Major Wall Street banks take the lead! Q4 earnings season for US stocks kicks off

The financial sector showed strong performance in the first week of 2026, with US bank giants hitting new highs! How to position options before earnings reports?

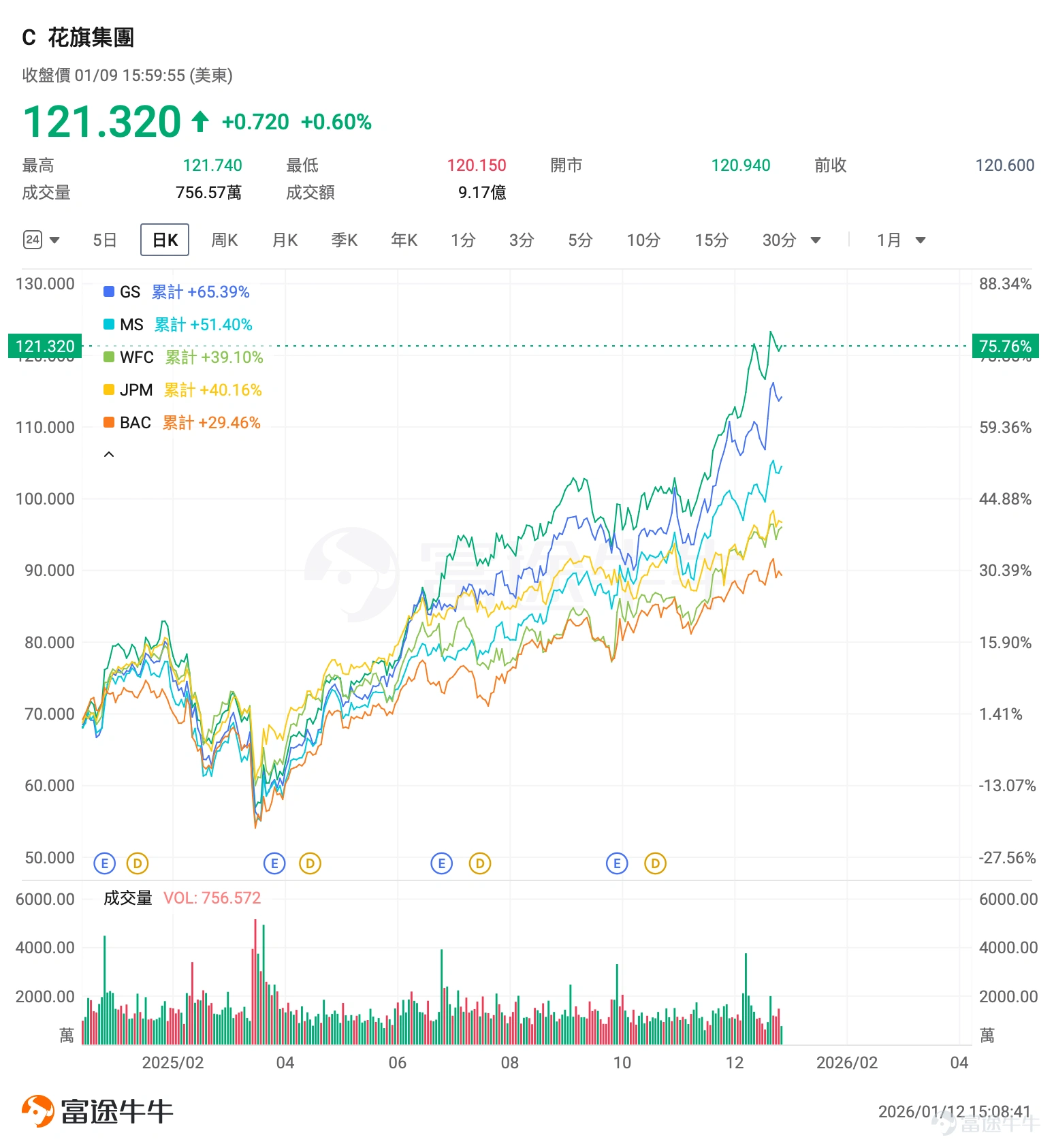

At the start of 2026 in the US stock market, giant US banks have all reached new highs,$JPMorgan (JPM.US)$ 、 $Bank of America (BAC.US)$ 、 $Wells Fargo & Co (WFC.US)$ 、 $Morgan Stanley (MS.US)$ 、 $Goldman Sachs (GS.US)$ 、 $Citigroup (C.US)$All reached new highs.

