毛利率降至17.6%,特斯拉Q4業績引擔憂?

Futu Research | Tesla Earnings Review: Growth is weak, valuation pressure is high

After the US stock market on January 24 EST$Tesla (TSLA.US)$The fourth quarter report of 2023 was released, and both revenue and profit fell short of expectations. 23Q4 achieved revenue of US$25.17 billion (same below), lower than Bloomberg's agreed estimate of US$25.87 billion; Non-GAAP EPS was $0.71, lower than the forecast of $0.73. (The sharp increase in GAAP net profit this quarter was largely due to the inclusion of approximately $5.9 billion in one-time non-cash tax revenue).

Tesla's other businesses, such as FSD, DOJO, and robotics, are very imaginative in the medium to long term, and have contributed a lot of valuation to Tesla, but electric vehicle sales are still the core basic market.Judging from this quarter's earnings report, Tesla will continue to face growth pressure in 2024.

1. Bicycle revenue declined, and revenue fell short of expectations

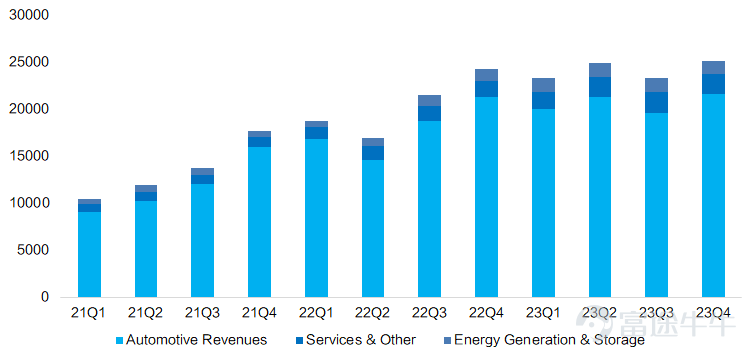

In 23Q4, Tesla's automotive business achieved revenue of US$21.56 billion, an increase of 1% over the previous year. Among them, car sales alone were 20.63 billion US dollars, carbon credit sales revenue was 430 million US dollars, and car rental revenue was 500 million US dollars. Since sales are already a clear brand, this quarter's revenue that fell short of expectations was mainly due to bicycle revenue.

Figure: Tesla's quarterly revenue (million dollars)

Source: Bloomberg, compiled by Futu Securities

What is behind the high sales volume in the fourth quarter is “price for volume.”In the fourth quarter, Tesla delivered more than 484,000 vehicles, up 11% from the previous month, and the overall delivery volume in 2023 increased 38% year on year to 1.81 million vehicles, achieving the previously set target. This already includes the impact of early car purchases due to changes in subsidy policies.

Figure: Tesla's quarterly sales volume (units)

Source: Bloomberg, compiled by Futu Securities

However, from the perspective of bicycle revenue ASP, Tesla's bicycle revenue (excluding carbon credits and leasing) fell to 42,600 US dollars month-on-month in the fourth quarter, down about 1,000 US dollars from the previous quarter. The decline in bicycle revenue is related to the price reduction strategy in the US in the fourth quarter. The price reduction of Model 3 and Model Y in the US in the fourth quarter was at least 3% (considering discount activities and insurance benefits, etc., the actual price reduction may be even larger), while the price increase in China was small.

2. Under the influence of the price war, gross margin is still under pressure

The overall gross margin at the 23Q4 company level fell from 17.9% in the previous quarter to 17.6%. It has been declining for 7 consecutive quarters, lower than Bloomberg's agreed estimate of 18.1%;

Figure: The company's overall gross profit margin (excluding carbon credits and car leasing)

Source: Bloomberg, compiled by Futu Securities

Under conditions where bicycle revenue ASP continues to decline, if we want to maintain a stable or increase in gross margin, we need to rely on a larger reduction on the cost side. The main factors affecting gross margin this quarter were:

1) Price cuts for major models in the US — negative

2) In terms of upstream raw material costs, lithium carbonate prices showed an overall downward trend in the fourth quarter — positive

3) Bicycle depreciation costs increased in the third quarter due to factory shutdowns, and normal production resumed in the fourth quarter — positive

4) Productivity increase at Berlin and Texas plants — positive

5) Cybertrunk's commissioning led to cost expansion — negative

The market originally expected that, driven by the above many positive factors, gross margin could be effectively increased this quarter. However, judging from the actual situation, although the gross margin of the automobile business improved slightly, the increase was very limited, and the gross profit of the automobile business is still under pressure.

