Powell's remarks come as a much-needed boost! Is a rate cut in October on the horizon?

Tengsi: Analysis of the Interest Rate Cut Cycle | A retrospective look at the Federal Reserve's past interest rate cuts: How do different maturities of bonds perform?

Issue No. 2

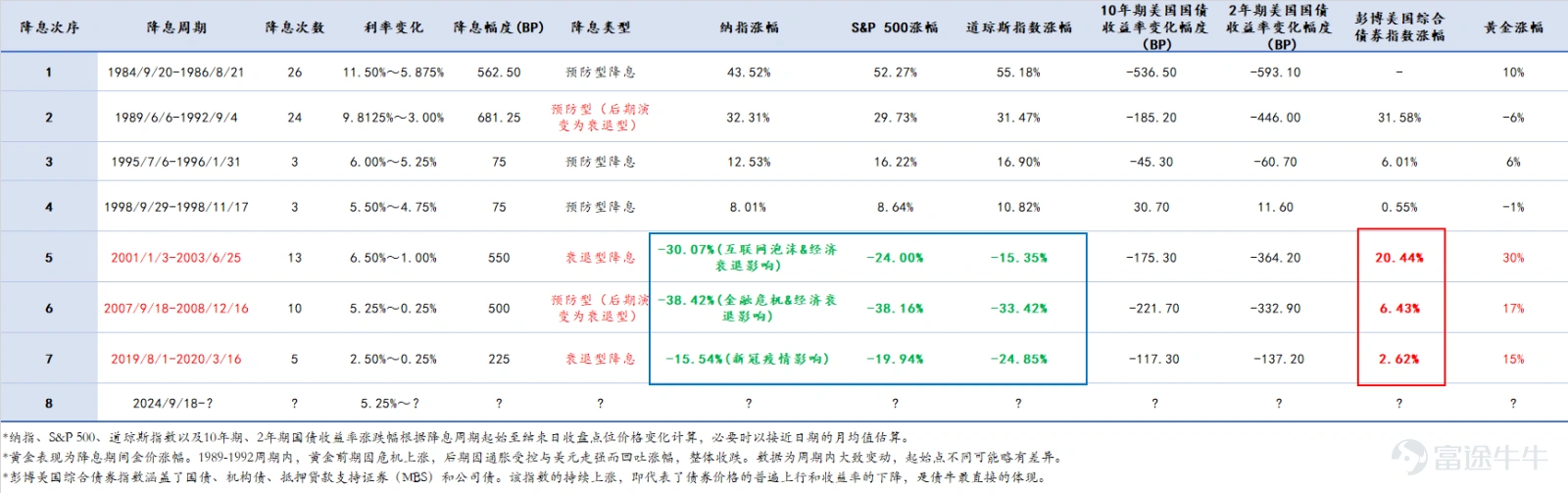

In the previous issue's column, the article reviewed the performance of various assets during seven interest rate cut cycles since 1980. In preventive interest rate cut cycles, all asset classes performed positively overall, while in recessionary interest rate cut cycles, stocks exhibited significant volatility, and bonds stood out as safe-haven assets.

According to CME FedWatch, the probability of a 25 basis point rate cut in September is currently at 99.4%, while the probability of a 50 basis point cut in October stands at 55.3%.Past economic cycles have shown that once the Federal Reserve initiates an interest rate cut cycle, the speed and magnitude of subsequent cuts will depend on the forthcoming economic data. An interest rate cut cycle can benefit bond investors in terms of returns. Stock market returns, on the other hand, are contingent upon economic conditions, the extent of economic slowdown, and the pace of that slowdown. Historically, since 1980, the seven interest rate cut cycles have generally featured the basic characteristic of 'declining yields and rising prices' in the bond market. So, will the performance of bonds with different maturities differ?

How Interest Rate Cuts Drive the Bond Market: The Logic of Price and Yield

The Core Inverse Relationship Between Bond Prices and Yieldsis fundamental to understanding the impact of interest rate cuts. When the Federal Reserve initiates a rate cut and market interest rates trend downward, existing bonds become more attractive due to their relatively higher coupon rates, driving prices up while stimulating demand for safe-haven assets, further amplifying the upward momentum in the bond market.

