美股科技股業績來襲!繼續狂歡or調轉方向?

Futu Research | Amazon Financial Report Review: Logistics Helps E-commerce Exceed Expectations in Profit Release

Amazon's revenue and operating profit for the fourth quarter both exceeded Bloomberg's consensus expectations. The revenue was $169.96 billion, a year-on-year increase of 14%, higher than the expected $166.21 billion, with an excess of 2%; in terms of profit release, the operating profit was $13.21 billion, higher than the expected $10.49 billion, exceeding expectations by 26%. AWS cloud business growth rate is basically in line with market expectations, with a year-on-year growth of 13%.

I. E-commerce constitutes the main part of the revenue, while cloud business contributes core profits

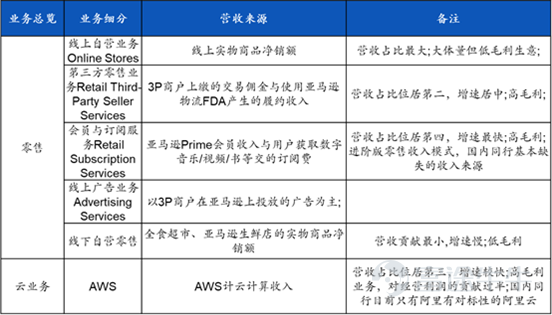

Amazon's business focus lies in: profit release of e-commerce business, recovery of cloud business (reflecting incremental business contributed by AI), and the competition for market share in advertising business.Amazon's business categories can be divided into retail and cloud services, with its main sources of revenue being online self-operated, online third-party retail business, membership and subscription services, advertising services, offline self-operated retail, and cloud services (AWS), etc.

(1) The e-commerce business constitutes the main revenue source, including amazon's self-operated and third-party retail business, accounting for nearly 70% of the revenue; due to the significant investment in logistics infrastructure during the epidemic period, the North American e-commerce business has been in a loss state since 21Q4. Starting from 23, a series of cost reduction, efficiency improvement, and reform measures have been implemented, leading to the gradual increase in profits of the North American e-commerce business quarter by quarter, while the losses of the international e-commerce business have also been narrowing simultaneously.

(2) The cloud computing business accounts for about 14% of the revenue, contributing more than half of the operating profit. Last year, due to relatively low enterprise IT expenditures, the growth rate was low, but signs of cloud business recovery began to appear from 23Q3 onwards.

(3) The advertising business currently has a small scale but impressive growth, being the fastest-growing business last year. With amazon's deepening layout in the advertising field, it is expected to become the second growth driver.

Image: Amazon business structure

Source of Information: Company Announcement, Compilation of Futu Securities

II. E-commerce business exceeding profit expectations

The performance of the e-commerce business in the fourth quarter once again underestimates the strength of consumer spending in the market.Online self-operated business increased by 9.3% year-on-year, third-party retail business increased by 19.9% year-on-year, with both growth rates improving month-on-month and exceeding expectations.

Figure: Amazon's online self-operated business and third-party retail business year-on-year growth (%)

Source of Information: Company Announcement, Compilation of Futu Securities

As a leading North American e-commerce company, Amazon directly benefits from consumer spending.From October to December, the monthly retail sales rates in the United States were -0.1%/0.3%/0.6%, exceeding market expectations for three consecutive months. The fourth quarter is the North American holiday shopping season. Despite consumers facing a high-interest rate environment,But retailers greatly stimulated consumption with large discounts and flexible payment methods such as 'buy now, pay later'.According to Adobe Analytics data, American consumers spent a record $222.1 billion in online consumption during the traditional gold shopping season from November 1 to December 31, 2023, setting an e-commerce record.

In terms of its own competitiveness, Amazon set another sales record on Black Friday, benefiting from increased promotional activities, extended duration, increased discount intensity, and improved delivery speed.

(1) Launched the new promotion shopping event Prime Big Deal Days in the fourth quarter, and extended the time for Black Friday and Cyber Monday holiday shopping events.

(2) In the first quarter of 23, the company completed the transformation of its fulfillment network, transitioning from a national to 8 independent regional networks. Significantly reducing delivery distances, shorter travel distances, and less contact means lower service costs, resulting in a substantial increase in delivery speed, with a 65% increase in same-day or next-day deliveries compared to last year.

(3) Increased discount efforts. Throughout the quarter, customers saved nearly $10 billion through discounts and coupons, an increase of nearly 70% compared to last year.

The transformation of the fulfillment network continues to reduce costs this quarter., while transportation costs (including long-haul transportation, marine transportation, and railroads) have also decreased, leading to a continuous improvement in the fulfillment cost rate, dropping from 15.6% in the previous quarter to 15.3%. The service cost per unit in the USA has decreased by more than $0.45 compared to the previous year.Cost reductions enable the company to offer more low-priced goods in the future to meet the needs of cautious consumers while remaining profitable.

