騰訊Q3毛利上漲16%!後市你點睇?

What are the highlights of Tencent?

At the 11th Hong Kong Top 100 Awards Ceremony, the "Stock King" won multiple major awards. $TENCENT (00700.HK)$ On November 13, after the Hong Kong stock market closed, the highly anticipated third-quarter financial report was released.

The profit performance of the stock king in the third quarter seems quite impressive, but it actually met the expectations of BofA, CICC, and other investment banks. In the trading on November 14, investors showed a cautious and optimistic attitude. Tencent's stock price fell by 0.10%, but compared to the 1.96% drop in the Hang Seng Index and the 3.08% drop in the Hang Seng Tech Index, the overall performance still stood out.

Caihua Society will analyze the third-quarter financial report of the Stock King for readers from seven main points.

Overall: Significant improvement in quarterly profit margin.

In the third quarter of 2024, Tencent's revenue growth was less than double digits, increasing by 8.13% year-on-year, reaching at least 167.193 billion yuan. However, the non-GAAP operating profit achieved double-digit growth, increasing by 18.59% year-on-year to 61.274 billion yuan. The non-GAAP attributable net income to shareholders also surged by 33.15% year-on-year to 59.813 billion yuan, reflecting an improvement in the profitability of its continuing operating business.

Starting from the third quarter of 2024, Tencent will rename network advertising to marketing services to better reflect the wide range of marketing solutions and supporting technical services provided by its online marketing platform.

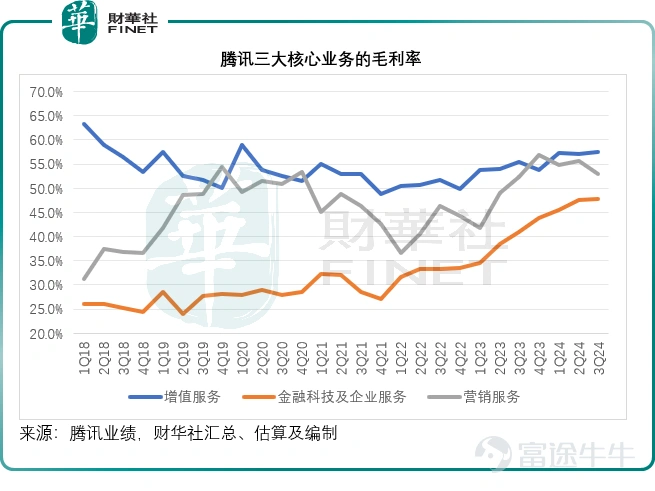

Caihua Society noted that Tencent's three core reporting segments—value-added services, fintech and enterprise services, and marketing segments—saw an increase in gross margin in the third quarter of 2024 compared to the same period last year, with increases of 2.0 percentage points, 6.9 percentage points, and 0.7 percentage points respectively.

By division, the gross margin of value-added services is 57.5%, up 1.9 percentage points year-on-year, mainly due to the increased proportion of high-profit service revenue, along with the improved profitability of music and long video business, as well as the relatively low proportion of low-profit live streaming revenue.

The gross margin of marketing services has increased to 53.0%, rising by 0.7 percentage points year-on-year, mainly driven by the growth in high-profit video account and WeChat search advertising revenue.

The gross margin of fintech and business services increased to 47.8%, up 6.9 percentage points year-on-year, mainly due to the improved cost efficiency of cloud business, growth in wealth management service revenue, increased e-commerce technical service fees, enhanced monetization of enterprise WeChat and other business services.

In terms of operating expenses, in the third quarter, sales and marketing expenses were 9.411 billion yuan, up by 19.0% year-on-year, mainly due to increased promotional and advertising expenses for new games in domestic and international markets; research and development expenses were 17.89 billion yuan, up by 8.7% year-on-year, mainly driven by investments in strategic areas including AI, with the R&D expenses as a percentage of revenue rising from 10.6% in the same period last year to 10.7%.

The non-GAAP net profit attributable to shareholders' expanded to 35.77%, compared to 29.05% in the same period last year and 35.57% in the previous quarter.

