PCE meets expectations! Can U.S. stocks start strongly in September?

Tensi Interest Rate Cut Cycle Analysis | How did the main assets go in the 7 interest rate cut cycles since 1980?

Since September 2024, the Federal Reserve began its first cycle of cutting interest rates in 4 years, marking a shift in MMF policy from austerity to easing. Currently, market expectations for interest rate cuts in September 2025 are heating up.According to the CME FedWatch tool, the probability of cutting interest rates by 25 basis points in September is 87.3%, and the probability of cutting interest rates by 50 basis points in October is 42.9%.

A cycle of interest rate cuts refers to a period in which the federal funds rate is continuously lowered by at least 50 basis points (bp) from its peak, usually in response to a recession, slowing inflation, or financial crisis.

Does cutting interest rates equal a bull market? Who will perform better, stocks, Bonds, or gold? The answer is no simple yes or no; the reason for cutting interest rates is far more important than the act of cutting interest rates itself. This article reviews the Federal Reserve's seven-round interest rate cut cycle from 1984 to 2019, analyzes the background of interest rate cuts, the economic environment and the performance of major assets, explores the implications of historical experience for the current cycle, and looks forward to the potential impact of the interest rate cut in September 2025.

Review of previous interest rate cut cycles (1984-2019)

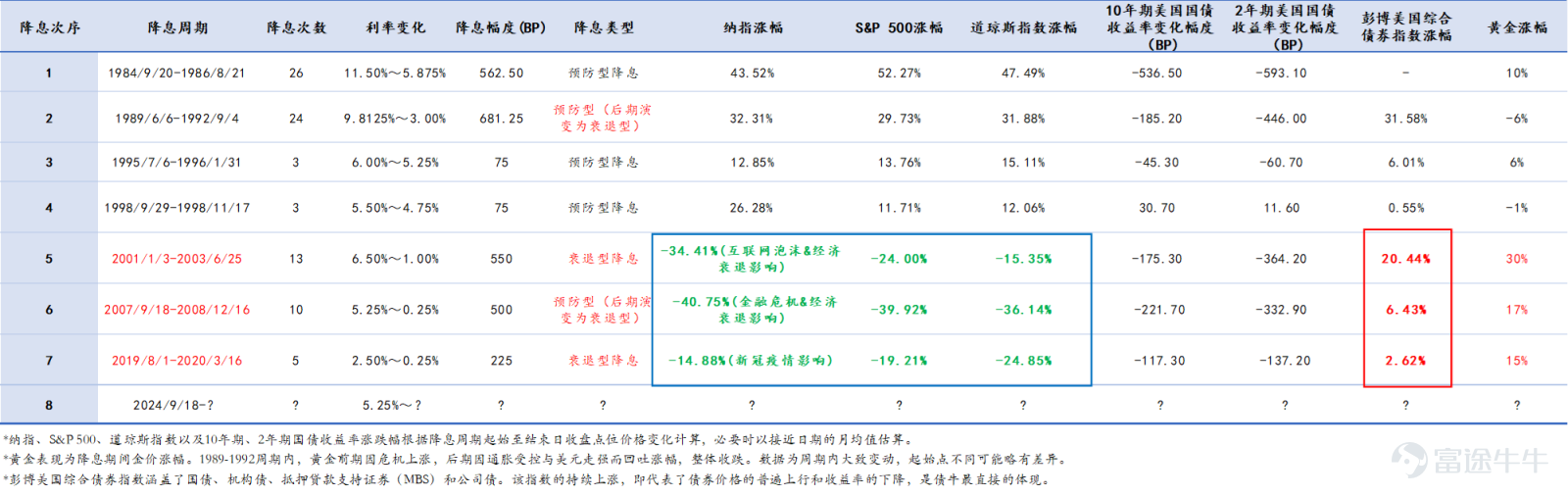

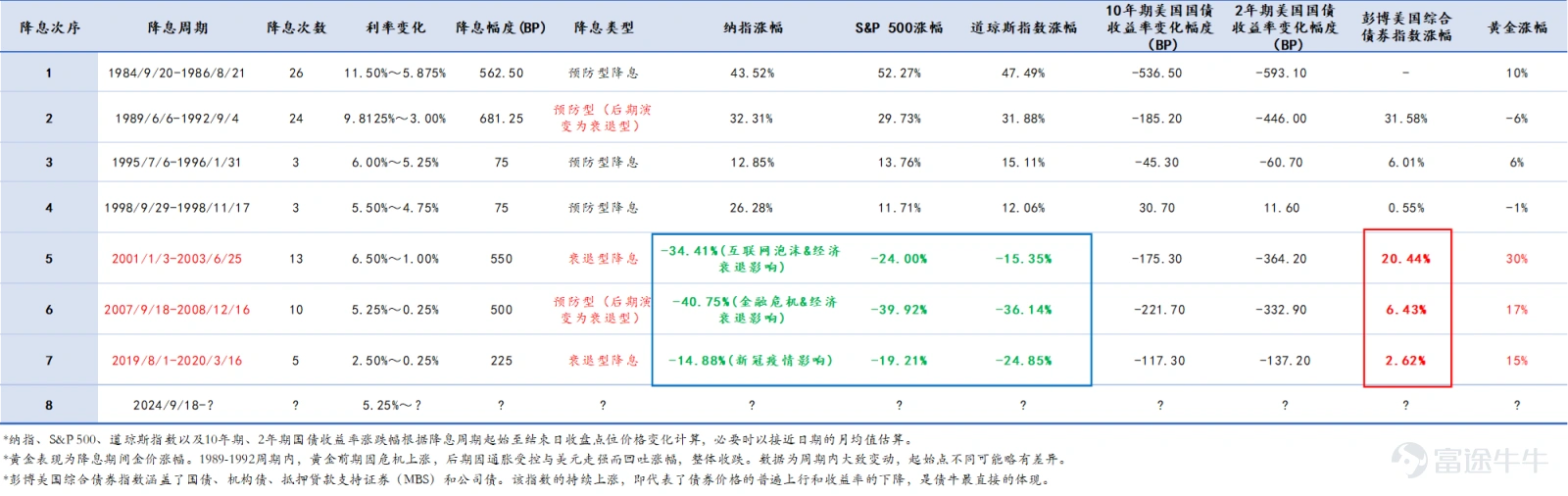

Since 1984, the Federal Reserve has experienced a total of 7 major interest rate cuts. Most cycles have continued for more than 1 year, and interest rate cuts have exceeded 500 basis points (bp).Interest rate cuts are generally divided into recessionary (dealing with economic recession) and preventive (avoiding potential risks).

Preventive interest rate cuts are a forward-looking operationTake the initiative when the economy is not in recession but growth momentum is slowing down and downside risks increase. Usually accompanied by low inflation or downward pressure on inflation expectations, there may be a risk of “potential deflation”, but there has been no widespread price decline.The aim is to prevent future recessions, and the management is “anticipation.”

Recessionary interest rate cuts are a reactive operationRespond passively when the economy has already fallen into recession, GDP continues to grow negatively, the unemployment rate rises sharply, and the data deteriorates across the board.The aim is to mitigate the current crisis, and the response is “reality.”

If prevention fails, the former will evolve into the latter.

The following is an overview of the background and Assets performance of each cycle:

