【產品推薦官】邊個牛牛功能最幫到你賺錢?

【Investment Talk】What do you think of Google's results? Focus on the underlying plate and growth points

In the global search engine field,$Alphabet-C (GOOG.US)$Uniquely, even the ChatGPT-backed Bing under Microsoft could not threaten Google's status as the leader. GOOGLE'S MARKET CAPITALIZATION HAS ALSO SURPASSED $2 TRILLION THIS YEAR, SECURING THE TOP FIVE GLOBAL MARKET CAPITALISTS.

After the US stock market close on July 23,$Alphabet-C (GOOG.US)$The latest results will be published. Every time a company publishes results, perhaps it means a good deal or investment opportunity. Before that, investors need to figure out how to understand its performance.

How do I look at Google's performance? What are the main points of concern? whoseThe core may lie in 3 aspects, including a base plate, a growth point, and its shareholder return.

1. Basic portfolio: advertising business

To look at a company's performance, you first need to focus on the businesses that account for the highest revenue. in$Alphabet-C (GOOG.US)$In terms of revenue, advertising revenue accounts for nearly 80% of total revenue, which can be said to be Google's bottom line. For Google's advertising business, there are two main points to pay attention to.

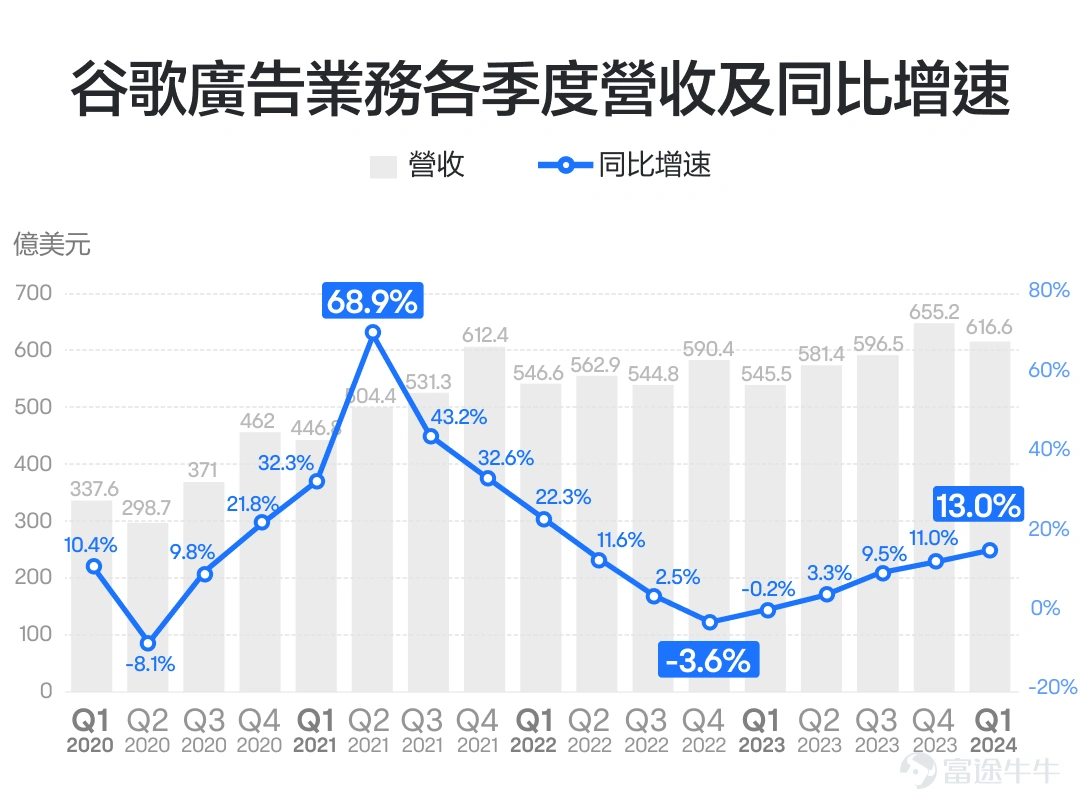

First, focus on the growth of advertising revenue.

The advertising business has a certain cyclical attribute. When the economy is not expected, businesses need to reduce efficiency. The first thing to do is to compress advertising, which puts pressure on the entire advertising industry to grow.

