全球投資者關注!聚焦2024巴郡股東大會

Futu Research | Berkshire (BRK.A) First Quarter Earnings Forecast: Overall profit is under pressure, and the dual challenges of operation and investment go hand in hand

introduction

From May 3 to 5, EST, Buffett's shareholders' meeting, an annual global investment event known as the “Spring Festival Gala for the Investment Community,” will soon be held. Berkshire's financial report for the first quarter will also be announced at that time. Overall, operating costs are still under considerable pressure this quarter. Combined with fluctuations in stock prices of holdings, overall profit is likely to be under pressure.

Berkshire business model

Berkshire Hathaway's business model is to generate cash flow through steady management and diversified operations (especially in the insurance sector) and use this cash flow to invest, so the Berkshire business empire can be divided into business activities and investment activities;

Source: Futubull

Berkshire's business is divided into operating activities and investment activities. It predicts Berkshire's Q1 performance, focusing on two aspects: operating performance and return on investment. Let's analyze them one by one next.

Operating activities: High costs and pressure on operating profits

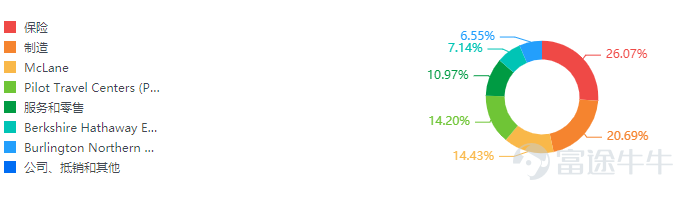

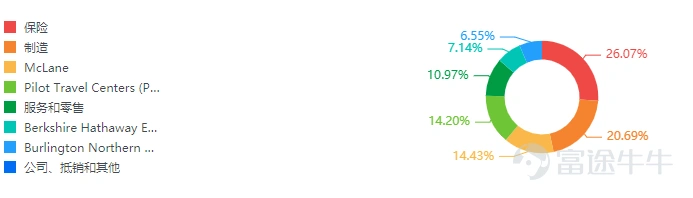

The business landscape is mainly divided into insurance business and non-insurance business. The insurance business is Berkshire's core business, while the non-insurance business covers various industry sectors such as manufacturing, service, and retail.

1. Revenue: Probability to maintain positive growth

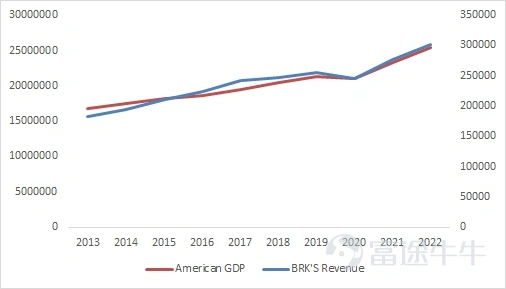

Berkshire Hathaway's business is centered and diversified in the US, and the overall revenue growth trend remains generally positively correlated with US GDP growth. At the same time, due to Berkshire's countercyclical nature and market dominance in specific fields, the company's revenue performance may be superior to GDP performance in times of economic downturn.

(For example, the insurance business, especially reinsurance, may be more complicated due to increased compensation for disaster events. It may either be pressured by increased claims or benefit from higher insurance premiums.)

Figure: Comparison between US total GDP and Berkshire revenue trends (unit: million US dollars)

Data sources: World Bank, Bloomberg

Overall, since 2015, overall revenue has entered a period of steady growth. There are three major sources of revenue: sales and service, insurance, railways, and energy, with each business accounting for a steady share over the years. Sales and service remained stable at 55%, and the insurance and railways, utilities and energy sectors accounted for around 23% and 20%.