Additionally, capital expenditures in the third quarter significantly increased, rising by 113.54% year-on-year to 17.094 billion yuan. Management revealed that operating capital expenditures were 14.7 billion yuan, up by 122% year-on-year, mainly allocated for GPU service investments. Non-operating capital expenditures were 2.4 billion yuan, up by 74% year-on-year, mainly used for CIP.

Highlight one: Gaming

In the third quarter of 2024, Tencent's international gaming revenue was 14.5 billion yuan, up by 9% year-on-year; domestic market gaming revenue increased by 14% year-on-year to 37.3 billion yuan.

Tencent's Chief Strategy Officer James Mitchell's views on the gaming industry: Whether overseas or domestically, the industry's scarcest resource is everlasting games, while the competition in the new game track is becoming increasingly fierce.

James added that for those hot games with well-placed investments, the opportunity to make them last longer is more attractive than ever.

Tencent's strategy is to leverage the strengths of different studios.

Tencent has many capable studios, with a large part especially skilled in player-versus-player games, and they will continue to double down on their strengths. Many studios outside of Tencent excel in story-driven games on the content side, such as 'Black Myth: Wu Kong.'

There are also some studios specializing in strategy games, such as 'Whiteout Survival.' For these types of studios, Tencent will seek investment, and sometimes deepen and enhance investment relationships with these external studios through game distribution.

James believes this strategy is correct,which involves leveraging internal studios and investments, as well as cooperation with external studios, so that each studio can focus on its own areas of expertise.

For the future development strategy of the gaming business, Liu Chiping stated that they will maintain and expand the number of evergreen games while creating games with the potential to become evergreen. However, Tencent's future focus on game development will be on producing high-quality games, rather than winning through quantity.

Key Point Two: Marketing Services

In the third quarter of 2024, Tencent's marketing services revenue increased by 16.6% year-on-year to 29.993 billion yuan, driven by strong demand from advertisers for Video Number, mini programs, and WeChat search advertising inventory, along with a slight contribution from brand advertising for the Paris Olympics. However, this positive impact may not be repeated in the fourth quarter.

In terms of industry classification, advertising spending in the gaming and e-commerce industries increased year-on-year, surpassing the reduced spending in the real estate and food & beverage industries. Segment gross profit increased by 18.2% year-on-year to 15.894 billion yuan.

Performance in specific subfields:

1) Video Number's marketing services revenue grew by over 60% year-on-year.

Due to the company's systematic enhancement of WeChat's transaction capabilities, advertisers have increased their utilization of its marketing tools to boost content exposure and sales conversion.

2) Mini programs' marketing services revenue showed strong growth year-on-year, as their mini-games and short videos provide high value returns and increase closed-loop demand.

3) WeChat search advertising revenue more than doubled year-on-year, driven primarily by the increase in commercial search volume and click-through rates. Leveraging the capabilities of large language models, WeChat search has enhanced its understanding of complex searches and content, improving the relevance of search results.

James looks ahead to 2025,The macroeconomic environment will be an important background factor that sets the tone for the overall advertising market, as it determines consumer confidence and thus influences their consumption behavior.

In this context, Tencent's relative performance will depend on:

First, its advertising technology and the ability to use GPUs, continuing to increase click-through rates from the current very low levels to higher levels through neural networks, thereby mechanically converting into more revenue.

Secondly, the deployment of specific inventory, especially Video Number and WeChat Search: In terms of the Video Number, Tencent moderately increased advertising loads in the third quarter, contributing to over 60% of the year-on-year growth disclosed, but the advertising load is still significantly lower than peers.

According to the data provided by James, the current industry average is about 15%, while Tencent's current level is only 3%-4%.

Looking ahead, with the increase of advertising volume, James expressed confidence that Tencent can continue to surpass the industry average level without the need for active contributions from e-commerce. Once the advertising volume reaches about two-thirds of the current industry level, or approximately 10%, it can truly enter a virtuous circle, then initiate e-commerce, and advertising will become increasingly important.

However, he also mentioned that based on its growth trajectory, this scenario will still take several years.