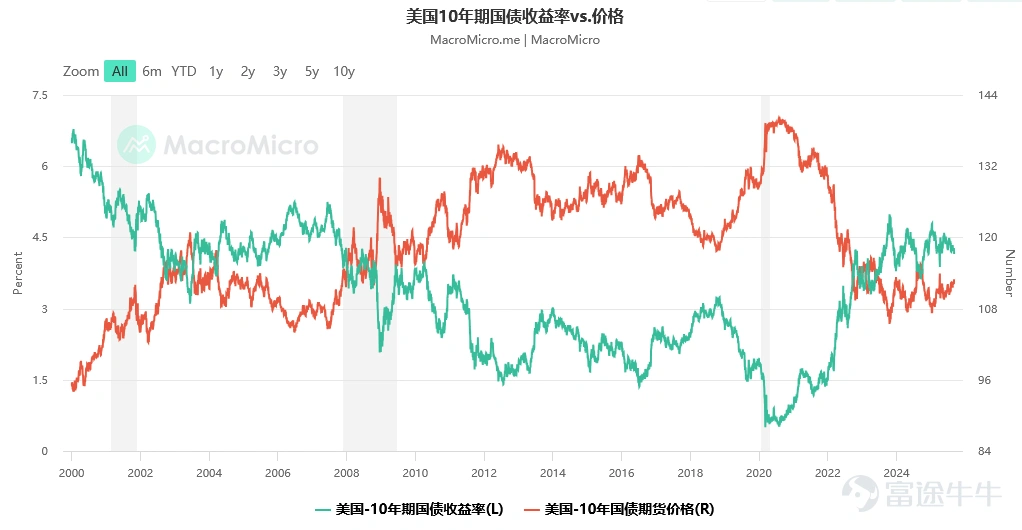

Taking U.S. Treasury bonds as an example, during the rate cut cycles of 2001 and 2007, the average yield on 10-year Treasury bonds fell by approximately 150 basis points, with prices of 10-year Treasury bonds rising by more than 20% in 2007.

Source: MacroMicro

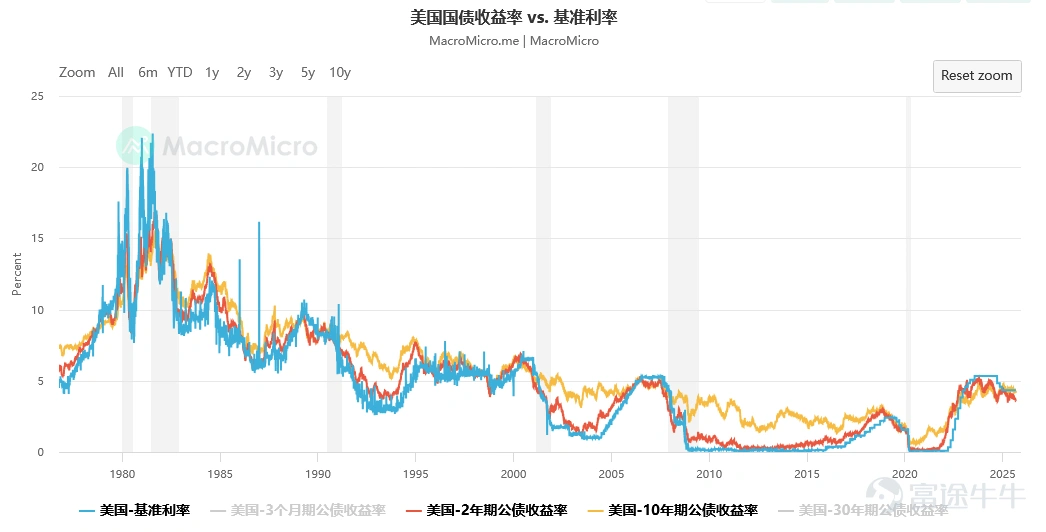

The Impact of the Term Structure: Differences Between Short-term and Long-term Bonds

The effects of interest rate cut cycles on the term structure of bonds are also noteworthy. In terms of the term structure, the yield curve often exhibits a steepening transition during rate cut cycles, with spreads widening, which further supports the performance of medium- to long-term bonds.Due to the differences in yield and price sensitivity between short-term (e.g., 1-3 year Treasury bonds) and long-term bonds (e.g., those with maturities of 10 years or more), generally speaking,in a rate cut cycle, the yield on short-term bonds tends to decline more significantly, while the prices of long-term bonds are more sensitive to changes in interest rates.

Source: MacroMicro

These two phenomena seem contradictory, but they actually stem from two different driving mechanisms.

In summary:

Magnitude of yield declineMainly driven byMarket Expectationsthe sensitivity of short-term bonds to the Federal Reserve'simmediate policy changesis greater.

Price SensitivityMainly driven byduration, long-term bonds have a greater impact on their prices due to their longer maturity in relation to changes in interest rates.Present value of principalis more significant.

For example, during the interest rate cut cycle following the burst of the Internet bubble from 2001 to 2003, the Federal Reserve reduced the interest rate from 6.5% to 1%, the yield on the 2-year U.S. Treasury bond fell from 5.0% to 1.1%, and the yield on the 10-year U.S. Treasury bond dropped from 5.5% to 3.1%, resulting in a significant increase in Treasury bond prices during the same period.

Below, we will analyze the 2-year and 10-year U.S. Treasury bonds as examples.

Why might the yield on short-term bonds (2-year) decline more significantly?

This primarily concerns"expectations"。

2-Year Treasury Bonds:Their yields mainly reflectthe market's average expectations for the Federal Reserve's policy interest rate over the next two years,which react more violently. Once expectations for interest rate cuts intensify, funds flow into short-term bonds, rapidly driving down their yields.