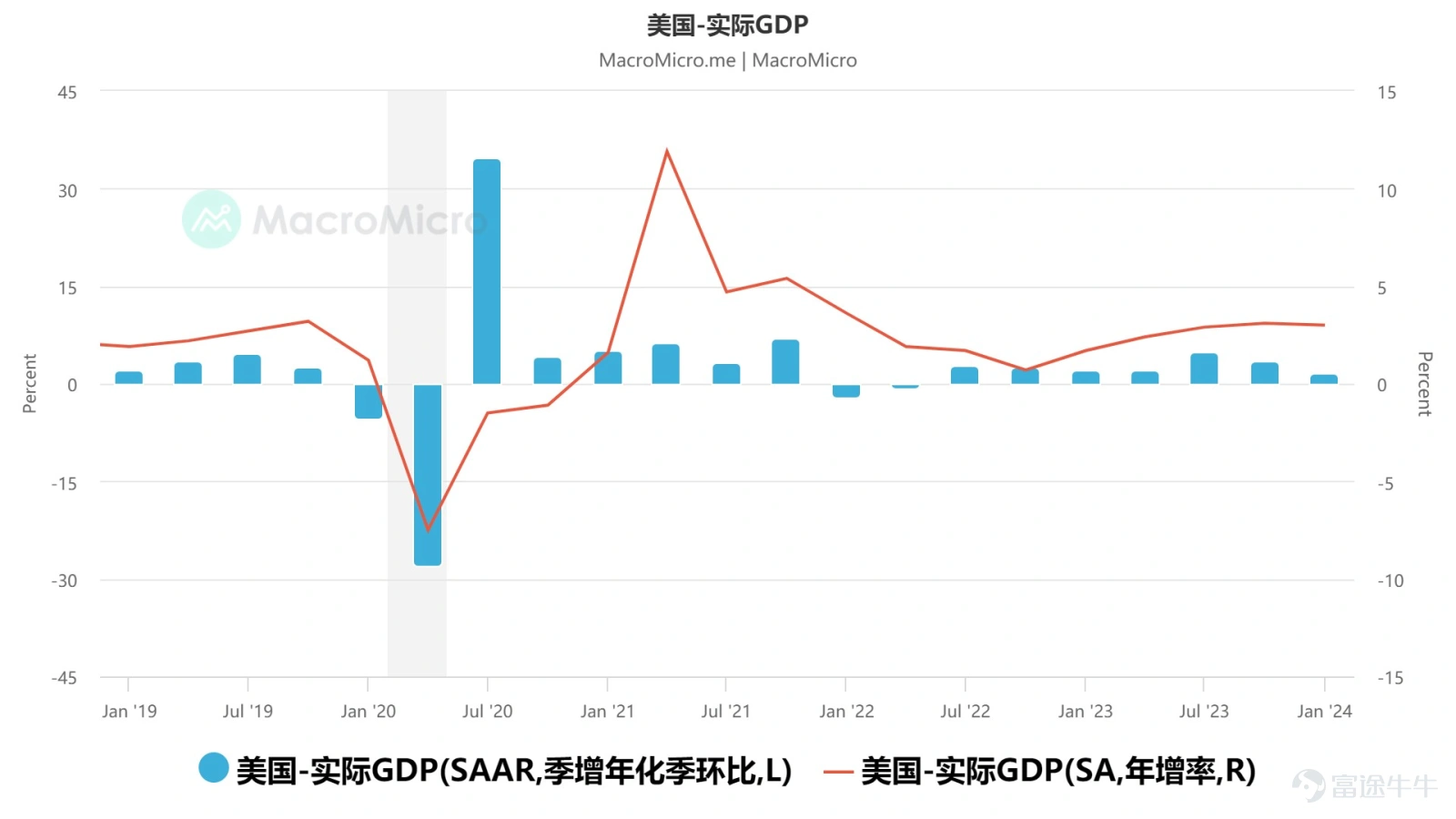

According to the latest data, in the first quarter of 2024, the US gross domestic product (GDP) grew at an annual rate of 1.6%, lower than the growth level of the fourth quarter of the previous year, but showed some resilience, so Berkshire's revenue is likely to maintain positive growth.

Figure: US Real GDP

Data source: MacroMicro

1. The insurance business is expected to remain stable or grow this quarter.

Insurance performance in the previous two years was dragged down by high natural disaster losses. In 2023, business picked up due to reduced disaster losses and improved GEICO coverage — thanks to reasonable premium increases and claims reduction. In the first quarter of 2024, if disasters remain low, the premium strategy will continue to be effective, and the insurance business is expected to grow steadily.

As for the first quarter, the insurance business is expected to stabilize or grow if no large-scale disasters occur and the premium adjustment strategy continues to be effective. The decline in natural disaster performance in the previous two years was mainly due to natural disaster losses. While disaster losses were low in 2023, GEICO's underwriting performance improved, premiums increased and claim frequency declined, and insurance business performance returned to an upward trajectory.