Figure: Amazon's fulfillment costs (in million USD) and fulfillment cost rate (%)

Source of Information: Company Announcement, Compilation of Futu Securities

Sales expenses increased due to seasonal promotions, with the proportion of revenue increasing compared to the previous period. Other expenses also decreased to varying degrees, with the research and development expense ratio decreasing from 14.8% to 13% period-on-period, and the management expense ratio decreasing from 1.79% to 1.77% period-on-period.

The improvement in expenses led to profits released beyond expectations.. In the fourth quarter, the North American e-commerce segment achieved an operating profit of 6.46 billion US dollars, with an operating profit margin reaching 6.1%, and the profit margin continued to increase compared to the previous period. Due to the increase in expenses, international business saw operating losses increase to 0.42 billion US dollars period-on-period, significantly narrowing compared to a loss of 2.2 billion US dollars in the same period last year.

Chart: Operating profit (million US dollars) and profit margin (%) of the Amazon North American e-commerce segment.

Source of Information: Company Announcement, Compilation of Futu Securities

The fulfillment expense ratio is expected to continue to decrease in 2024, with current logistics networks still having room for savings. Due to increased investments in AWS and AI next year, the research and development expense ratio is expected to remain stable or slightly increase, while management and sales expenses are expected to remain stable. International business can be divided into mature country markets (mainly in Europe, Japan) and newly entered country markets. As service costs decline, the profit margins for mature country market operations are expected to gradually approach North American levels.

Third, AWS cloud service growth rate rebounded on a quarter-on-quarter basis.

In the fourth quarter, AWS business achieved revenue of $24.2 billion, a year-on-year growth of 13%, basically in line with market expectations. The quarter-on-quarter revenue increment of AWS in the fourth quarter exceeded $1.1 billion, accelerating from the previous quarter's $0.919 billion.If calculated at a fixed exchange rate, this quarter's revenue growth rate increased from 13% in the previous quarter to 14.85%, with two consecutive quarters of year-on-year growth rebounding.

Chart: Amazon AWS business revenue (million US dollars) and year-on-year growth (%).

Source of Information: Company Announcement, Compilation of Futu Securities

Looking at the competitive landscape of the cloud computing trio in the third quarter.In Q4 of 23, Amazon's AWS cloud service revenue grew by 13%, Microsoft's Azure cloud computing business revenue grew by 30%, and Google Cloud business revenue grew by approximately 25%. Due to Microsoft's collaboration with Openai and its advantage in office software for TO C end-users, it is the first to benefit from the demand for AI. Driven by AI, the intelligent cloud business is actively catching up, and the penetration rate of AI services in Azure Cloud has significantly increased. AI services contributed 6% to the growth (compared to 1% in the previous quarter).

Currently, the combined market share of the three companies is as high as 67%, according to Synergy's data.In the fourth quarter, Amazon still ranks first with a market share of 31%, but the share decreased by 2 percentage points compared to the previous quarter.Microsoft's market share in the fourth quarter increased by 2% to 25% compared to the previous quarter, while Google's market share remained stable at around 11%.

Chart: Market share of cloud computing business

Source: Synergy, Futu Securities compiled

In the short term, we believe that AWS's leading position remains relatively stable, but in the medium term, it depends on how much performance increment it contributes to AI.Amazon's advantage in the cloud computing field is attributed to its cost advantage in the Infrastructure as a Service (IAAS) sector and the product diversification in the Platform as a Service (PAAS) sector.

From the current landscape, Amazon's cloud business has layouts in the computation layer, intermediate layer, and application layer. Some outstanding developments in the fourth quarter include:In the computation layer, it announced an expanded strategic cooperation with Nvidia, becoming the first cloud provider to equip Nvidia's latest GH200 Grace Hopper superchip in the cloud, and launched the new generation Graviton4 processor and AWS Trainium2; in the intermediate layer, represented by Bedrock, it provides a wide range of foundational large models (Anthropic, Cohere, Meta Llama2, Stability AI, Amazon Titan) to help developers customize AI applications; in the top application layer, Amazon has built dozens of AI programs, launched the brand-new generative AI work assistant Amazon Q in the fourth quarter, and Rufus, a shopping assistant, in February.

Another major highlight of the cloud business is the improvement in profit margin.. In the fourth quarter, AWS operating profit was $7.2 billion, an increase of $2 billion year-on-year, with an operating margin of 29.6%, compared to 24.3% in the same period last year, remaining basically stable on a quarter-on-quarter basis. The increase in profit margin mainly reflects the reduction in the number of AWS employees and the slowing recruitment pace.

It is expected that the company will continue to focus on cloud business investment in 2024.In 2023, the full-year capital expenditure (including equipment financing leases) was $48.4 billion, a decrease of $10.2 billion year-on-year, mainly due to reduced fulfillment and transportation investment in the e-commerce business. Due to the increase in AWS infrastructure construction in 2024, as well as investment in AI generation and large language models, it is expected that capital expenditures in 2024 will increase year-on-year.

Fourth, the advertising business is expected to capture market share.

