博通績後延續大跌!抄底良機or危險信號?

Futu Research | Broadcom's financial report review: Bull head turn or phased peak?

Leading global chip design company Broadcom released its performance for the third quarter of fiscal year 24. The overall performance was impressive, with revenue increasing by 47% year-on-year to $13.072 billion, and Non-GAAP diluted EPS increasing by 18% year-on-year to $1.24, exceeding market expectations. However, after the company's performance was released, the after-hours stock price fell by more than 8%, mainly due to the unexpected slowdown in revenue growth of semiconductor solutions in this quarter, which was lower than expected. At the same time, the company's performance guidance for the fourth quarter was also below expectations, causing market concerns.

So, has Broadcom been wrongly punished by the market? Has the semiconductor industry recently approached its cyclical peak? Next, we will analyze starting from Broadcom's financial report, clear up the fog, and provide investment advice for investors.

Where are the future growth points for Broadcom's performance?

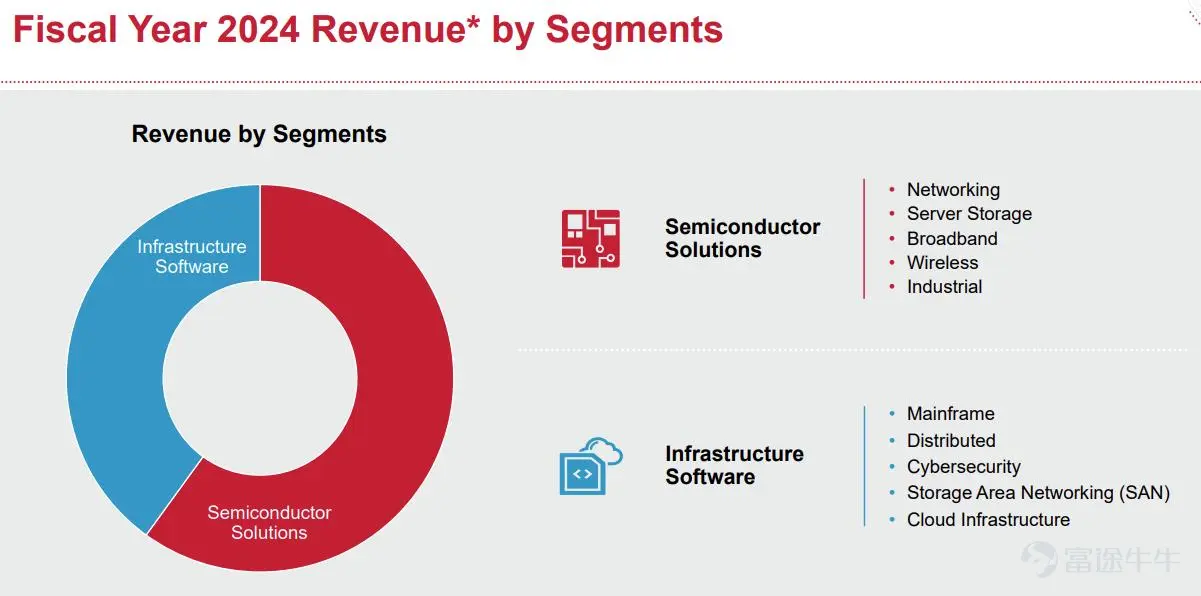

Broadcom's revenue comes mainly from two parts: semiconductor solutions and infrastructure software business. Among them, the proportion of semiconductor solutions revenue is relatively large, accounting for more than 50%, while the scale of infrastructure software business has rapidly expanded since the acquisition of VMware.

Source: Company Announcement

In this quarter, the company's revenue increased by 47%, mainly benefiting from the 200% growth of the infrastructure software business, thanks to the acquisition of VMware. The impact of the acquisition is expected to continue into the next quarter, and the subsequent growth rate will return to normal levels. In this quarter, the growth rate of semiconductor solutions revenue slowed to 5%, mainly due to the weak growth of non-AI business, with broadband revenue declining by 49% and non-artificial intelligence network revenue declining by 41%, offsetting the strong performance in the AI field. The performance guidance was also below expectations, largely due to the drag from non-AI business.

In the long term, the growth driver for Broadcom's performance is still the increasing demand for AI chips.

Broadcom's custom AI chips and network chips are essential components for data center suppliers to build AI systems, so Broadcom is undoubtedly one of the core targets benefiting from the surge in AI demand. This quarter, the company once again raised its sales expectations in the AI field, with expected sales of AI components and custom chips reaching 12 billion US dollars in fiscal year 24, up 9.1%. This is the company's second upward revision of expectations, indicating a continued positive outlook for AI demand.

