The Big Short Strikes Again: Shorting Tesla! Do You Agree?

Massive orders for AI computing power are surging! Who is reveling in OpenAI's trillion-dollar gamble, and what underlying concerns does it conceal?

Entering 2025, the global investment frenzy in the AI sector continues to intensify, but scrutiny over its potential bubble is also becoming increasingly severe.At the center of this discussion, the focal point is undoubtedly OpenAI.

Based on publicly available information, since the beginning of this year, OpenAI has signed deals worth approximately $1 trillion to secure computing power for running artificial intelligence models. The counterparties to these agreements include $Advanced Micro Devices (AMD.US)$ 、 $NVIDIA (NVDA.US)$ 、 $Oracle (ORCL.US)$ and $CoreWeave (CRWV.US)$ , among others. These enterprises' interests are also tied to OpenAI's future profitability.

According to currently disclosed agreements, the following companies or entities are known to have signed various computational power supply agreements with OpenAI and are now busy purchasing the latest NVIDIA servers.

$Broadcom (AVGO.US)$ : Signed a multi-year agreement with OpenAI to deploy 10 gigawatts of AI data center capacity.

$Oracle (ORCL.US)$ : The company signed a $300 billion agreement with OpenAI aimed at adding 4.5 gigawatts of computing power for the 'Stargate' project.

$Microsoft (MSFT.US)$ : A revised cooperation agreement has been signed with OpenAI, under which the latter commits to purchasing an additional $250 billion worth of Azure cloud services. In return, Microsoft agrees to relinquish its priority supply rights for cloud services and supports OpenAI's capital restructuring. Upon completion of the restructuring, Microsoft will hold a 27% stake.

$NVIDIA (NVDA.US)$ : OpenAI will utilize NVIDIA’s systems to build and deploy at least 10 gigawatts (GW) of AI data centers, using millions of NVIDIA’s graphics processing units (GPUs) to train and deploy OpenAI’s next-generation AI models. To support this landmark strategic partnership, NVIDIA plans to invest up to $100 billion in OpenAI.

$Advanced Micro Devices (AMD.US)$ : OpenAI announced that it will procure and deploy up to 6 gigawatts of AMD Instinct series GPUs, with potential sales reaching as high as $90 billion. In exchange, AMD issued OpenAI warrants to purchase up to 160 million shares of AMD stock at an exercise price of $0.01 per share.

$Amazon (AMZN.US)$ : Amazon Web Services (AWS) announced a $38 billion computing power contract with OpenAI, marking a historic first collaboration between the global cloud computing leader and the AI frontrunner.

$CoreWeave (CRWV.US)$ : Backed by NVIDIA, the emerging cloud computing company OpenAI has placed multiple incremental orders this year, with the latest contract amounting to as much as $22.4 billion.

$Alphabet-C (GOOG.US)$ : In July this year, OpenAI added Google Cloud as a service provider for ChatGPT, though details of the contract remain undisclosed.

Apart from these companies,the larger 'AI blueprint' lies in the 'Stargate' project.In January this year, OpenAI CEO Sam Altman announced at the White House that the scale of the 'Stargate' data center project would be 10 gigawatts. However, during a live broadcast last week, the overall target had tripled. OpenAI has already reached agreements with partners in the UAE and Norway to construct data centers of 1 gigawatt and 230 megawatts, respectively, in those locations.

In fact, OpenAI has issued so many contracts, tying a host of tech giants to one rope, while the capital markets are closely watching OpenAI’s ability to fulfill these commitments.Investors may question whether such circular financing carries risks and which aspects require close monitoring. This article will clarify the thought process for fellow investors.

Does such circular financing carry risks?