Throughout history, Assets performance in interest rate cut cycles has been highly dependent on the motivation to cut interest rates (preventive vs. recessionary). In the past seven interest rate cut cycles,There were four “recession-type interest rate cuts”(From “preventive” to “recessionary interest rate cuts” in 1989-1992 and the latter half of 2007-2008),“Recessionary interest rate cuts” are often accompanied by large and frequent interest rate adjustmentsThe main Assets trend is also different from “preventive interest rate cuts.”

Overall, in preventive interest rate cuts, asset performance is more positive, and stocks and Bonds often return positively; in recessions, Bonds and gold perform prominently as safe-haven assets, and stocks fluctuate greatly.

The bond market: the direct beneficiary of falling interest rates

In successive interest rate cut cycles, interest rate cuts often benefit Bonds, that is, bond yields have declined sharply and prices have continued to rise.In addition to the fourth rate cut (September to November 1998), US 10-year and 2-year Treasury yields rebounded,In several other interest rate cut cycles, 10-year/2-year US Treasury yields all fell sharply, and the US Composite Bond Index showed a sharp rise, indicating favorable Bonds.

Its core mechanism isThere is an inverse relationship between Bonds prices and yields: When the Federal Reserve cuts interest rates, the market benchmark interest rate falls, and the coupon interest rate for newly issued Bonds falls, making existing high-interest Bonds more attractive, thus boosting their prices. Judging from the pricing model, the price of a Bonds can be expressed as the sum of the present value of future Cash/Money Market flows. A decrease in yield will directly increase the present value and drive up the price.

The specific situation varies by type:In preventive interest rate cuts (such as 1995-1996), the economy achieved a “soft landing”, inflation was controlled, 10-year and two-year US Treasury yields declined slightly (average 50 bps), and the US composite Bonds index rose by 5%-10%.In 1998, before interest rate cuts, US 10-year Treasury yields had already declined, and the US GDP growth rate improved in the 3rd quarter compared to the same period, so medium- to long-term interest rates rebounded during this short round of interest rate cuts.

In recession-type interest rate cuts (such as the 2001-2003 Internet bubble), economic uncertainty increased, capital poured into Bonds to take refuge, driving a sharp decline in yield (average 250 bps), and the US composite Bonds index could rise by about 20%.For example, in 2008, the yield on 10-year treasury Bonds fell from 4% to 2%, and bonds became a “safe haven.”

Stock market: prevention means rise; recession means decline

Interest rate cuts usually stimulate the stock market by reducing borrowing costs and raising corporate profit expectations. If you take stock of the previous interest rate cut cycles, you can findThe performance was optimistic during the “preventative interest rate cut”. All three major stock indexes recorded positive increases, and the increases were significant.Among them, despite the short cycle in 1998, the NASDAQ rose 26.28%, showing the resilience of the technology sector with improved liquidity expectations.

