2026 IPO bonanza! Over 90% of new stocks rose on their debut

Fullhan Micro IPO: Diversified Breakthrough and Global Expansion

In 2025, China's domestic semiconductor industry will spark a wave of dual-capital platform listings on 'A+H' markets. In this capital layout trend, companies adopting the dual-platform strategy span core sub-sectors such as chip design, manufacturing, equipment, storage, and optical modules, reflecting a collaborative industrial development pattern of 'multi-point blossoming'.

Behind this trend lies a triple resonance of industrial recovery, capital recognition, and enterprise development needs.

First, the global integrated circuit market is accelerating its recovery driven by emerging demand. In 2024, the market size reached $626.8 billion, a year-on-year increase of 19%, marking the industry's official entry into a new growth cycle. This provides Chinese semiconductor companies with vast external space to expand globally.

Second, global capital markets’ favor towards Chinese tech stocks continues to rise. Wu Zhuoren, Senior Economist at Natixis, stated directly that companies view the Hong Kong market as 'a key step to expand the investor base and broaden R&D financing channels.' The current high valuation of Hong Kong-listed tech stocks has become a 'good prerequisite' for subsequent overseas expansion.

Third, the semiconductor industry's characteristics of 'high R&D investment and long-cycle returns,' coupled with the deepening of global competition, make it urgent for companies to widen their financing channels and pool global resources through dual-capital platforms, injecting sustained momentum into technological iteration and market expansion.

Take Fullhan Microelectronics as an example. Its prospectus explicitly mentions that this Hong Kong fundraising will be specifically used for the construction of marketing and R&D centers in Southeast Asia, Europe, and other regions. Through in-depth localized operations, it will solidify the foundation for global market expansion and help the company seize opportunities amid globalization trends.

01.

Weak Security Cycle: Recovery Opportunities Amid Performance Fluctuations

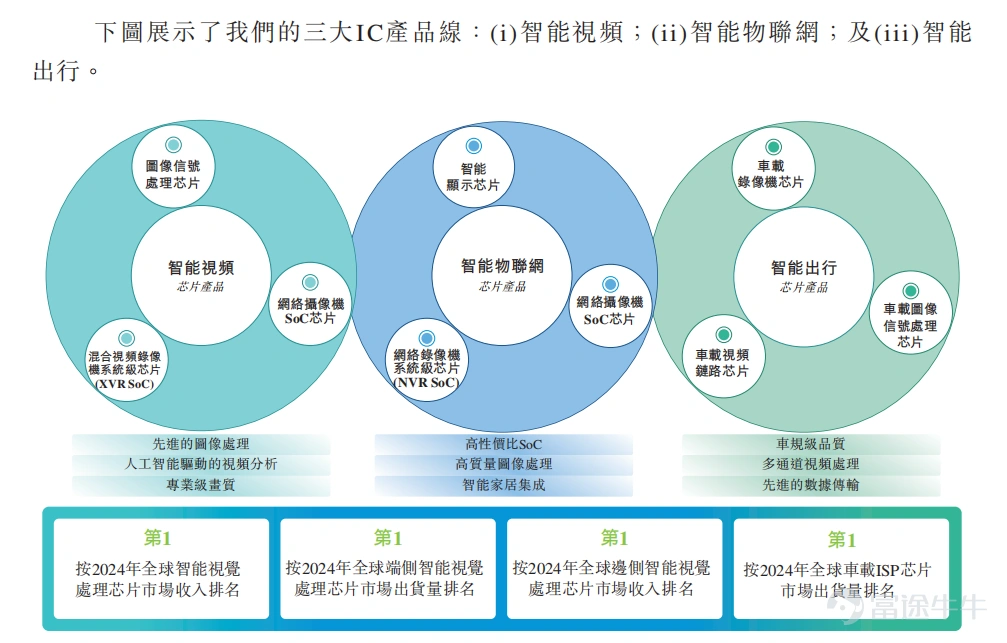

As a leading fabless chip design company in China, Fullhan Microelectronics has long been committed to the research, development, and innovation of intelligent vision technology. With its profound technological expertise, in 2024, the company achieved four global firsts: top revenue in the intelligent vision processing chip market, highest shipment volume and revenue for edge-side and end-side intelligent vision processing chips, and top shipment volume in automotive ISP chips.