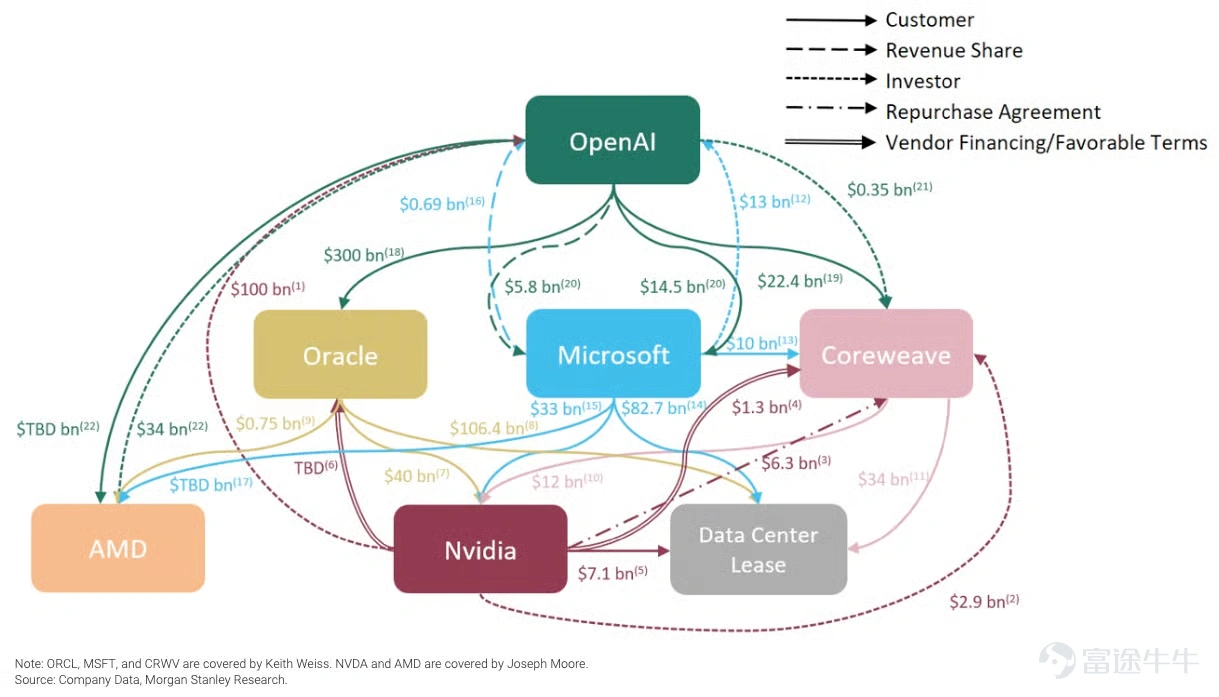

First, as illustrated in this chart compiled by Morgan Stanley, these examples represent only the tip of the iceberg, fully demonstrating the intricate web and substantial scale of funds involved in circular transaction structures.

Source: Morgan Stanley

Morgan Stanley strategists noted,“Circularity is becoming a core feature of the AI era: suppliers simultaneously act as customers, investors, and creditors, making the sources of funding increasingly complex.”

The strategists stated, “Key players in the AI sector are becoming increasingly intertwined—suppliers provide funding to customers, customer concentration is rising, and both parties engage in revenue-sharing agreements, take-or-pay contracts, and supplier repurchase arrangements.” According to their analysis, suppliers are supporting customer operations through equity investments and innovative financing mechanisms.

This mechanism, in turn, enhances the customer’s balance sheet, enabling other suppliers selling to that customer to assume more debt.In other words, the AI economy has formed a self-reinforcing closed loop.