Recessionary interest rate cuts occur when the economy is already in recession or has experienced major external shocks. Despite the drastic easing of MMF policy, it is still difficult to offset the negative effects of the economic downturn and the deterioration of corporate profits.The stock market performed poorly when the US economic recession was severe or affected by a sudden crisis. Among all recession-type interest rate cuts, the stock market fell significantly.The S&P 500 fell between 19.21% and 59.92%, and the NASDAQ fell between 14.86% and 40.75%. The S&P 500 fell nearly 60% during the 2007-2008 financial crisis, one of the worst stock market recessions in modern times.

Gold: Real interest rates and risk aversion jointly drive the price of gold

Gold's overall performance is good, as a safe-haven Assets,Gold is stronger in a recession-type interest rate cut cycleThe average increase was around 20%, fluctuating slightly under “preventive interest rate cuts,” but there are still downside risks.

Case Study: 1995 Interest Rate Cut Cycle - A Classic Example of the Federal Reserve's “Soft Landing”

From July 1995 to January 1996, the Federal Reserve implemented a six-month cycle of cutting interest rates, cutting interest rates a total of three times. The federal funds rate was lowered by a total of 75 basis points (bp), from 6% to 5.25%. The Federal Reserve then kept interest rates stable for over a year until it raised interest rates in March 1997. 1995 was a mid-cycle preventative interest rate cut. GDP grew by 3.5%, unemployment was 5.6%, and inflation was 2.8%. The economy was strong but faced the risk of slowing growth.

This round of interest rate cuts was viewed as a model for a “soft landing,” which not only avoided a recession but also controlled inflation. The economy has reached a soft landing, GDP continues to grow, unemployment is stable, and inflation is under control.Assets trends are positive, stocks benefit from a low interest rate environment, moderate Bonds, and a mix of Commodity.

Stocks:The S&P 500 returned 21.4% for 12 months (calculated after the first rate cut). Trend: Slight initial fluctuations, then a strong rise, benefiting from the start of a bull market in technology stocks (the rise of the Internet) and improvements in corporate profits. There are no recessionary fears, and market confidence is high.

Bonds:The 10-year Treasury yield fell from 6.03% to 5.58%, and the price rose but was limited (due to stable inflation expectations). Trend: Moderate and positive returns in the first half of the year, then stable; Bonds are safe haven, but interest rate cuts are small, and returns are not as high as during the recession period.

Commodity: Gold:The increase in the price of gold was moderate, only 6%. After interest rates were cut, the growth rate of the US economy began to pick up, the unemployment rate fell, and the price of gold subsequently fell.

WTI Crude Oil:Price change +15% during the period (from $17/barrel to $19.5/barrel). Trend: Stable demand, OPEC supply control, moderate rise; energy stocks benefit.

Preventive cyclical assets have positive returns, and stocks lead (on average higher than recessions), reflecting rising risk appetite. There was no major collapse in 1995, and the market benefited from interest rate cuts, which continued the bullish market in the 1990s.

Prospects for 2025 interest rate cuts: a cautious shift in a data-dependent model

Currently, some analysts believe that the state of the US economy is somewhat similar to the preventive interest rate cut cycle of 1995.The core inflation rate has gradually declined to 2.9%. Although it is still higher than the Fed's long-term target of 2%, it is showing a steady downward trend. The unemployment rate remained at 4.2%. Although slightly above recent lows, it is still at an historically low level. The real GDP growth rate remained in a moderate range of 1.5% to 2.3%, indicating that the economy may be evolving towards a “soft landing,” without the typical characteristics of a recession. Furthermore, Federal Reserve Chairman Powell released a “dovish” signal at the Jackson Hole annual meeting last week, boosting market optimism about the shift in MMF policy.

However, history does not simply repeat itself.Compared with 1995, the current economy faces several structural differences: the size of federal government debt is at a historically high level, geopolitical conflicts continue to disrupt the supply chain, there is still uncertainty about the sustainability of falling inflation, and some market participants are concerned that the US economy may face the risk of “stagflation.” Furthermore, there are significant signs of overinvestment in fields such as artificial intelligence. OpenAI CEO Sam Ultrman has warned many times that the current AI investment climate has similar characteristics to the internet bubble in the late 1990s, reflected in high valuations, a massive influx of capital, and a surge in the number of startups. Although he acknowledged the groundbreaking significance of AI technology, he also pointed out that irrational investment could trigger adjustments.

In this complicated context, it is expected that the Federal Reserve's path of cutting interest rates will be more cautious.Any sign of a recovery in inflation or weakening employment or growth data that exceeds expectations may trigger a reassessment of MMF policy and may lead to significant fluctuations in financial markets.

(Note: This article is based on public information and past data, and does not constitute investment advice.)

[Column preview]

Thank you for reading this article on the interest rate cut cycle analysis!This column will continue to update the trend of the Federal Reserve's interest rate cut policy, and provide you with a systematic and in-depth market interpretation based on historical rules and current similarities and differences.

What would you like to see next? What Indicators or data would you most like us to help interpret? As well as other macroeconomic topics or investment strategy questions you are concerned about, please leave a message in the comments section!

Your feedback will help us deliver more focused and useful content. We look forward to continuing the discussion with you in the next issue!

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment

12

8