Source: Fuhangwei Prospectus

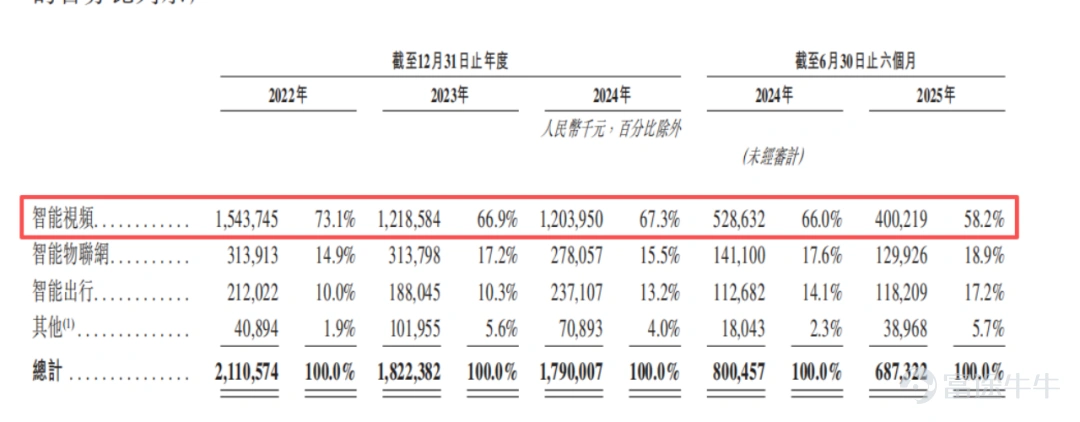

The company’s three major IC product lines cover intelligent video, intelligent IoT, and intelligent mobility sectors. Among these, intelligent video business serves as Fullhan Microelectronics’ “revenue anchor,” widely applied in core security scenarios such as network cameras and video conferencing cameras. From 2022 to 2024, revenue contribution from this segment remained consistently above 65%, providing robust support for stable operations.

Source of the image: Fuhangwei prospectus

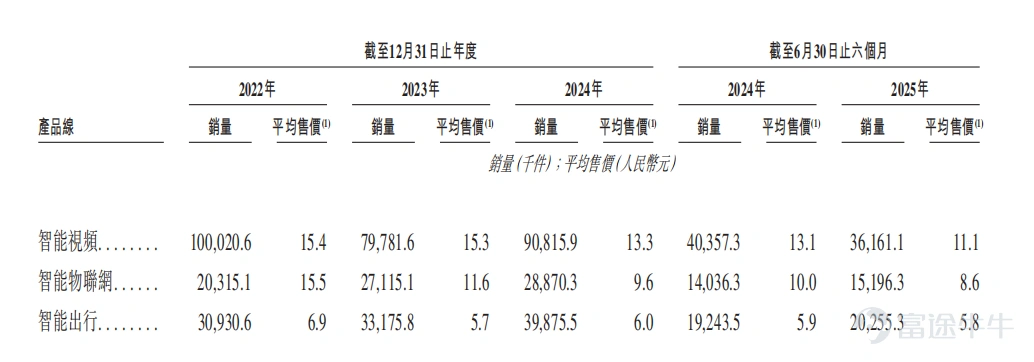

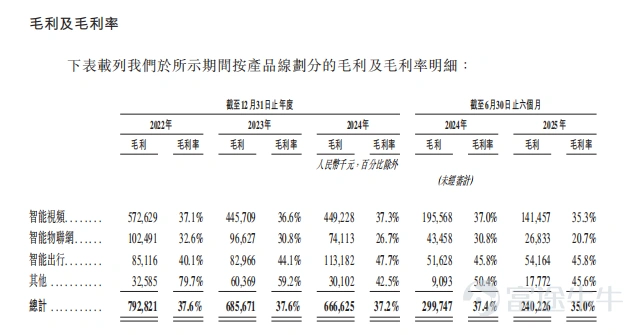

However, in recent years, the domestic security industry has entered a cyclical adjustment phase, with optimization of supply and demand structures bringing temporary challenges. To address market fluctuations and consolidate market share, Fullhan Microelectronics faces short-term pricing pressures. The average selling price of intelligent video products dynamically adjusted from 15.4 yuan in 2022 to 11.1 yuan in the first half of 2025. As a result, the gross margin of this business dropped from 37.1% in 2022 to 35.1% in the first half of 2025.