$KBW Nasdaq Bank Index (.BKX.US)$Up about 33% since the beginning of 2025, far outpacing the broader market.

Against the backdrop of slowing global growth and increasing uncertainty, bank stocks are regarded as 'assets of certainty' due to their stable profitability and sustainable dividends, leading to a reassessment of their value. The unique business models and shareholder return mechanisms of US bank stocks make them offer both high returns and growth potential.

This article will analyze the drivers behind the surge in major US bank stocks, combined with a preview of the upcoming Q4 2025 earnings report this week, to explore pre-earnings options trading strategies to help investors seize opportunities.

The surge in major US bank stocks: A combined result of macroeconomic environment, policy support, and internal industry transformation.

Among the major Wall Street banks, $Goldman Sachs (GS.US)$ the stock price has surged by approximately 65% since the beginning of 2025, $Citigroup (C.US)$ with a cumulative increase of about 76%, $Bank of America (BAC.US)$ up 30%, $JPMorgan (JPM.US)$ up 40%, $Wells Fargo & Co (WFC.US)$ up 39%, $Morgan Stanley (MS.US)$ up 51%.

Macroeconomic Environment and Monetary Policy: Stable Growth and Rate Cut Benefits Support Industry Fundamentals

The US economy demonstrated strong momentum in Q3 2025, with GDP growth reaching 4.3%, significantly surpassing market expectations.Although Q4 may be affected by short-term factors, thanks to implemented tax cuts and the artificial intelligence (AI) investment boom, most institutions predict that economic growth will stabilize within the 2.0%-2.5% range in 2026. A Morningstar report highlighted that this overall stable macro environment provides solid support for banking sector performance.

Meanwhile, the shift in the Federal Reserve's monetary policy has become a key driver.The Federal Reserve cut interest rates three times in the last four months of 2025, with a cumulative reduction of 75 basis points, lowering the benchmark rate to a range of 3.5%—3.75%. The rate cuts directly reduced banks' cost of liabilities and stimulated corporate financing and M&A activities, significantly benefiting investment banking revenues from bond underwriting and M&A advisory services.

Although rate cuts may compress some net interest margins, banks can achieve effective hedging through revaluation gains on assets such as real estate and private equity held on the asset side. The market widely expects further room for rate cuts in the first half of 2026, prompting capital to flow from the bond market into high-dividend bank stocks, further boosting sector valuations.

Regulatory Easing and Business Recovery: Unlocking Capital Vitality and Driving Diversified Growth

A more relaxed regulatory environment is currently the most direct industry catalyst.The 'bank-friendly' policies promoted by the Trump administration aim to reduce capital requirements for large banks. According to Jefferies, this move could release approximately $2.6 trillion in additional lending capacity for the U.S. banking sector; Goldman Sachs estimates it will bring $180 billion to $200 billion in extra capital. Regulatory easing not only enhances banks' ability to lend and expand but also strengthens their valuation advantage.

At the business level, a diversified model has become the core of profitability resilience.Leading banks like Goldman Sachs and Morgan Stanley have higher proportions of non-interest income, effectively hedging against credit cycle fluctuations. In 2025, the global M&A market saw a strong recovery, with total transaction value surging to $4.5 trillion, nearly a 50% year-on-year increase, setting the second-highest historical record, which directly boosted investment banking revenues. Meanwhile, large-scale financing by companies competing for AI infrastructure has further increased loan demand and capital markets revenue for banks.

2026: Yield Curve, Capital Markets, and Ongoing Regulatory Benefits to Drive Bank Stocks

Looking ahead to 2026, the performance of bank stocks is expected to be driven by the following major factors:

The 'bull steepener' yield curve lays a foundation for profitability.Recently, the U.S. Treasury market has shown a 'bull steepener' trend characterized by rapidly declining short-term interest rates and relatively stable long-term interest rates. This is particularly beneficial to bank profitability because banks typically finance through short-term liabilities while deploying assets in the form of long-term loans. An improved interest margin environment will directly solidify their net interest income base.

Mergers and acquisitions and the IPO wave continue.Goldman Sachs and other institutions predict that the fundamental drivers of M&A activity in 2026—such as capital abundance, recovery of the IPO market, and corporate strategic restructuring intentions—will remain strong. Market expectations suggest that several tech giants, including OpenAI and SpaceX, may launch IPOs, bringing investment banks hundreds of millions in advisory and underwriting fees. PwC also noted that if the macro environment remains stable, 2026 could become the 'best IPO window in years.'

