NDX and XND usage scenarios

In the first part, we discussed why the NASDAQ 100® Index (NDX) and NASDAQ 100 index options (NDX and XND) are attracting a lot of market participants. Next, we will explain the differences between NDX and XND index options and provide examples of some applications of these tools.

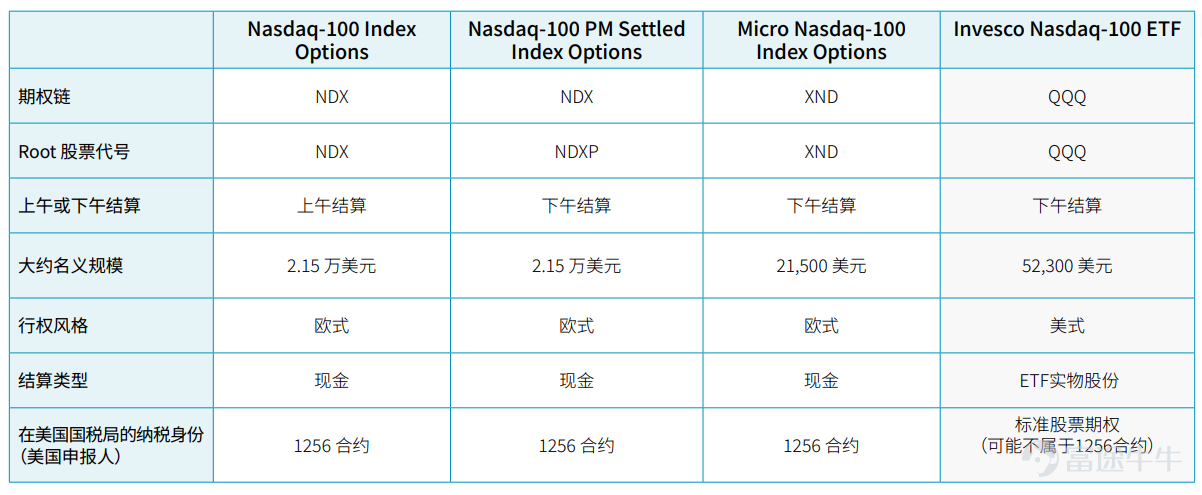

NDX, XND, and QQQ

We revisit the key differences between major options products linked to NDX in the table below.

Key Points

NDX(P) and XND index options belong to European options, using cash settlement, may enjoy preferential tax treatment. Therefore, NDX(P) and XND cannot be exercised or transferred before expiration. If index options are held until expiration and have intrinsic value, the amount will be settled in cash to the holder's account. Lastly, for US taxpayers, index products usually enjoy preferential tax treatment (1256 contracts), so option profits may be subject to a lower blended tax rate.

Standard stock options and ETF options are American options, settled physically at expiration, usually not enjoying preferential tax treatment. Therefore, short options can be transferred at any time on or before the expiration date. According to options clearinghouse data, approximately 6% of options are exercised before the expiration date. This is usually done for managing balance sheet assets or for obtaining dividends. In such cases, the seller of (Call) options will ultimately sell 100 shares of the underlying ETF for each option being assigned and be responsible for paying the quarterly dividends. Finally, the gains from stock options (held less than 365 calendar days) are usually taxed at the taxpayer's income tax rate (higher bracket).

Understand nominal exposure.

NDX(P) and XND are both index products designed to track the performance of NDX. In other words, if the value of NDX increases (or decreases) by 1% on a given day, the value of NDX(P) and XND should also increase (or decrease) by 1% accordingly. The difference lies in the nominal value of each index and the nominal value of the exposure generated. Let's first understand how these two are interrelated.

All derivative contracts involve leverage. For options, leverage comes from the contract multiplier. All standard index (and stock/ETF) options control 100 units of the underlying index or security. More specifically, the buyer has the right to buy/sell the underlying index/security at a specific (exercise) price. Based on the exercise price and contract multiplier, we can calculate the nominal exposure of the contract.

Let's start with stocks as an example, then move on to two indices.

The trading price of stock XYZ is $60 per share.

• The trading price of the XYZ call option with a strike price of $60 is $1.50.

