China and the US begin implementing the Kuala Lumpur economic and trade consultation consensus.

Why does the relief of liquidity pressure following the end of the U.S. government shutdown still leave Hong Kong stocks weak and powerless?

With the easing of geopolitical tensions, the market had high hopes for the Hong Kong stock market in October and beyond. However, reality once again dashed those hopes: from October to early November, instead of soaring, the Hong Kong stock market appeared rather 'precarious.'

As a result, bearish voices have resurfaced in the market, with statements like 'the market has entered an adjustment period' and 'Hong Kong stocks are overvalued,' leaving many friends perplexed and disheartened throughout October and struggling through November, seemingly missing a small rebound at the end of November. Then came the unclear direction of the sideways market in December.

So, what exactly are the main factors influencing the Hong Kong stock market? And which sectors of the Hong Kong stock market hold potential for significant opportunities? With these questions in mind, this article is written, with the core viewpoints as follows:

Firstly, the 'abnormal' performance of the Hong Kong stock market is mainly due to the impact of the previous U.S. government shutdown on liquidity; now that the shutdown has ended, liquidity pressures in the market will ease.

Secondly, the fundamentals of the Hong Kong stock market are primarily influenced by the mainland economy. In this article, we are optimistic about the consumer market, especially flash sales businesses, which will raise the ceiling for related industries.

Thirdly, time is on the side of the Hong Kong stock market, and there is no need to worry excessively in the short term.

The main factor behind recent volatility in Hong Kong stocks: U.S. government shutdown

Under the linked exchange rate system, the Hong Kong dollar exists as a 'proxy' for the U.S. dollar, making the Hong Kong stock market a U.S. dollar-denominated market. This positioning means that the liquidity of the Hong Kong stock market almost rises and falls with that of the U.S. stock market.

To study Hong Kong stocks, the primary focus should be on the United States.

The most significant factor disturbing dollar liquidity recently has been the government shutdown. On September 30, 2025, due to disagreements between the Republican and Democratic parties over expenditures related to healthcare benefits, the U.S. Senate failed to pass a new temporary appropriations bill before the end of the previous fiscal year, leading to the exhaustion of funds necessary to maintain government operations. Starting from October 1, the U.S. federal government experienced another 'shutdown,' the first in nearly seven years.