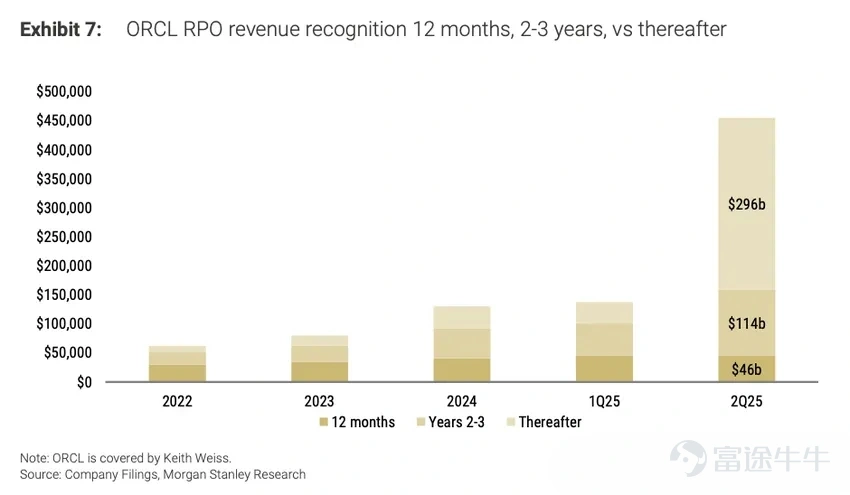

However, it is worth noting that many of the orders behind these circular transactions involve long-term contracts.As contract durations continue to extend, the scale of accumulated unfulfilled obligations (RPO) is growing significantly, undoubtedly amplifying the risk exposure associated with potential order cancellations in the future.

For instance, Oracle's long-term RPOs (obligations to be fulfilled three years from now) for the second quarter of 2025 have surged to over 65%. Behind this substantial figure lies a notable risk of order cancellations.

Source: Morgan Stanley

This phenomenon evokes memories of the circular investment patterns between Nortel, Lucent, and Cisco and internet startups during the dot-com bubble era.While this closed loop of capital and business flow has efficiently fueled the rapid expansion of AI infrastructure in the short term, it has also raised concerns that 'circular investments' are creating a self-fulfilling illusion of prosperity, potentially culminating in a financial bubble.

UBS Group notes that while this risk warrants attention,the current situation differs significantly from earlier tech bubbles.

First, the scale of circular transactions is not sufficient to destabilize the market.For example, the collaboration between OpenAI and NVIDIA is projected to account for approximately 13% of NVIDIA’s expected revenue in 2026. If the planned deployment of one gigawatt is completed in the second half of 2026, with total capital expenditure estimated at $50 to $60 billion, NVIDIA will receive $35 billion. Of this, around $10 billion may be reinvested back into OpenAI, with subsequent investments contingent upon actual progress in AI commercialization—a performance-based model rather than a speculative fixed commitment.

Second, the financial health of today’s leading AI companies far surpasses that of the telecom giants of the past.Most major technology companies rely on operating cash flow to fund capital expenditures rather than depending on debt financing. By 2025, the free cash flow (after deducting capital expenditures) of the world’s four largest technology firms is expected to reach $203 billion, demonstrating robust investment capacity and a sustainable capital structure.

Third, valuation levels are more reasonable, with higher earnings quality.At the end of the 1990s, leading internet companies had forward price-to-earnings ratios as high as 60 times, whereas today’s AI giants average approximately 35 times, supported by more stable cash flows and balance sheets. This suggests that the market has not entered an irrational valuation bubble.

UBS Group noted,Although medium-term risks remain—particularly if the adoption of AI or revenue growth falls short of expectations—the industry’s fundamentals remain solid in the short term.This round of investment and financing activity is actually supporting supply chain performance expectations and may even lead to upward revisions in earnings.

Which segment should be closely monitored?

First, Oracle's bonds, which represent the 'weakest link' in AI leverage, require attention.

The latest data shows that the cost of five-year credit default swaps (CDS) for Oracle has risen to its highest level since October 2023. The spread on its 4.9% coupon bonds maturing in 2033 widened by 26 basis points to 83 basis points.

Market analysts warn that while the AI boom is driving record highs in U.S. equities, Oracle’s rapidly expanding debt could become the first crack in the narrative of an AI bubble. Oracle currently has approximately $95 billion in outstanding debt, making it the largest corporate issuer outside the financial sector in the Bloomberg High-Yield Index.

Market observers have pointed out that,Oracle's debt situation may become a key indicator for testing the sustainability of the AI investment boom.Therefore, it is crucial to closely monitor Oracle’s CDS trends — this could be where the first cracks in the AI bubble narrative appear.