• The notional exposure embedded in the XYZ call option with a strike price of $60 is $6,000, as the buyer has the right to buy 100 shares of XYZ stock at $60 per share.

• Nominal Value = Strike Price * Contract Multiplier

Alternative solution

• To buy 100 shares of XYZ stock at $60 per share, it would require $6,000.

• Buying a call option with a strike price of $60 at a price of $1.50 would involve paying a premium of $150. The notional exposure within the option contract period would be $6,000.

• Compared to other major U.S. stock indices, the value of NDX is relatively high.

• If the NDX is at 21,500 points (value), the nominal value of an at-the-money option (strike price at 21,500) would be $2.15 million. NDX index options investors can control approximately $2.15 million of notional exposure with one option.

The NDX is reported at $21,500:

• The trading price of NDX call options with a strike price of $21,500 is $15

• The nominal exposure embedded in call options with a strike price of $21,500 is $2.15 million, as the buyer controls 100 NDX at a price of $21,500 per unit • Nominal Value = Strike Price * Contract Multiplier

The high value of the NDX provides end users with a significant nominal exposure, leading to a high leverage options market.

XND is a mini index product equivalent to one percent of the standard index value. Therefore, if the value of NDX is $21,500, the value of the Micro Nasdaq 100 Index (XND) is approximately $215 (21,500/100 = 215). With greater flexibility in nominal exposure, XND provides an effective way to capture trends in NDX price movements.

For investors interested in the unique characteristics of index options, smaller indices are more accessible and require a smaller allocation of capital. Many market participants do not need a nominal exposure of $2.15 million, and XND helps meet the needs of these investors.

• The trading price of XND call options with a strike price of $215 is $0.15

• The nominal exposure embedded in call options with a strike price of $215 is $21,500, as the buyer controls 100 XND at a price of $215 per unit

• 名义价值 = 行权价 * 合约乘数

XND的假设使用场景

XND 指数期权是灵活的投资工具,使用方式与其他股票期权或指数期权相同。无论是为了潜在投资组合保护、收益率提升还是方向性风险敞口,都可以使用 XND 指数期权来实现。

假设的投资组合保护

假设有位投资者拥有一个业绩表现与 NDX 指数类似的投资组合(即相较基准NDX指数,该投资组合的贝塔值较高)。在过去几年中,该投资组合的价值可能已经大幅增长。举例来说,假设投资组合价值约为 25,000 美元。该投资者倾向于持有其投资组合,但担心市场可能出现回调。

这种情况下,可以考虑微型指数期权产品,例如 XND。

继续前例,假设这名投资者一直在为购房首付款存钱,快要实现储蓄目标,但如果其投资组合价值损失了 20%,那将是一个重大打击。

鉴于XND 指数期权的目前名义保障规模(约 21,500 美元),该投资者可能倾向于持有单一看跌期权价差策略。一张价差期权有可能抵御该 投资组合中的大部分不利市场波动。许多参与者选择看跌期权价差策略是为了降低入市成本,因为在六个月的时间里,跌幅超过 20% 的情 况并不多见。对于这种规模的投资组合而言,名义敞口较大的产品保障数额太大。

In this case alone, potential homebuyers may purchase a 215/172 put option spread strategy expiring within 180 days.

The exercise price of 172 is 20% lower than the current value of the index.

The spread is 6.50. The position requires a payment of 650 US dollars plus any friction costs.

Considerations in different scenarios

Perhaps over the next few months, the market will continue to rise. Assuming the NDX index rises by 5% in the next 180 days, the put option spread strategy will lose value at expiration. However, the portfolio may still earn approximately 5%, i.e. $1,250 (25,000 * 1.05). Taking into account the worthless put option spread, investors may still profit over the 6-month period ($1,250 - 650) $600.

Assumed Outcome: Portfolio value is approximately $25,600

Perhaps the investor's intuition is correct, and the market will experience a sell-off over the next six months. Assuming a 15% market decline, the stock portfolio will lose around $3,750 (decreased by 15%). This is where the hedging strategy shines. In this scenario, XND drops from 215 to 182.75 at expiration, a spread of 32.25, settled in cash. In US dollars, the value of one spread option is $3,225. They paid $6.50 for this protection. Therefore, after deducting the initial cost, their option hedge profit is (32.25 - 6.50) $25.75 ($2,575).

