Futu Research | Online Music Sees Strong Growth – What Is the Investment Potential of Tencent Music?

Introduction

On March 19, Eastern Time,$TME-SW (01698.HK)$The company released its unaudited financial results for 2023 and the fourth-quarter report. According to the financial statements, Tencent Music's total revenue for 2023 reached RMB 27.752 billion (all amounts in RMB unless otherwise stated), slightly surpassing Bloomberg's consensus estimate. Despite a volatile macroeconomic environment and increasing industry competition, Tencent Music has demonstrated steady growth and strong market adaptability due to its continuous efforts in online music operations and ongoing enhancements to user experience. As of March 20, Tencent Music's share price on the Hong Kong stock exchange exceeded HKD 44.

As a global leader in digital music entertainment, Tencent Music is deeply embedded in China’s vast consumer market. With its exceptional content ecosystem, innovative music-social strategies, and robust copyright management capabilities, the company holds a pivotal position in the global music industry. The core businesses consist of online music services (62%) and social entertainment services (38%). Notably, online music services account for more than 60% of Tencent Music's total revenue, making them the primary driver of overall earnings; thus, this segment's growth trajectory deserves close attention.

Next, we will conduct a detailed analysis of Tencent Music's latest quarterly financial report.

I. Steady Overall Revenue with Strong Growth in the Online Music Business

According to the financial report, Tencent Music's Q4 2023 revenue totaled RMB 6.893 billion, down 7.16% year on year; full-year revenue reached RMB 27.752 billion, a 2% decline from the prior year, slightly above Bloomberg's consensus estimate of RMB 27.3 billion. The company's performance was primarily driven by growth in music subscription revenue, strong digital album sales, and a recovery in online advertising revenue, which to some extent offset the negative impact of persistently weak social entertainment revenue on overall revenue. Overall, the company's online music business has emerged as the primary driver of future earnings growth.

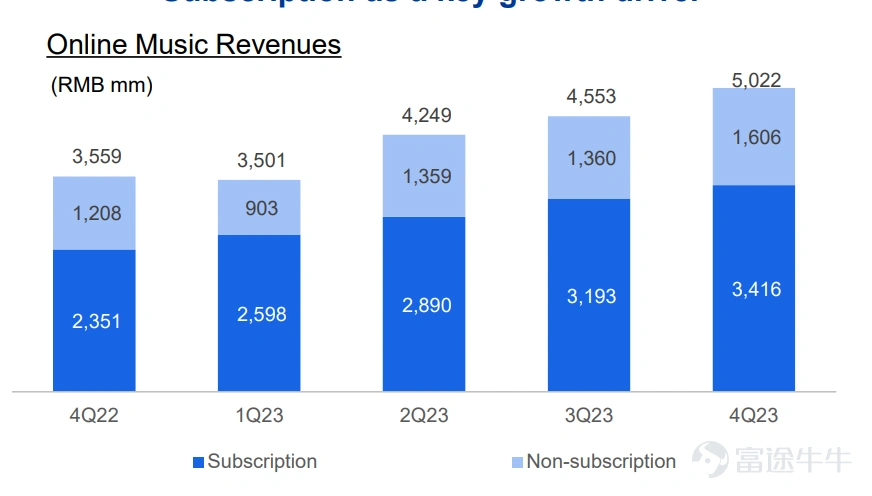

Subscription revenue and advertising services are driving growth in the online music business. Tencent's online music segment posted robust expansion, generating RMB 17.325 billion in revenue in 2023, up 38.79% year on year. In the fourth quarter, online music service revenue reached RMB 5.02 billion, a 41.1% increase from the same period last year, accounting for 72.9% of total revenue.

Figure: Revenue Performance of the Online Music Business (Unit: Million RMB)