Previously,$Alphabet-C (GOOG.US)$Ad revenue growth is way down from its high point in Q2 2021, especially starting in Q2 2022. Google's ad growth is more of a cliffhanger, with two consecutive quarters of negative growth starting in Q4 2022 as the Fed moves into a rate hike.

However, in Q2 2023, Google's ad revenue showed a better-than-expected drop of about 3.3% year-on-year, and in the latest 2024Q1 results, ad revenue grew 13.0% year-on-year for four consecutive quarters. In future results, we still need to remain focused on whether its ad revenue growth will continue to rebound.

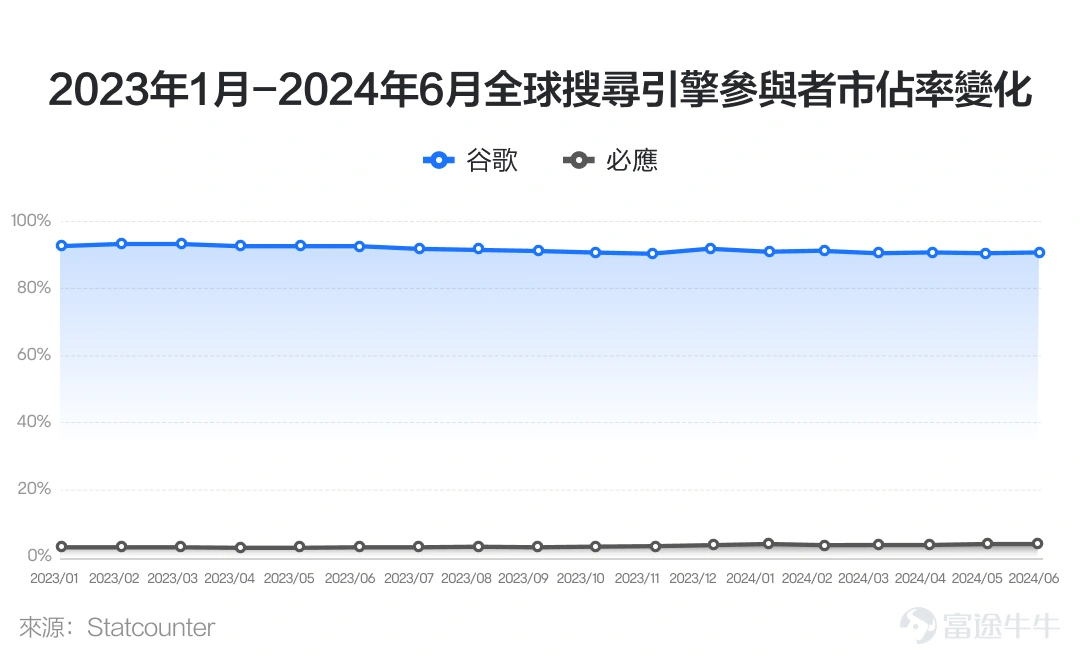

Second point, follow the change in market share under the ChatGPT impact of Google Search.in$Alphabet-C (GOOG.US)$In the advertising business, the vast majority of revenue is contributed by Google Search ads. This is the root of the development of Google Survival.

In Statcounter's statistics, we see that between January 2023 and June 2024, with ChatGPT added, the market share of Bing under the banner of Microsoft increased slightly by one percentage point. Google's market share also showed a slight decline, but still remained above 90%, maintaining its monopoly status, its moors and competitiveness may not have suffered a major impact. We can then continue to see if Google's market share remains stable.