Source: Fuhao Microelectronics IPO prospectus

Source: Fuhao Microelectronics IPO prospectus

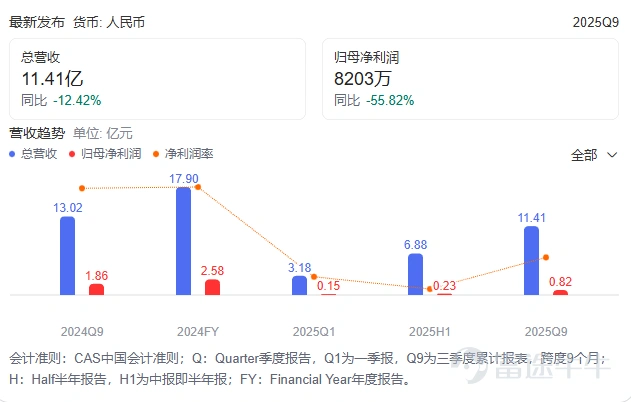

Reflected in overall performance, the company's revenue gradually adjusted from RMB 2.111 billion in 2022 to RMB 1.79 billion in 2024, with net profit attributable to shareholders optimizing from RMB 378 million to RMB 232 million. In the first half of 2025, affected by short-term fluctuations in industry demand, revenue decreased by 14.04% year-on-year to RMB 688 million, while net profit attributable to shareholders improved by 78.1% year-on-year to RMB 23 million. However, this short-term adjustment is not due to operational pressure but rather a strategic choice by Fuhao Microelectronics to focus on long-term value and proactively adapt to the industry cycle, with core resources consistently allocated towards R&D and technological innovation.

Source: Baidu (Fuhao Microelectronics financial report)

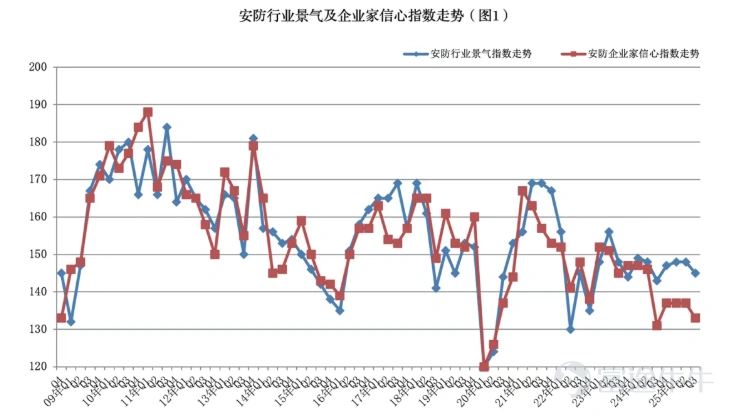

Notably, China’s domestic security industry has shown clear resilience and signs of recovery during this weak cycle. According to data from the China Security Association, the industry prosperity index for Q3 2025 stood at 145, a slight decrease of 3 points from the previous quarter but an increase of 2 points compared to the same period last year, remaining in the “relatively prosperous range.” Additionally, 59% of surveyed companies reported their business conditions as “good,” showing a year-on-year and quarter-on-quarter upward trend.

Source: China Security Association

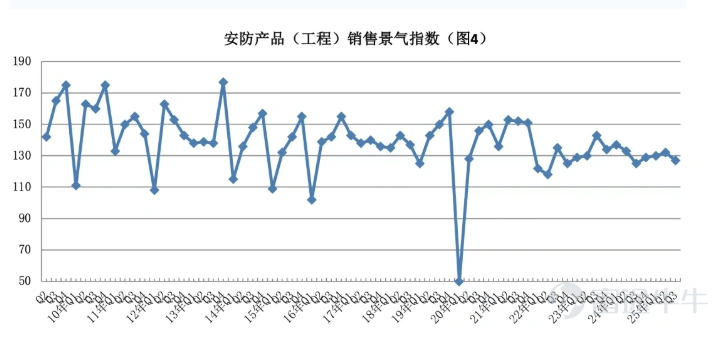

From the sales perspective, the prosperity index for security product (project) sales reached 127, up 2 points year-on-year. Among firms, 43% achieved sales growth, while 41% maintained stable sales, indicating that market demand is gradually stabilizing.