Data source: Company financial reports

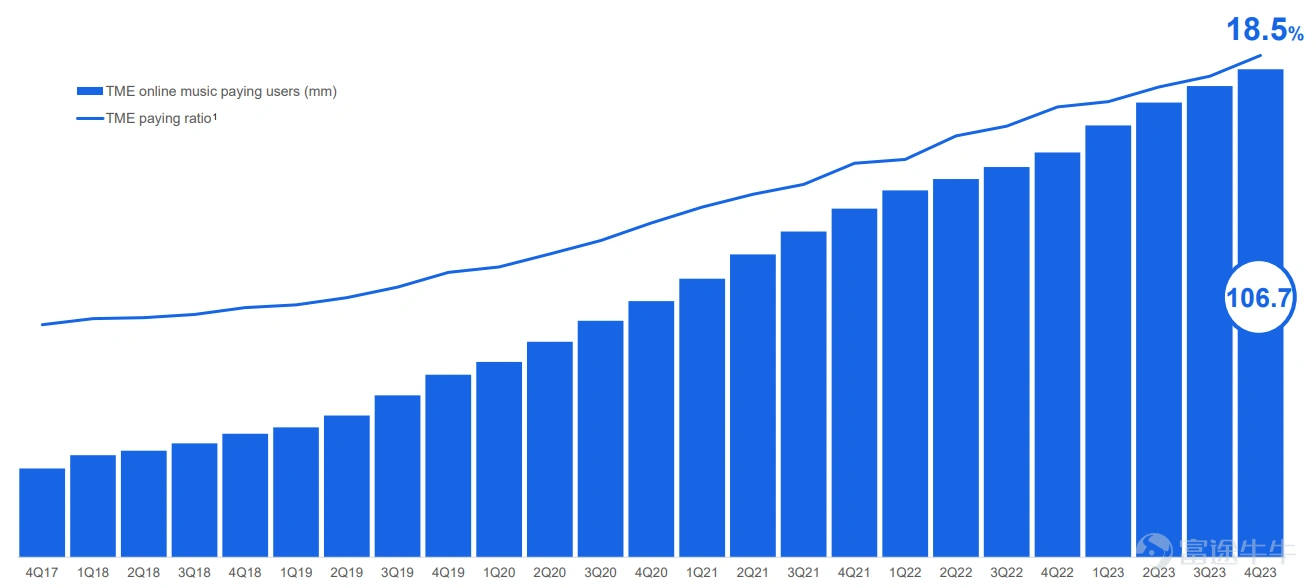

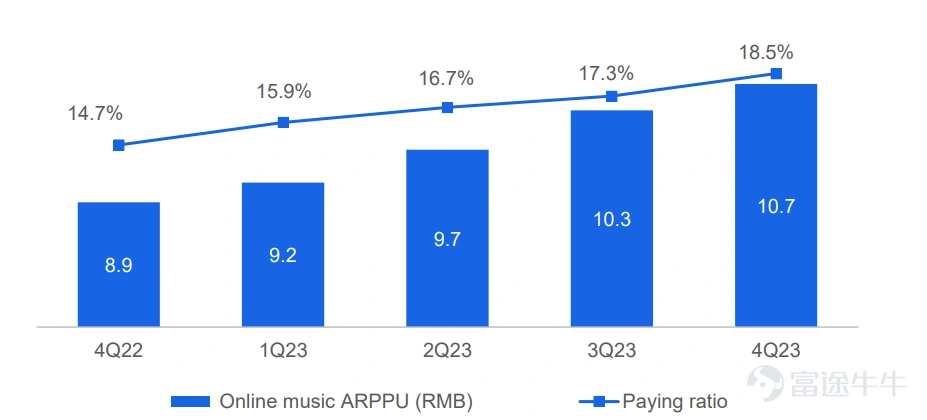

(1) The number of subscribers continues to grow steadily.The primary driver of growth in the online music business is the company's sustained expansion of its paid membership base, fueled by advertising-driven marketing initiatives and bundled sales of artist merchandise. According to the financial report, the company's total number of paid online music subscribers increased by 1.6 million year over year to 106 million in 2023, representing a 19.8% year-over-year rise. Meanwhile, the paid-subscriber conversion rate climbed to 18.5%, underscoring the company's strong ability to convert free users into paying customers.

Figure: Paid User Conversion Rate (%)

Data source: Company financial reports

(2) ARPPU has increased for six consecutive quarters.Thanks to more effective adjustments to pricing policies and enhancements to membership benefits, the company was able to reduce discounts on recurring monthly subscriptions while simultaneously boosting user retention through proactive operations. As a result, the company's Q4 2023 monthly ARPPU increased by 20.22% year over year to RMB 10.7 per month, surpassing Bloomberg's consensus estimate of RMB 9.85.

Looking ahead, the company will continue to drive ARPPU growth by scaling back certain ineffective promotions and expanding its Super Membership offering. According to guidance provided during the latest quarterly earnings call, the company plans to introduce differentiated subscription packages—such as Super Membership and IoT-based plans—to further boost ARPPU. Management disclosed on the call that the company's ARPPU for the current quarter stood at RMB 10.7, still below the list price of RMB 15 for the continuous monthly subscription plan, indicating room for ARPPU expansion over the medium to long term.

In addition to its online music business, the company's social entertainment segment represents another major business pillar. As the online music business continues to accelerate, market participants are concerned that the social entertainment segment might weigh on overall performance; therefore, it is crucial to monitor how this segment unfolds going forward.