Figure: Gross profit margin of the automobile business (excluding carbon credits and car leasing)

Source: Bloomberg, compiled by Futu Securities

However, the two major energy and service businesses other than the automobile business also experienced a month-on-month decline in gross margin. Tesla's service division business mainly includes non-warranty after-sales service, paid charging services, used car sales, etc. As supply increases and prices fall, the value of Tesla's used cars depreciated faster than competitors' cars. The gross margin of the service business fell from 6% to 3%, and the energy business also fell from 28% to 22% due to factors such as the seasonal slowdown in energy storage installations, which further reduced gross margin at the company level.

Figure: Tesla used car price trends

Source: CarGurus, compiled by Futu Securities

Overall cash flow from operating activities fell 10% year on year in 2023, while capital expenditure increased by 24% year on year, leading to a 42% year-on-year decline in free activity cash flow to US$4.4 billion for the year.As a result, although Tesla's stock price rose significantly in 2023, it was more of an increase in valuation. It certainly includes many businesses such as FSD, DOJO, and robotics other than the automobile business, and the fundamentals of the automobile business are deteriorating.

3. 2024 will be a challenging year, but there is no shortage of short-term catalysts to be realized

From the perspective of the automotive business alone, 2024 will undoubtedly be a challenging year, facing the following uncertainties. For a detailed analysis of the following factors, see “Futu Research | Tesla 23Q4 Earnings Forecast: Gross Margin Expected to Remain Under Pressure”.

1) As the Federal Reserve cuts interest rates, it helps reduce consumer buying pressure and loan costs — positive

2) Raw material prices are expected to remain low, and productivity will continue to rise — positive

3) The US subsidy of 7,500 US dollars was abolished because the Model 3 used batteries produced in China; the German tram subsidy in Europe ended early; the Model 3 subsidy in France was abolished — negative

4) Tesla launched a new round of price cuts in Europe and China at the beginning of the year — negative

5) Auto workers' salary increases, rising labor costs affect profit margins — negative

6) The Shanghai factory has limited room for marginal incremental growth. The increase in production capacity mainly depends on the Berlin and Texas plants. 24 years is not a period of rapid increase in production capacity — negative

7) Capital expenditure is expected to exceed $10 billion in 2024, up from $8.9 billion in 2023 — negative

8) The competitive landscape is becoming fiercer — negative

Next-generation production platforms and Cybertruck are expected to lead Tesla into a new stage of growth, but these businesses will all wait for 2025 to be realized one after another, and 2024 will be a painful period of “no return” for Tesla.

1) Cybertruck: This year's production is almost sold out, and Tesla did not disclose the exact sales volume. The 4680 battery no longer limits Cybertruck production, but considering manufacturing complexity, the model's production capacity is expected to climb for a longer period than other models, and it is estimated that 250,000 units may only be delivered in 2025.

2) Next-generation production platform: Production is expected to begin in Texas in the second half of 2025. After the new platform is put into operation, the production cost of vehicles will be drastically reduced, so that Tesla is no longer in trouble with gross margin. It is also possible that Tesla models under 200,000 will come out.

Based on the above adverse factors, and without any other significant changes, we speculate that Tesla will likely experience a slowdown in revenue growth and pressure on profits in 2024.We use the “return on investment = EPS growth* valuation+shareholder return” method to calculate Tesla's return on investment:

1) Weak EPS growth: The year-on-year increase in 2023Q4 delivery volume has declined to 20%. Against the backdrop of many negative environments in 24, we are optimistic that sales growth will slow down, with a 20% year-on-year increase of 2.17 million units, an increase of 360,000 units; prices are expected to continue to drop 2% in the face of intense competition and withdrawal of subsidy policies. The gross margin is expected to continue to decline but the decline will decrease; the growth rate of the energy business has declined rapidly in '23, and the carbon credit business will slow down as traditional car companies switch to new energy vehicles one after another;

Based on this assumption, overall revenue in 2024 is estimated to be US$112.8 billion, up 16% year on year; of this, automobile sales revenue is US$94.4 billion, up 14% year on year; Non GAAP net profit is expected to be US$11 billion in 2024, up 1.6% year on year.

2) Shareholder returns:Tesla currently has no dividends or buyback plans

3) Valuation is likely to be compressed:As of January 24, 2024, Tesla's current market value is 660.6 billion US dollars, corresponding to 60 times the 2024 net profit. 24 years of growth make it difficult to absorb the current high valuation. However, it was difficult for story businesses to contribute substantial profits in '24, and valuations are expected to fall somewhat as growth stalls. However, there will be no shortage of event catalysts during the period, such as the delivery of the humanoid robot “Optimus” and the launch of the latest FSD version V12, which can be watched.

In view of the above factors, we suggest that investors should avoid Tesla's valuation risks more now and wait until the new business significantly boosts revenue and profit, or that the tram business grows more significantly before investing.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (10)

to post a comment

23

32