Secondly, UBS Group summarized five key lessons from the bursting of the dot-com bubble:

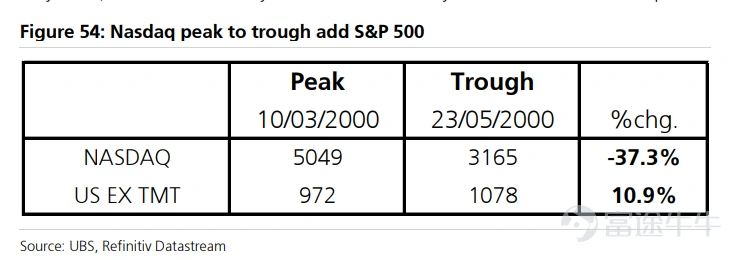

In the early stages of the bubble burst, non-bubble sectors often perform well. During the period from March to May 2000 when the Nasdaq fell by 37.3%, non-tech stocks rose by 10.9%, and the S&P 500 overall declined by 10%. This provided investors with an opportunity to reallocate their portfolios.

The "echo effect" is worth noting. On September 1, 2000, the S&P 500 almost returned to its previous high on March 24, falling short by only 0.4%, while the Nasdaq was still 16% below its peak. This "double-top" pattern can easily mislead investors.

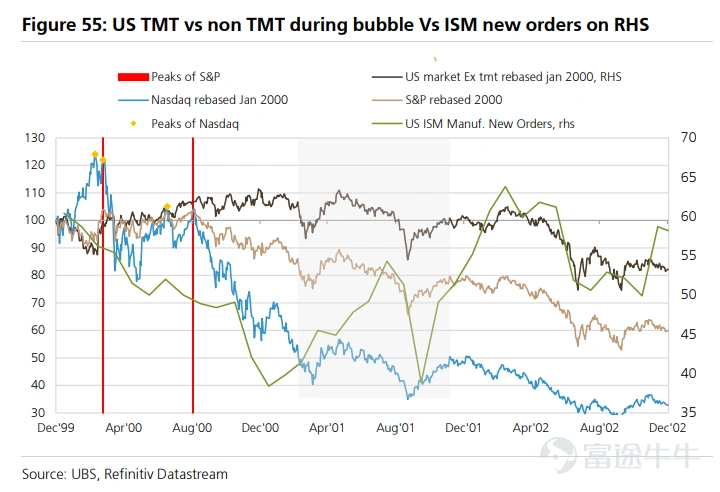

True bear markets often coincide with economic recessions. As the collapse of tech investments triggered a sharp slowdown in economic activity, the ISM New Orders Index dropped from 60 in January 2000 to 38 in January 2001, and the U.S. officially entered a recession in February 2001. Non-tech stocks fell by 33% from their peak.