Therefore, he believes that with the improvement of advertising technology, the increase in video account advertising load, the growth of WeChat search, Tencent will continue to outperform the overall advertising market in the coming years. This will gradually open up the closed-loop of e-commerce while maintaining market share, which will be more advantageous for them.

Key Point Three: WeChat Mini Stores

The goal of WeChat Mini Stores is to create and develop a unified and reliable e-commerce platform within WeChat, allowing merchants to operate indexed and standardized product stores. These products will become data structures within WeChat, representing product information.

At the same time, merchants will undergo certification and quality monitoring to enhance consumer experience and provide greater quality assurance for products, as well as drive traffic. Store experiences will be integrated into the WeChat service ecosystem, bringing new traffic to other applications such as chat, group chat, Moments, and other media properties like Official Accounts, Mini Programs, search, video accounts, and recommendation engines.

In simple terms, WeChat Mini Stores allow users to know what products merchants are selling, and then drive traffic to them through the WeChat ecosystem.

The difference between WeChat Mini Stores and Mini Programs:

Liu Chiping stated that the 2 trillion transactions in the third quarter of the Mini Programs were actually mostly service revenue, not physical goods transactions.

The significance of WeChat Mini Stores is that when users transact in Mini Programs, Tencent does not know the transaction content, what items were sold through the Mini Programs, and it is also difficult for merchants to attract new customers through natural traffic via Mini Programs.

但如果产品通过微信小店售卖,则商家就能够触达微信社交平台的所有流量端,包括通讯、社交平台以及视频号,这给予商家比小程序更优质的体验。

刘炽平提到,微信小店的基础设施仍有许多需要改善的地方,还要增加许多功能,提升客户服务和体验,还要提供许多商家工具。一旦这一切都完成了,其就会把这个基础设施与各种流量商铺联系起来。并强调管理层没有从短期的角度来看待微信小店的前景,而他相信,随着其真的打造出所有这些产品、功能和实用程序,那么增长就会随之而来。

对于前景,他表示中国最近的刺激经济措施非常具有建设性,也非常及时,管理层对更长远的经济前景有信心。他相信经济增长将会恢复,只是时间上可能不太确定,而且这些措施也需要时间来实施和发挥效果。就目前的宏观经济环境而言,在宣布有关政策后,10月份交易货值有所上升。

看点四:微信支付

第3季度中国零售业有较低的单位数增长,但是微信的支付收入却按年下降。

Liu Chiping believes that the main differences are due to two reasons:

1) In this year, Tencent has been clearing low-quality trades, especially those with frequent losses. This actually affects its overall payment volume.

2) The coverage of WeChat Pay does not represent all retail consumption in China, it actually tends more towards small daily payments. Therefore, when evaluating its payment business, the focus is more on the number of transactions rather than transaction volume or revenue, and the number of transactions has actually increased by about 10% year-on-year.

Key Point Five: Tencent's AI Applications

Liu Chiping believes that currently AI is most useful in content recommendation and ad targeting because the AI engines in these two use cases can increase user engagement. At the same time, it also brings higher increment targeting and response rates to its applications, both of which directly benefit business and ad revenue, enhancing the scale of video number and revenue performance.

Revenue from IaaS now only accounts for 10% of artificial intelligence. Nevertheless, he believes that AI revenue is actually lower than that of U.S. cloud companies.

The main reason is,

First, China does not really have a large enterprise market. Many U.S. companies are actually adapting to AI, and as they test how AI can contribute to their business, they are purchasing a lot of computing power, which has not yet happened in China.

Second, there is a large Software as a Service (SaaS) ecosystem in the USA, where everyone is trying to integrate AI into their offerings to charge customers more. The SaaS ecosystem is not very active in China.

Third, there are fewer AI startups in China, which are actually buying a lot of computing power.

Therefore, AI in cloud computing in China has a certain scale, but he believes it will not grow explosively like in the USA. As for how AI will infiltrate Tencent's different products and services, he believes it will be in content recommendations and advertising. Meanwhile, it is actually a productivity tool used frequently by everyone, for example, assistant tools significantly improve operation and operational efficiency.

