing on the A-share market, Child King Children's Products Co., Ltd. (hereinafter referred to as Child King, 301078.SZ) has set its sights on the Hong Kong stock market. On December 11 last year, it filed an application for listing on the Main Board of the Hong Kong Stock Exchange, with Huatai International acting as the sole sponsor.

Behind the Hong Kong IPO lies the dwindling population dividend that has increasingly weakened the growth of Child King's core business in maternal and infant consumer goods, along with the heavy burden of 1.9 billion goodwill brought about by strategic attempts at mergers and acquisitions aimed at transforming the company.

Under pressure from its main business, the company's stock price fell oscillatingly from a high of RMB16.17 per share on June 5, 2025, to a low of only RMB9.44 per share. As of January 13, the company’s stock closed at RMB11.32 per share, with a turnover rate of 8.42%.

However, it is worth mentioning that the earnings forecast for the whole year of 2025 provided by the company has raised expectations significantly. The net profit attributable to shareholders is expected to increase by 51.72%-82.06% year-on-year to RMB275 million-RMB330 million, while the net profit after deducting non-recurring gains and losses is expected to rise by 71.12%-108.68% year-on-year to RMB205 million-RMB250 million.

Performance affected by demographic factors; first three quarters showed good performance.

Childking was originally founded as a maternity and baby supplies store in Nanjing by Wang Jianguo in 2009, being the largest one-stop shopping mall for maternal and child products at that time. In 2016, Childking restructured into a joint-stock company and ranked on the 2016 China Chain Store Top 100 list as the only maternal and baby retailer. Also in 2016, the company embarked on its journey to enter the capital market, listing on the NEEQ (National Equities Exchange and Quotations) that year, but later voluntarily delisted in 2018 because the NEEQ could no longer meet its financing needs. In October 2021, Childking officially went public on the ChiNext board.

In terms of equity structure, as of the date of signing the prospectus, Wang Jianguo controls 27.14% of Childking's voting rights through Jiangsu BOSIDA and the acting-in-concert party Nanjing Qianmiao Nuo.

Starting from physical stores, Childking had a total of 3,710 offline sales outlets as of the end of September 2025, including 1,033 self-operated family stores and 174 direct-sale technology hair care stores. According to Frost & Sullivan, Childking ranks first in the Chinese new consumption sector for families based on the cumulative registered membership as of the end of September 2025 and GMV in 2024.

However, given the impact on both the real economy and population growth rates today, is the retail of maternal and child products still a ‘hot commodity’?

The prospectus shows that from 2010 to 2016, the number of newborns in China increased overall and reached about 17.86 million in 2016 following the implementation of the two-child policy. However, as the policy dividend weakened, China’s birth rate started to decline continuously from 2017 to 2023.

According to Frost & Sullivan, the market size of China's new family consumption market rose from RMB4.6 trillion in 2020 to RMB5.23 trillion in 2024, with a compound annual growth rate of only 3.2%.

Childking frankly admitted in its risk factors that the end-users of its maternal and child products are infants aged 0-14 and women. A continuous decline in the birth rate may reduce the potential customer base for maternal and child products and services, thereby limiting the industry's long-term growth prospects.

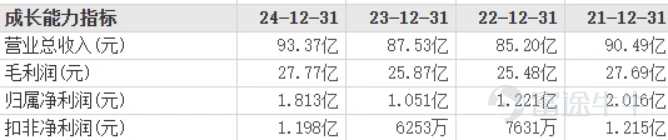

Reflected in the company's performance, both revenue and profit of Child King stagnated relatively in 2023. For the reporting periods from 2022 to September 2025, the company's revenues were RMB 8.52 billion, RMB 8.753 billion, RMB 9.337 billion, and RMB 7.349 billion respectively, while net profits during these periods were RMB 120 million, RMB 120 million, RMB 205 million, and RMB 229 million respectively. In 2023, when the company's revenue grew by only 2.73%, the profit for that year remained relatively stagnant.

In fact, according to the annual reports disclosed by Child King, since 2022 within the reporting period, the company’s profitability has been under continuous pressure. After acquiring Leyou Group, which also engages in maternal and infant product retail, in 2023, the company's performance improved. Specifically, out of Child King's RMB 205 million profit in 2024, Leyou Group contributed RMB 124 million, accounting for 60%.

According to the annual report, in 2022, Child King's net profit attributable to shareholders dropped by 39.44% year-on-year to RMB 122 million, while the non-GAAP net profit attributable to shareholders fell by 37.21% year-on-year to RMB 76.3083 million. In 2023, the company's net profit attributable to shareholders continued to decline by 13.92% to RMB 105 million, with the non-GAAP net profit attributable to shareholders decreasing by 18.06% to RMB 62.5255 million.

In 2024, the company reversed its previous downtrend. Although revenue increased by only 6.68% year-on-year to RMB 9.337 billion, both the net profit attributable to shareholders and the non-GAAP net profit attributable to shareholders achieved double-digit growth. The net profit attributable to shareholders grew by 72.44% year-on-year to RMB 181 million, while the non-GAAP net profit attributable to shareholders surged by 91.6% year-on-year to RMB 120 million.