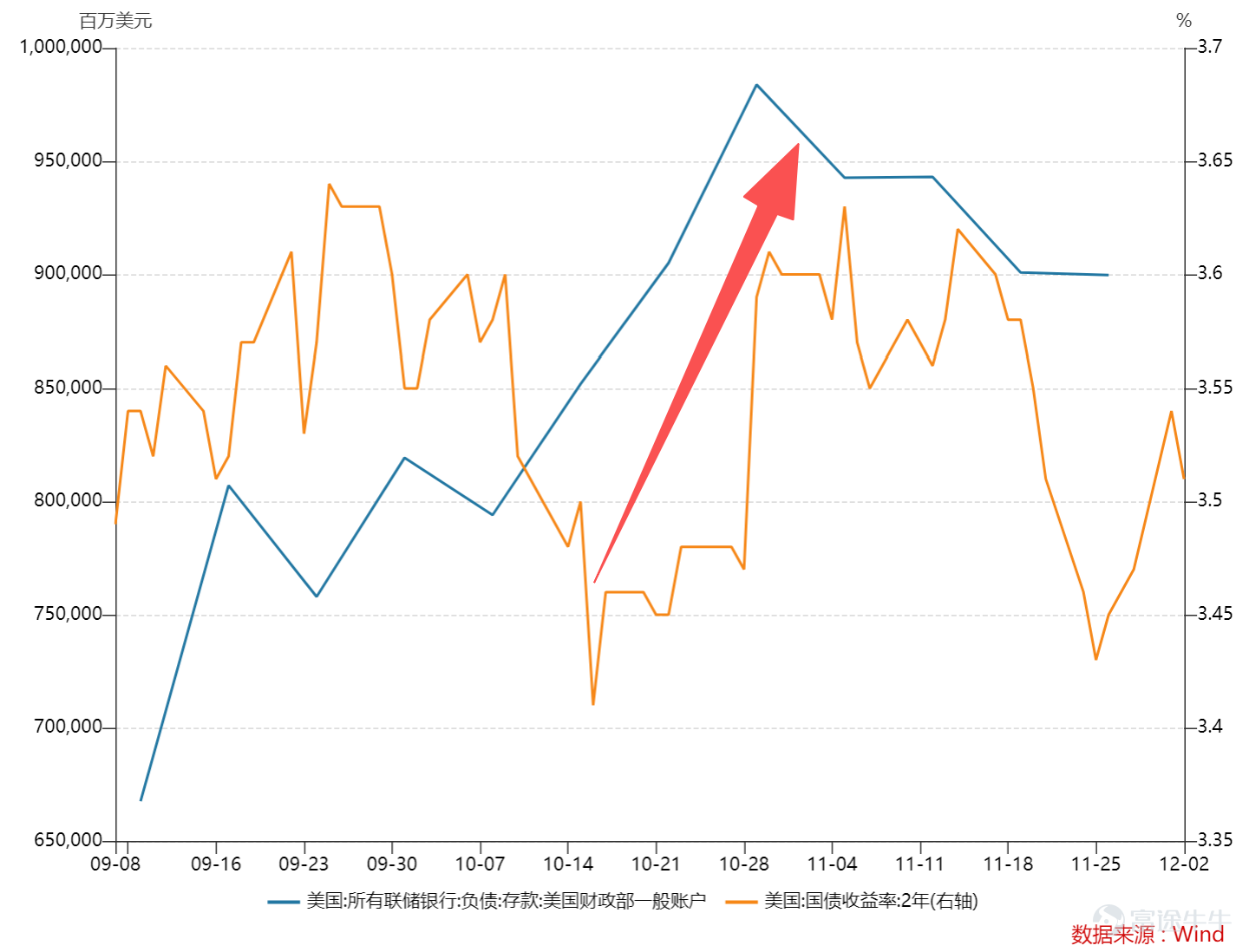

After the government shutdown, financing activities such as treasury issuance continued, but almost all government spending operations came to a complete halt, causing the U.S. Treasury account to become 'inflow-only.'

At that time, while the Federal Reserve was still in the 'balance sheet reduction cycle' (although Powell had already hinted at the possibility of an early conclusion to this process), the Treasury’s account also continued to 'absorb' liquidity through the bond market, significantly negatively impacting the liquidity of U.S. financial markets.

In the above chart, we can clearly observe that after October, there was a very noticeable increase in the balance of the U.S. Treasury General Account (close to one trillion dollars), directly compressing the market value of U.S. Treasuries (with yields climbing). Previous public opinion and market analysis predominantly interpreted the rebound in U.S. Treasury yields from the perspective of the Federal Reserve (Powell repeatedly made hawkish remarks). However, this may have underestimated the unique constraint posed by the government shutdown on liquidity. Under the influence of this factor, prices across the bond market, stock market, precious metals, and other commodities saw substantial corrections, and Hong Kong stocks were naturally not immune.

The easing of geopolitical tensions is certainly a major positive for Hong Kong stocks, but it unfortunately coincided with the U.S. government shutdown. In other words, as the shutdown ends and the Treasury General Account balance is released again, market liquidity will be replenished, and various assets will return to their fair values.

This U.S. government shutdown lasted 43 days, the longest in history. With both political parties and financial markets gradually losing patience, Democrats and Republicans returned to the negotiating table to resolve differences and break the deadlock.

On November 12 local time, U.S. President Trump signed a temporary appropriations bill passed by both chambers of Congress at the White House, thus ending the longest federal government 'shutdown' in history, which had lasted 43 days. Hong Kong stocks should not be far from seeing the light at the end of the tunnel. Notably, whenever favorable developments regarding the shutdown were reported, capital markets responded with significant positive feedback. This sufficiently indicates that when the U.S. shutdown ends, it should mark the end of the adjustment period for Hong Kong stocks.

As U.S. monetary policy shifts towards an easing cycle, although the market obviously still awaits the Federal Reserve’s decision on whether to 'cut rates' at the December meeting scheduled for December 9th and 10th—whether it meets the optimistic market expectation of completing the 'final rate cut' within this year—the outcome will play a decisive role in shaping the liquidity environment. Additionally, year-end institutional position adjustments (profit-taking or planning for next year) have caused some sectors to become more volatile; however, attention should be paid to the actual impact of liquidity factors.