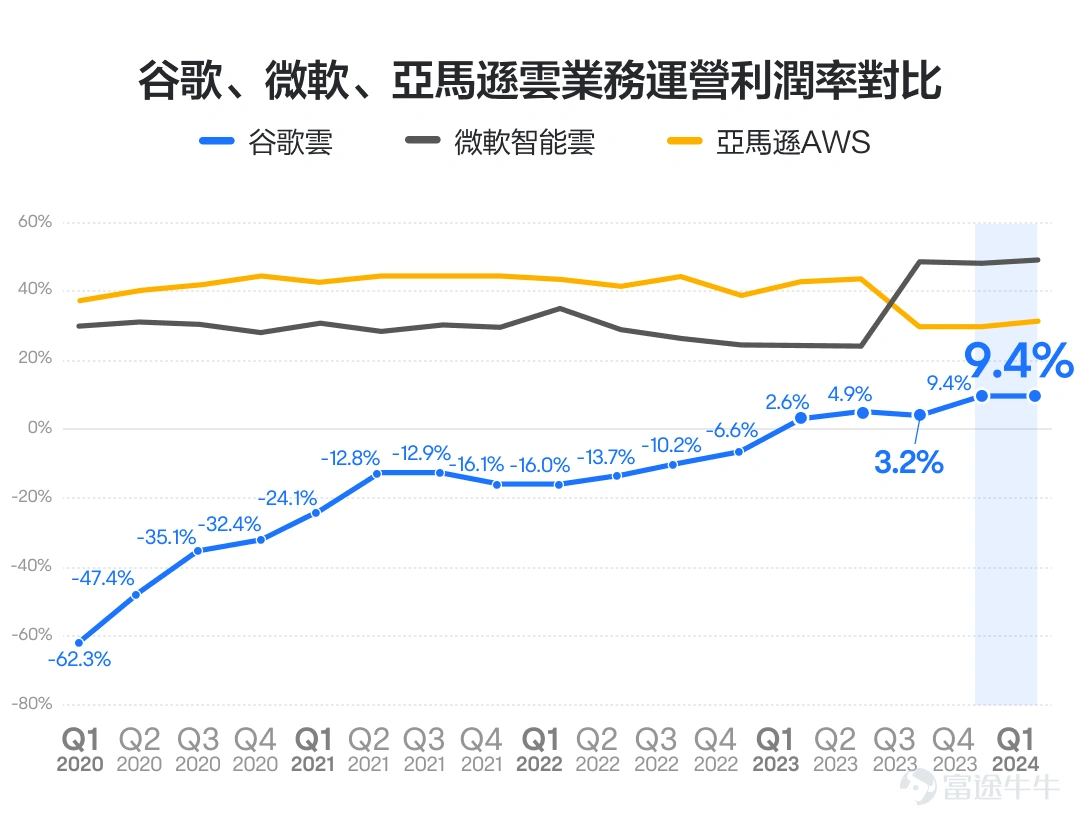

2. Growth point: Google Cloud

If you say the advertising business is Google's core platform, then the cloud business is$Alphabet-C (GOOG.US)$The core growth point. As of Q1 2024, Google Cloud ranked only 10% of overall revenue, but was one of the company's main growth engines. For Google cloud business, there are two points to consider as well.

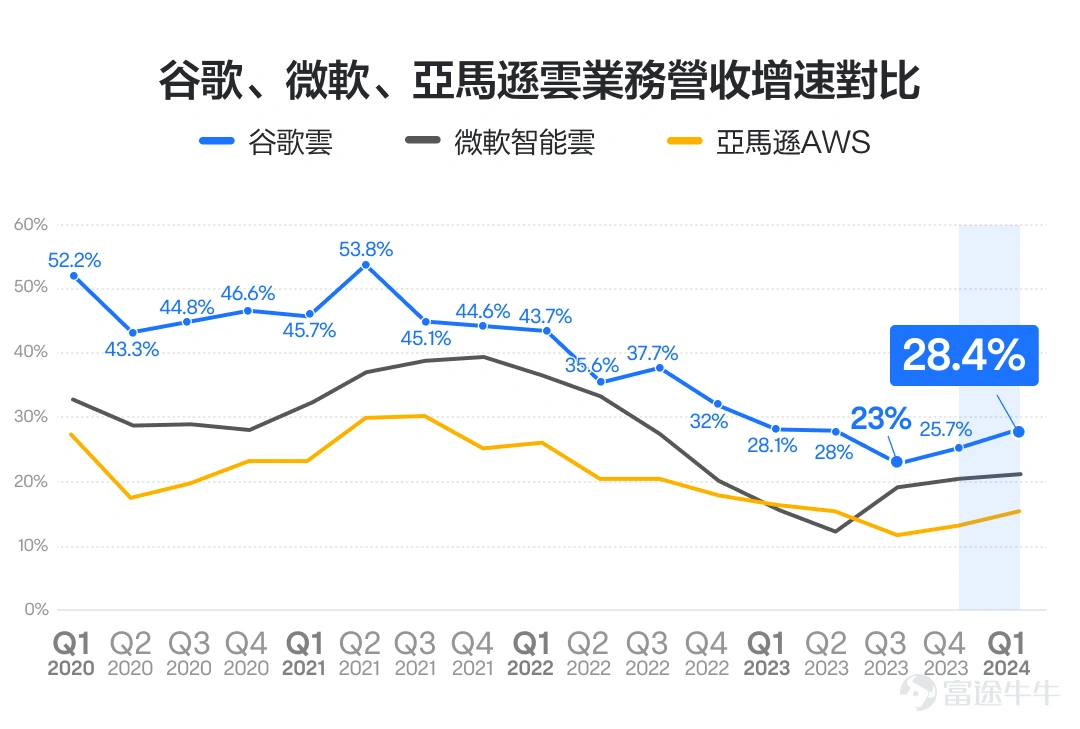

First, see if Google Cloud can continue to grow at a high rate.

