China and the US begin implementing the Kuala Lumpur economic and trade consultation consensus.

Trump once again moves the market! Recalling the April plunge, will the TACO trade reappear?

During Friday's trading session, impacted by Trump's tariff threats, the U.S. stock market relived the "April plunge" from six months ago, with high-risk assets like cryptocurrencies and two major economic bellwethers—crude oil and copper—plummeting, while U.S. bonds and gold prices surged.

At present, the market is interpreting events according to the April playbook, hoping for the return of the TACO trade.The so-called TACO stands for "Trump Always Chickens Out" (Trump always backs down at the last moment).

This year, whenever Trump has brandished the tariff stick,Wall Street has developed a mature profit model based on the market effects of his policies—the "TACO trade."

Reviewing the market performance in the first few months of this year, the "TACO trade" has exhibited a recurring cycle from euphoria to panic. At the beginning of the year, market expectations of deregulation and tax cuts following Trump's return to the White House propelled the stock market to soar, with the S&P 500 index hitting a new historical high in February.

However, the positive trend did not last long. When Trump began prioritizing tariff issues, investor enthusiasm quickly waned. By mid-March, following Trump’s initial announcement of large-scale tariff impositions, the S&P 500 index entered a technical correction, falling more than 10% from its peak.

The subsequent events unfolded as Wall Street anticipated: Trump temporarily paused or scaled back some tariff measures, causing a rebound in the stock market. However, this recovery was extremely short-lived — on April 2, after Trump announced what he called reciprocal tariffs, benchmark indices were once again pushed to the brink of a bear market.

On April 9, after Trump posted on social media that it was a good time to buy and suspended the Liberation Day tariffs, the U.S. stock market embarked on a strong rebound. From April 9 to October 9, the S&P 500 index surged by over 35% cumulatively.