II. Social and Entertainment Business Continues to Decline; Bottom Expected This Quarter

In the social entertainment segment, adjustments to certain live-streaming interaction features and stricter compliance and risk-control measures have continued to weigh on traditional live-streaming engagement businesses. In 2023, Tencent Music's social entertainment revenue declined further to RMB 10.427 billion, a year-on-year drop of 34.24%. The financial statements clearly show that the slight overall revenue decline was primarily attributable to the drag from the social entertainment business.

(1) The number of social entertainment subscription users has declined for three consecutive years.In Q4 2023, the company's social entertainment segment recorded 7.6 million subscription users, a year-on-year decrease of 2.56%. The decline in subscription numbers was primarily attributable to the company's adjustments to certain live-streaming interaction features, the implementation of more stringent compliance procedures, and the enhancement of risk control management.

(2) Social and entertainment users' willingness to pay has also declined significantly.In Q4 2023, ARPPU stood at RMB 78 per month, down 9.5% quarter over quarter. This marks the fifth consecutive quarterly decline for the company's social entertainment business since Q3 2022, and the downward trend is expected to be difficult to reverse in the near term. However, based on the Q4 earnings call, the company has already begun implementing proactive measures in Q4 2023—such as expanding its karaoke business—which are expected to gradually moderate the rate of decline in ARPPU for the social entertainment segment starting in Q3 2024.

III. Effective Cost and Expense Control Leads to Steady Improvement in Profitability

Notably, despite a decline in revenue, the company's profitability remains at an excellent level.

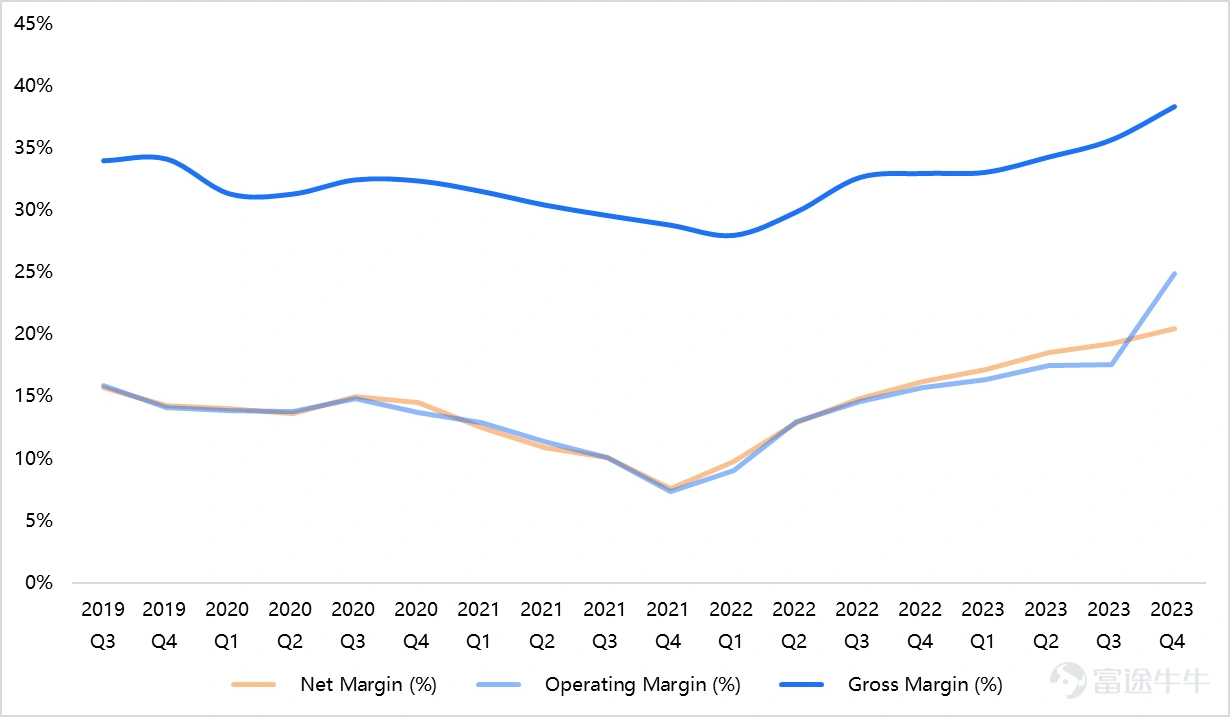

In the fourth quarter of 2023, Tencent Music's gross margin expanded from 35.65% to 38.3%, and its full-year gross margin rose from 30.96% to 35.29%. On the net profit front, the company's net margin increased from 13.54% in 2023 to 18.86%, with full-year net profit reaching 4.92 billion yuan, up 28.15% year over year—slightly above Bloomberg consensus estimates. The steady growth in profitability was primarily driven by robust revenue growth in music subscription and advertising services, as well as a higher share of original content.