Currently, Google Cloud ranks third in the cloud computing services industry, and while its market size is far behind Amazon and Microsoft, cloud business growth remains ahead of the three.

However, Google's cloud business growth has slowed significantly amid a slowdown in overall growth in the cloud services market. Growth in the previous two quarters of 2023 remained steady at around 28%, dropping to less than 23% in fiscal 2023Q3.

However, in 2024Q4-2024Q1, Google's cloud business growth rebounded steadily, returning to above 28% again.

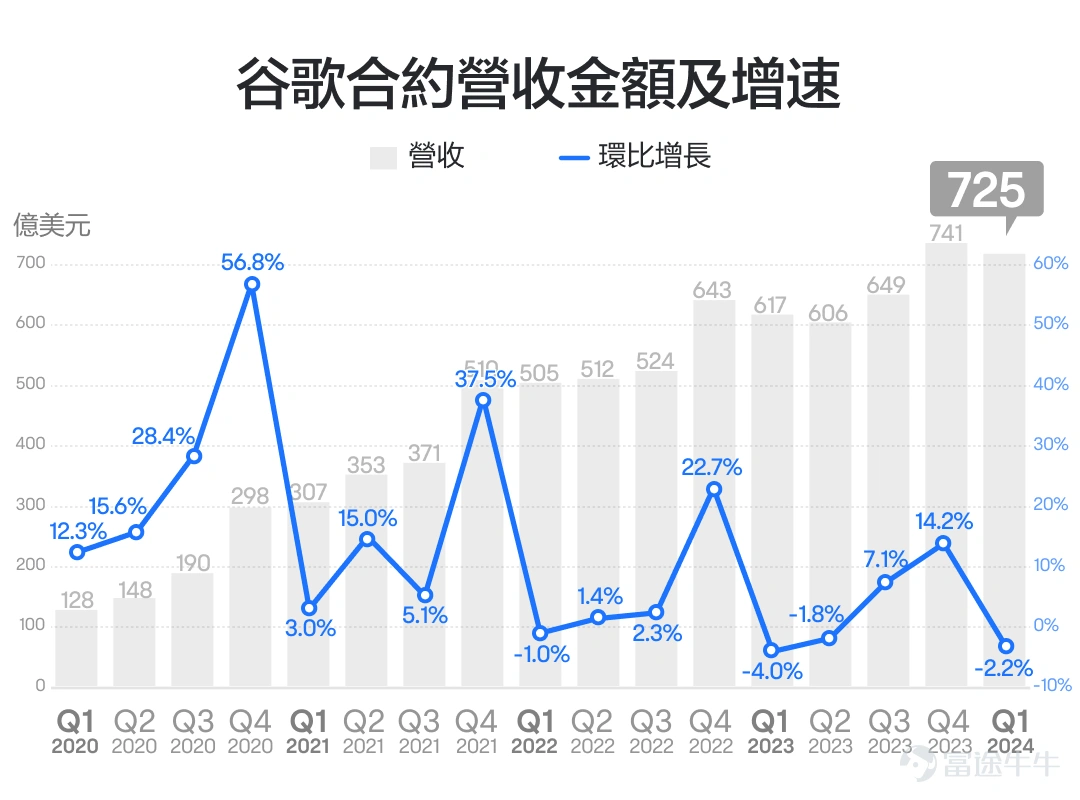

For Google Cloud revenue growth expectations, we can focus on one forward-looking metric, namely:Revenue backlog (revenue backlog) disclosed in results, mainly the amount of unexecuted customer orders signed by Google Cloud, which can be said to be the balance of Google's cloud business.

We see Google Cloud's contract revenue of approximately $72.5 billion in 2024Q1, a slight decline after experiencing strong growth for two consecutive quarters in 2023Q3-Q4, after which we need to see if its contract revenue can continue its previous growth momentum after adjustment. If it continues to slide, it may not be good news for the growth expectations of Google's cloud business.