A rebound in mainland China's consumer sector is imminent.

After explaining the recent 'abnormal' performance of Hong Kong stocks from the perspective of liquidity, we shift our focus back to mainland China. With the rising trend of mainland enterprises going public in Hong Kong, Hong Kong stocks are increasingly reflecting the economic health of the mainland at a fundamental level. For instance, the popularity of DeepSeek has almost driven the entire technology concept sector in Hong Kong stocks.

So, which areas do we expect to perform well next? Here, we present a very 'counterintuitive' conclusion: the rise of the consumer market is imminent.

Many might argue against this with completely opposing views, using terms like 'involution' and 'insufficient domestic demand,' which are among the most common descriptors for the mainland consumer market. How can we speak of a rise under such conditions?

Admittedly, mainland China’s CPI has remained subdued for a long time, but the year-on-year growth of CPI excluding energy and food has rebounded to a new high this year. Notably, this recovery in core CPI is not due to a low base effect, fundamentally different from the situations in 2021 and 2024. In particular, the year-on-year CPI in the clothing industry is approaching the 2% threshold.

These developments are partly the result of government macroeconomic regulation. After Q2 2025, senior-level meetings were held multiple times to address the 'involution' issue, implementing supply-side reforms in certain industries to stabilize price trends. On the other hand, consumer companies have stimulated demand through business model innovations, with flash sales being a notable example.

Years ago, Wang Jianlin and Jack Ma made a 'bet.' The latter believed that online transactions would account for more than half of the retail market, while the former was highly skeptical. At that time, the era of rapid online economic growth prevailed, and public opinion mostly sided with Jack Ma. However, even now, the online penetration rate remains around 30%, and once online retail exceeded 20%, its growth rate began to decline significantly.

While the online economy is indeed efficient, its rapid expansion can disrupt existing interest structures. For instance, the franchise model commonly adopted by brands sees local dealers heavily investing in store operations, only for the online economy to diminish their stores' original value, prompting offline franchisees to employ various means to constrain the former.

A typical case is the clothing and home appliance industries, where the phenomenon of 'channel exclusivity' (selling different models online and offline) has intensified over the past few years, making it increasingly difficult to sell identical products at the same price both online and offline. Offline channels use product exclusivity to protect themselves.

Flash sales, however, are notably different. Although this business model is led by online enterprises, offline stores can also receive equitable profit distribution. The chain of 'online platform – traffic – delivery capacity – stores' is linked by shared interests, breaking down barriers between online and offline and reshaping the business model, thereby reigniting consumer enthusiasm.

As flash sales operations deepen, key sectors such as logistics providers (e.g., SF Express同城 (09699.HK)) $SF INTRA-CITY (09699.HK)$ This year, the performance in Hong Kong stocks has been quite remarkable, and it will remain one of our key focuses. As the liquidity factors mentioned earlier continue to ease, this sector should deliver even stronger performance.

Moreover, as flash sales deepen, some traditional business models within certain industries will also be reshaped, with Weilong Food (09985.HK) being a typical example. $WL DELICIOUS (09985.HK)$ The offline distribution system gains premium value due to the influx of online traffic, and innovations in the business model will once again expand the growth ceiling.

Our key areas of focus moving forward are:

1) Brands with strong recognition and widespread channel penetration that possess significant commercial leverage (e.g., Uniqlo, Weilong);

2) Platform-based companies that use flash sales to unlock new growth potential (e.g., Alibaba (09988.HK)). $BABA-W (09988.HK)$ )

Liquidity is influenced by the U.S., while fundamentals depend on the mainland economy. These factors make Hong Kong stocks particularly vulnerable to 'squeeze plays,' and the multitude of interference factors often frustrates investors. At this point, we need only focus on the primary and secondary contradictions, which will clarify many issues. The liquidity concerns for Hong Kong stocks are nearing resolution, and the macroeconomic fundamentals are at an early stage of improvement. In terms of timing, the conditions are highly favorable for Hong Kong stocks.

At this juncture, what investors need to do is maintain confidence in Hong Kong stocks and strategically position themselves in sectors with long-term value.

Author: Tiexin

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

2

3