Each generation has its own "Moutai"! The "three sisters of new consumption" in the Hong Kong stock market have been hitting new highs repeatedly, what other opportunities are worth capturing?

Each generation has its own 'Moutai'!

This year, the new consumption sector in the Hong Kong stock market has shown a strong trend, becoming the focus of market attention.

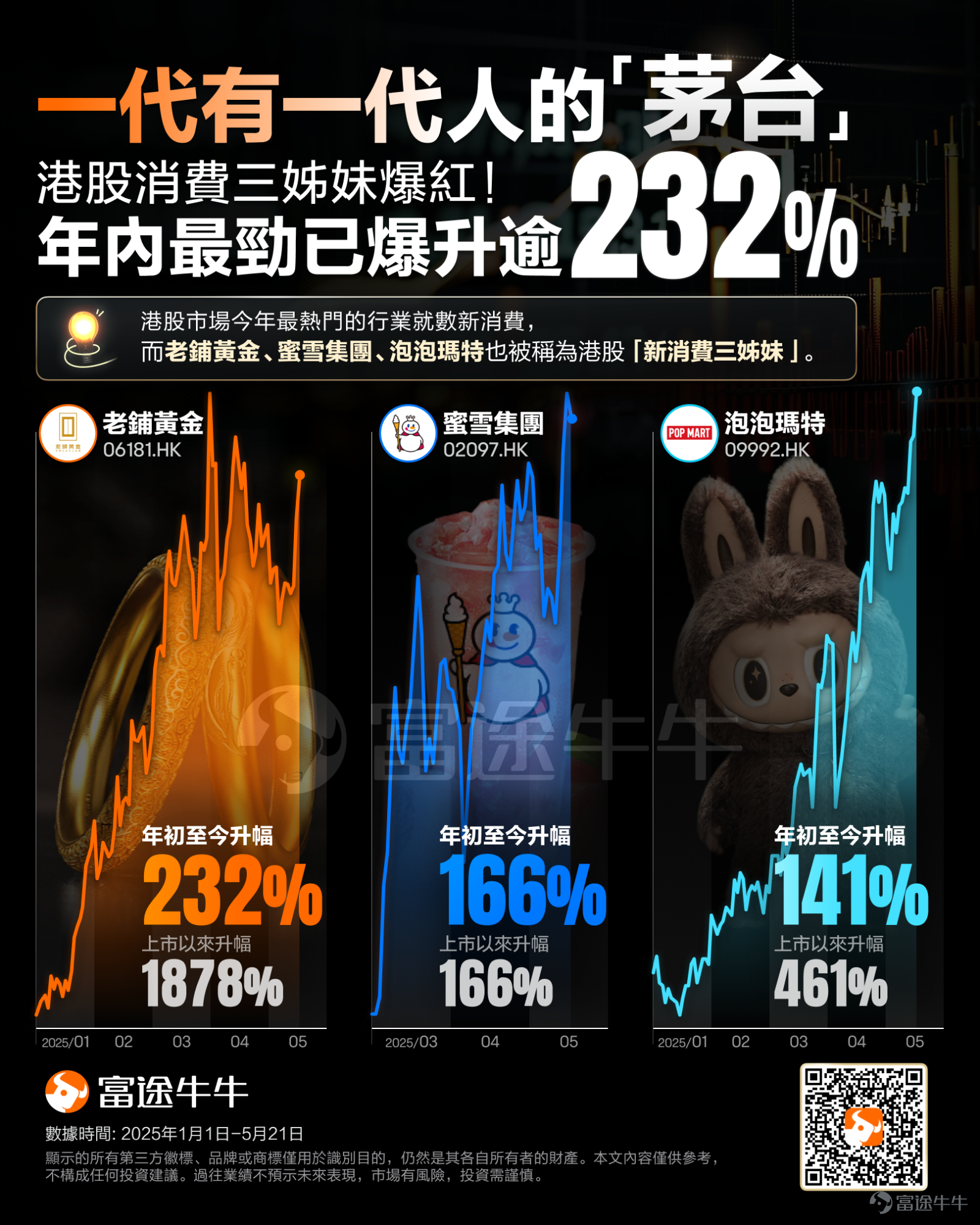

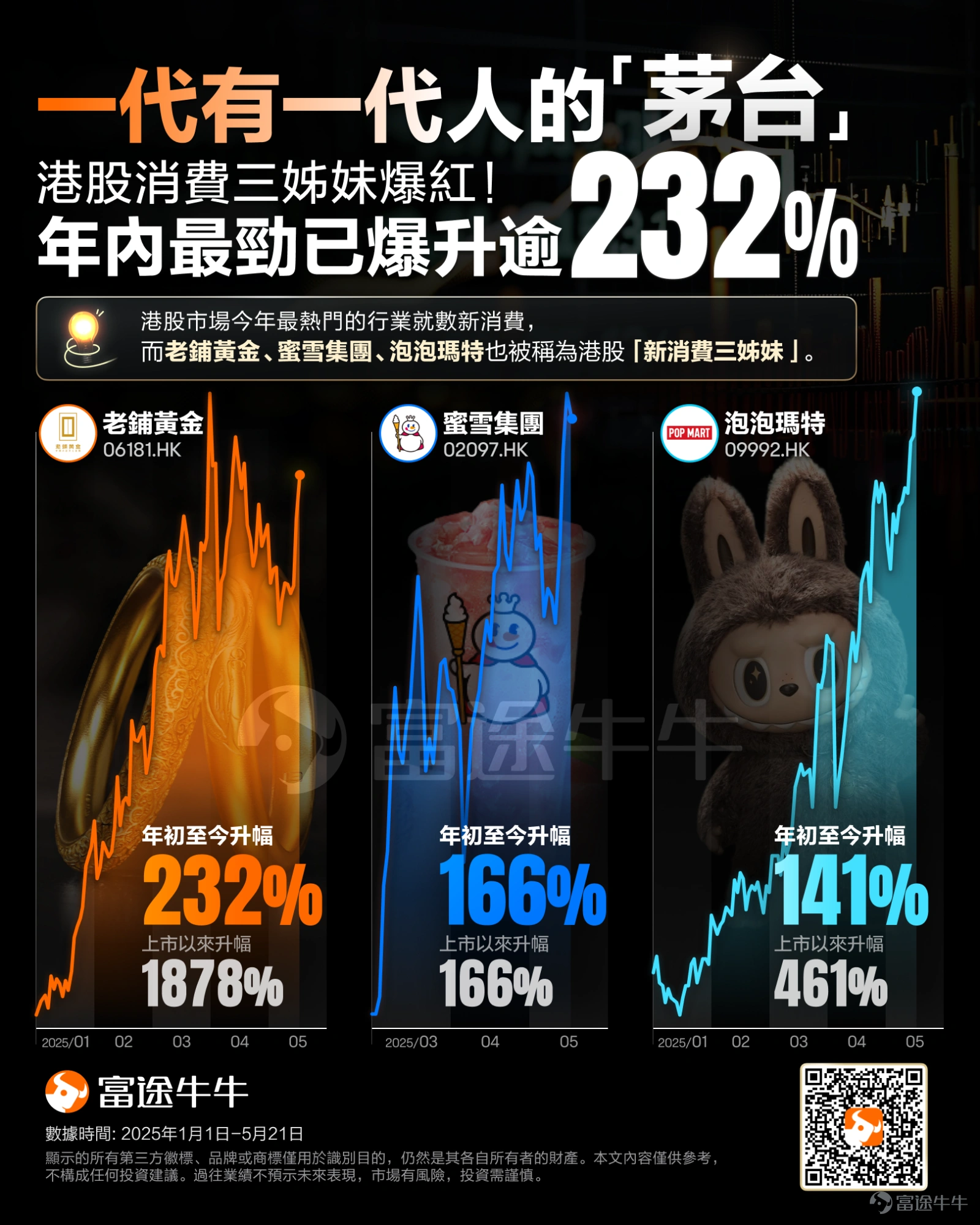

Among them, $MIXUE GROUP (02097.HK)$ 、 $POP MART (09992.HK)$ 、 $LAOPU GOLD (06181.HK)$ It is even hailed by the market as the 'Three Sisters of New Consumption' in Hong Kong stocks. These three companies have led a group of new consumption stocks to repeatedly create new highs this year, with Lao Pu Gold increasing by over 232% this year, and Mijiu Group and POP MART both increasing by over 140%.

The investment logic of emerging consumer bull stocks is increasingly pointing to the same key word -Emotional value.

In recent years, new consumption characterized by emotional value and self-satisfaction has risen, reflecting the changes in consumer habits and the diversification of consumption demands.Consumers are no longer satisfied with just the basic functions of Commodities; they are beginning to place greater emphasis on the emotional experiences and satisfaction derived from the consumption process.

The media states that buying a cup of 'happy lemon water' provides joy through blind box socialization, fulfilling the 'self-satisfaction' needs for personalized expression and significant collectible value in Gold. Clearly, emotional resonance brings product premium.The emotional consumption of young people has restructured the valuation logic of companies.In the consumption market, the saying 'whoever gains young people gains the world' is undoubtedly an eternal truth.

What other new consumption Concept stocks are worth paying attention to?

Wu Yuanyi, the manager of the GF Value Core Fund, stated,In the New consumption Sector, new consumption models are emerging in various fields, such as the "grain economy" and the rise of domestic consumption goods, highlighting the transformation and progress in the consumer domain driven by the development of the times.