Assumed Outcome: Portfolio value is approximately $23,825

Thanks to index options hedging, the account value only decreased by 4.5% ($1,175), instead of losing 15% ($3,750) due to a stock pullback.

Lesson: Index options hedging strategies can allow investors looking to protect capital to rest easy. Depending on the end user's needs, various methods can be used to implement a hedging strategy. Ultimately, the intention of a hedging strategy is to offset losses. This concept may seem counterintuitive to investors.

Your primary asset is your capital base. The goal is for your capital base to grow over time. Hedging strategies can be actively or passively deployed, but the motivation is to limit the risk exposure caused by significant market downturns. In short, holding hedging tools does not necessarily mean wanting to understand how they operate.

Return on Investment Increase

We continue with the hypothetical investor previously mentioned, whose portfolio value is $25,000 and highly correlated with the NDX—however, this time, the investor hopes to increase the ROI within a specific period. By a simple calculation, assuming the investor's portfolio consists of non-dividend-paying growth companies (many growth companies do pay dividends).

Index options overlays can be used to boost the portfolio's ROI. Many individual and institutional investors adopt a tactical strategy of selling call options on index options to generate income. As index options expire every day throughout the year, the time horizon differences are significant. Generally, ROI increase strategies involve options with at least one month (or longer) until expiration.

Assumptions

• A portfolio with a higher beta value compared to XND

Stock value = $25,000

Strategy: Sell a 5% out-of-the-money call option expiring in one month, which may potentially increase the portfolio's return. Example: Sell a 30-day 5% OTM call option.

For example, selling a 5% out-of-the-money call option expiring in 30 days.

If XND is at 215, hypothetically an investor sells a one-month to expiry call option on XND with a strike price of 227.

Receiving approximately $1.00 in premium (assuming a volatility trading at around 17%). This could happen monthly.

Considerations in different scenarios

Ideally, the basket of stocks / indices should have a growth slightly lower than 5% during the expiration period. In this scenario, the long stock position can be profitable, and the short call option would expire out-of-the-money (worthless), allowing the investor to realize the entire premium. If done monthly (which is highly unlikely), the yearly call writing strategy might potentially increase the overall portfolio performance by around 500 basis points (or 5%).

(Assuming that out-of-the-money Call options rise by 45 basis points per month, a total of 12 times).

In a market of sustained narrow fluctuations, implementing a Call option writing strategy can also increase the portfolio's ROI. However, in this case, the value of the stock has not increased. According to our previous assumption, the Call option writing strategy may have a similar impact (around 500 basis points).

If the index (along with a basket of stocks) continues to decline, implementing Call options writing can partially mitigate the downturn, but it is limited to the premium received. If the loss in security value exceeds the proceeds from selling options, the net performance will be negative. However, its performance will be better than not using the Call option writing strategy.

In a market where the index continuously breaks through the exercise price (+ received premium), the Call option writing strategy on the index will underperform, as the short options cap upside participation during the existence period.

Understanding when short index Call options perform well and when they do not is crucial. Short index Call options perform well in declining markets, narrow fluctuations, or slight uptrends. In a sustained strong bull market, the performance of short index Call option strategies is subpar.

Directional Risk Exposure

Directional risks associated with index options are almost identical to directional risks associated with stock options or ETF options. Similar to other options markets, you can use various index option strategies to reflect bullish, bearish, or neutral views. The only differences lie in settlement, style, and potential tax implications.

As mentioned earlier, index options are not exerciseable or assignable before expiry. More importantly, at expiration, all in-the-money (ITM) options will be cash-settled. In contrast, long Call/Put strategies using stock/ETF options will convert to long/short positions in the underlying security at expiration. The final distinction is in taxation. We have emphasized the potential benefits of index options for U.S. taxpayers.

Conclusion

The use of mini index options like XND is no different from how market participants operate stock options and ETF options. These options are often deployed to hedge existing price risks (or portfolio risks) and can also serve as a means to enhance potential portfolio returns. Furthermore, index options are also commonly used to express directional expectations for market leveraged operations within specific time periods.

The recent growth of these products is closely related to the availability of daily options, enabling end users to apply option strategies and express their market views in a more refined time granularity.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

3

5