Source: China Security Association

The performance of leading companies in the industry provides direct confirmation of the recovery trend. For instance, Hikvision’s revenue for the first three quarters of 2025 increased by 1.18% year-on-year, and its net profit attributable to shareholders grew by 14.94%. Meanwhile, Dahua Technology saw its revenue grow by 2.06% year-on-year during the same period, with a significant 38.92% surge in net profit attributable to shareholders. The improvement in profitability among top companies sends positive signals across the upstream and downstream supply chain.

“Currently, the country is prioritizing the expansion of domestic demand as a key direction for economic development, and the crackdown on ‘internally competitive’ practices within the industry is becoming more profound. Personally, I believe that competition in the security industry will cool down significantly in 2026, no longer resembling the chaotic situation of price wars in the past,” said Du Lei (pseudonym), a veteran in the security industry, when discussing industry trends.

He further analyzed: 'On the one hand, whether it’s TOB, TOC, or TOG, people's demands for security have long changed—they are no longer satisfied with basic monitoring that can only record and capture, but want intelligent systems integrated with new technologies such as AI, IoT, and big data, which can also be linked to public services. In this way, companies that rely solely on homogenized hardware and survive by winning bids through price wars will definitely not meet the threshold of these new demands. Market resources will increasingly concentrate in the hands of leading companies and specialized firms with continuous R&D capabilities, industry knowledge, and the ability to deliver comprehensive solutions, leaving less and less room for low-price competition.'

'On the other hand, leading companies like Hikvision have started focusing on profit quality rather than blindly pursuing revenue scale since the second half of 2024. This is actually setting a good example, aiming to help the entire industry break out of the vicious cycle of ‘low-quality competition → low profit → inability to innovate → more low-quality competition.’ Although this process won’t happen overnight, and there may still be price wars in some niche areas, the general direction is certainly moving towards letting technology create value.'

Du Lei specifically mentioned: 'This aligns perfectly with Fullhan Microelectronics’ consistent focus on R&D. The current industry competition isn’t about who sells cheaper anymore, but who has stronger technology and better solutions. Fullhan Microelectronics’ continued investment in R&D precisely matches the rhythm of the industry transformation, allowing it to seize this wave of opportunities going forward.'

As Du Lei mentioned, Fullhan Microelectronics has never slackened its investment in R&D. Since 2022, the company’s R&D expenses have continued to grow, with their proportion of revenue steadily increasing. In the first half of 2025, R&D investment reached 171 million yuan, accounting for 24.8% of revenue. By the end of June 2025, the R&D team had grown to 438 people, representing 81% of the total workforce.

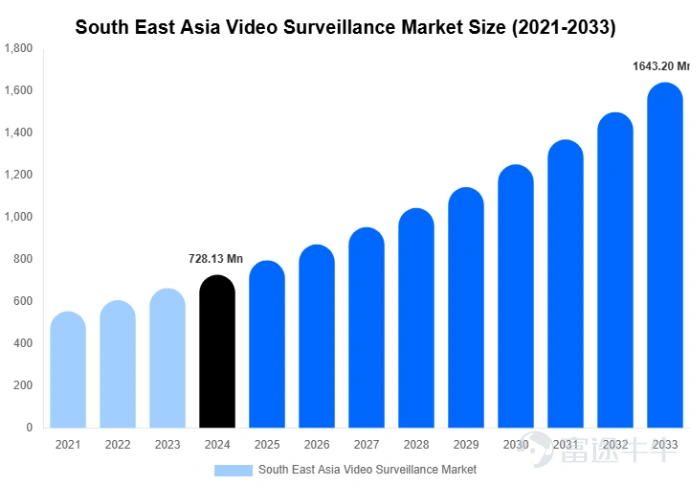

While the domestic market is gradually recovering and the competitive landscape is improving, overseas markets have opened up an entirely new growth space for Fullhan Microelectronics. Unlike the cyclical adjustments in the domestic market, the security markets in regions such as Southeast Asia are in a phase of continuous expansion: driven by rising local safety needs (the number of foreign nationals involved in criminal cases on Indonesia's Bali Island grew by 16% year-on-year in 2024), the video surveillance market in Southeast Asia is rapidly expanding.

