Futu Research | Starbucks Financial Report Review: North America's basic market is stable, international expansion is under pressure, and overall investment value is mediocre

Event Overview

On January 31st, Starbucks released its financial report for the first quarter of the 2024 fiscal year. Revenue was $9.425 billion, a year-on-year increase of approximately 8.2%; net income was $1.024 billion, a year-on-year increase of nearly 20%; global same-store sales increased by 5%, same-store transactions increased by 3%, and average ticket price increased by 2%. Starbucks has lowered its full-year revenue guidance for the 2024 fiscal year, expecting growth of 7% to 10%, lower than the previous forecast of 10% to 12%.

For Starbucks, the focus is on researching store opening conditions and same-store sales, as well as studying the competitive landscape by region.

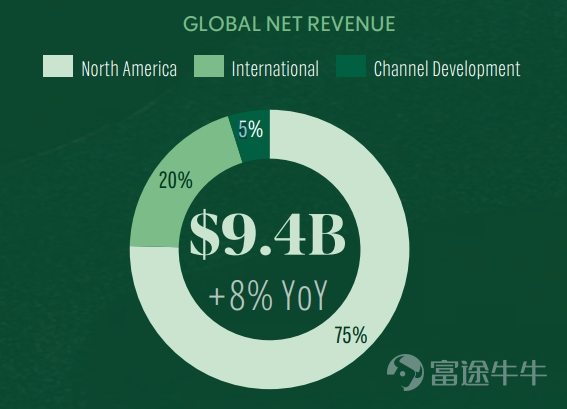

(1) From the perspective of business region segmentation, Starbucks' global business is divided into three major reporting segments: North America, International, and Channel Development. According to financial data, it can be seen that North America is still the company's basic market and main development engine. In terms of net income, North America accounts for 75%, international accounts for 20%, and channels account for 5%.

Figure: Starbucks Net Revenue Composition

Source of Information: Company Announcement, Compilation of Futu Securities

(2) In terms of store count, the United States and China are Starbucks' main revenue battlegrounds, with 16,466 stores in the United States and 6,975 stores in China, accounting for 61% of the company's global stores.

Chart: Store Quantity Information

Source of Information: Company Announcement, Compilation of Futu Securities

In short, the North American business is the key driver of Starbucks' net income, and the development of the Chinese market also has a significant impact on the company's performance growth and overall valuation. The next step will be to analyze these two markets.

1. North American Market: Despite some resistance due to the "Middle East issue", performance remains solid.

The North American market (including the United States and Canada) still accounts for 74.6% of revenue, higher than the 72.5% in the FY2022 annual report. Specifically, the North American market achieved revenue of $6.55 billion in Q1, a year-on-year growth of 14%, comparable store sales growth of 10%, with average ticket contribution of 9% and transaction volume contribution of 1%; operating profit margin improved to 21.4%, higher than expected.

Why are there these changes?

随着COVID-19疫情限制措施的逐渐放宽,消费者重新回到了实体店铺进行社交活动和休闲消费,星巴克作为线下体验型零售的一部分从中受益匪浅。同时,美国消费者信心指数的飙升表明了消费者的乐观情绪和购买力正在恢复。随着工资增长超过物价上涨,消费者的可支配收入增加,这直接刺激了消费支出,包括在咖啡店等非必需品上的开支。

四季度美国市场消费支出强劲带动星巴克销售额和利润增长。随着工资增长超过物价涨幅,密歇根大学上周表示,美国消费者信心指数自去年11月以来飙升29%,为1991年以来最大的两个月增幅,进一步显示出消费者情绪正在改善。

图:密大消费者信心指数

数据来源:Choice,富途证券整理

具体到星巴克,营业收入计算=客单价*客流量

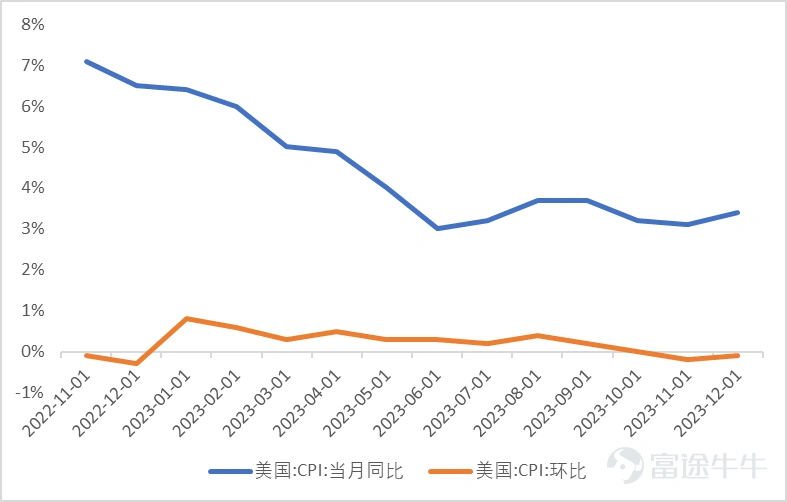

(1)客单价方面,提升幅度有所下降。

四季度美国通胀已有所降温,一定程度上减弱了星巴克通过提价转移成本压力的能力,通常来说消费者在物价趋稳时对价格上涨的接受度可能降低;

但鉴于星巴克仍然保有稳固的议价权,预计客单价提升水平回归相对平稳的增长态势,即保持低个位数增长,我们可以预期的是由于其成功执行了价格上调策略以应对成本上升,同时并未导致客流量大幅下滑,显示了品牌忠诚度和顾客对星巴克产品的接受度较高。

Figure: U.S. CPI trend.

Source: Wind, Futu Securities compilation.

(2) In terms of passenger flow, it has declined.

Due to the impact of the 'Middle East Affairs,' people have called for a boycott of Starbucks, resulting in a decrease in passenger flow, offsetting a portion of the growth. However, this event is unlikely to affect the company's long-term operation, and quarter two is expected to see a recovery in passenger flow.

Since 'Middle East Affairs' may refer to political disputes or conflicts related to the region, such as the Palestinian-Israeli conflict or regional wars, these events have caused local people to feel dissatisfied with Western companies. When a company is seen as a symbol of Western culture or policies, it may become a target of civil protests or boycotts. At the same time, the boycott behavior in the Middle East may have created market space for local coffee brands, allowing consumers to turn to locally recognized brands, which has affected Starbucks' performance in the local market.

Although in the short term, this boycott has had a negative impact on Starbucks, as a global brand, Starbucks' business strategy has a certain resilience and adaptability, enabling it to mitigate losses by adjusting market strategies, strengthening business development in other regions, and responding to public relations issues in a timely manner.

(3) In terms of profitability, the scale effect, more reasonable pricing strategy, and improvement in the company's operating capabilities have offset the negative impact of rising labor costs, and the operating profit margin has exceeded expectations, reaching 21.4%.

We expect that as the intensity of the event decreases, consumers' purchasing behavior may gradually return to normal, and Starbucks' passenger flow in the affected areas will recover in the second quarter. In the long run, Starbucks' global layout and brand strength will help it withstand the risks brought by fluctuations in a single market.

In the Chinese market, the growth of same-store sales in this quarter is weak, and there is still significant pressure on future operations under the current strategy.

The performance of the Chinese market in this quarter has shown a "volume increase" growth, but there is also pressure from the decline in average customer price caused by consumer downgrading. Same-store sales in China rose by 10%, same-store transaction volume rose by 21%, and average customer price dropped by 9%. This performance is not as good as the recovery of social retail and catering industry in the fourth quarter.

Figure: Chinese market data

Source of Information: Company Announcement, Compilation of Futu Securities

Benefiting from the low base in 2022 and the release of suppressed catering demand for a long time, the catering industry growth rate is relatively high in 2023. Based on the analysis of previous years' data by the Chinese Cuisine Association, the catering market recovered and warmed up from January to February 2023, and the income of catering continued to grow at a two-digit rate after March. The second quarter and the fourth quarter performed particularly well, with growth rates of catering income reaching 31.7% and 24.3% respectively. At the same time, according to data from the China Hotel Association, the total revenue of the catering industry in 2023 exceeded 5 trillion yuan for the first time, which meets the expectations of the association. Even compared with the total annual catering revenue of 4,672.1 billion yuan in 2019, the growth of catering revenue in 2023 still exceeds 13%, showing remarkable performance.

Figure: Catering revenue and total social retail sales (in 100 million RMB)

Source of information: Chinese Cuisine Association, Wind, Futu Securities collation

In the coffee field where Starbucks is located, there are many competitors, and the coffee market has fallen into a "price war" under the trend of pursuing cost-effectiveness. At the same time, as consumers have a deeper understanding of coffee and their consumption becomes more rational, it is difficult for brand tone to support high premiums. Chains and individual coffee shops positioned at the high-end in the Chinese market have all implemented varying degrees of price reductions. At the same time, coffee as a fast-moving consumer good is difficult to have brand premiums. Therefore, the high pricing of Starbucks in the Chinese market has a high level of uncertainty in terms of how long it can be sustained. This quarter's unexpected decline of 9% in average customer price may verify this logic.

Figure: Starbucks China and its Competitors

Source of Information: Company Announcement, Compilation of Futu Securities

According to the recent conference call, Starbucks China management adheres to its core business philosophy and has no intention of engaging in price competition strategy.

At the same time, actively promoting the market 'encryption' strategy, aiming to further improve store penetration rates in existing cities, and expanding to new county-level markets through the 'city expansion' plan. However, there are challenges in the current coffee industry landscape: on the supply side, the trend of franchise store opening may lead to temporary risk of excess capacity; on the demand side, consumer behavior tends to be conservative and cautious. This puts Starbucks in a delicate situation in the Chinese market, especially in the process of expanding into lower-tier cities and sinking markets, where pricing of its products may not match the consumption capacity of local residents, thereby increasing the difficulty of market development.

In summary, in the future Chinese market, Starbucks needs to maintain its brand advantage in the global market, as well as flexibly adapt to and deeply understand the changing demands of the Chinese market. By constantly adjusting and optimizing its business model, it can sustain continuous growth in the intense competitive environment.

However, we expect that the decline in same-store sales in the China region during this financial reporting season may just be the beginning, and if appropriate and timely strategic adjustments are not made, the future performance of Starbucks in the China region is likely to be not very optimistic.

III. Shareholder Returns Have Improved Compared to the Previous Quarter, Beware of Valuation Correction Risk

(1) This quarter, the company's net income was $1.024 billion, and its free cash flow was $1.788 billion. The company will return all net income and free cash flow to shareholders, distributing cash dividends of $0.648 billion and repurchasing stocks totaling $1.26 billion, for a total return of $1.91 billion to shareholders. Assuming the continuation of shareholder buybacks in the Q1 fiscal quarter of 2024, based on the current market cap, there is approximately a 7% return rate for shareholders; with the growth of the company's EPS, and under the condition of maintaining stable valuation, there can be approximately a 15%-20% investment return rate.

(2) Inferring the future, investment return = EPS * valuation + shareholder return.

According to the financial report:

1) EPS growth

Currently, Starbucks has 28,587 stores and plans to reach 50,000 stores by 2030. The compound annual growth rate from the current year to 2030 is expected to be 3.8%. However, if the China region experiences a significant decline in revenue due to intense competition (accounting for 12% of revenue), this will have a significant impact on Starbucks' overall performance. However, with the current pace of store openings, it is expected that the overall decline in the China region will result in almost no growth for nearly 3 years, which will have a significant impact on EPS.

Assumption 1: If the China region can stabilize its base, assuming that store growth and same-store sales growth are relatively consistent (2% inflation), the combined effect of future store openings and same-store sales growth will result in EPS exceeding (1+3.8%)*(1+2%)-1=5.87%.

Assumption 2: If the China region experiences a more serious decline, it is expected that Starbucks will be unable to achieve growth for three consecutive years.

2) Valuation and shareholder return

Currently, Starbucks has a PE ratio of 25x and a market cap of $105.3 billion, with annual free cash flow of nearly $3.5-4 billion, which is roughly 25-29 times the market cap. At the same time, partial debt repayment will be made.

In general, if Starbucks does not make progress in other international markets, once the business in the Chinese market declines under fierce competition, the investment value will be greatly discounted in the next few years. For the current Starbucks, the investment value is relatively ordinary, and investors need to closely monitor the progress of other international businesses.

Risk Warning

The consumer recovery is not as expected, and industry competition is intensifying, with significant risks of rising raw material and labor costs.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (2)

to post a comment

28

19