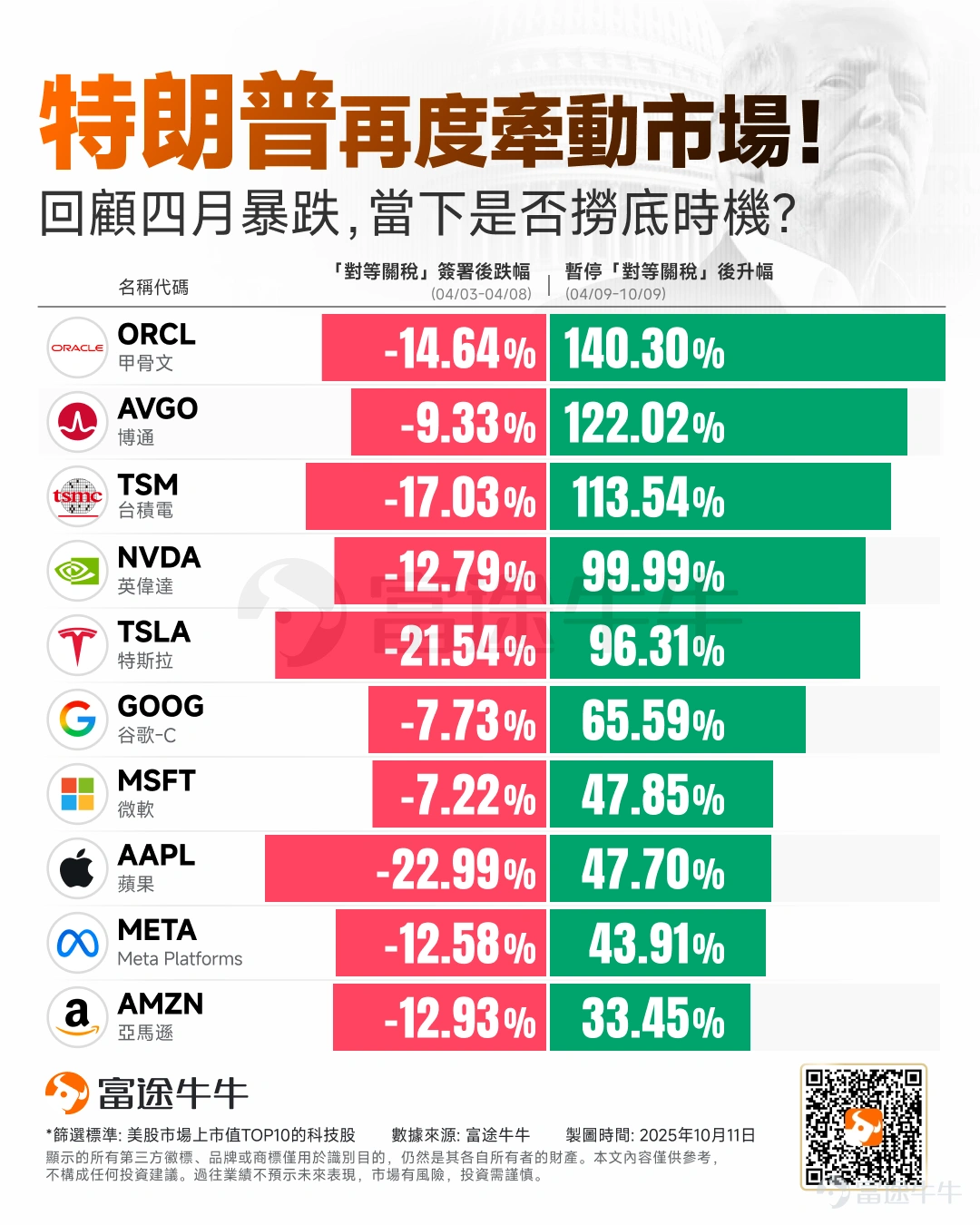

Looking at the performance of tech giants, under the themes of the "TACO trade" and AI-driven trading, they all experienced varying degrees of rebounds after April 9., of which $Oracle (ORCL.US)$ 、 $Broadcom (AVGO.US)$ 、 $Taiwan Semiconductor (TSM.US)$ More than doubled compared to April 8; $NVIDIA (NVDA.US)$ 、 $Tesla (TSLA.US)$ Increased by over 90%; $Alphabet-C (GOOG.US)$ 、 $Microsoft (MSFT.US)$ 、 $Apple (AAPL.US)$ 、 $Meta Platforms (META.US)$ 、 $Amazon (AMZN.US)$ The increase ranged between 30% and 66%.

Then,From the current standpoint, what are the differences compared to April? What should be monitored next? How should investors proceed? The following will explain one by one.

What are the differences compared to April?

According to CICC research,several key differences were found between the current situation and the equivalent tariff measures implemented in early April:

First, the degree of surprise was different.After all, the market had already gone through it once, giving it some psychological preparation. Unlike on April 2, when the measure came as a completely unforeseen surprise, which is the biggest difference.

Second, the scope was different.From the U.S. perspective, the previous equivalent tariff measures targeted almost all global markets, whereas this time it primarily focuses on China. Although the relationship with China remains the most important, the scope still differs. Combined with the first point, this explains why yesterday's 'triple selloff' in stocks, bonds, and currency—as well as volatility—was less pronounced than in April, with more focus on equity sell-offs while there was little movement in U.S. Treasuries and the U.S. dollar.

Third, future expectations differ.Following the last round of equivalent tariffs, the market was essentially ‘driving in the fog,’ having no idea how the situation would evolve. This time, although significant uncertainties remain, the upcoming APEC meeting (October 31 - November 1) prior to the effective date of November 1 may prompt market hesitation. Trump later also indicated that he has not ruled out the possibility of a meeting.

Fourth, the preparations and circumstances of both parties are vastly different.From the U.S. perspective, compared to early April, 1) so far, except for India, the U.S. has reached agreements with most markets; 2) a ceasefire in the Middle East appears to have been achieved; 3) the Federal Reserve has cut interest rates and may continue to do so; 4) the Great Beautiful Act has been passed; 5) concerns about an AI bubble caused by DeepSeek's sudden rise no longer exist. From China’s perspective, both A-shares and H-shares have risen significantly to new highs, though macro fundamentals have weakened recently. However, overall expectations and readiness should be notably stronger than in April.