According to Deep Market Insights, the market size reached $728 million in 2024 and is expected to grow to $1.643 billion by 2033, with a compound annual growth rate (CAGR) of 9.37% from 2025 to 2033. Among this, camera products hold the largest market share, providing a clear entry opportunity for Fullhan Microelectronics’ smart video chips.

Image source: Deep Market Insights

02.

AI Endpoints: Short-term Pain Points to Solve, Long-term Growth Expected

To mitigate the impact of cyclical fluctuations in the security industry, Fullhan Microelectronics is actively promoting a business diversification strategy, focusing on two emerging sectors—smart IoT and intelligent mobility—gradually building a development pattern of 'core business stability, emerging business expansion,' effectively reducing reliance on a single business risk.

In the field of smart IoT, Fullhan Microelectronics' products are mainly applied in diverse scenarios such as home cameras, video doorbells, smart home appliances, and wearable video devices, with their business share steadily increasing: from 2022 to 2024, the revenue contribution of this business grew from 14.9% to 15.5%, becoming an important supplement to the company’s performance.

However, due to the global AI end-products generally being in the early market education stage and some categories facing dual challenges of supply chain adaptation and market acceptance, this business is still in the preliminary stages of technical exploration and market validation. It is currently experiencing short-term pressures such as declining product unit prices and limited revenue scale.

In the first half of 2025, the business generated revenue of 129 million yuan, with room for further expansion. The average selling price dropped from 15.5 yuan in 2022 to 8.6 yuan in the first half of 2025, marking a 44.5% decrease.

Taking AI glasses as an example, Fullhan Micro has already taken the lead in technological positioning. The MC6350 chip launched in 2025 achieved industry breakthroughs with three core advantages: adopting a 12nm low-power process, video recording power consumption is only 1/4 that of mainstream products; equipped with an 8×8mm ultra-small package integrating 256MB DDR, effectively reducing terminal BOM costs; leveraging mature AI-ISP technology to precisely address the industry pain point of blurry night shooting, providing core computing power support for terminal product upgrades.

Image source: Fuhangwei official account

However, looking at the current state of the industry, smart glasses still face short-term challenges such as low shipment volumes and high return rates. According to data from Luo Tu Technology, total sales of smart glasses (including AR glasses) in Q1 2025 were only 116,000 units, with AI camera glasses sales reaching just 16,000 units. E-commerce platform data further confirms this situation: the return rate for Xiaomi AI glasses on platforms like JD.com and Douyin is around 40%, with the industry average return rate generally in the 40%-50% range, and some brands even reaching 60%. This reflects that products are currently mainly 'experience-based' consumption and have yet to enter the mass adoption phase.

The core issue behind this phenomenon lies in the fact that the AI glasses industry has not fully reconciled the 'triangular contradiction' of 'lightweight, battery life, and high-performance chips'—pursuing lightweight design often leads to reduced battery life, improving battery life may increase product weight, and equipping high-performance chips can exacerbate power consumption issues. Balancing these three elements has become a common technical challenge for the industry.

Despite this, global research institutions and tech companies have not slowed down their exploration efforts but are instead focusing on key technological areas, continuously tackling challenges and painting a broad future landscape for the smart glasses sector.

Source: DoNews graphic based on publicly available information

Behind these efforts lies optimism about the future of AI glasses. The ultimate vision for smart glasses is to become popular, fashionable, and comfortable wearable computing devices. Such products will not only seamlessly collaborate with smartphones but also rely on sensors, AI, and natural interaction technologies to extend and enhance human senses, potentially developing into 'human enhancement organs.' Meta founder Zuckerberg once predicted that smart glasses might eventually replace smartphones as the next-generation core personal communication and computing platform.

