2025 "Top 100 Hong Kong Stocks" Selection

In-depth Analysis of the 2026 Robot 'Rush to Hong Kong': A Comprehensive Review of Investment Logic

Entering 2026, a wave of robot company listings is surging in the Hong Kong stock market. From humanoid robot newcomers to professional robot companies specializing in logistics, industry, and home applications, many are rushing to submit listing applications in Hong Kong. This trend raises several questions for investors: How large is the robotics field? How is its industrial chain structured? Faced with numerous 'stories' and 'concepts,' how should investors distinguish truth from fiction to uncover real value?

This article starts by categorizing Hong Kong-listed robot stocks into different tracks, clarifying the differences and strategic positioning logic of core types such as home-use, embodied, and humanoid robots. It then analyzes the competitiveness of Hong Kong-listed companies in key parts of the upstream and downstream supply chains—core components, main body manufacturing, and system integration—and combines industry policies with market size data to dissect sector investment opportunities and potential risks, offering readers a panoramic reference.

Comprehensive Classification of Hong Kong-listed Robot Stocks

The robot sector in Hong Kong stocks has formed a multi-track parallel pattern, where different types of companies differ significantly in technological approaches, commercialization progress, and application scenarios.

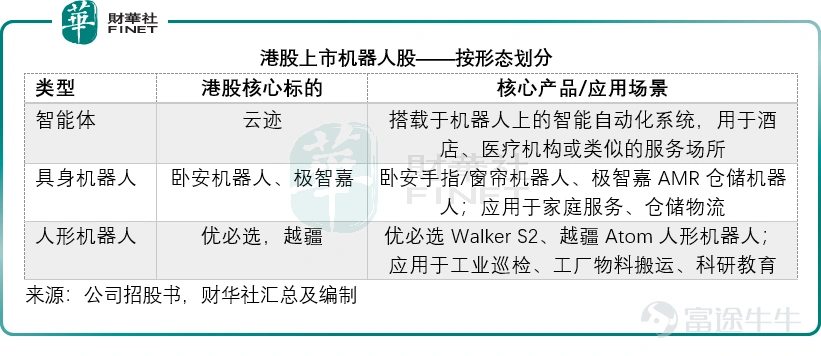

By form, Hong Kong-listed and soon-to-be-listed companies might be divided into three categories: intelligent agents, embodied robots, and humanoid robots.

1) Robotic Service Intelligent Agents: Intelligent automation systems mounted on robots used in hotels, medical institutions, or similar service venues. Integrated with AI technology, they provide human-centric end-to-end services through direct interaction with users. Core Hong Kong-listed companies include Yunji (02670.HK).

2) Embodied Robots: Physical robots that are non-humanoid and focus on precise execution of specific functions, covering subcategories like mobility and manipulation. Core Hong Kong-listed companies include$ONEROBOTICS (06600.HK)$ 、 $GEEKPLUS-W (02590.HK)$ , with flagship products such as Woan Finger/Curtain Robots and Geekplus-W AMR warehouse robots, which can be applied in home services and warehousing logistics.

3) Humanoid Robots: Possessing human-like forms with heads, torsos, and limbs, along with autonomous movement capabilities, they rely on embodied intelligence to interact with their environment. Core Hong Kong-listed companies include $UBTECH ROBOTICS (09880.HK)$ , and Dobot (02432.HK), with key products like Ubtech Robotics Walker S2 and Dobot Atom humanoid robots, applicable in industrial inspection, factory material handling, and scientific research education.

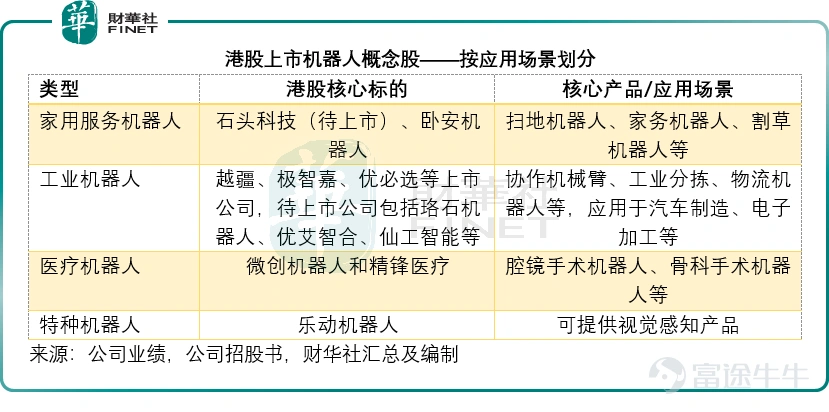

By usage scenario, they may be categorized into several major groups such as home service robots, industrial robots, medical robots, and special-purpose robots.