The company's management disclosed that the potential market for the company's AI business is expected to reach 30 billion to 50 billion US dollars annually in the next 3-5 years. Looking at the revenue of 12 billion US dollars in fiscal year 24, there is still room for doubling in the future, effectively driving the company's performance growth.

Why did the stock prices of semiconductor companies perform poorly after the release of their financial results?

Although the overall performance exceeded expectations, Broadcom's stock price fell more than 8% after the release of its financial report. Similarly, when we reviewed the performance of semiconductor companies' stock prices after the release of this financial report season, we found that the performance of most semiconductor companies' stock prices was not optimistic. Specifically:

(1) Nvidia announced a strong second-quarter report, with revenue and net income both significantly exceeding market expectations, but the stock price fell nearly 7% after hours that day, and closed down 6.38% the next day.

(2) Taiwan Semiconductor released a strong second-quarter report, with both performance and guidance very optimistic, but the stock price fell 1.38% after the results.

(3) ASML Holding's second-quarter report exceeded market expectations, but third-quarter revenue guidance fell short of expectations, and the stock price fell 12.74% after the results.

(4) AMD's second-quarter performance showed strong growth, with third-quarter guidance meeting expectations. The post-results stock price increase narrowed to 4.36%, but the stock price fell 8.26% the next day. In addition, we can also see that the PHLX Semiconductor Index has fallen nearly 20% from its July peak.

So why are semiconductor companies not seeing optimistic stock performance despite strong performance? The reasons are as follows:

(1) Overly high market expectations.After a huge rise in the previous period, driven by the AI wave, the market has continuously raised performance expectations for semiconductor companies, especially for future performance growth. Once the performance guidance of semiconductor companies fails to meet the highest expectations and cannot digest the high valuation, the stock price of the company will experience a significant pullback.

(2) Poor AI investment returns or downstream demand impact.The current semiconductor market boom is mainly attributed to the rise of the AI wave, and the performance growth of semiconductor companies comes from the increasing demand for AI chips from downstream customers. However, the return on investment in AI by major semiconductor customers is not optimistic. It can be seen from the second quarter reports released by major technology and internet companies that the massive AI capital expenditure has not brought corresponding returns, but instead has lowered profitability. Therefore, under this background, if downstream customers cannot continue to increase capital expenditure, semiconductor companies will face the problem of declining order growth rate and slowing performance growth.

(3) The high base number inevitably leads to a slowdown in performance growth.Semiconductors belong to a cyclical industry. 2023 and 2024 are explosive high-growth cycles for the industry. After 2025, with the continuous increase in chip supply and the cooling of industry demand, combined with the high base issue, the revenue growth rate of the semiconductor industry will inevitably slow down.

Therefore, we can determine that the semiconductor industry is approaching the top of the industry cycle. With the slowdown in the company's performance growth rate after 2025, the company's valuation needs to return to a reasonable level.

3. How to deploy trading strategies in the current market environment?

In the current market environment, we need to pay special attention to the prospects of semiconductor company's performance growth.

1. Trading strategies for Broadcom

Based on Broadcom, it is expected that AI custom chips will become the driving force for the company's performance growth, and EPS growth will remain in double digits in fiscal year 2024 and 2025. In terms of shareholder returns, the company's dividend yield (TTM) is approximately 1.33%, and no share buyback plan has been announced, which is not attractive to shareholders. The company's current market cap is $711.359 billion, and the PE ratio (TTM) is 131.97. Calculated based on earnings expectations for fiscal years 2024 and 2025, the forward PE ratios are 32x and 25x, respectively, which are relatively reasonable valuations with limited upside potential for stock price.

Investors who hold the underlying stocks can use the investment strategy of selling high call options with the cover call strategy. Investors who do not hold the underlying stocks can wait for the stock price to further decline before buying at opportune times.

2. Trading strategies for the semiconductor industry

Currently, the semiconductor market is at its peak, with high industry valuations. It is recommended to closely monitor changes in the US macroeconomic environment and the progress of AI technology. US macroeconomic data is very volatile, and the latest manufacturing data is not optimistic. The upcoming non-farm payroll data release tonight will have a significant impact on the market.

It is expected that the semiconductor industry will experience significant volatility in the short term and face the risk of a pullback. Currently, the well-known leveraged ETF for shorting semiconductors is SOXS. However, leveraged ETFs with multiple times leverage have high losses and are not recommended for long-term holdings. It is advisable to engage in trend-based trading and sell for short-term profits.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (7)

to post a comment

148

33