Figure: Profit Margin Trend (%).

Data source: Company financial reports

In terms of costs, the company has maintained effective control over both costs and expenses. In 2023, the company's cost of revenue totaled 17.957 billion yuan, a year-on-year decrease of 8.22%. The financial report attributes the decline in cost of revenue primarily to lower revenue-sharing expenses resulting from reduced revenue from social entertainment services; however, this was partially offset by increases in copyright-content costs, advertising-agency fees, and payment-channel expenses.

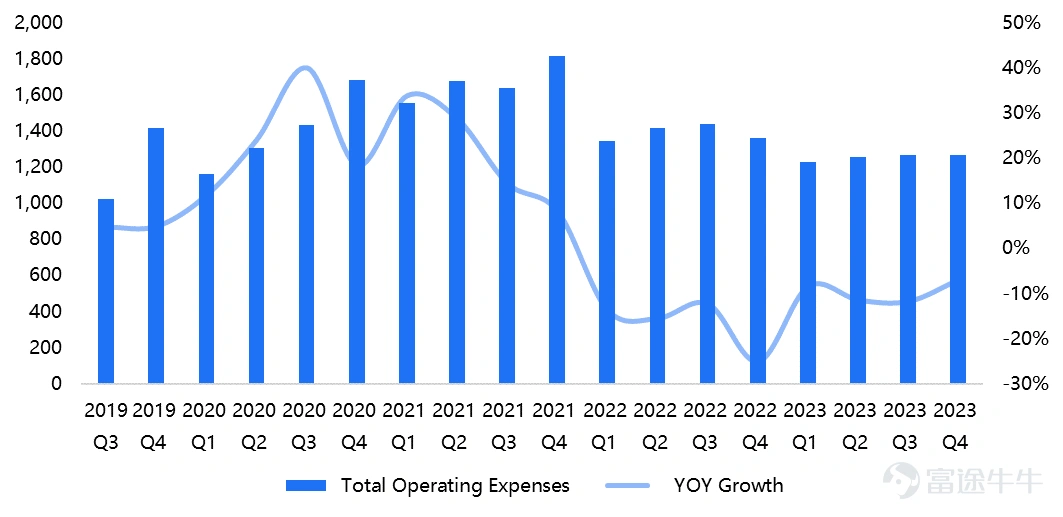

From a cost perspective, the company's full-year operating expenses in 2023 totaled 5.018 billion yuan, down 9.7% year on year. By segment, the company's sales expense ratio fell from 9.16% in the prior year to 5.17%, primarily due to lower promotional spending on social entertainment services; meanwhile, the general and administrative expense ratio declined from 35.35% to 23.78%, largely reflecting reduced personnel costs and the fact that the 2022 figures included expenses related to the company's secondary listing in Hong Kong.

Overall, the company's cost of revenue and various expense ratios have declined, demonstrating strong control over costs and operating expenses and thereby further enhancing its profitability.

Figure: Changes in Total Operating Expenses (Unit: Million Yuan)

Data source: Company financial reports

IV. The Competitive Landscape of Online Music Is Clear, with Tencent Music Holding a Distinct Advantage

Another major reason for Tencent Music's outstanding performance is the current competitive landscape of the online music market, which is highly favorable to it.

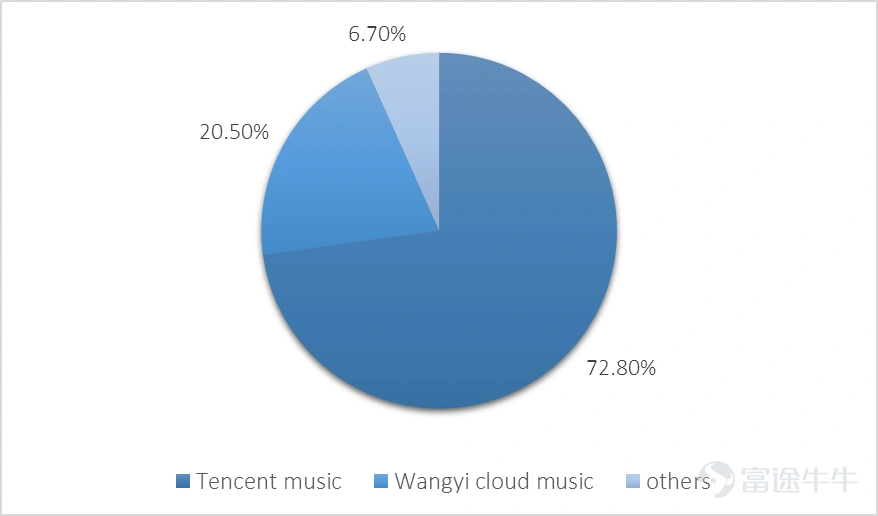

In terms of industry competition, according to iResearch data, in 2023 Tencent Music held a 72.8% share of the domestic music market, with a significant advantage over NetEase Cloud Music and other online music platforms in both music content and user base.

Figure: Tencent Music's Market Share (%)

Data source: iResearch

(1) Tencent Music holds exclusive on-platform music rights to songs by renowned artists such as Jay Chou. In July 2021, China's State Administration for Market Regulation ordered Tencent and its affiliates to terminate exclusive music licensing agreements within 30 days, discontinue the practice of paying high upfront royalties and other similar copyright fees, and ensure that mutual licensing arrangements cover at least 99% of the catalog; however, Tencent Music has nonetheless managed to attract a substantial user base by retaining exclusive rights to just 1% of the music library.

For example, in Apple Music's 2023 Top 100 Hottest Songs in Mainland China, Jay Chou accounts for 62 tracks, dominating the entire top five and nine of the top ten. Moreover, Jay Chou's management company, JVR, maintains an exclusive partnership with Tencent Music, underscoring just how pronounced Tencent Music's content advantage remains thanks to its robust copyright portfolio.

(2) In terms of user scale, in Q4 2023, Tencent Music's online music business had 576 million monthly active users, down 4.2% year on year; however, the number of paying users increased, with a paid user ratio of 18.52% in Q4 and an ARPPU rising to 10.7 RMB per month. During the same quarter, NetEase Cloud Music recorded 205 million monthly active users, with a paid user ratio of 21.43%. Currently, Tencent Music is leveraging its massive user base to continuously convert existing users, which is expected to further boost its subscription revenue in the future.

Figure: Conversion Rate of Paid Users in the Online Music Business (Unit: Million RMB)

Data source: Company financial reports

Overall, the competitive landscape of the online music industry is well-defined, with Tencent Music's oligopolistic position remaining unshaken in the near term. This favorable environment enables the company to maintain its focus on boosting paid subscription conversion among its existing user base, thereby providing robust momentum for revenue growth.

So, what is the company's investment value?

From a fundamental perspective of the company:

In 2023, Tencent Music's revenue remained stable. Although the decline in its social entertainment segment weighed on performance, strong growth in the online music business helped offset some of the negative impact. Going forward, the primary driver of the company's earnings growth is expected to be the online music segment, while the social entertainment business is now broadly at or near its bottom.

Revenue growth in the online music business depends on the increase in the number of paying users and ARPPU. (1) In terms of the number of paying users, the company's current monetization rate is 18.5%, which still has considerable room for improvement compared with competitors such as NetEase Cloud Music and Spotify. (2) As for ARPPU, the company's ARPPU this quarter was RMB 10.7, still lower than the listed price of RMB 15 for a continuous monthly subscription, indicating that there is room for ARPPU to increase in the medium to long term.

Therefore, following the bottoming out of the social media business, revenue growth in the online music segment is expected to propel the company's performance back onto a growth trajectory, with revenue projected to post positive year-over-year growth in 2024 and EPS poised for double-digit expansion.

From the perspective of shareholder returns:

Historically, the company has delivered robust shareholder returns. According to its disclosures, Tencent Music announced a US$500 million share-repurchase program on March 21, 2023; as of December 31, 2023, it had repurchased US$174.5 million worth of shares, with an additional US$325.5 million still available under the program. Assuming a repurchase of approximately US$200 million in 2024, the annualized repurchase yield would be around 1%. The company enjoys strong cash reserves: as of December 31, 2023, its cash, cash equivalents, and time deposits totaled RMB 32.22 billion, positioning it well to continue delivering generous shareholder returns. In addition, during its earnings call, the company indicated that it is actively exploring the possibility of initiating dividend payouts.

Overall, the company's current market capitalization stands at approximately RMB 140.2 billion, and its EPS is expected to post double-digit growth in 2024 and 2025. At present, the company's valuation corresponds to a trailing-12-month P/E ratio of around 25–28 times, which will require robust earnings growth to sustain this valuation. In addition, investors are advised to closely monitor the company's future share-repurchase and dividend plans.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

12

4