1) Home service robots: These consumer-grade robots primarily target household consumption scenarios, addressing essential needs such as cleaning, companionship, and housework. Due to substantial demand, these robots have generally achieved mass production and companies have turned profitable. Key representative companies include Anwa Robotics and A-share listed company Roborock (688169.SH), which plans to list in Hong Kong. Its common products include robotic vacuum cleaners, lawn mowing robots, humanoid housekeeping robots (to be released), etc., used for home cleaning and daily companionship.

2) Industrial robots: These are specialized devices serving industrial manufacturing processes, enabling automated production and material handling, including collaborative and mobile subcategories. Representative companies include listed firms such as Geekplus-W, Geeks+, and Ubtech Robotics. Meanwhile, many robot concept companies awaiting listing are also industrial robot makers, including Rockontrol Robotics, Youibot, Seer Intelligence, Canrop Robotics, and Kaleadex Technology. These companies mainly provide collaborative robotic arms and industrial logistics robots that can be applied in automobile manufacturing, electronics processing, and flexible production.

3) Medical robots: Focused on precision medical scenarios, these high-precision devices assist or replace human labor in performing surgical and rehabilitation operations. Representative companies include MicroPort Surgical Robot (02252.HK) and GenFon Medical (02675.HK). They offer laparoscopic surgical robots, orthopedic surgical robots, vascular interventional surgical robots, etc., applicable in surgical procedures and post-operative rehabilitation.

4) Special-purpose robots: These dedicated robots are designed for extreme or specialized environments with capabilities to withstand harsh conditions and perform high-precision tasks. Representative companies include LeDrive Robotics, which has submitted an IPO application but is not yet listed. LeDrive Robotics’ strengths lie in its visual perception products, which mainly supply leading intelligent robot enterprises, while the company itself also offers lawn mowing robots.

Overview of the robotics industry chain in Hong Kong stocks

The robotics industry chain is divided into upstream core components (accounting for 60%-70% of costs, with the highest technical barriers), midstream body manufacturing and system integration (the core segment connecting technology and applications), and downstream application scenarios (key to commercial implementation). Listed companies in Hong Kong stocks have formed a complete industrial chain layout, with key players capable of domestic substitution in critical areas. Below is a detailed breakdown of each segment:

1) Upstream core components: Core components are the 'bottleneck' part of the robotics industry, covering reducers, motors, controllers, sensors, and more, which were long monopolized by foreign enterprises. In recent years, Hong Kong-listed and A+H-listed companies have made continuous breakthroughs in this field, driving down industry costs and laying the foundation for mass production.

ReducerAs a core component of robot joints, represented by harmonic reducers and RV reducers, companies like CRRC Times Electric (03898.HK) and Shanghai Electric (02727.HK), both listed in Hong Kong, have achieved domestic technological breakthroughs, suitable for industrial robot and resilient robot joints.

MotorIn the motor domain, servo motors and hollow cup motors provide core power output for robots. Wolong Electric Drive (600580.SH), which has filed for listing on the Hong Kong Stock Exchange, has mature technology and has become a core supplier to leading robotics companies. Its comprehensive capacity layout should support large-scale production needs within the industry.

ControllerAs the 'brain' of robots, motion controllers and servo systems are key products. Canrop Robotics and Seer Intelligence, among others awaiting listing, are leaders in the localization of industrial robot control systems. They support multi-robot collaborative operations and adapt to flexible manufacturing scenarios. As robots undergo intelligent upgrades, controller complexity continues to increase, with market scale growth outpacing the industry average.

sensorsis the key for robots to achieve environmental perception, with strong demand for categories such as 3D vision, tactile sensors, and inertial sensors. XtalPi Holdings (02228.HK) integrates visual perception, AI, and robotics technologies to solve highly challenging problems in chemical research.Hesai Group (02525.HK)and RoboSense (02498.HK), leading LiDAR companies, are naturally extending from the autonomous driving field into robotic perception systems.