All of Tencent's products are being tested with mixed reality and they are trying to integrate AI into production processes and user experience use cases to improve efficiency and user experience. Now, he has seen more and more people using the corresponding features of its products and services. But it may take several quarters to see large-scale actual use cases.

As for monetization, James mentioned that advertising will not be embedded in commercial search results. Currently, Tencent is focused on enhancing advertising appeal to users rather than immature monetization.

Key Point Six: Cooperation with Taobao

James mentioned that cooperation with $Alibaba (BABA.US)$ Taobao, under its umbrella, has just begun.

James pointed out that the case of Taobao using WeChat Pay in October is very impressive.This is beneficial to Tencent because it increases its overall e-commerce, digital payment service total payment volume (TPV) and revenue. It is also advantageous for Taobao, as there is reason to believe that the majority of customers using WeChat Pay within Taobao are new customers of Taobao.

James believes that as WeChat Pay users find it increasingly easier to transact on Taobao, advertising Taobao on WeChat will become more favorable.

Focus 7: Selling Investments and Rewarding Shareholders

In the third quarter of 2024, Tencent generated a free cash flow of 58.5 billion yuan.

As of September 30, 2024, Tencent's cash balance was 95.462 billion yuan, an increase of 23.705 billion yuan from the end of the previous quarter and an increase of 40.722 billion yuan from the beginning of the year.

Despite a significant increase in capital expenditures to 17.094 billion yuan in the third quarter, Tencent still has plenty of cash available for distribution.

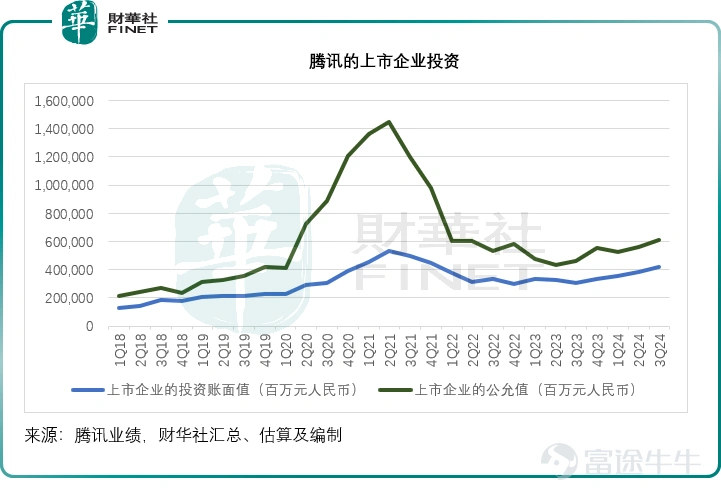

In addition, Tencent's fair value of investments in listed companies reached 612.5 billion yuan. Caixin estimates that the fair value of these investments in listed companies is approximately 419.016 billion yuan, which is 1.5 times their book value, indicating that Tencent could realize a decent return by selling these listed investments.

Richard Liu stated that the buyback target for 2024 is 100 billion Hong Kong dollars, which has now slightly exceeded 90 billion US dollars, and the buyback amount for this year is very likely to exceed 100 billion.

He pointed out that Tencent is in a favorable position to return cash to shareholders because its recurring business is actually generating a large amount of cash flow while having a very large investment portfolio, basically self-financed, and these investments will not withdraw any funds from its operating cash flow. On the contrary, when distributing shares or selling large assets, it can provide additional returns.

James also mentioned that Tencent is actively optimizing its investment portfolio. Over the past few months, with the significant rebound in various asset markets, Tencent has been actively reducing its investments to recover capital.

Richard Liu pointed out that based on the development of cloud business and AI investments, Tencent has a progressive capital expenditure plan. However, compared to many US companies, the relative scale of the capital expenditure plan is at a normal level. Therefore, he believes Tencent is expected to generate a considerable amount of free cash flow next year for dividends and share buybacks.

By: Mao Ting

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (4)

to post a comment

8

8