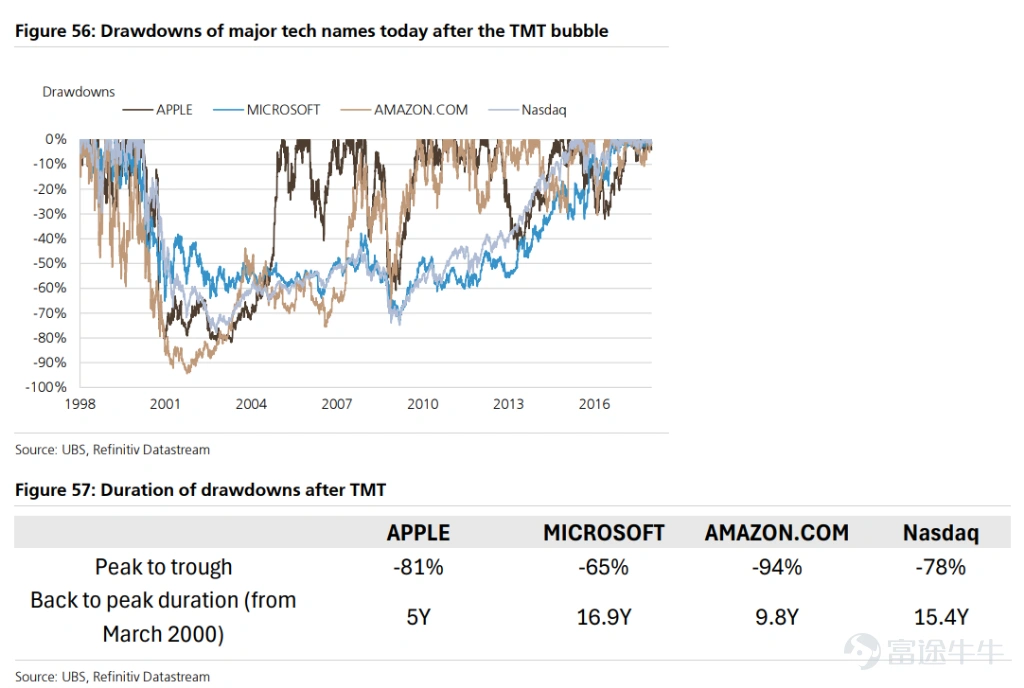

There are numerous examples of concepts being fundamentally correct but prices being severely overvalued. Microsoft, Amazon, and Apple fell by 65% to 94% from their peaks and took 5 to 17 years to return to their previous highs. Many components of the "Nifty Fifty" also experienced similar fates. This serves as a reminder to investors that even betting on the right technological trend, excessive valuations can still lead to long-term capital losses.

Finally, the ultimate winners of the value chain may exceed expectations. The real winners of the dot-com bubble were not telecom operators, but companies that captured the value chain through users (such as Apple), enterprises leveraging social media (like Meta and Google), and providers of critical software that cannot be disrupted (such as Microsoft). This suggests that investors need to deeply consider the distribution of value in technological transformations.

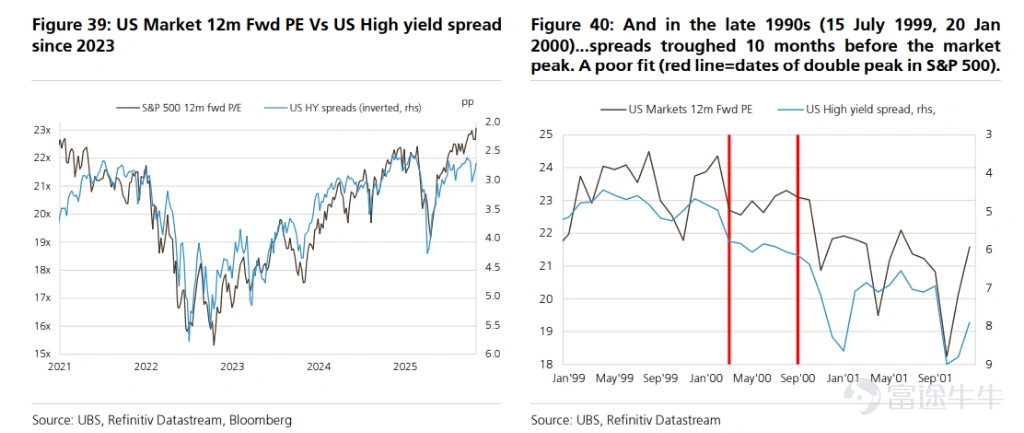

Additionally, credit spreads are also important indicators to watch.The chart below illustrates the annual change rate of the S&P 500 Index alongside the spread between Moody's Baa-rated (investment-grade) corporate bond index and the 10-year U.S. Treasury yield.A widening spread is often accompanied by lower annual returns in financial markets.

During the dot-com bubble, credit spreads bottomed out approximately ten months before the stock market peaked, as the debt market was heavily utilized to finance tech investments. While the correlation between current tech stocks and credit spreads is higher, this leading relationship may differ in the current cycle.

UBS analysis indicates that despite concerns over a potential bubble driven by the AI theme, several key indicators have not yet reached extreme levels typical of historical bubble peaks.Investors need to closely monitor multi-dimensional signals such as valuation, earnings momentum, investment scale, and market breadth to determine when the bubble transitions from an 'early stage' to a 'peak risk' phase.

Finally, the listing process of OpenAI serves as another critical risk indicator.As the acknowledged core of the current AI bubble, its IPO could become a landmark turning point signaling the peak and subsequent reversal of the bubble. Market concerns suggest that a trillion-dollar IPO event might not only drain market liquidity but also act as the trigger for bursting the bubble and sparking a systemic crisis.

According to Reuters citing sources familiar with the matter, OpenAI is considering going public at a valuation of up to $1 trillion, with expectations to file for an IPO with securities regulators as early as the second half of 2026, targeting an official listing in 2027.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (10)

to post a comment

44

183