Similar characteristics of the market cognition stage are also reflected in the AI home appliance sector. A home appliance brand dealer, Liu Hang (pseudonym), stated that AI home appliances represent a clear future trend for the industry. However, current consumer focus on major home appliances remains on basic quality, with some users worried that AI features are cumbersome and subsequent repair costs could be high. Market acceptance still needs time to develop.

According to Luo Tu Technology data, the TV market’s branded whole-unit shipments in November 2025 were approximately 3.22 million units, reflecting a 15.7% year-over-year decline, indicating that AI home appliances’ market penetration is still progressing slowly.

Source: LuoTu Technology

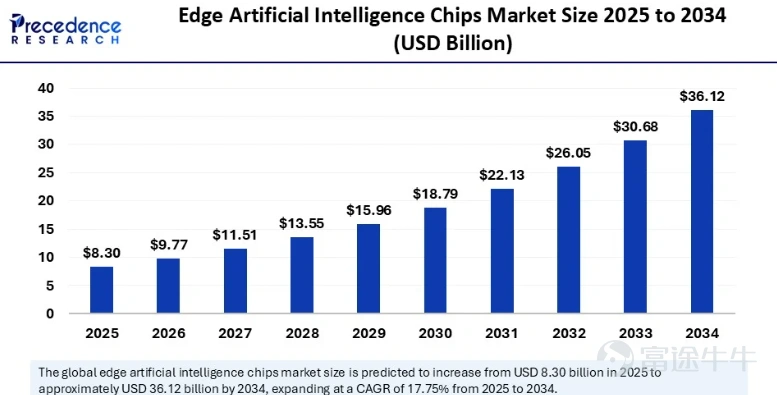

However, short-term industry pains have not overshadowed long-term growth potential. Against the backdrop of rapid development in the global AI + AIoT industries, edge-side AI chips, as the core computing power carrier for intelligent terminals, are entering a golden period of continuous market expansion.

Precedence Research predicts that the global edge AI chip market size will be $8.3 billion in 2025 and is expected to grow at a compound annual growth rate of 17.75% to reach $36.12 billion by 2034. The surge in demand for low latency and real-time data processing at the edge is becoming the core driver of market growth, providing solid industry support for the long-term development of Fullhan Micro’s intelligent IoT business.

Image source: Precedence Research

Source: Precedence Research. In addition to its smart IoT business, Fullhan Micro's concurrently expanding smart mobility business primarily serves applications such as in-vehicle cameras and dashboard displays. From 2022 to 2024, revenue from this business steadily increased from 10% to 13.2%, forming a synergistic growth trend with the smart IoT business, which helped push the proportion of smart video business revenue back to a reasonable 58.2% in the first half of 2025, further shaping the company's diversified business structure.

Of course, the smart mobility business also faces phased challenges, such as relatively small revenue scale and declining selling prices. Revenue from this business was 118 million yuan in the first half of 2025, with the average selling price of products dropping from 6.9 yuan in 2022 to 5.8 yuan in the first half of 2025.

However, in terms of industry trends, the automotive ISP market is continuously expanding as autonomous driving levels increase. QY Research predicts that the global market size will reach 7.34 billion yuan by 2031, indicating vast growth potential. In the automotive-grade ISP chip sector, international companies like ON Semiconductor, Sony, Mobileye, and TI have formed an integrated 'CIS+ISP+AI' full-stack trend, demonstrating technological leadership. However, their closed architecture and high costs present broad opportunities for domestic substitution by Chinese enterprises.

Source: DoNews graphic based on publicly available information

In this context, domestic companies such as Fullhan Micro, VeriSilicon, OmniVision, and SmartSens are accelerating the domestic substitution process. In the future, Fullhan Micro’s smart mobility business is expected to achieve simultaneous breakthroughs in scale and profitability, driven by industry growth and domestic substitution benefits.

03.