Bank regulation is expected to continue easing.Vice Chair of the Federal Reserve, Bowman, outlined key directions for U.S. bank regulation during her testimony at a Senate Banking Committee oversight hearing on December 2, 2025. These include potentially lowering implied capital requirements in stress tests, reducing the additional capital burden for Global Systemically Important Banks (GSIBs), and implementing Basel III 'final rules' more leniently.

Moreover, regulatory clarity in areas such as cryptocurrencies may open up new business growth opportunities for banks.

Earnings Preview: Major U.S. banks’ Q4 2025 results set for dense release next week.

This week,$Goldman Sachs (GS.US)$ 、 $Bank of America (BAC.US)$ 、 $Citigroup (C.US)$ 、 $JPMorgan (JPM.US)$ 、 $Morgan Stanley (MS.US)$ and $Wells Fargo & Co (WFC.US)$This week, will sequentially release their Q4 2025 earnings reports, becoming a crucial test point for assessing the sustainability of recent gains.

JPMorgan will be the first to release its earnings report on January 13, followed by Bank of America, Wells Fargo & Co, and Citigroup on January 14. Goldman Sachs and Morgan Stanley will announce their results on January 15.

After the earnings reports are released, investors can focus on the following key metrics:

– Net Interest Income (NII):This is the core profit driver for traditional retail banks. Previously, in Q3 2025, JPMorgan, Wells Fargo, and Citi all exceeded expectations for net interest income (NII). After the Federal Reserve continued to cut rates in Q4, it is important to monitor the actual impact of changes in the interest rate environment on their net interest margins and loan demand.

– Credit Quality:Pay attention to changes in non-performing loan ratios and credit loss provisions, which directly reflect economic expectations and the banks' risk control capabilities. In Q4, affected by the government shutdown, the economic slowdown may lead to a decline in bank loan balances and slightly worsening write-offs. The ongoing K-shaped recovery in the U.S. economy could also result in rising credit card delinquency rates and increased bad debt write-downs.

– Capital Position and Returns:Monitor regulatory capital adequacy ratios and updates on shareholder return programs, such as dividends and stock buybacks, which affect the stability of the bank and its attractiveness to investors.

– Investment Banking Revenue:Includes fee income from M&A advisory, equity and bond underwriting, which directly reflects the activity level of capital markets.

– Trading Revenue:Focus on its performance in areas such as fixed income, foreign exchange, and commodities, which is closely related to market volatility.

Key focus areas for each bank

– JPMorgan: Market attention on the sustainability of investment banking and trading businesses

$JPMorgan (JPM.US)$Will release earnings report pre-market on January 13 Eastern Time,Institutional forecasts expect JPMorgan to achieve revenue of $46.245 billion in Q4 2025, an increase of 8.13% year-over-year; expected earnings per share of $5.004, an increase of 4.03% year-over-year.

JPMorgan’s Q3 revenue and profits exceeded expectations, mainly due to a 16% surge in investment banking income and record trading business performance. JPMorgan ranked first in global investment banking fees and, driven by the recovery in ECM and M&A activities, has reconsolidated its position as the leading global investment bank with an 8.7% market share, surpassing peers.

However, this recovery relies more on improvements in market conditions. Amid challenges posed by complex geopolitical conditions, investors will focus on whether the rebound in the company's investment banking business is sustainable. The record trading business income was due to high market volatility in Q3, and whether this performance can be sustained in the Q4 capital market environment remains to be seen.

– Bank of America: Market attention on whether consulting income can continue to soar in Q4

$Bank of America (BAC.US)$Will release earnings report pre-market on January 14 Eastern Time,Institutional forecasts expect Bank of America to achieve revenue of $27.625 billion in Q4 2025, an increase of 8.99% year-over-year; expected earnings per share of $0.96, an increase of 16.71% year-over-year.

As the second-largest bank in the United States, Bank of America saw robust Q3 earnings growth driven by record performance in investment banking and wealth management businesses, alongside better-than-expected loan loss figures. Net profit rose to $7.7 billion, a year-on-year increase of 58%. Bank of America has profited significantly from the booming M&A market in 2025, with advisory revenues surging; investors will focus on whether this revenue momentum continues into Q4.