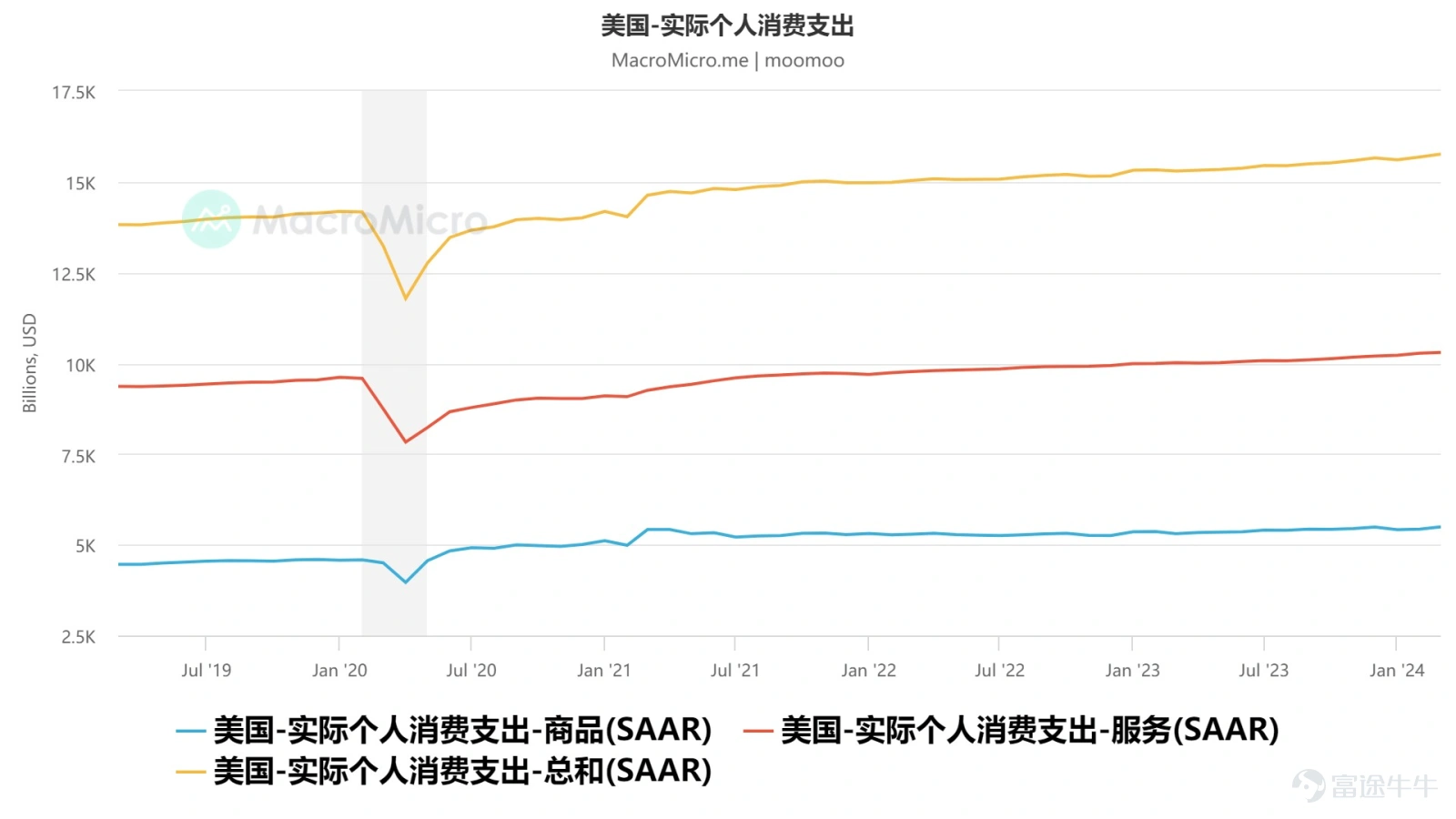

2. For non-insurance businesses, it is mainly closely related to the recovery of economic activity, the speed of recovery in consumer demand, and supply chain conditions.

Markit's manufacturing and service sector PMI both remained above the boom and dry line (usually 50) in the first quarter. The manufacturing and service industries were in an expansion range, and individual consumer spending also showed a steady growth trend. It can be inferred that the order volume and revenue probability of the company's related businesses will be positively boosted.

Figure: Actual personal consumption expenditure in the US (unit: million US dollars)

Data source: MacroMicro

2. Costs: Facing the double pressure of rising energy prices and wage growth

Over the past three years, Berkshire's main costs have been concentrated on energy sales costs and operating expenses. Combined, these two items accounted for 64%-73%, which shows that they dominate and are highly volatile.

Energy cost of sales (Energy cost of sales) Energy costs are directly affected by international commodity prices such as crude oil and natural gas. International oil prices showed an overall upward trend in the first quarter. At the end of March, the Brent crude oil futures price once rose to 87 US dollars/barrel, up nearly 10 US dollars/barrel from the level at the end of 2023. In the first quarter of 2024, the average price of Brent crude oil futures was 81.76 US dollars/barrel, down 1.09 US dollars/barrel from the previous month and 0.34 US dollars/barrel year on year. This puts pressure on Berkshire's costs.

For energy operating expenses (Energy operating expenses), rising energy prices are also putting pressure on energy operating expenses. If the possibility of natural disasters and unforeseen events is compounded, it is likely to increase the pressure on energy operating expenses.

Figure: Price changes in Brent crude oil futures (unit: USD/ton)

Data source: MacroMicro

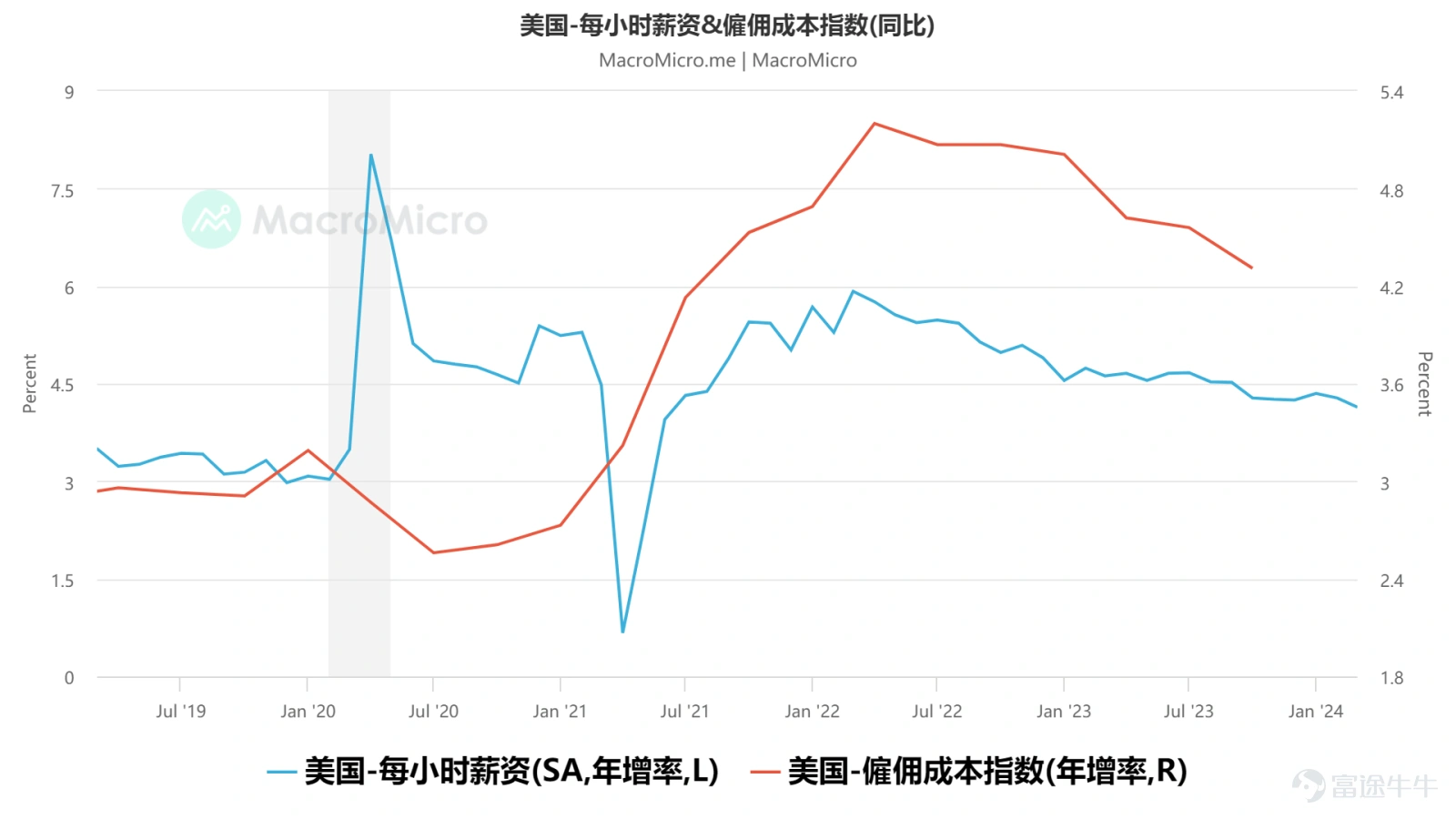

At the same time, pressure on labor costs remains significant, and wage growth continues unabated. Take BNSF as an example. One of the main reasons why profits fell more than expected last year was that wage growth exceeded expectations. As for the first quarter, wage growth remained high even though it slowed month-on-month. This pressure on labor costs may put pressure on the operating margins of related businesses in the short term.

Figure: US Labor Cost Index

Data source: MacroMicro

As a result, based on comprehensive revenue and cost judgments, operating profits for the first quarter were under considerable pressure.

Investment return - likely negative growth

The balance sheet clearly shows that Berkshire's asset allocation model is: holding a small amount of cash, mainly investing in U.S. Treasury Bills (short-term US Treasury bonds with an immediate term of more than three months but less than a year) and Investments in Equity Securities (equity investment), a typical barbell strategy.

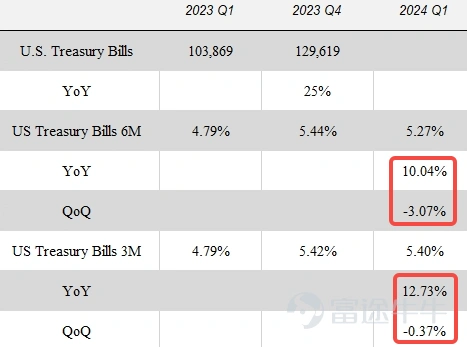

1. Treasury bond yield - short-term treasury bond yields increased year-on-year, fluctuating slightly from month to month

Berkshire also increased purchases of short-term treasury bonds this year. According to the 2023 annual report, Berkshire holds US$129.619 billion in short-term US Treasury bonds, an increase of 25% over the previous year. As a result, US short-term bond yields are closely tied to Berkshire's earnings. According to the US 3-month Treasury yield and the US 6-month Treasury yield data, the yield on US short-term treasury bonds remained at about 5.3% in Q1 in 2024, with little change from month to month, with a large year-on-year increase — an increase of about 10%.

The specific data is shown in the following table:

Data source: Company earnings report, Bloomberg

As a result, changes in yield are compounded by an increase in Berkshire's purchasing power of treasury bonds. Earnings on short-term treasury bonds in the first quarter may have increased well year over year, but there may be a decline from month to month.

2. Stock investment - facing downward pressure

Berkshire's heavy stock is still Apple, and the fluctuation in Apple's stock price weighs heavily on the overall portfolio performance. Regardless of the year-on-year or month-on-month performance, Apple's stock price has declined. Combined with the rise in other holdings, the overall portfolio investment income will probably fall by about 2% month-on-month, and may be able to maintain low single-digit growth at the same time.

Table: Berkshire's shareholding

Data source: Company earnings report, Bloomberg

Overall, Berkshire's investment earnings performance this quarter is unlikely to be very optimistic.

Investment advice: Use options strategies to optimize cost structures

Stock investment value is equal to EPS (earnings per share) * valuation (price-earnings ratio, net price-earnings ratio, etc.) * shareholder return (dividends, repurchases, etc.).

In terms of shareholder returns, there have been few regular dividends in Berkshire's history. The last regular dividend was in 1967; however, in recent years, Berkshire has significantly increased its share repurchase efforts.

Total repurchases in 2020 were US$24.7 billion, total repurchases in 2021 were US$27.1 billion, total repurchases in 2022 were US$9.2 billion, and total shares were repurchased for the full year of 2023. 2021 is the peak year for Berkshire's recent buybacks. According to another report, Buffett has repurchased a total of 3808 Class A shares since this year, involving an amount of about 2.2 billion to 2.4 billion US dollars.

If calculated according to the 2023 repurchase amount, the repurchase can probably bring about 1% return to shareholders. Therefore, Berkshire's stock price mainly depends on profit and valuation.

As for the first quarter, investment returns were dragged down, and profit growth was probably not optimistic, which may lead to a short-term decline in stock prices.

For quarterly reporting strategies:Given Berkshire's solid fundamentals, derivatives can be used to cope with stock price fluctuations if there is a short-term decline in stock prices. If you already own or plan to hold a stock (such as Berkshire shares) for a long time, you can earn a premium (option fee) by selling (or “shorting”) a call option on that stock to optimize the cost structure or increase the return on holding the stock.

Strategy logic:

1. Income premium: If you sell a call option higher than the current market price, you can get a premium income. This part can directly increase the return on the investment portfolio.

2. Cost optimization: If the stock price does not rise above the execution price of the option, the option will not be executed when it expires. Investors can keep the stock and continue to enjoy their shareholders' rights. At the same time, the royalties previously collected can be seen as reducing the cost of holding shares.

3. Limited upside return: The downside of this strategy is that it limits the stock's upward return. If the stock price exceeds the execution price of the sold call option before the option expires, the stock will be bought at a lower execution price, and investors will lose the additional profit from the continued rise in the stock price.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment

20

15