Actuators and JointsIn terms of actuators and joints, Sanhua (02050.HK) has transitioned from automotive thermal management to focus heavily on linear and rotary actuators, being regarded by the market as a core supplier for humanoid robots. Johnson Electric (00179.HK) leverages its precision micro-motor technology to actively participate in the development of joint drive modules. Companies like Zhaowei Electromechanical, which have submitted listing applications, apply satellite transmission system technology to robotic dexterous hands, becoming crucial for fine operations in humanoid robots.

Companies such as Joyson Electronics (00699.HK) and Lens Technology (06613.HK), which will achieve A+H listings by 2025, rely on their manufacturing and R&D capabilities in automotive electronics and precision components to naturally integrate into the robotics supply chain.Industry Synergy。

2) Midstream Body Manufacturing and System Integration: Core Carrier of Commercialization.

The midstream is the core link in the robotics industry, where body manufacturing determines product performance, and system integration achieves precise adaptation of 'robots + scenarios.' Hong Kong-listed companies hold advantages in body manufacturing across multiple tracks including industrial, humanoid, and other forms of robots, while system integration focuses on high-growth scenarios.

Midstream body manufacturing and system integration are the core carriers of robot commercialization, with body manufacturing directly determining product performance, and system integration achieving precise adaptation of 'robots + scenarios.'

In the industrial robot body track, Dobot and Cloos Robotics are core representatives. Dobot’s collaborative robot shipments rank among the top two globally, and it plans to launch a new generation of high-load collaborative robots in 2025. Cloos Robotics’ SCARA robots feature a high localization rate and significant cost-performance advantages.

In the field of mobile robot bodies, Geekplus-W is the world's largest warehouse fulfillment robot supplier, providing solutions for warehouse fulfillment and industrial handling scenarios; Kelix, which has already submitted its listing application, is a comprehensive intelligent in-plant logistics robot provider with three core product lines including Multi-Shuttle Robots (MSR), Autonomous Mobile Robots (AMR), and Conveyor Sorting Robots (CSR). Both companies maintain strong growth momentum.

The humanoid and embodied robot body track is currently a focal point for capital. Ubtech Robotics leads in the commercialization of humanoid robots, targeting delivery of over 500 Walker S2 units by 2025, with a production capacity goal of reaching the ten-thousand-unit level by 2026. Woan Robotics, known as the 'first AI embodied home robotics stock,' boasts a rich product portfolio, receiving over 200 times oversubscription during its IPO, with its share price rising on the first day of trading.

In the system integration track, Standard Robots (awaiting listing) and Youi Robotics (awaiting listing) focus on high-growth scenarios such as flexible manufacturing and warehouse logistics, offering end-to-end service capabilities encompassing 'robots + software + maintenance.' By 2026, manufacturing will become the core battleground for system integration, with leading companies seeing a significant increase in implemented cases and order volumes experiencing rapid growth.

3) Downstream application scenarios: Demand-driven, with ecosystem synergy accelerating penetration.

The release of demand from downstream application scenarios is the core driver of growth in the robotics industry. Currently, industrial manufacturing, healthcare, smart homes, and warehouse logistics have become key growth areas. Hong Kong-listed companies achieve a positive cycle of 'technology-scenario-performance' through collaboration with leading downstream enterprises.

The release of demand from downstream application scenarios is the core driver of growth in the robotics industry, with four major growth areas now established: industrial manufacturing, healthcare, smart homes, and warehouse logistics. Hong Kong-listed companies achieve a positive cycle of 'technology-scenario-performance' through synergy with leading downstream enterprises.

In industrial manufacturing scenarios, Zoomlion Heavy Industry (01157.HK) and Zhengzhou Coal Mining Machinery Group (00564.HK) are actively promoting the integration of industrial robots in the construction machinery sector, accelerating production automation upgrades through collaboration with robot body enterprises. CATL (03750.HK), a leader in the new energy sector, also utilizes robots extensively for battery sorting operations.

In healthcare scenarios, MicroPort Surgical Robot holds the top domestic market share in laparoscopic surgical robots, with an increasing number of clinical implementation cases. Fosun Pharma (02196.HK) focuses on rehabilitation robots, driving the intelligent transformation of medical services.