Second, look at Google Cloud's profit margin.The cloud computing industry has a more pronounced scale effect to a certain extent, and only after a certain scale it is possible to be profitable. The more customers that spend the same money on developing products, the higher the profit margins may be. While Google Cloud's revenue growth is far outpacing Amazon and Microsoft, its profitability has also been the strongest due to its minimal revenue size.

For a long time, Google Cloud has been in a state of continuous loss and has been a bottleneck for its overall profitability levels.

The good news is that its loss margin tended to narrow overall until Q1 2023, with Google Cloud's revenue reaching a tipping point, plus cost optimization brought by cutters, Google Cloud finally achieved its first quarterly profit in history and continued to contribute to positive earnings in the subsequent fiscal 2023Q2-2024Q1.

Google's cloud operating margin has exceeded 9% since Q4 2023Q4.

For the upcoming fiscal quarter, we need to see whether Google's cloud revenue growth will continue to rebound and, as a result of scale, drive operating margins to continue to rise.If Google's cloud margin continues to improve momentum, it will also drive Google's overall profitability up a notch.

3. Shareholder return: share repurchase situation

For$Alphabet-C (GOOG.US)$For such tech giants, the volume of revenues and profits is already so huge that it may be difficult to replicate the miracle of rapid growth in the early stages of growth,The future normal may be medium-low growth.

For stock price movements, its long-term drivers may include two aspects,On the one hand is the growth of results and on the other is the return to shareholders.If you don't grow enough, you may get shareholder returns. The core of shareholder returns is mainly stock repurchases and dividends. And Google has a larger hand in terms of repurchases.

By repurchasing shares, on the one hand, you can reduce the number of outstanding shares, increase the profit per share, on the other hand, inject additional capital and liquidity into the market, and, finally, reduce the company's net assets and increase the return on net assets, which can have a very positive effect on the share price.

In recent quarters, Google's repurchases have remained at around $15 billion, second only to Apple among all tech giants. Its net asset return has remained high for most of the past few years, at around 20%.

For future results, we can continue to monitor Google's repurchases, which will perhaps inject more confidence into the market if sustained high repurchases.

Writing here, you may have some new insights into how to read Google results.It's worth mentioning that every time many star companies post results, it can mean a tough trading opportunity for different types of investors.

For example, if an investor feels that a company's recent performance will release some positive signals and favor short-term stock prices by interpreting past performance and incorporating recent progress, investors may consider doing more, and doing more could be to consider buying positive stocks, or consider buying bullish options, etc.

Conversely, if investors feel that the latest performance of a company will be less than optimistic and put pressure on short-term stock prices, investors may consider going blank, or consider buying bearish options, etc.

Of course, if investors feel that the direction of a company's performance is not very clear, but the stock price may fluctuate significantly upwards or downwards after the results are released, then investors may consider doing more of its share price volatility and consider buying both bullish and bearish cross strategies to gain a foothold In Opportunity.

In this context, the beef sirus master recommended a new feature of Futubull, viaMARKET PAGE > HONG KONG STOCKS, US STOCKS, ETC. MARKET TAG PAGE > PERFORMANCE EXCEEDS EXPECTATIONS,Click hereCan also be reached directly,Quickly identify quality companies and seize opportunities for market volatility。

Positive and negative values represent more or less than expected, respectively, and percentage values indicate specific gaps, which can beClick hereLearn more.

Finally, summarize

Advertising business is$Alphabet-C (GOOG.US)$The underlying unit, whose revenue has rebounded in almost two quarters, we need to keep an eye on its continued growth.

Google search is the foundation of the advertising business, and we need to keep an eye on whether its market share remains high.

Google Cloud is a key growth point for Google, and its growth rate remains at the forefront of the giants, and we need to focus on forward indicators of this revenue growth in contract revenue.

Google Cloud has a relatively low operating margin, and we need to watch for improvements in its margin.

Against the backdrop of lower Google growth expectations, its high repurchases have a positive effect on the share price, and we can focus on the persistence of its high repurchases.

Each time a company publishes results, it may bring potential trading opportunities. Investors can consider the right types of trades based on their individual risk tolerance.

👉👉Click hereGo to class, or follow @ Futubull Tong, Get more investment dry goods and greatly improve your investment skills!

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (2)

to post a comment

24

15