Global Expansion: Multi-dimensional Breakthrough in Overseas Markets

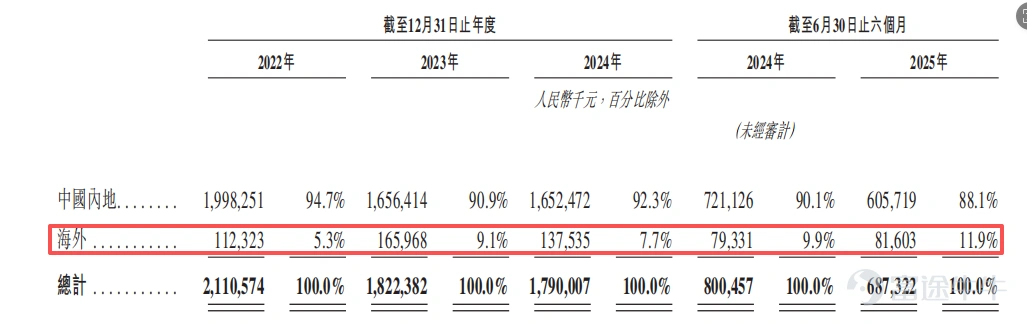

With the continuous growth in global demand for AI chips, Fullhan Micro is accelerating its overseas market expansion. The proportion of overseas revenue increased from 5.3% in 2022 to 11.9% in the first half of 2025, showing clear momentum in international growth.

Image source: Fuhangwei financial report

However, objectively speaking, Fullhan Micro's overseas business is still in its infancy. Taking the first half of 2025 as an example, Amlogic and Beijing Junzheng’s overseas revenues were RMB 2.961 billion and RMB 1.876 billion respectively, significantly higher than Fullhan Micro's RMB 0.82 billion. Moreover, Amlogic's products have already fully covered major global markets such as North America, Europe, and Latin America, showcasing strong international operational capabilities.

The core reason for this gap lies in Fullhan Micro's past focus on the domestic vision chip market, with overseas expansion yet to achieve scale effects. To narrow this gap and unlock global growth potential, the company has clearly articulated a “three-step” globalization strategy: initially focusing on establishing a foothold in Southeast Asia, gradually expanding into the European market in the mid-term, and finally entering the American market opportunistically, forming a progressive and steady path to globalization.

However, the road to going global is not smooth, as Fullhan Micro must face multiple real-world challenges including compliance requirements, price competition, and geopolitical conflicts. Taking the Southeast Asian market as an example, data from Uboxcam shows that in Q1 2024, Google Nest cameras held less than 7% market share in emerging markets in Asia-Pacific (Southeast Asia/India). The core issue was the difficulty in competing with low-priced local brands, and price wars in end markets easily transmitted upstream along the supply chain, directly squeezing the profit margins of chip suppliers, creating significant pressure for Fullhan Micro’s entry into the Southeast Asian market.

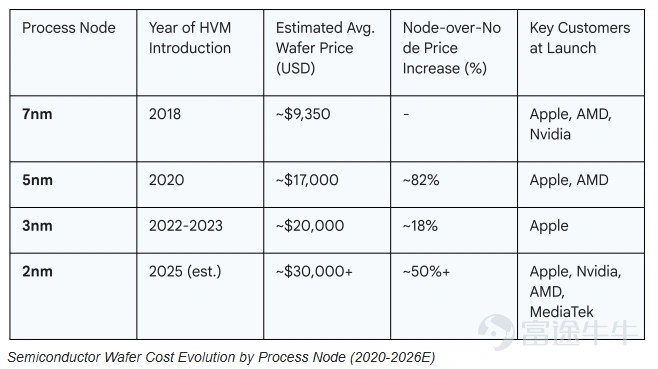

More critically, wafer manufacturing costs have entered an upward cycle, further increasing the uncertainty of profitability abroad. According to 'EE Times ASIA,' Taiwan Semiconductor plans to raise prices by 5%-10% for advanced processes below 5nm starting in 2026, with 2nm wafer prices expected to increase by more than 50%. Currently, the unit price of 300mm wafers for 3nm processes is about $20,000, and after the price hike, 2nm product prices may soar above $30,000.