In smart home scenarios, Haier Smart Home (06690.HK) and Midea Group (00300.HK) promote deep integration of home robots with the smart home ecosystem, launching integrated smart devices for sweeping and mopping. Driven by consumption upgrades, the home service robot market continues to expand.

In warehouse logistics scenarios, Sinotrans (0598.HK) and SF Holding (6936.HK) apply AMR robots at scale in warehousing sorting and material handling processes, effectively improving logistics efficiency while reducing labor costs. Benefiting from the rapid development of e-commerce and express delivery industries, demand for warehouse logistics automation remains strong, with robot penetration rates continuing to rise.

Capital-Driven Growth and Commercial Realities: Hidden Concerns and Divergence Beneath the Boom

The clustering of robotics companies on the Hong Kong stock market is the result of a synergy between industrial logic and capital market rules, but the commercialization challenges behind the prosperity must also be heeded.

Why are robotics companies choosing to go public in Hong Kong? We believe there may be three reasons: an inclusive listing system, an efficient refinancing mechanism, and considerations regarding internationalization and valuation.

Chapter 18C of the Hong Kong Stock Exchange allows unprofitable specialized technology companies to list, providing critical financing channels for robotics firms that are still in high R&D phases and have yet to turn a profit.

At the same time, the flexible placement mechanisms of Hong Kong stocks make post-listing refinancing more convenient. For example, both Ubtech Robotics and Dobot have frequently conducted follow-on financings after their listings to support their large-scale technological R&D expenditures.

Hong Kong stocks serve as an important window for global capital allocation in China’s high-tech assets, helping listed companies enhance their international brand image and attract long-term investment funds.

However, with the increasing number of robotics companies going public, investors will become more selective when picking these firms. Therefore, 2026 is also seen as the year of the 'commercialization test' for robotics concept stocks.

We have noticed that whether it’s already-listed leaders like Ubtech Robotics and Dobot or upcoming IPO candidates like Galaxis Technology and Ledo Dynamics, all are operating at a net loss, with significant R&D investments and relatively small revenue scales being the main causes of losses.

In cutting-edge fields like robotics, there is still a long way to go from lab prototypes to stable, low-cost mass-producible products and then to scaled delivery. Only by achieving scaled delivery can early-stage capital investments be amortized, which holds the key to reducing costs, improving efficiency, and ultimately turning a profit.

However, whether it's industrial robots, logistics robots, or consumer robots in relatively mature markets, they face fierce competition. This is evident from the numerous robotics companies filing for IPOs, not to mention countless startups waiting for capital attention. Additionally, price wars initiated by various companies could accelerate the survival of the fittest among robotics enterprises.

Investment Logic and Future Outlook: Choices in an Era of Differentiation

In such an environment, how should one establish a rational investment logic?

We believe the following evaluation dimensions need to be considered:

1) Technological Moat: The proportion of self-developed key core components (e.g., chips, algorithms, etc.), professional barriers, and supply chain advantages.

2) Application Scenarios and Cash Flow: Prioritize evaluating leaders in niche markets that have established viable commercial models and are already generating stable orders and cash flow.

3) Commercial Progress: Closely track the implementation of mass production orders, customer validation feedback, and cost reduction curves, which are critical in determining whether a company can ultimately achieve economies of scale.

At the same time, beware of the following risks:

1) Some listed companies' valuations include extremely high expectations; if mass production progress or order volumes fall short of expectations, or competition intensifies, they may face significant valuation corrections.

2) Capital will not favor all robotics concept stocks indiscriminately; companies lacking core technology and with unclear commercial models will eventually be eliminated.

3) High-end chips and precision components are dependent on foreign sources, and supply chain security could threaten order fulfillment, which also requires vigilance.

In summary, for investors, the opportunity does not lie in chasing every robotics concept, but in precisely identifying those 'pragmatists' who possess irreplaceable technological barriers and have built sustainable business models in real-world scenarios. In the next 1-2 years, as mass production orders are delivered and financial reports are disclosed, the sector will inevitably undergo a profound value reevaluation and pattern differentiation. After the dust settles, the true trendsetters will emerge.

By Mao Ting

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

9

2