In the fourth quarter, advertising revenue was $1.45 billion, a 26.8% year-on-year growth,with continued growth for four consecutive quarters, mainly driven by Sponsored TV.In November 2023, Amazon Advertising updated its ad platform and added a new advertising product, Sponsored TV, which allows merchants to run video ads on streaming TV platforms (such as Amazon Fire TV or other smart TV platforms partnered with Amazon). These ads typically appear during program breaks or as part of the content, helping sellers promote their products and services.

Amazon's subscription service revenue grew by 14% this quarter, and the second season of 'Thursday Night Football' attracted 24% more viewers year-on-year, also drawing investments from advertisers.

Figure: Advertising Business Revenue (in million USD) and Growth Rate (%)

Source of Information: Company Announcement, Compilation of Futu Securities

Although the current scale is still relatively small, we believe that Amazon's advertising business is expected to continue to maintain high growth rates and capture market share.Compared to competitors, Amazon's advertising business has significant advantages in having Prime Video and e-commerce assets, being closer to end-consumer demands. Users on Amazon usually have clearer shopping intentions, and Amazon can leverage its vast user behavior database to provide highly precise targeted advertising services. This results in higher conversion rates compared to advertising formats seeking potential customers on other non-e-commerce platforms.

Is Amazon currently expensive or not?

With the significant release of profits and the promotion of AI, Amazon recently hit a historic high. Looking ahead to 2024, we have the following conclusions:

1. EPS Growth

(1) E-commerce Business

Recent strong employment data in the USA implies short-term strong consumption driving force. Alongside the decline in inflation in the USA and Europe, although consumers may face some pressure, overall there will not be a collapse, and consumers' purchasing power and consumption demand are expected to remain stable. With the promotion of adding more cost-effective products and significantly improved delivery speed, the growth rate of the e-commerce business in 2024 is expected to slightly accelerate. Fulfillment network was an important driver of cost optimization in 2023, and this trend is expected to continue in 2024, but the space will shrink.

(2) AWS Business

The cloud computing industry is expected to continue to rebound in 2024. Synergy Research data shows that the total spending of global enterprises on cloud computing in the fourth quarter of 2023 reached $74 billion, an increase of $5.6 billion compared to the previous quarter, setting a historic high growth rate. The overall cloud computing market size in 2023 increased by 19% from 2022.

Although the trend of enterprise IT cost optimization continued in the fourth quarter, the optimization speed continued to slow down, with an increase in new transactions driven by AI. Leading companies benefit from scale, distribution, and deep customer relationships, and AI revenue will appear earlier in leading companies, giving them an advantage over other companies. It is expected that Amazon will benefit from the overall cloud computing environment, and the growth rate may not return to the level of 2022, but it is expected to significantly rebound compared to this year.

(3) Advertising Business

The strategy of increasing prices and introducing advertising will help drive subscription and advertising revenue growth. Starting from early 2024, Amazon's streaming service Prime Video has introduced ads in the USA, UK, Germany, and Canada, which means users who want an ad-free experience will need to pay an additional $2.99. Amazon has also adjusted the price of its Prime service, increasing the price of Prime subscriptions (including the full Prime service with Prime Video) from $14.99 per month to $17.98 per month.

For the first quarter, Amazon expects net revenue to be between $138 billion and $-143.5 billion, while analysts expect $142.01 billion. Operating profit is expected to be between $8 billion and $-12 billion for the first quarter, with analysts expecting $9.12 billion.However, due to Amazon extending the server lifespan from 5 years to 6 years starting in January 2024, this will lead to a decrease in depreciation expenses on the books.It is expected to contribute an additional $0.9 billion to operating profit in the first quarter, representing approximately 7.5% to 11% of the guided operating profit. Excluding accounting adjustments, the mid-point of the profit guidance is in line with market expectations.

Based on the above assumptions, we expect revenue to reach $650.4/731.8/819.4 billion from 2024 to 2026, with year-on-year growth of 13.2%/12.5%/11.9%, and net income expected to be $41.4/52.5/69.5 billion.

2. Shareholder Returns

Amazon currently has no dividend or share buyback plans. With the release of profits from its e-commerce business, free cash flow continues to improve. Free cash flow in 2023 was $36.8 billion, compared to -$-11.5 billion in 2022. However, considering that there are still many capital expenditures in 2024, the possibility of a buyback plan in the short term is relatively low.

3. Valuation

As of February 2, 2024, Amazon's market cap is 1.78 trillion, equivalent to 48 times the operating profit in 2023, 58 times the net income; equivalent to 43 times the projected net income in 2024, and 25 times the projected net income in 2026.

We believe that Amazon's valuation has reached a reasonable range, and with no other conditions changing, there is limited upside potential.There are still doubts in the market about whether the strong purchasing power in 2024 can continue. Amazon AWS is expected to benefit from the recovery of the cloud computing industry, but compared to that, Microsoft and Google currently have a more obvious advantage in AI large models. If the valuation is to further increase, it needs to track the marginal changes in high-frequency macro consumption data and breakthroughs in AI.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

7

10