Image source: "EE Times ASIA"

AMD CEO Lisa Su also publicly stated that chip production costs at their Arizona plant in the United States are 5%-20% higher compared to Taiwan, with premium pricing for 4nm chips potentially reaching 30%. This means that as Fullhan Micro expands overseas in the future, it will face continuously rising cost pressures, and whether these cost increases can be effectively passed on to downstream customers remains highly uncertain.

However, industry pioneers have accumulated rich experience in going global, providing valuable lessons for Fullhan Micro. At the operational level, leading companies generally enhance competitiveness through deepening localization strategies: Amlogic has established technical support centers in North America and Europe to enable rapid response to customer needs; Sigmastar Technology has set up offices in Southeast Asia to align with local market demands, driving steady regional revenue growth.

At the same time, by forming deep partnerships with international leading clients—such as Actions Technology collaborating with Harman and Sony to develop high-end audio chips—companies can quickly enter the high-end market and effectively enhance brand influence and market competitiveness.

In terms of risk management, companies have built 'dual circulation' systems to withstand geopolitical risks: Sigmastar Technology adopts differentiated supply chain layouts between domestic and overseas operations to ensure delivery stability under extreme circumstances; Beijing Junzheng and Allwinner Technology deepen cooperation with domestic foundries while actively stockpiling overseas supply chain resources, forming complementary support.

Additionally, Hikvision has long been deeply engaged in the global market, with overseas business revenue accounting for over 30%. Its mature experience in overseas channel development, localized operations, and risk control also provides important references for Fullhan Micro.

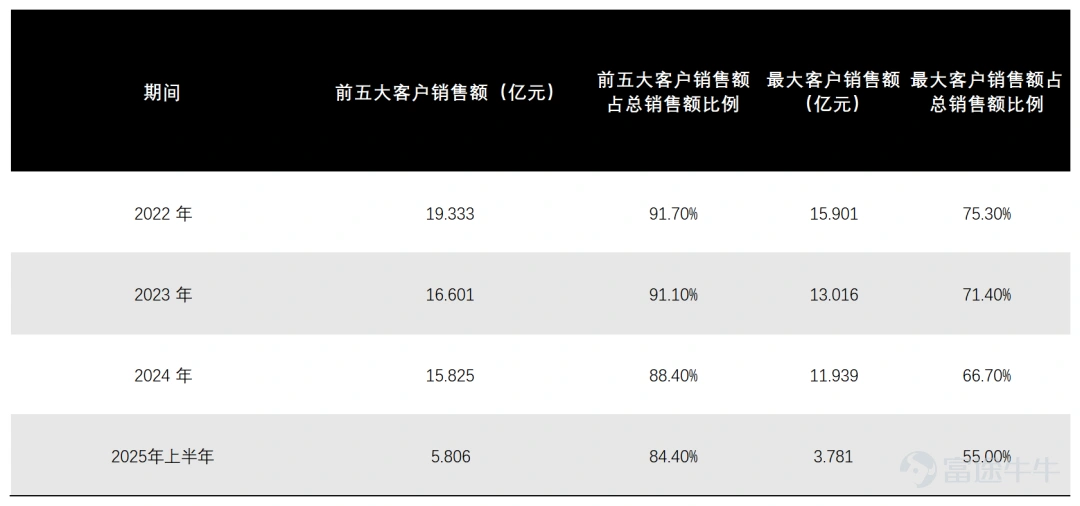

Notably, Fullhan Micro has proactively taken steps to manage risk by optimizing its client portfolio to reduce reliance on any single customer — the sales contribution from its top five clients decreased steadily from 75.3% in 2022 to 55% in the first half of 2025. This has significantly enhanced its risk resistance, laying a solid foundation for capturing overseas growth opportunities and navigating fluctuations in the international market.

Image source: Fuhangwei prospectus, chart by DoNews

Despite facing cyclical pressures in the security industry, insufficient development in the AI end-user market, and challenges in overseas expansion, Fullhan Micro is well-positioned to benefit from industry recovery, technological upgrades, and domestic substitution trends over the long term. If the company continues to strengthen its technological edge and accelerates market adoption, it is poised to seize new growth opportunities amid industrial transformation and achieve steady development.

By Cao Shuangtao

Editor | Yang Bocheng

Cover Image | DouBao AI

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment