多空分歧加劇!英偉達績後如何操作?

Futu Research | Nvidia Financial Report Review: Slowing growth in performance is inevitable, how should investors respond?

In the chess game of investments, each financial report release is like a crucial move, and NVIDIA's latest financial report is undoubtedly a powerful move in this game. On August 28th, Eastern Time, NVIDIA, the highly anticipated global leading GPU manufacturer, released its Q2 fiscal year 2025 report, which had impressive performance. However, the stock price experienced significant volatility after the results, dropping more than 8% at one point.

Next, we will analyze the highlights and concerns of Nvidia's second quarter performance as well as the future performance growth expectations, and discuss investment strategies for Nvidia.

1. The strong growth of the data center business, but the future revenue growth rate is expected to gradually slow down.

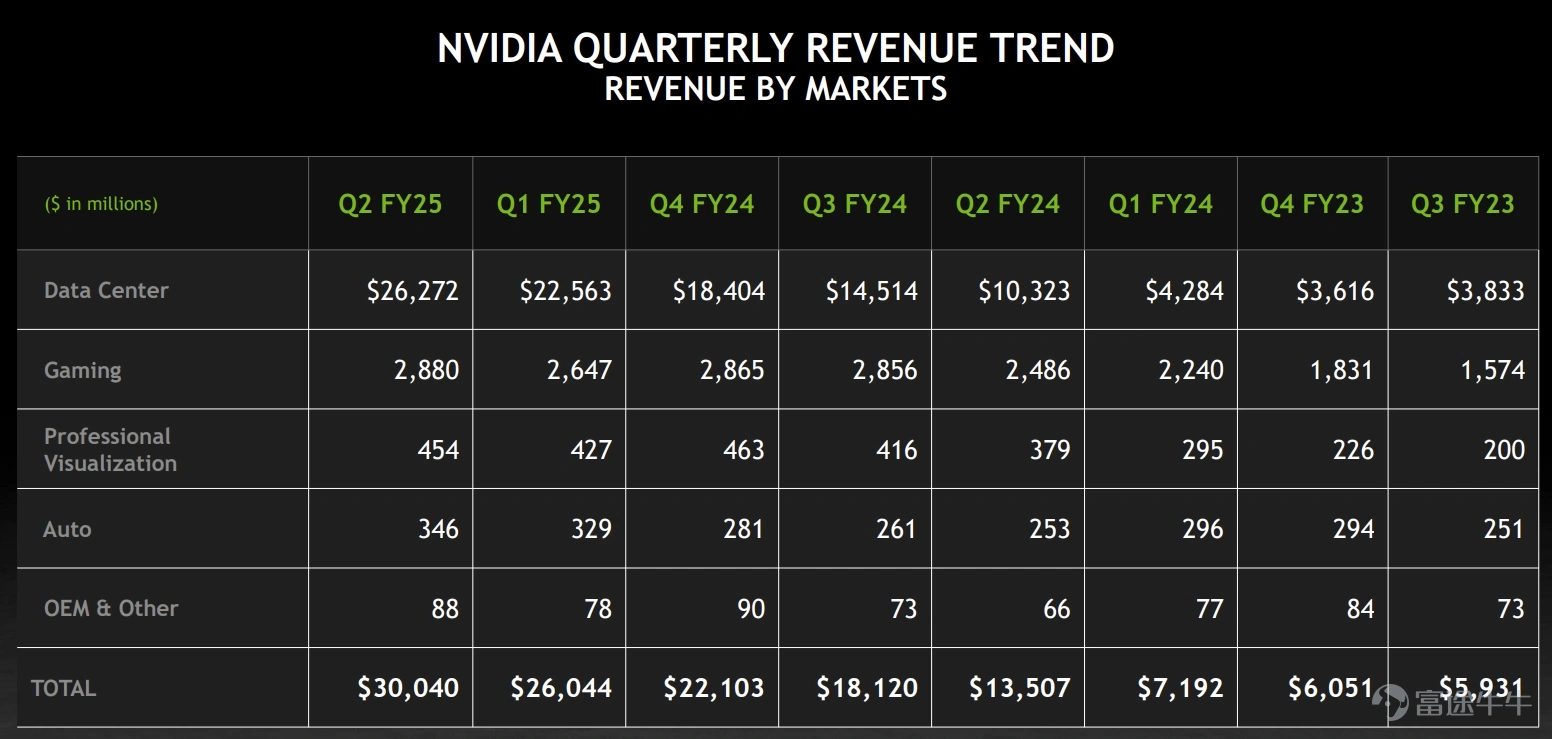

The company's revenue in the second quarter was $30.004 billion, a 122% year-on-year increase, still performing well. The data center business contributed 88% of the revenue, making it a solid revenue pillar. Therefore, the company's future performance will almost entirely depend on the growth of the data center business. Next, let's specifically break down the performance of the segmented business.

1. Data Center Business

In the second quarter, data center revenue was $26.272 billion, a 154% year-on-year increase, mainly due to strong demand from downstream customers for Nvidia Hopper, GPUs, and network platforms, exceeding analysts' expectations of $25.1 billion. Cloud service providers account for about 45% of the data center revenue, with over 50% coming from consumer and internet-related companies.

The main product in the company's data center business currently is the H200 chip based on the Hopper architecture, and the shipment volume is expected to continue growing in the second half of the 25 fiscal year. The company expects to start mass production of Blackwell architecture chips in the fourth quarter, with expected revenue reaching several billion dollars.

Benefiting from strong demand for AI, the company's data center business still has strong growth potential, but the expected slowdown in revenue cannot be ignored.

The explosive growth period of Nvidia's revenue in this round began in FY24Q2. Therefore, under the gradually increasing high base, the revenue growth rate this quarter has significantly slowed to 427% from the previous quarter, and it is expected to inevitably face pressure from slowing revenue growth rates in subsequent quarters.

Meanwhile, based on the financial reports of technology giants who are downstream customers of NVIDIA in the second quarter, the current substantial AI capital expenditure has already had a negative impact on profits and cash flow. The return on AI investment is relatively low, so it is uncertain how long NVIDIA can sustain its downstream client orders.

The semiconductor industry has obvious cyclicality.From NVIDIA's own annual revenue growth rate, it is also apparent that high-speed revenue growth can be sustained for 2-3 years, followed by entering a bottleneck period. After the high-speed growth of 125.85% in fiscal year 24, fiscal year 25 is already the second year of high-speed growth. If downstream order demand saturates, it is expected that NVIDIA's growth will significantly slow down after fiscal year 26.

2. Other businesses such as gaming.

In addition to the datacenter business, NVIDIA's other businesses have relatively smaller scale and steady growth without many highlights. In the second quarter, revenue from gaming and AI PC business grew 16% YoY to $2.88 billion; revenue from professional visualization business grew 20% YoY to $0.454 billion; revenue from automotive and robotics business grew 37% YoY to $0.346 billion.

Overall, the company's revenue growth rate will gradually slow down.According to the company's performance guidance, the revenue for the third quarter is expected to be $32.5 billion, with a fluctuation range of 2%, namely $31.85 billion to $33.15 billion. The YoY growth rate is about 76%-83%, and the MoM growth rate is around 6.03%-10.35%, indicating further slowdown in growth.

Chart: Revenue breakdown of NVIDIA's segmented businesses (in million US dollars)

Data Source: Company Announcement

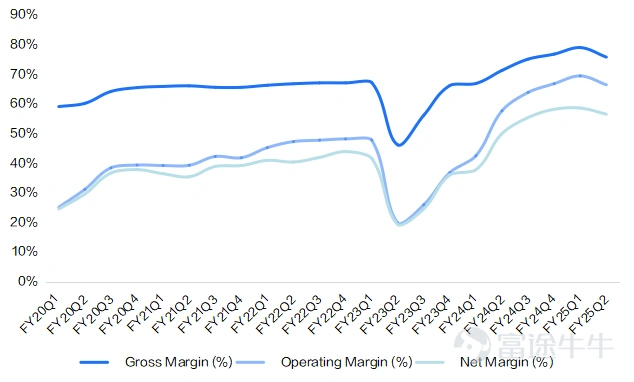

Second, the gross margin is expected to further decline in the second half of the year, and the EPS growth rate will slow significantly.

Regarding the gross margin, the company's gross margin in the second quarter was 75.7%, a decrease of 3.2 percentage points from the previous quarter's 78.9%. The company's gross margin has basically peaked. NVidia’s gross margin has achieved two consecutive years of growth, mainly due to product demand far exceeding supply, and continuous pricing increases leading to a sustained increase in gross margin. Currently, due to the gradual catch-up of NVidia chip supply and the increase in Blackwell chip R&D costs, the change in product mix is expected to further lower NVidia's gross margin to a reasonable range.

According to the company's performance guidance, the non-GAAP gross margin for the third quarter is expected to be 75%, with a fluctuation of ±50 basis points, i.e. 74.5% to 75.5%. It is expected that the company's gross margin for the whole year will remain around 75%, i.e. the gross margin for the fourth quarter may further decline to around 70%.

On the net profit side, the company's adjusted net profit for the second quarter increased by 151.51% year-on-year to 16.952 billion US dollars, with a net margin of 56.43%, a decrease of approximately 2.08% from the previous quarter, mainly due to the decline in gross margin, while operating expenses remained excellent. The adjusted EPS for the second quarter increased by 152% year-on-year to $0.68, a significant slowdown from the growth rate of 486.36% in the previous quarter, primarily due to a significant slowdown in revenue and the decline in gross margin.

Overall, with the increase in supply and changes in product mix, it is expected that the company's gross margin will further decline in the second half of the year, with the annual gross margin at around 75%. Against the backdrop of slowing revenue and declining gross margin,the EPS growth rate in the second half of the year will further slow down.

Chart: NVidia Profit Margins Performance (%)

Source of information: company announcement.

3. Trading Strategy

NVIDIA's high stock price is based on high expectations for performance, and judging future performance requires close tracking of downstream customer demand. From the current market situation, downstream customers are experiencing erosion of profits and cash flows due to low AI input-output ratio, which negatively impacts NVIDIA's future order visibility. At the same time, due to the high base value of performance, the company's future revenue growth rate will inevitably face the problem of slowdown, and the decline in gross margin will significantly slow down NVIDIA's future EPS.

Therefore, although AI demand still exists, it is expected that the company's EPS growth rate will slow down significantly in the next three years, especially starting from the 26th fiscal year, the EPS growth rate will fall sharply to a level of 20%-40% growth.It is expected to put significant pressure on overall performance.

In terms of valuation, due to the significant slowdown in EPS growth rate in the next three years, the current valuation PE (TTM) of 59x and the forward PE (FY25) of around 46x, based on a market cap of $3.08 trillion, are both relatively high.

In terms of shareholder returns, the company has announced a buyback program of around $50 billion without setting an expiration date. In the first half of 2025, the company plans to return $15.4 billion to shareholders through stock buybacks and cash dividends, with an expected annual shareholder return rate of 1%, which is relatively low in attractiveness.

As investors, what should we do?

Investors hold shares of Nvidia.

Assuming investors already hold Nvidia's stocks, considering the difficulty of short-term price increase, they can consider selling high-priced call options to earn premiums. If exercised, they can also sell the stocks at a satisfactory price. Considering the short-term risk of price correction, investors can also consider selling high and buying low, selling the stocks first and then buying them back at a lower price.

Investors do not hold shares of Nvidia.

Assuming investors do not hold shares of Nvidia, they can consider buying at a reasonable price below $100 after price correction. At the same time, they can adopt a strategy of selling put options with a strike price below $100 to earn premiums. If exercised, they can buy the stocks at a lower cost. Due to the high attention and strong fundamentals of Nvidia, shorting Nvidia alone carries greater risks. It is advisable for investors to be cautious.

In this investment feast woven by numbers and strategies, Nvidia's financial report is undoubtedly a sumptuous main course. As investors, our task is to remain vigilant and use wisdom and patience to seize every investment opportunity. Remember, market fluctuations are temporary, and the intrinsic value of the company is our compass for decision-making.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (13)

to post a comment

129

63