Jiang Weihua, the manager of the Yongying Emerging Consumption Smart Selection Fund, stated thatEach era has its own enterprises.Companies that are proactive and can identify unmet consumer demands will always be rewarded by the market. The demand for many traditional consumer goods has been relatively well met, while the demand gaps for self-pleasing products remain significant, and we maintain a positive focus on these new areas.

Futu News has整理了一些新消費公司的 港股市場部分,为投资者参考:

Among them, the grain economy includes $POP MART (09992.HK)$ 、 $BLOKS (00325.HK)$ 、 $MNSO (09896.HK)$ ; Beauty care includes $MAO GEPING (01318.HK)$ 、 $GIANT BIOGENE (02367.HK)$ 、 $CHICMAX (02145.HK)$ ; Traditional gold ornaments include $LAOPU GOLD (06181.HK)$ ; Dining, tea drinks, etc. include $MIXUE GROUP (02097.HK)$ 、 $GUMING (01364.HK)$ 、 $CHABAIDAO (02555.HK)$ 、 $NAYUKI (02150.HK)$ 、 $AUNTEA JENNY (02589.HK)$ 、 $WL DELICIOUS (09985.HK)$ 、 $GUOQUAN (02517.HK)$ 、 $DPC DASH (01405.HK)$ ; New energy vehicles include $XIAOMI-W (01810.HK)$ 、 $LI AUTO-W (02015.HK)$ 、 $XPENG-W (09868.HK)$ 、 $NIO-SW (09866.HK)$、 $LEAPMOTOR (09863.HK)$Wait.

It is worth noting that most companies have achieved good gains this year, apart from the three consumption sisters in the Hong Kong stock market. Gu Ming and Blueco have risen over 160%, Wei Long Wei Wei has increased by 125%, and Shangmei Co., Ltd. has surged over 100%.

What do Institutions think?

According to an article from the Securities Times, foreign investment banks are also bullish on the future prospects of the 'new consumption three sisters' in the Hong Kong stock market. The new consumption track is welcoming structural opportunities, and leading companies that align with the 'emotional consumption' theme and have enhanced brand strength and competitiveness are favored by the market.

Morgan Stanley's latest research report raised the target price of POP MART to HKD 224.Corresponding to this year.Forecasted PE.Approximately 40 times, 30 times next year, and a 'Shareholding' rating has been given. Morgan Stanley analysis identifies three major reasons:

First, LABUBU 3.0 global demand is strong, especially in the American market, and it is believed this can promote POP MART to open new stores in the United States and other regions, becoming the main growth driver for this and next year; second, POP MART's supply chain in Vietnam has been quickly established and is performing well, with most goods exported to the United States expected to be shipped from Vietnam in the third quarter of this year, helping to mitigate the impact of cooling China-U.S. trade relations; third, new products in the U.S. have seen price increases of 12% to 27%, and this seems to be accepted by consumers, which could increase the average product price and, in the long run, improve profit margins in the U.S. business.

Daiwa released a report initiating coverage of MIXUE Group, giving a target price of 539 HKD and a 'Outperform' rating.Bullish on its growth prospects, mainly based on economies of scale, leading position in the mass market, and overseas expansion potential. Daiwa expects its same-store sales growth for 2025-2027 to be 5%, 3%, and 3% respectively, with Net income growth year-on-year of 22%, 20%, and 18%. Competition in the takeout platform is advantageous for MIXUE Group's same-store sales growth, with an expected increase of over 10% in same-store sales in April, supporting recent stock prices.

Regarding Lao Pu Gold, recently Goldman Sachs issued a report stating thatLao Pu Gold's management is confident in achieving a long-term goal of over 1 billion yuan in total commodity transaction volume (GMV) per store.This means it is more than double the 0.259 billion yuan level in 2024 and exceeds the nearly 0.5 billion yuan GMV level per store of global luxury brands, including Hermès, in 2023.

The firm raised Lao Pu Gold's Net income forecast for 2025 to 2027 by 23% to 45%, mainly reflecting its management's optimistic expectations for sales prospects. Management expects sales to grow more than double year-on-year in the first quarter of this year, and the firm expects that the company will receive further support from new stores in first-tier cities, partially offsetting the impact of declining gross margins and employee stock ownership plan costs. The firm raised Lao Pu Gold's target price from 553 HKD to 976 HKD, maintaining a 'Buy' rating.

Hong Hao pointed out that HK stocks are expected to reach new highs in the third quarter.In terms of national policy support, as well as their own profit growth and valuation, the Technology, Consumer, and Medical sectors are relatively the most attractive sectors.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (9)

to post a comment

56

28