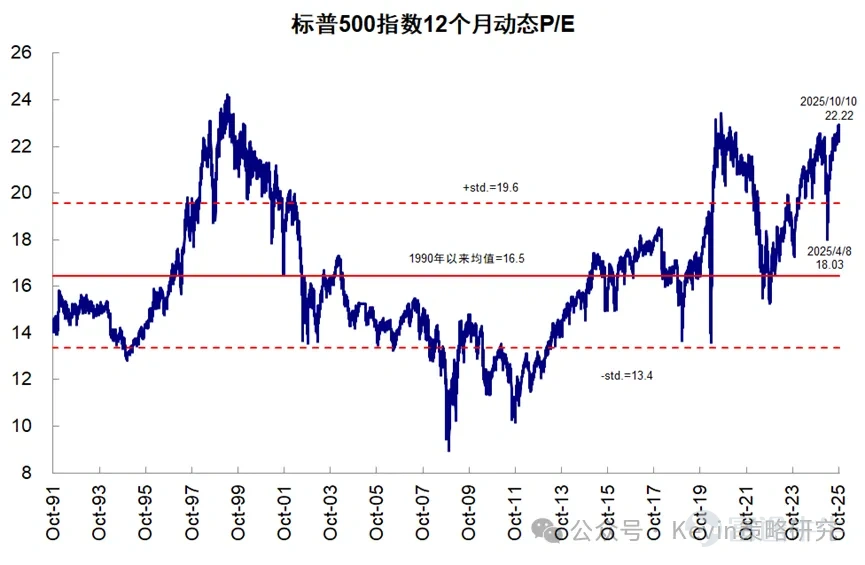

Fifth, the positions of the market are different.Both U.S. and Chinese markets have accumulated substantial unrealized gains, and valuations are higher than before, with the Chinese market showing a larger increase. U.S. stocks, especially the Magnificent Seven, began to correct after DeepSeek's rise in February disrupted the U.S.'s dominance in AI. Currently, the valuation of the 'Magnificent Seven' is around 31 times, still lower than the peak of 33.7 at the end of last year and beginning of this year, compared to 26.8 before the equivalent tariff measures, and a low of 23 after the sharp decline. The current valuation of leading Chinese technology and consumer companies is around 20 times, higher than the previous high of 18.8 before the equivalent tariff measures, with a low of 14 times after the tariffs.

The overall index valuations are similar. The S&P 500 Index is currently at 21 times, with a peak of 22 at the end of last year, 20.5 times before the equivalent tariff measures, and a low of 18 times afterward. The Hang Seng Index is currently at 11.7 times, compared to a high of 10.8 before the equivalent tariff measures and a low of 8.8 times afterward.

What needs to be watched next?

CICC stated that what fundamentally influences market trends remainsthe progress of tariff negotiations,particularly how compromises will be reached before APEC and November 1, which remains the core issue.

Additionally, beyond the macro level,Investors also need to focus on several key support levels of the index.

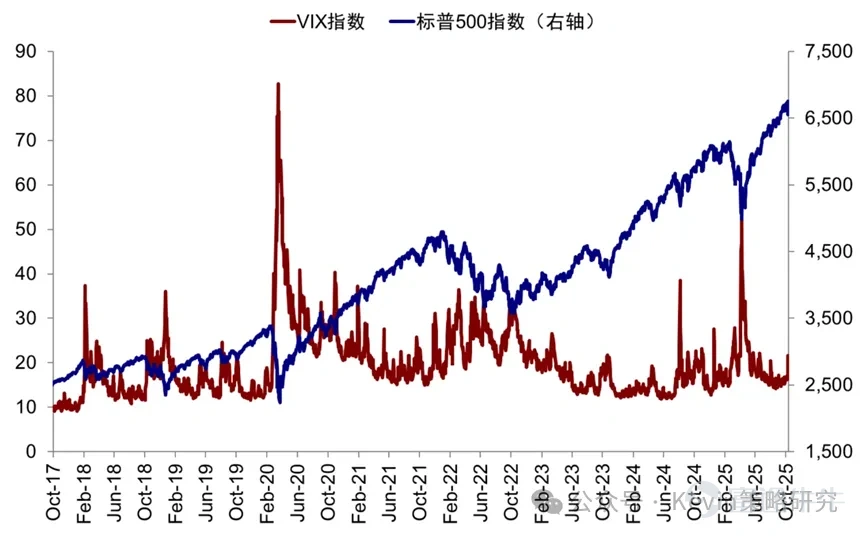

CICC research found that after the reciprocal tariffs were imposed on April 2, the VIX index surged to 60, and currently stands at 21.7. The S&P 500 fell to its 120-week moving average before stabilizing; presently, the 120-week moving average corresponds to 5420 points (17% below the current level).The key support levels prior to this are 6500 and 6200.

The Hang Seng Index previously stabilized after falling to the 250-day and 60-week moving averages; currently, these correspond to approximately 22500 points (14% below the current level).The next key support levels are 25700 and 24500.

How should investors proceed?

From a market perspective, compared to early April,a relatively 'unfavorable' factor is the high level of unrealized gains and elevated valuations,which has led to a stronger desire to take profits and secure gains, potentially causing short-term volatility.

However, this remains a short-term logic.The relative advantage is that the level of panic and preparedness is better than it was at the time,with AI industry trends in both China and the US becoming clearer, and the US monetary and fiscal policies gradually gaining momentum. Thus, a similar level of panic and volatility would only occur if the market becomes convinced that compromise is entirely hopeless.

Therefore, CICC Securities' preliminary judgment is that,short-term fluctuations driven by sentiment may be unavoidable, but the market will also closely monitor the progress of negotiations before November.

If investors have already reduced some of their positions,they can wait and choose a better opportunity to re-enter quality growth sectors at a lower cost.

If investors have not reduced their positions,it may not be necessary to take action during the initial period of peak panic; they can wait until the panic subsides somewhat and adjust accordingly as needed.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (19)

to post a comment

137

299