– Wells Fargo & Co: Market focuses on the aftermath of the asset cap removal

$Wells Fargo & Co (WFC.US)$Earnings report scheduled for release pre-market on January 14 Eastern Time.Institutional forecasts predict Wells Fargo & Co’s Q4 2025 revenue at $21.681 billion, up 6.39% year-over-year, with expected earnings per share of $1.667, an increase of 16.57% year-over-year.

Goldman Sachs and other banks' Q3 2025 earnings surprises were mainly due to strong investment banking performance, which is not a core business for Wells Fargo & Co. The better-than-expected Q3 results for Wells Fargo were primarily driven by growth in consumer business and a reduction in credit loss provisions. Additionally, Wells Fargo has been constrained by an 'asset cap' for the past seven years, as punishment for the fake accounts scandal and various issues under previous leadership.

The Federal Reserve lifted the asset cap in June 2025, allowing Wells Fargo & Co to seize the opportunity, with total assets surpassing the $2 trillion mark for the first time in Q3 2025. Investors will closely watch whether Wells Fargo further expands post-cap removal in Q4 and achieves long-term operational efficiency improvements.

– Citigroup: Market focuses on the effectiveness of the company's business transformation

$Citigroup (C.US)$Earnings report scheduled for release pre-market on January 14.Institutional forecasts predict Citigroup's Q4 2025 revenue at $20.516 billion, up 4.77% year-over-year, with expected earnings per share of $1.396, an increase of 4.19% year-over-year.

Citigroup's Q3 saw strong performance across all five business segments—services, markets, banking, wealth management, and U.S. personal banking—all setting new Q3 revenue records. This reflects that Citi’s recent business restructuring and digital transformation investments are beginning to pay off, with investment banking fee income growing 17%, benefiting from the ongoing recovery in M&A activity.

Since Fraser took office, Citi has continued to implement a business focus strategy, which involves exiting retail banking operations in low-margin or non-core regions and concentrating on business segments with competitive advantages such as institutional services and wealth management. In Q4, investors will focus on the further results of Citi's business transformation. This strategic shift led to an increase in expenses in Q4. Additionally, due to the impact of California wildfires in Q3, Citi's credit quality came under pressure, and the market will be watching for any growth in non-performing loans in Q4.

– Goldman Sachs: The market is focused on whether the company’s strategic transformation effectiveness and regulatory risks have improved.

$Goldman Sachs (GS.US)$The earnings report will be released pre-market on January 15.Institutions expect Goldman Sachs to achieve revenue of $14.256 billion in Q4 2025, representing a year-over-year increase of 2.79%; expected earnings per share are $11.566, reflecting a year-over-year decrease of 3.21%.

Goldman Sachs’ Q3 revenue hit a record high for the same period, driven by a wave of mergers and acquisitions, with investment banking revenue surging 42%, significantly surpassing market expectations. Total assets under management rose to $3.45 trillion. Although investment banking revenue soared in Q3, its sustainability in Q4 remains uncertain. The market will continue to monitor changes in the backlog of investment banking deals and the impact of the market environment.

After undergoing strategic realignment from 2022 to 2024, Goldman Sachs has exited the mass retail banking business 'Marcus' and refocused on Global Banking & Markets (GBM) and Asset & Wealth Management (AWM). The market will be paying attention to the effectiveness of this strategic transformation, particularly progress in asset and wealth management as well as developments in emerging businesses related to digital assets/blockchain.

Furthermore, Goldman Sachs’ litigation and regulatory reserves reached $131 million in Q3, a significant increase from $41 million in the same period last year. Regulatory risks remain, and investors will be watching to see if these risks improve in Q4.

– Morgan Stanley: The market is focused on whether the company can leverage regulatory tailwinds to deliver better-than-expected earnings.

$Morgan Stanley (MS.US)$The earnings report will be released pre-market on January 15.Institutions expect Morgan Stanley to achieve revenue of $17.681 billion in Q4 2025, representing a year-over-year increase of 8.99%; expected earnings per share are $2.442, reflecting a year-over-year increase of 10.0%.

Morgan Stanley's Q3 results beat expectations across the board, with equity trading revenue surging 35%. Additionally, driven by active IPOs and convertible bond issuance, investment banking revenue grew over 44% year-over-year. As part of the growth in investment banking relied on the backlog of projects from the first half being executed, investors will focus on the execution of new projects in Q4.