The company admitted in its prospectus that the growth in 2024 was mainly due to the acquisition of Leyou Group in August 2023, which expanded the company’s business presence in northern China.

In the first three quarters of 2025, Child King's revenue grew by 8.1% year-on-year, while the net profit attributable to shareholders surged by 59.29% year-on-year.

Wind data shows that from 2022 to 2024, the year-on-year growth rates of Child King’s revenue were -5.84%, 2.73%, and 6.68% respectively, while the year-on-year growth rates of net profit attributable to shareholders were -39.44%, -13.92%, and 72.44%. The year-on-year growth rates of the non-GAAP net profit attributable to shareholders were -37.21%, -18.06%, and 91.6% respectively.

Despite the acquisition of Leyou Group, the revenue contribution from the company's maternal, infant, and children business still declined as of the end of September last year, standing at 90%, 90.1%, 90.3%, and 88.3% for each respective period, representing a year-on-year drop of 2.2 percentage points in the first three quarters of 2025.

In terms of gross margin, from 2022 to 2024, the gross margins of the maternal, infant, and children business were 20.8%, 19.9%, and 21.1% respectively, dropping by 1.9% year-on-year to 18.9% in the first three quarters of 2025.

Wind data shows that from 2022 to 2024, the overall gross margins of Child King were 29.91%, 29.56%, and 29.74% respectively. In the first three quarters of 2025, the company’s overall gross margin was 28.61%, a year-on-year decrease of 0.89% compared to the same period last year.

Huaxin Securities' research report points out that the company focuses on maternal and child retail and value-added services, primarily providing one-stop shopping and comprehensive growth services for children aged 0-14 and pregnant women. The franchising business is expected to grow significantly by 2025, with Siyu Industrial being consolidated into its financial statements. The company also plans to initiate an H-share listing to deepen its international strategic layout, with future performance likely to continue its upward trend. According to the Q3 2025 report, the EPS forecast for 2025-2027 has been adjusted to RMB 0.27/0.36/0.44 (previously RMB 0.29/0.40/0.56). The current share price corresponds to PE ratios of 40/30/25 times. The 'Buy' investment rating is maintained.

Heavy burden of 1.9 billion goodwill, ongoing mortgage loans

It is worth mentioning that the acquisition of Leyou Group in 2023 was only the first step towards 'self-rescue' amid pressure on the core business. In 2022, Baby King proposed a 'three-expansion strategy': expanding product categories, expanding business tracks, and expanding business formats, aiming to build a full age-range product category for parent-child families based on user needs, continuously pushing the boundaries of parent-child family consumption.

Under the guidance of the 'three-expansion' strategy, after acquiring Leyou Group in August 2023, the company acquired Xingyan Biotech, which operates cosmetics brands, in January 2025, and then acquired Siyu Group, which engages in scalp and hair care businesses, in July of the same year.

Huaxin Securities noted that by the end of 2024, the company will have fully controlled Leyou International, completing its market layout in northern China; it has initially formed a dual-core business model of 'maternal and child retail + beauty services.' Additionally, the company continues to push for business model innovation, introducing the new Ultra store format, which focuses on visual innovation, scenario recreation, product quality enhancement, service reengineering, and experience upgrades across five dimensions, redefining the boundaries and value connotations of maternal and child consumption. It deeply integrates trendy IPs, rice economy, and AI technology, leading industry value elevation through first-release economics.

Moreover, Siyu Industrial is the leading enterprise in China's hair care and maintenance sub-sector, showing strong synergies with the company in member operations, market layout, channel sharing, industrial collaboration, and business expansion. As of the end of 2024, Siyu Industrial had 2,503 stores and over 2 million members. The acquisition is expected to directly boost the company’s second-half performance and strengthen its leading position in local lifestyle and new family service sectors.

It is important to note that the equity stakes in Leyou Group, Xingyan Biotech, and Siyu Group acquired by Baby King are currently under mortgage.

The prospectus shows that in 2023, 2024, and January-September 2025, the company took loans from banks amounting to RMB 583 million, RMB 501 million, and RMB 460 million, respectively, using 65% of Leyou Group's equity as collateral. In September 2025, the company continued to mortgage 35% of Leyou Group's equity to secure a bank loan of RMB 291 million, pledged 100% of Siyu Biotech's equity for a bank loan of RMB 990 million, and used 60% of Xingyan Biotech's equity as collateral for a bank loan of RMB 91.2 million.

Based on disclosed data, Baby King recorded goodwill of RMB 782 million in both 2023 and 2024. By the end of September 2025, the company's goodwill had reached RMB 1.931 billion. Meanwhile, interest-bearing bank and other borrowings surged from RMB 423 million in 2022, reaching RMB 1.059 billion in 2023, RMB 989 million in 2024, and RMB 2.574 billion as of October 2025.