Long-term yields are constrained by multiple factors:The 10-year yield not only reflects interest rate expectations but also includeseconomic growth and inflation expectations(term premium). These long-term factors can offset some of the downward pressure brought about by interest rate cuts. Therefore, the decline in the 10-year yield is generally not as pronounced as that of the 2-year yield.

Why are the prices of long-term bonds (10 years) more sensitive to changes in interest rates?

This primarily concerns"price" and "risk", with the core indicator beingduration。

Duration is a measure of the sensitivity of a bond's price to changes in interest rates, which can be approximately understood as the weighted average time required to recover the principal and interest of a bond investment. The longer the term, the longer the duration.

Formula: Percentage change in price ≈ -Duration × Change in interest rate

10-year government bond:It has a longer duration (for example, possibly up to 8-9 years), assuming a duration of 9 years, and if interest rates decline,1%its price would increase by approximately9%。

2-Year Treasury Bonds:The duration is very short (approximately 1.9 years). Similarly, as interest rates decline,1%its price only rises by about1.9%。

This clearly indicates that,long-term bonds, due to their longer duration, are far more sensitive to interest rate changes than short-term bonds.

Therefore, although the volatility of the 2-year bondYieldis greater, the impact of interest rate changes on the price of the 10-yearbondis significantly stronger than that on the 2-year.

Bond selection during a rate-cutting cycle: Duration determines volatility and yield.

Market Source: Futubull

The historical trends of various U.S. Treasury bond ETFs clearly indicate that,although the overall trends are consistent, the volatility characteristics are closely related to the term structure.

Ultra-short-term Treasury bond ETFs (such as SGOV and BIL, which track 0-3 month Treasury bonds) exhibit almost no significant volatility during interest rate fluctuations, with minimal daily price changes,reflecting their high stability as cash-like assets.The underlying assets of these products have very short durations and low interest rate sensitivity, primarily demonstratingLiquidity Managementthe characteristics of instruments, with yields closely aligned to policy rates but limited capital gain potential.

As the duration lengthens, interest rate risks gradually become apparent.While 1-3 year Treasury bond ETFs (e.g., SHY) still maintain relatively low volatility, their price response to interest rate changes has increased. The volatility of bond ETFs with maturities extended to 3-7 years (IEI) and 7-10 years (IEF) has significantly risen, with a more pronounced price increase slope in a declining interest rate environment, demonstrating higher interest rate elasticity.

Notably, long-term Treasury bond ETFs (e.g., TLT, which tracks bonds with maturities exceeding 20 years) exhibit the steepest price movements during a rate-cutting cycle, with volatility significantly surpassing that of short-term products.Due to their longer duration, the capital gains effect from falling interest rates is considerably amplified, making them a powerful tool for investors speculating on declining cycles, but they also entail higher price volatility risks.

In summary, while the trends of different maturities of Treasury bonds are aligned in an expected interest rate decline environment, their risk-return characteristics are distinctly different:Ultra-short-term bonds are suitable for liquidity allocation, while medium- to long-term bonds offer greater price elasticity; the longer the duration, the more pronounced the potential volatility and returns.Investors can select bonds of varying durations based on their risk preferences and portfolio objectives to achieve asset preservation and enhanced returns during a rate-cutting cycle.

(Note: This article is based on publicly available information and historical data, and does not constitute investment advice.)

Are bonds favorable during a rate-cutting cycle?Gao Teng Asian Income Fundfocusing on Asian dollar investment-grade bonds, employing a strict diversification strategy, flexibly adjusting portfolio duration, rigorously controlling single credit risk, and pursuing stable returns across cycles.Assist you in positioning according to trends and seizing macro opportunities.

Thank you for reading this analysis on the interest rate cut cycle!This column will continue to update the Federal Reserve's interest rate cut policy trends, providing you with systematic and in-depth market interpretations based on historical patterns and current similarities and differences.

What content would you like to see next? Which indicators or data do you most want us to help interpret? Any other macro themes or investment strategy questions you care about are welcome in the comment section!

Your feedback will help us provide more focused and practical content. Looking forward to continuing the discussion with you in the next issue!

$S&P 500 Index (.SPX.US)$ $Nasdaq Composite Index (.IXIC.US)$ $Dow Jones Industrial Average (.DJI.US)$ $Hang Seng Index (800000.HK)$ $Hang Seng TECH Index (800700.HK)$$U.S. 2-Year Treasury Notes Yield (US2Y.BD)$$U.S. 10-Year Treasury Notes Yield (US10Y.BD)$$iShares 0-3 Month Treasury Bond ETF (SGOV.US)$$SPDR Bloomberg Barclays 1-3 Month T-Bill ETF (BIL.US)$$iShares 1-3 Year Treasury Bond ETF (SHY.US)$$iShares 3-7 Year Treasury Bond ETF (IEI.US)$$iShares 7-10 Year Treasury Bond ETF (IEF.US)$$iShares 20+ Year Treasury Bond ETF (TLT.US)$

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

13

17