Morgan Stanley's wealth management segment continued its strong performance in Q3. By the end of Q3, total client assets under wealth management and investment management reached $8.9 trillion. Benefiting from economies of scale, asset management fee income increased by 12% year-over-year. Investors will closely watch whether wealth management can continue to act as a stabilizer for growth in Q4. Furthermore, regulatory-wise, the Federal Reserve has agreed to reduce Morgan Stanley’s stress capital buffer (SCB) from 5.1% to 4.3%, potentially enabling the company to deliver an above-expectations earnings report in Q4 due to this regulatory relief.

Options strategy setup before earnings

For options traders, earnings season often brings volatility spikes. So far, the implied volatility (IV) of US stock options for the aforementioned six major banks has risen to high levels. For instance, IV percentiles for Morgan Stanley, Citi, and others are above 70%, making selling options more favorable.

Moreover, since the majority of banks’ Q3 outperformance was mainly due to spikes in investment banking and trading businesses, sustainability of these businesses in Q4 remains questionable. Therefore, a conservative bullish strategy is recommended.

1. Covered Call (holding bank stocks + selling puts)

– Operation:Holding the underlying stock + selling call options on the bank stock.

– Purpose:By selling call options, you collect premium as an 'extra dividend' for holding shares. If the share price is below the strike price at expiration, the option expires worthless, and you keep the premium. If the share price is above the strike price, your stock may be called away at the strike price, but you still benefit from the premium and gains up to the strike price.

– Risks and suitable investors:Sacrifice potential upside from significant price increases in exchange for limited downside protection provided by the premium. Suitable for investors who are neutral or mildly bullish on the market outlook.

2. Short Iron Condor: Selling the Iron Condor options strategy

The Iron Condor options strategy is suitable for more advanced options investors. For neutral-to-bullish expectations during earnings season, the goal is to profit from the IV crush (decline in volatility post-earnings), hence adopting the sale of an Iron Condor.

– Operation:This involves four options (all with the same expiration date): selling one put option with a lower strike price + buying one put option with an even lower strike price + selling one call option with a higher strike price + buying one call option with an even higher strike price. The distance between these four strike prices is equal, and both sold options are slightly out-of-the-money.

– Profit:When the underlying asset's price at expiration is between the two sold strike prices, all options expire worthless, and the profit equals the initial net premium collected.

– Risk and suitability:In a market with unclear direction, this strategy profits from 'selling volatility' to capture time decay. Compared to naked option selling, risk is limited; however, transaction costs may erode profits due to the involvement of four options contracts. This strategy typically has a higher probability of success but limited profit per trade.

Finally, Options Sir brings a small perk for fellow investors. Welcome to claim it!Beginner's Options Package

This event is exclusive to invited HK users. Click to learn more.Detailed rules of the event >>

Market conditions are complex and volatile,Options strategyOverwhelmed by choices? Futubull helps you build a portfolio in three steps.Options strategy, making investment simple and efficient!

Risk Warning

An option is a contract that grants the holder the right, but not the obligation, to buy or sell an asset at a fixed price on a specific date or at any time before that date. The price of an option is influenced by various factors, including the current price of the underlying asset, the strike price, the time to expiration, andimplied volatility。

implied volatilityreflects the market's expectation of volatility in the option over a future period. It is data derived inversely from the Black-Scholes option pricing model and is generally considered an indicator of market sentiment. When investors anticipate higher volatility, they may be more willing to pay a higher price for options to help hedge risks, thereby leading to a higherimplied volatility。

Traders and investors useimplied volatilityto evaluateoption pricesthe attractiveness, identify potential mispricing, and manage risk exposure.

Disclaimer

This content does not constitute any offer, solicitation, recommendation, opinion, or guarantee regarding securities, financial products, or tools. The risk of loss in trading options can be substantial. In certain circumstances, the losses you incur may exceed the initial margin amount deposited. Even if you set contingent orders, such as “stop-loss” or “limit” orders, they may not prevent losses. Market conditions may render such orders unexecutable. You may be required to deposit additional margin within a short period. If you fail to provide the required amount within the specified time, your open positions may be liquidated. However, you will remain responsible for any shortfall in your account resulting from such liquidation. Therefore, before engaging in trading, you should study and understand options and carefully consider whether such trading is suitable for you based on your financial situation and investment objectives. If you trade options, you should familiarize yourself with the procedures upon option exercise and expiration, as well as your rights and obligations upon option exercise and expiration.

Editor/Doris

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

21

30