Among these figures, the proportion of secured bank loans in Baby King’s total interest-bearing bank and other borrowings from 2022 to October 2025 were 100%, 86.2%, 88.4%, and 91.4%, respectively, with interest rates ranging between 2.65% and 4.55%.

Under large-scale loan acquisitions, the cash flow from financing activities of Child King has been under pressure for years. The figures for 2022-2024 were -RMB 207 million, -RMB 276 million, and -RMB 129 million, respectively, and as of July 4, 2025, it was -RMB 25.423 million. The company stated in its prospectus that the outflow of cash flow from financing activities was mainly due to the repayment of interest-bearing bank loans and other borrowings.

Child King’s debt repayment pressure is also reflected in its liability indicators. In each period, the company's asset-liability ratios were 62.3%, 65.7%, 56.8%, and 64.3%, the current ratios were 1.6, 1.8, 1.5, and 1.4, and the quick ratios were 1.2, 1.4, 1.2, and 1.1, respectively.

Selling expenses close to RMB 7 billion, membership GMV declines

With the rise of online shopping in recent years, Child King has also established an operational model that integrates online and offline operations. Through multiple sales and service channels such as same-city instant retail, the Child King app, WeChat mini-programs, etc., they aim to meet user needs more accurately anytime and anywhere. Meanwhile, new customers are continuously acquired through public platforms like Douyin, Xiaohongshu, and other streaming media video accounts. Specifically, Child King no longer uses physical stores merely as places to sell products but instead transforms them into experience centers for goods and services for families with children, as well as social interaction communities.

According to the prospectus, Child King has independently developed a leading digital platform in the field of family services, achieving full-process digitization and establishing over 1,500 user tags and more than 700 intelligent models. They have also independently developed the first large model, 'KidsGPT Smart Advisor,' and created several AI agents including AI parenting and AI technical operations. According to Frost & Sullivan, in 2024, based on the scale of digital investments and the size of the digital team, Child King ranks as the company with the largest digital investment in China's new consumption industry for families with children.

However, despite significant investments in digital operations, its monetization capabilities still seem to need further improvement. The prospectus shows that since its establishment, Child King has implemented a membership system. As of the end of September 2025, the number of registered members exceeded 97 million. Based on 2024 GMV and the cumulative number of registered members as of the end of September 2025, Child King ranks first in China's new consumer sector for families with children.

Despite being crowned with the 'No. 1' title, both GMV generated from members and average GMV per consumer have declined for Child King.

In each reporting period, GMV from Child King’s members amounted to RMB 12.766 billion, RMB 12.062 billion, RMB 12.403 billion, and RMB 8.717 billion, respectively. This figure dropped by 5.51% year-on-year in 2023 and failed to recover to the 2022 level by 2024.

Meanwhile, the average GMV per consumer also showed a significant decline across each period, at RMB 1,135.3, RMB 955, RMB 1,000.9, and RMB 893.3, respectively, with a drop of 15.88% in 2023.

It is worth noting that, despite the company's efforts in expanding its online presence in recent years, the revenue share from online sales still needs improvement. In each period, revenue from offline sales accounted for 50%, 56.5%, 54.1%, and 58.4%, while revenue from online instant retail accounted for 50%, 43.5%, 45.9%, and 41.6%, respectively.

On the other hand, the company's sales and distribution expenses during this period have remained considerably high, with each period reaching 1.815 billion yuan, 1.812 billion yuan, 1.887 billion yuan, and 1.401 billion yuan respectively, accumulating to over 6.9 billion yuan over three years and nine months. In contrast, R&D expenditures were only 88.314 million yuan, 51.265 million yuan, 39.831 million yuan, and 28.208 million yuan for the same period.

Regarding the pressures and challenges faced by traditional brick-and-mortar business models transitioning to online instant retail, Song Xiangqing, Vice President of the China Business Economics Association, pointed out that shifting from offline distribution to online retail presents significant operational and management challenges. Issues such as data and system integration, the separation of data between online and offline channels, and difficulties in forming a complete user profile and sales analysis cannot be ignored. Substantial resources are required to build a unified digital platform for integrating omnichannel data, necessitating continuous technological investment.

Huo Hongyi, a well-known business consultant and corporate strategy expert, believes that for companies starting with traditional physical stores, their advantage may still lie in offline distribution. Establishing an integrated online and offline sales model will inevitably bring cost pressures. The costs associated with the offline model mainly focus on distributors, warehousing, and logistics, while online retail must bear a series of new costs such as platform commissions, traffic acquisition, content creation, online customer service, and fulfillment delivery. This poses significant challenges to a company’s digital management capabilities and operating costs.

According to Tianyancha, as of January 14, Child King has been involved in 350 legal cases, 42% of which were trademark infringement disputes. In 2013, 2014, and 2023, the company was listed as an enforcement target four times, with the total enforcement amount reaching 3.2802 million yuan. (Produced by Harbor Finance)

Chen Qian, 'Harbor Commercial Observer'

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment